Description

Steering Successful Growth:

Steering growth:

Value Capture in M&A

Value creation and M&A

Results of a 2015 Crowe Horwath LLP Survey

Audit | Tax | Advisory | Risk | Performance

. Introduction

Contents

Introduction

3

Executive Summary

4

Capturing Value Across the M&A Transaction Value Chain

6

Maximizing Value Capture

9

For Good Reasons

11

Harnessing the Value of Cross-Border Transactions

21

Overcoming Cross-Border Pitfalls

25

The Seven Pillars of M&A Success

26

Conclusion

29

Methodology

The past year has seen a huge resurgence in deal-making activity around

the globe. Fueled by a combination of cheap debt, increased boardroom

confidence, and the return of growth after the financial crisis of 2008, mergers

and acquisitions (M&A) in the United States reached highs not seen for almost

a decade. After a period of self-reflection and consolidation, companies are

looking to inorganic growth again, and their executives are hoping their M&A

efforts will spur innovation, capture synergies, and make up for lost time.

With this growth in deal activity, however, comes increased pressure to ensure that

the deals completed generate the maximum value as competition and pricing are

running high. But what separates the deals that capture value from the deals that do

not? With this question in mind, Crowe Horwath LLP teamed with Mergermarket, a

provider of M&A intelligence, to interview 100 U.S.

corporate executives about some of their most recent deals – looking in particular at what the acquiring companies set out to achieve, the processes they used, and whether they deemed the deals successful or unsuccessful in terms of capturing value. In this report, we use the collected data to identify some of the important differences between good and bad deals, and we provide some comments from the interviewed executives. 30 Deal-making levels will remain at record highs as long as companies are hungry for growth and have access to cheap cash. While these factors put pressure on management teams to do a deal, no business wants to turn a potentially big opportunity into a costly mistake.

Making a merger or acquisition successful is one of the toughest tasks in business today; in such a competitive environment, it is also one of the most crucial. While nobody can guarantee a successful deal, we hope that this report will provide insight into the paths taken by successful acquirers. We trust that you find this report helpful, and we welcome your feedback. Marc Shaffer Partner, Crowe Horwath LLP +1 312 857 7512 marc.shaffer@crowehorwath.com 2 Chris Nemeth Director, Crowe Horwath LLP +1 312 899 8405 chris.nemeth@crowehorwath.com 3 . Steering Successful Growth: Value Capture in M&A Executive Summary After a record 2014, deal-making continues to thrive this year. According to Mergermarket data, $719 billion worth of deals were made in the first quarter of 2015 – up 13.4 percent from the same period the previous year. This is the highest first-quarter value figure since 2007. Cross-border activity is also thriving, with a 12.2 percent year-on-year increase in M&A value. seeks to answer that question – in particular, how the characteristics of successful deals differ from those of less successful deals and why a specific deal either builds or loses value at particular points on the M&A transaction value chain as the deal moves toward completion. Following are some of the key findings of this survey. The growing appetite to spend, however, comes at a time when companies face major challenges. Macroeconomic factors – such as slow economic growth in Europe, a slowdown of emerging markets’ economies, and falling oil prices – have spurred consolidation in some sectors, making the realization of expected synergies more important than ever. In addition, the rise in the number of activist investors has increased the pressure on boards to maximize shareholder value through buybacks, dividends, and M&A.

Corporate executives who don’t respond adequately to this pressure could be grilled at annual shareholder meetings and even asked to resign. Also, increased business activity among countries brings with it an increase in the challenges often associated with cross-border transactions, such as regulatory issues and cultural differences. With so many factors in play, how can companies have a better chance of consistently creating value from their mergers and acquisitions? This report 4 Everyone can improve. The survey shows that even the most experienced deal-makers, by their own admission, are leaving substantial value on the table. There appears to be room for improvement at all stages of the M&A transaction value chain – from M&A strategy clarification, deal targeting, due diligence rigor, and integration execution. Strategic clarity and insight set the table for success.

The more successful deal-makers performed more value-clarification processes than the unsuccessful companies did. More time spent upfront on clarifying and understanding exactly how best to extract the value from a merger or acquisition is a hallmark of better deals. Synergies are not created equal. “Strategic” deals focused primarily on commercial synergies – including market and channel expansion, new product offerings, and cross-selling – proved to be substantially more challenging and problematic than deals focused on goals such as consolidation, removing production capacity from the market, and economies of scale. Contemporary due diligence transcends the financials. Expanded due diligence – incorporating areas like IT, operations, human resources, and culture – was reported to be in almost nine out of 10 of the successful deals cited by the respondents. Conversely, it occurred in just 59 percent of the unsuccessful deals. Integration is crucial – and a particular area of opportunity. Surprisingly, many of the otherwise experienced deal-makers responding to the survey indicated that they had inadvertently neglected or underestimated the integration aspect of the M&A transaction value chain and lost value as a result.

This finding holds for both pre-close integration planning and post-close integration execution. By almost every integration execution dimension surveyed, the more successful deal-makers seemed to invest more in the integration activity. For instance, half of successful deal-makers used an integration scorecard, compared to only 37 percent of unsuccessful ones. The percentages were similar when successful and unsuccessful respondents (54 percent and 35 percent, respectively) were asked whether they consulted external expertise for executing the integration.

In general, while most deal-makers seem to understand that integration is utterly critical to capturing value, integration is not consistently receiving the early attention and adequate resources necessary for the delivery of its full value. Good advice augments the internal team’s capability and drives results. Virtually across the board, using qualified external advisers enhanced the value of the deals. Eighty-eight percent of the respondents whose companies executed successful deals and used an external consultant during the due diligence process said that having the adviser onboard generated significant value. By contrast, those in the unsuccessful deal category unanimously said that their companies should have used advisers during due diligence, integration planning, negotiation, and/or process management. Deals abroad are even tougher. Perhaps not surprisingly, the survey indicates that cross-border transactions present far more challenges and risks than domestic deals do.

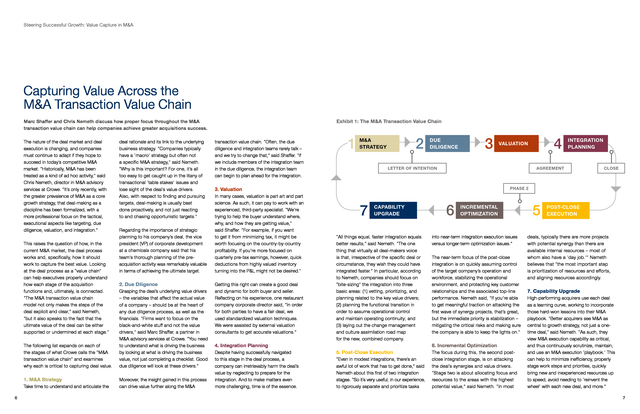

These issues are further compounded by companies’ inability or unwillingness to deploy qualified internal resources for these transactions and tendencies not to supplement their teams with local knowledge. 5 . Steering Successful Growth: Value Capture in M&A Capturing Value Across the M&A Transaction Value Chain Exhibit 1: The M&A Transaction Value Chain Marc Shaffer and Chris Nemeth discuss how proper focus throughout the M&A transaction value chain can help companies achieve greater acquisitions success. The nature of the deal market and deal execution is changing, and companies must continue to adapt if they hope to succeed in today’s competitive M&A market. “Historically, M&A has been treated as a kind of ad hoc activity,” said Chris Nemeth, director in M&A advisory services at Crowe. “It’s only recently, with the greater prevalence of M&A as a core growth strategy, that deal-making as a discipline has been formalized, with a more professional focus on the tactical, executional aspects like targeting, due diligence, valuation, and integration.” This raises the question of how, in the current M&A market, the deal process works and, specifically, how it should work to capture the best value. Looking at the deal process as a “value chain” can help executives properly understand how each stage of the acquisition functions and, ultimately, is connected. “The M&A transaction value chain model not only makes the steps of the deal explicit and clear,” said Nemeth, “but it also speaks to the fact that the ultimate value of the deal can be either supported or undermined at each stage.” The following list expands on each of the stages of what Crowe calls the “M&A transaction value chain” and examines why each is critical to capturing deal value. 1.

M&A Strategy Take time to understand and articulate the 6 deal rationale and its link to the underlying business strategy. “Companies typically have a ‘macro’ strategy but often not a specific M&A strategy,” said Nemeth. “Why is this important? For one, it’s all too easy to get caught up in the litany of transactional ‘table stakes’ issues and lose sight of the deal’s value drivers. Also, with respect to finding and pursuing targets, deal-making is usually best done proactively, and not just reacting to and chasing opportunistic targets.” Regarding the importance of strategic planning to his company’s deal, the vice president (VP) of corporate development at a chemicals company said that his team’s thorough planning of the preacquisition activity was remarkably valuable in terms of achieving the ultimate target. 2. Due Diligence Grasping the deal’s underlying value drivers – the variables that affect the actual value of a company – should be at the heart of any due diligence process, as well as the financials.

“Firms want to focus on the black-and-white stuff and not the value drivers,” said Marc Shaffer, a partner in M&A advisory services at Crowe. “You need to understand what is driving the business by looking at what is driving the business value, not just completing a checklist. Good due diligence will look at these drivers.” Moreover, the insight gained in this process can drive value further along the M&A transaction value chain.

“Often, the due diligence and integration teams rarely talk – and we try to change that,” said Shaffer. “If we include members of the integration team in the due diligence, the integration team can begin to plan ahead for the integration. 1 2 M&A STRATEGY DUE DILIGENCE 3 Getting this right can create a good deal and dynamic for both buyer and seller. Reflecting on his experience, one restaurant company corporate director said, “In order for both parties to have a fair deal, we used standardized valuation techniques. We were assisted by external valuation consultants to get accurate valuations.” CLOSE PHASE 2 7 CAPABILITY UPGRADE “All things equal, faster integration equals better results,” said Nemeth. “The one thing that virtually all deal-makers voice is that, irrespective of the specific deal or circumstance, they wish they could have integrated faster.” In particular, according to Nemeth, companies should focus on “bite-sizing” the integration into three basic areas: (1) vetting, prioritizing, and planning related to the key value drivers; (2) planning the functional transition in order to assume operational control and maintain operating continuity; and (3) laying out the change management and culture assimilation road map for the new, combined company. 4.

Integration Planning Despite having successfully navigated to this stage in the deal process, a company can irretrievably harm the deal’s value by neglecting to prepare for the integration. And to make matters even more challenging, time is of the essence. INTEGRATION PLANNING AGREEMENT LETTER OF INTENTION 3. Valuation In many cases, valuation is part art and part science.

As such, it can pay to work with an experienced, third-party specialist. “We’re trying to help the buyer understand where, why, and how they are getting value,” said Shaffer. “For example, if you want to get it from minimizing tax, it might be worth focusing on the country-by-country profitability.

If you’re more focused on quarterly pre-tax earnings, however, quick deductions from highly valued inventory turning into the P&L might not be desired.” 4 VALUATION 6 INCREMENTAL OPTIMIZATION into near-term integration execution issues versus longer-term optimization issues.” The near-term focus of the post-close integration is on quickly assuming control of the target company’s operation and workforce, stabilizing the operational environment, and protecting key customer relationships and the associated top-line performance. Nemeth said, “If you’re able to get meaningful traction on attacking the first wave of synergy projects, that’s great, but the immediate priority is stabilization – mitigating the critical risks and making sure the company is able to keep the lights on.” 6. Incremental Optimization 5.

Post-Close Execution “Even in modest integrations, there’s an awful lot of work that has to get done,” said Nemeth about this first of two integration stages. “So it’s very useful, in our experience, to rigorously separate and prioritize tasks The focus during this, the second postclose integration stage, is on attacking the deal’s synergies and value drivers. “Stage two is about allocating focus and resources to the areas with the highest potential value,” said Nemeth. “In most 5 POST-CLOSE EXECUTION deals, typically there are more projects with potential synergy than there are available internal resources – most of whom also have a ‘day job.’” Nemeth believes that “the most important step is prioritization of resources and efforts, and aligning resources accordingly. 7.

Capability Upgrade High-performing acquirers use each deal as a learning curve, working to incorporate those hard-won lessons into their M&A playbook. “Better acquirers see M&A as central to growth strategy, not just a onetime deal,” said Nemeth. “As such, they view M&A execution capability as critical, and thus continuously scrutinize, maintain, and use an M&A execution ‘playbook.’ This can help to minimize inefficiency, properly stage work steps and priorities, quickly bring new and inexperienced resources up to speed, avoid needing to ‘reinvent the wheel’ with each new deal, and more.” 7 .

Maximizing Value Capture The value chain presents tremendous opportunities and pitfalls for companies engaged in M&A. In this section, we outline what is separating good deals from unsuccessful ones. Spotlight on M&A Strategy One salient finding from the survey is that acquisitions focused on commercial synergies appear to be more difficult to undertake and complete successfully than those targeting operational synergies. In every case, the survey elements that are tied to commercial synergies – for example, incremental product or service offerings, the impact on gross margin, and access to new geographies, markets, or channels – had higher rates of failure than success. Exhibit 2: The Drivers of Value Creation UNSUCCESSFUL DEALS SUCCESSFUL DEALS Incremental product/service offerings 80% 74% Operational synergies/cost reduction/economies of scale 67% 63% Increased top line, market share 61% 67% Access to new human capital, skills, and capability 59% 61% Access to new geographies, markets, or channels 57% Conversely, the deals that were focused on operational synergies or cost-based elements – including the rationalization of combined product offerings and working capital requirements – had higher rates of success (Exhibit 2). See sidebar “For Good Reasons,” page 11. 52% Rationalization of combined product offerings 39% 46% Working capital requirements 26% 41% Impact on gross margin 28% 22% Elimination of a competitor 20% 13% “Our key decision-makers enforced good procedures to be followed during the whole deal cycle.

Their thorough planning with regard to the pre-post acquisition activity was remarkable in terms of achieving the target – in fact it turned out to be a value add to our whole deal. Capital allocations were more effective and we were able to focus on areas that needed more attention and improvements.” VP of Corporate Development, chemicals company 8 9 . Steering Successful Growth: Value Capture in M&A For Good Reasons Exhibit 3: Strategies Executed During a Transaction UNSUCCESSFUL DEALS Executing the Strategy SUCCESSFUL DEALS Expanded due diligence period focused beyond ï¬nancial to forward-looking operational/integration issues 59% 91% Prioritization of resources and effort around highest value-capture initiatives 67% 91% While the use of synergy capture plans is common for both the successful and the unsuccessful deals of the survey respondents, there was a marked difference in the successful acquirers’ ability to “walk the talk” and put some teeth into those plans. The successful deal-makers deployed a greater portfolio of execution strategies – including an expanded due diligence period, the careful prioritization of resources, increased internal accountability for deal results, an M&A playbook and toolkit, and the use of an integration scorecard – than did the unsuccessful deal-makers (Exhibit 3). Utilization of synergy capture plan for each signiï¬cant synergy 85% 76% Increased internal accountability for deal results 54% 63% Utilization of M&A playbook and toolkit 39% 54% Utilization of integration scorecard 37% 50% Use of incremental external resources 41% 41% Use of succinct deal summary to clarify deal thesis and key value drivers 37% 37% 91% 67% Prioritization of resources and effort around highest value-capture initiatives Utilization of synergy capture plan for each signiï¬cant synergy UNSUCCESSFUL DEALS Prioritization of resources and effort around highest value-capture initiatives 0% 85% 10 While having a solid strategy in place is paramount, it is all for nothing unless a deal is executed properly. As one retail executive pointed out, “The execution was the most crucial stage in shaping the success of the deal.” TO 100% 91% Expanded due diligence period focused beyond ï¬nancial to forward-looking operational/ integration issues R AT E G IES P ST 100% SUCCESSFUL DEALS Chris Nemeth and Marc Shaffer explore the challenges of commercial synergy value capture. M&A is clearly an attractive and accepted method for gaining access to new markets, channels, product and service offerings, customer segments, and the like. However, the survey respondents indicated that deals focusing on these commercial synergies are significantly more challenging than those targeting operational, cost-focused synergies. Perhaps one way to understand this is that, in a cost-synergy deal, many of the important variables are internal to the acquiring company and thus in the buyer’s control.

In essence, executives are asking their own people to do things differently in order for the company to realize the efficiency benefits. For commercial synergies, however, the buyer is faced with myriad external factors in addition to the internal factors. Not only are the internal stakeholders asked to do things differently, but the external stakeholders, such as customers and suppliers, are being asked to do things differently as well. The acquiring company asks its customers to buy new things, buy more things, accept different pricing, and/or interact with the newly combined company in new and different ways. It’s easy for an acquirer to underestimate the disruption and challenges these changes create for customers, suppliers, and others, so the acquiring company’s executives can be blindsided by subsequently flagging results.

In addition, in cases where the deal is taking a competitor out of the market, customers often feel the need to offset their increased supply risk by further diversifying their sources of supply and as a result buy less from the newly combined company. Even beyond these factors, there are additional myriad external market forces, such as the response of competitors, foreign exchange rates, the customers’ business cycle, general supply and demand issues, and more. Failure to think holistically and realistically about the assumptions made about commercial synergies can easily result in company performance that trails expectations. Following are some tenets that executives pursuing M&A for the commercial synergies should bear in mind to increase the chances of success. „„ Consider commercial diligence. Don’t fixate on the balance sheet or trailing financials. If the commercial side of the business is what drove you to acquire it, then also look to focus on and examine the commercial aspects, including both the risks and potential benefits. priorities but also work to heighten key customers’ confidence and build “relationship equity” in the combined company right out of the gate. „„ Risk equals reward.

Consider the retention of existing key customers to be equally as important as incremental synergy capture. As any executive who’s lived through customer fallout from a troubled deal process will attest, “re-earning” the trust and business of a damaged customer relationship is often even more difficult and costly than capturing new customer synergies. „„ Don’t overpromise. With so many external factors to consider, it is better to be conservative about external analysts’ forecasts of sales synergies. The age-old wisdom of “underpromise and overdeliver” is a prudent operating principle when it comes to forecasting and communicating commercial synergy capture. „„ Listen to your customers at closing. Meaningfully involving key customers in the integration planning process can not only help guide the integration 11 .

Spotlight on Due Diligence Due diligence was treated as a more holistic activity – both in terms of its breadth and its depth – in the successful deals more so than in the unsuccessful deals. The due diligence period of successful deal-makers was likely to be more prolonged and have a greater scope. The due diligence process of 91 percent of the successful deal-makers was expanded, focusing beyond the financial aspects of the deal, while just 59 percent of those who had unsuccessful deals used an expanded scope of diligence (Exhibit 3). It is important for corporate executives to have the right goals in mind with due diligence. “Due diligence was conducted with the intention of maximizing deal value,” said one finance director at a chemicals firm.

“Our specialists helped in the timely execution and monitoring of the activity. The deal enabled our business to transform and helped us explore key geographies.” A Wider Scope Successfully executed deals reported by the survey respondents encompassed a much broader range of due diligence tasks than the unsuccessful deals. In successful deals, there was a greater emphasis on detailed pre-acquisition analysis of profit contribution by product and customer (91 percent, compared with 70 percent for unsuccessful deals), development of combined working capital requirements (81 percent, compared with 61 percent), and 12 verification of cost savings assumptions (76 percent, compared with 61 percent). Almost all the respondents’ companies, whether their deals proved to be successful or not, established objective financial and operational metrics preand post-acquisition (Exhibit 4). For successful deal-makers, these components of thorough due diligence were vital.

“Information was gathered well in advance, so we were able to spend ample time in transforming them into actionable insights,” said the finance director at a beverage group. “Gaining a 360-degree perspective of the deal was one of the most important factors in conducting our due diligence processes.” 81% of successful deal-makers considered the development of working capital requirements in the due diligence process, compared with 61% of unsucessful ones. Exhibit 4: Facets of the Due Diligence Process UNSUCCESSFUL DEALS SUCCESSFUL DEALS Establishment of objective ï¬nancial and operational metrics pre- and post-acquisition 98% 96% Detailed pre-acquisition analysis of proï¬t contribution by product and customer 70% 91% Development of combined working capital requirements 61% 81% Veriï¬cation of input cost savings assumptions 61% 76% 13 . Steering Successful Growth: Value Capture in M&A 91% of successful deal-makers did detailed pre-acquisition analysis of profit contribution by product and customer as part of the due diligence process. Moreover, performing due diligence on a wider range of aspects can help maintain a deal’s value as it progresses along the value chain. “The most important aspect of due diligence for us was the development of combined working capital requirements and cost savings to increase the long-term value,” said a construction firm CFO. The due diligence process for unsuccessful deals relied heavily on establishing pre- and post-acquisition financial and operational metrics (98 percent). Longer-term factors, such as the development of combined working capital requirements (61 percent), were ignored much more often than they were in the successful deals’ processes. One automotive executive who had been involved in an unsuccessful acquisition acknowledged that “activities that led to the development of combined working capital requirements were skipped, as the acquired business had a reputation and global presence. Workforces were to be combined and [we thought] this would help us in becoming more robust and active toward market changes, risks, and opportunities.” This near-sighted focus with respect to due diligence can be costly to firms in the long run. Another automotive executive said shortsightedness might have destroyed value during the due diligence process for his company’s deal, which was ultimately unsuccessful.

“We did not enhance our approach to conducting due diligence, 14 and there were no focused efforts at analyzing the profit contribution or predicting the sales volume,” he said. “Also, we did not look critically at working capital requirements or focus on identifying cost-saving opportunities.” The Value of Due Diligence The majority of the respondents involved in successful deals who used specific due diligence methods said that those methods added significant value to their deals. In particular, establishing objective financial and operational metrics pre- and post-acquisition (88 percent) and detailed pre-acquisition analysis of profit contribution by product and customer (82 percent) were highly regarded by the respondents. More than half of the respondents who did not establish objective financial and operational metrics pre- and post-acquisition, as well as conduct detailed pre-acquisition analysis of profit contribution by product and customer, acknowledged in hindsight that they should have done so (Exhibit 5). Lessons Learned Those engaged in unsuccessful deals, not surprisingly, realized less value from the due diligence process than the successful deal-makers did. Nonetheless, respondents seem to realize in hindsight the importance of performing due diligence on a broader range of aspects. Nearly three-quarters of the respondents with unsuccessful deals who did not develop combined Exhibit 5: How Facets of Due Diligence Added Value to Successful Deals 88% 12% 0% 82% 18% 0% Significant value 0% 100% 100% Detailed pre-acquisition analysis of profit contribution by product and customer Establishment of objective financial and operational metrics pre- and post-acquisition 32% Some value 68% 73% 27% 100% 0% Development of combined working capital requirements 100% Verification of input cost savings assumptions Exhibit 6: Facets of Due Diligence That With Hindsight Unsuccessful Deal-Makers Would Have Done 50% 50% 87% No Yes 13% 0% 100% Establishment of objective ï¬nancial and operational metrics pre- and post-acquisition 74% 26% 0% 100% Development of combined working capital requirements 0% 100% Detailed pre-acquisition analysis of proï¬t contribution by product and customer 63% 37% 0% 100% Veriï¬cation of input cost savings assumptions 15 .

working capital requirements said that with hindsight they would have done so, while 87 percent of those who did not conduct a pre-acquisition analysis of customer and product profit contribution said they should have (Exhibit 6). One construction sector CFO was particularly rueful about not conducting profit contribution analyses. “I think it was necessary to do this, as our failure to identify and analyze profit contributions led to disruptions, as well as inaccurate strategies that affected our finance management post-acquisition,” he said. 88% of unsuccessful deal-makers would use consultants for integration planning in hindsight. Some of the respondents regretted neglecting metrics beyond the typical financial and operational data in the due diligence process. “Due diligence was not a combined effort, and we lacked in due diligence big time,” said a VP of finance at a retail company. “We only gathered information on financial and operational metrics and did not give importance to other metrics.

But I do feel that we should have done due diligence on other metrics, too.” Spotlight on Integration The integration steps of the M&A transaction value chain (steps 4, 5, and 6) are obviously critical to actually realizing and reaping the value of the transaction. The integration period leverages and builds on all of the work, insight, and decisions of the prior steps. Yet failure at the integration stage, sadly, can render all of the prior work and investment for naught and can quickly decimate the value of the deal. 16 17 . Steering Successful Growth: Value Capture in M&A Successful deal-makers understand that good integration is not a “theoretical exercise” and requires more than simply committing a plan to paper. Whereas companies with both successful and unsuccessful deals used consulting help for strategy development, the more successful acquirers were far more likely to use qualified external resources to help with the integration process, particularly with integration execution (54 percent of the successful deal-makers and just 35 percent of the unsuccessful deal-makers) (Exhibit 7). Eighty percent of the respondents whose deals were successful said that consultants added significant value during integration planning, and 50 percent said that consultants added significant value during the integration execution (Exhibit 8). A VP of M&A at a mining company whose deal turned out successfully said, “Their experience helped us in making better decisions on the deal.” Exhibit 7: Areas of External Consultant Use Perhaps more significantly, the unsuccessful deal-makers said almost unanimously that in hindsight it’s clear that their companies should have used external consultants.

Eighty-eight percent of the respondents who did not use consultants in integration planning and due diligence said that they would do so if they could do the deal again. Moreover, 67 percent said that they should have used consultants during the execution of integration (Exhibit 9). to navigate. More than two-thirds of respondents from unsuccessful deals felt strongly that using outside advisers during the integration stage would have prevented some problems (Exhibit 9). “During the integration, our planning did not yield the expected outcome. There were delays, communication gaps, decision issues, and other problems that affected the integration,” said the VP of finance for a retail firm.

“If we had included an adviser, these issues could have been taken care of during the planning itself.” Integration proved to be one of the most difficult areas for the corporate acquirers 18 UNSUCCESSFUL DEALS Exhibit 8: The Value External Consultants Added to Successful Deals Due diligence SUCCESSFUL DEALS 12% Due diligence 78% 87% 88% Valuation (M&A and purchase price allocation) 24% 76% Management of the process or negotiations Valuation (M&A and purchase price allocation) 57% 80% 78% 43% Integration planning 20% Management of the process or negotiations 76% 63% 80% Integration execution 50% Integration planning 65% 63% 50% Strategy development or refinement 33% Integration execution Some value Significant value 54% 35% Strategy development or reï¬nement 54% 67% 43% Exhibit 9: Areas for Which, With Hindsight, Unsuccessful Deal-Makers Would Have Used External Consultants Due diligence 12% “We were using outside consultants for strategy development and other process management, as we wanted to keep the momentum in the deal process. Their experience helped us in making better decisions on the deal.” VP of M&A, mining company 88% Valuation (M&A and purchase price allocation) 30% 70% Management of the process or negotiations 44% 56% Integration planning 12% 88% Integration execution 23% 10% 67% Strategy development or refinement 50% No Unsure 5% 45% Yes 19 . Harnessing the Value of Cross-Border Transactions Cross-border deal-making is a large component of the recent uptick in M&A activity. According to Mergermarket data, there was $1.4 trillion worth of crossborder deals in 2014 – up 82.6 percent from 2013. This trend has continued into 2015, with cross-border deal values up again in the first quarter, by 12.2 percent. Corporate executives are increasingly keen to add value to their companies by expanding beyond national borders. $184.1 billion was the value of global crossborder M&A deals in the first quarter of 2015, up 12.2 percent from a year before. These transactions, while potentially lucrative when they provide new markets and geographies to buyers, can be much trickier to pull off than their domestic counterparts. The challenges – including differences in business practices, regulations, and culture – are reflected in the survey results.

Thirty-three percent of unsuccessful deals (as opposed to just 11 percent of successful deals) crossed national borders (Exhibit 10). Exhibit 10: Cross-Border and Domestic Deal Success 67% 33% 89% 11% 0% 100% Respondents with an unsuccessful deal Inside country of headquarters 20 0% 100% Respondents with a successful deal Outside country of headquarters 21 . Steering Successful Growth: Value Capture in M&A Exhibit 11: Strategies Executed During Cross-Border and Domestic Deals Expanded due diligence period focused beyond financial to forward-looking operational/integration issues 84% 48% Prioritization of resources and effort around highest value-capture initiatives 84% 67% Utilization of synergy capture plan for each significant synergy 82% 71% Increased internal accountability for deal results 61% 52% Utilization of M&A playbook and toolkit 49% 38% Doing Things Differently Particularly given the heightened risks inherent in a cross-border deal, the survey responses suggest that the acquiring companies need to do a lot more to increase their chances of success. While most domestic deal-makers executed a synergy capture plan (82 percent) and resource prioritization (84 percent), these strategies were, contrary to expectations, executed at an even lower rate in crossborder deals than in domestic deals (71 percent and 67 percent, respectively). This unfortunate contrast is even more pronounced for expanded due diligence, used in 84 percent of domestic deals and only 48 percent of international deals (Exhibit 11). In fact, most of the dimensions of due diligence were deployed less often in cross-border deals than domestic deals (Exhibit 12). was executed after planning and gauging all possible scenarios. We expanded the diligence period by focusing on the key areas and thoroughly inspecting all aspects and metrics,” said the senior VP of strategy at a chemicals firm.

“This helped us in addressing the operational issues, and integration was carried on with efficiency.” Help Wanted Like expanding the due diligence process, seeking help from outside the business can help realize the value of international transactions. The use of external consultants is more common for most aspects of crossborder deals than domestic deals. This is seen most clearly in the areas of integration planning (71 percent for “Moving the target company’s headquarters to another country was not facilitated by our own governing bodies. Hence, we had to comply with significant regulations and legal policies. And, as a result, we were forced to extend our due diligence period in order to bring successful solutions to the table.” Corporate Development Director, restaurant company 44% 43% Use of incremental external resources 39% 48% Use of succinct deal summary to clarify deal thesis and key value drivers 34% 48% Inside country of headquarters 22 Expanded due diligence can be crucial for navigating some of the complex issues involved in cross-border transactions – including new regulatory environments. “Being a cross-border deal it was advisable to consult external advisors for fair valuations and negotiations.

Also, in integration the external advisors helped ensure that the differences in culture and operations did overly skew the integration,” said the director of corporate development at a hospitality company. Exhibit 12: Facets of Due Diligence in Domestic and Cross-Border Deals Expanded due diligence can also help a company identify potential barriers early in the transaction, thus preventing potentially value-destroying issues from emerging later in the process. “The deal Utilization of integration scorecard Verification of input cost savings assumptions Establishment of objective financial and operational metrics pre- and post-acquisition 99% 90% Detailed pre-acquisition analysis of profit contribution by product and customer 80% 86% Development of combined working capital requirements 75% 62% Outside country of headquarters 71% 62% Domestic Cross-border 23 . Steering Successful Growth: Value Capture in M&A Overcoming Cross-Border Pitfalls cross-border deals and 56 percent for domestic) and the management of the process or negotiations (76 percent and 61 percent) (Exhibit 13). Exhibit 13: Use of External Consultants in Cross-Border and Domestic Deals Due diligence 76% 76% Using external consultants for international deals can help to bridge the gap between the buyer and seller – by helping both parties achieve culturally accepted deal positions, which helps when it comes to integrating the respective businesses, and in terms of value. “Being a cross-border deal, it was advisable to consult external advisers for fair valuations and negotiations, so we approached local and international advisers to identify the actual value and to determine the strategies needed,” said a corporate development director at a hospitality company. “Also, for integration we used external advisers for better planning and execution so that the differences in culture and operations did not overshadow the integration, as advisers were able to guide us well.” Companies entering new geographies for the first time also used advisers – particularly for due diligence. “Outside consultants were used for due diligence, as it was a challenging activity,” said a finance director at a retail company. “We wanted to gain key value from their insights and understanding of the transaction fertility in a market which was new to us.” 24 Marc Shaffer and Chris Nemeth offer ways that companies can improve the performance of their cross-border acquisitions. Valuation (M&A and purchase price allocation) 73% 67% Management of the process or negotiations 61% 76% Integration planning 56% 71% Strategy development or refinement 43% 52% Integration execution 38% 48% Domestic Cross-border In the contemporary deal economy, more often than not, cross-border transactions focus on penetrating new markets.

A decade ago, pursuing a deal in China would have been aimed at obtaining access to low-cost labor. Today, that transaction more likely reflects a desire for inorganic growth and access to the Asian market. This change in cross-border acquisition places the problem of capturing commercial synergies in an unfamiliar market at the very center of the deal. It’s little wonder that the survey revealed a tendency for cross-border deals to be less successful than domestic ones. Another reason cross-border deals appear to be tougher to execute is the need to navigate the cultural differences. Language can be a barrier, as can differing protocols and ways of doing business. The business culture norms of the United States, for instance, are likely to get short shrift in Asia and the Middle East, where often more time is needed to build relationships before productive negotiations can even begin. In addition, the roles of those involved in the M&A process can differ significantly in different cultures.

Whereas investment banks are often tapped to drive the early deal process in the U.S., for example, in Asia they tend to play the role of relationship managers. In the pursuit of an international acquisition, corruption is also a concern. A U.S. company involved in payments to officials — which might be commonplace in another country — could run afoul of the U.S. Foreign Corrupt Practices Act. The resulting civil and criminal penalties, as well as reputation damage, would cause tangible losses to the deal’s value, not to mention the company’s reputation. In addition, companies need to consider what their next move will be after completing a cross-border acquisition.

For instance, will it be a one-time investment, or is there a long-term acquisition plan? Further, how are the investments being financed and can cash be repatriated? Making sure that the strategy is sound and legal under the target country’s jurisdiction is another factor to consider. Finally, a potential buyer must consider the political and economic environment of the country where the proposed investment is based. While an emerging market country might be attractive, for example, an acquirer could face the challenge of coming to grips with the an unstable legal system, government, or economy in that country. On top of this, the country might have restrictions on foreign ownership levels that would cause the buyer to have unwanted “co-partners.” Because of these factors, combine so that cross-border mergers and acquisitions can be fraught with potential value-destroying pitfalls.

However, companies can increase their chances of capturing value by: „„ Assessing the risk early. It’s important to uncover potential corruption concerns early in the M&A process. Finding out early if it’s possible to restructure the payments into a more formal and legal process will provide time for the changes to be made.

And if that proves to be impossible, the potential buyer can get out of the deal at an early point. „„ Being upfront. In places where trust is a big part of the deal-making relationship, it is important for dealmakers to be upfront and honest about their intentions. Safeguards like escrow and indemnification clauses, for example, are offensive in some cultures where an oral agreement and a handshake are enough to cement a deal.

Also, a potential acquirer needs to explain its due diligence purpose and plan to the seller at the beginning of the relationship. „„ Using local help. Cross-border sellers with experience in particular areas of the world might be more comfortable with local people working on behalf of the buyer. Using a local agent can help ease the seller’s anxiety about aspects of the country of the buyer – U.S.

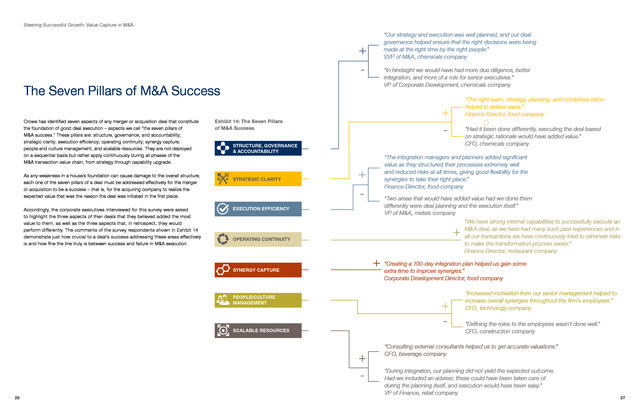

litigiousness, for example. 25 . Steering Successful Growth: Value Capture in M&A + The Seven Pillars of M&A Success Crowe has identified seven aspects of any merger or acquisition deal that constitute the foundation of good deal execution – aspects we call “the seven pillars of M&A success.” These pillars are: structure, governance, and accountability; strategic clarity; execution efficiency; operating continuity; synergy capture; people and culture management; and scalable resources. They are not deployed on a sequential basis but rather apply continuously during all phases of the M&A transaction value chain, from strategy through capability upgrade. As any weakness in a house’s foundation can cause damage to the overall structure, each one of the seven pillars of a deal must be addressed effectively for the merger or acquisition to be a success – that is, for the acquiring company to realize the expected value that was the reason the deal was initiated in the first place. Accordingly, the corporate executives interviewed for this survey were asked to highlight the three aspects of their deals that they believed added the most value to them, as well as the three aspects that, in retrospect, they would perform differently. The comments of the survey respondents shown in Exhibit 14 demonstrate just how crucial to a deal’s success addressing these areas effectively is and how fine the line truly is between success and failure in M&A execution. “In hindsight we would have had more due diligence, better integration, and more of a role for senior executives.” VP of Corporate Development, chemicals company “The right team, strategy, planning, and combined vision helped to deliver value.” Finance Director, food company + - Exhibit 14: The Seven Pillars of M&A Success STRUCTURE, GOVERNANCE & ACCOUNTABILITY STRATEGIC CLARITY “Our strategy and execution was well planned, and our deal governance helped ensure that the right decisions were being made at the right time by the right people.” SVP of M&A, chemicals company + - EXECUTION EFFICIENCY “Had it been done differently, executing the deal based on strategic rationale would have added value.” CFO, chemicals company “The integration managers and planners added significant value as they structured their processes extremely well and reduced risks at all times, giving good flexibility for the synergies to take their right place.” Finance Director, food company “Two areas that would have added value had we done them differently were deal planning and the execution itself.” VP of M&A, metals company “We have strong internal capabilities to successfully execute an M&A deal, as we have had many such past experiences and in all our transactions we have continuously tried to eliminate risks to make the transformation process easier.” Finance Director, restaurant company + OPERATING CONTINUITY + “Creating ato100-day integration plan helped us gain some extra time improve synergies.” SYNERGY CAPTURE Corporate Development Director, food company PEOPLE/CULTURE MANAGEMENT + - SCALABLE RESOURCES + 26 “Increased motivation from our senior management helped to increase overall synergies throughout the firm’s employees.” CFO, technology company “Defining the roles to the employees wasn’t done well.” CFO, construction company “Consulting external consultants helped us to get accurate valuations.” CFO, beverage company “During integration, our planning did not yield the expected outcome. Had we included an adviser, these could have been taken care of during the planning itself, and execution would have been easy.” VP of Finance, retail company 27 . Conclusion Companies face an M&A market that is ripe with opportunity. With the rise of deal volumes across the board, the availability of cheap debt, and the emergence of firms from their erstwhile shells as economies recover, the time appears right to start striking deals. However, companies are under enormous pressure to make only the deals that will drive value for their shareholders. Doing that requires executives to lay substantial groundwork before, during, and after the deal has been agreed upon. This groundwork comes in many forms.

The deal rationale needs to be considered carefully before the merger or acquisition, procedures need to be in place to maximize the efficiency of the deal process, and deal-makers need to be tirelessly engaged and obtain the appropriate assistance throughout all the stages of the M&A transaction value chain. The quality and extent of the due diligence and integration planning performed differ markedly between successful and unsuccessful deals. The successful deal-makers who responded to this survey offered a few pieces of high-level advice: „„ Expand your reach. Successful acquirers are cognizant of the wide scope of potential strategic intent deviations throughout a deal’s life cycle.

They monitor the broad range of deal rationales, put an array of resources – including senior support to maintain focus – toward the deal’s execution to examine the due diligence process from different perspectives, and look at the details as well as the deal as a whole. „„ Scrutinize to monetize. Going beyond the basics of due diligence ultimately saves time and money, and enhances value in the long run. Success requires expanding diligence to areas that are outside the standard financial areas and keeping in mind that due diligence is not a box-checking exercise; rather, it is a means of mitigating risks and maximizing value. „„ Add hands, add value. Obtaining external advice and assistance from qualified advisers at critical points of a deal can add significant value to the transaction.

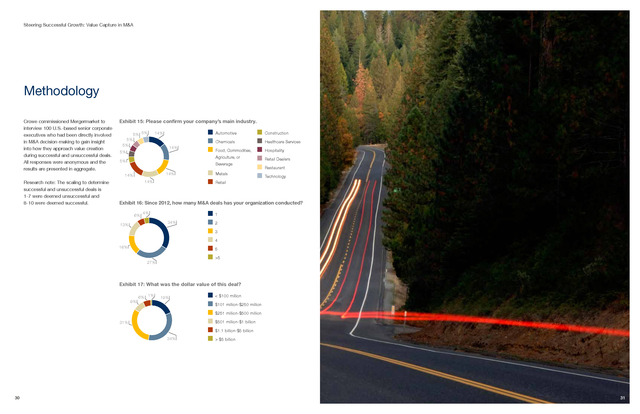

The biggest potential benefits of using consultants appear to come during the due diligence and integration stages. In light of the stakes of the typical deal, this targeted investment is shown to be beneficial. 28 29 . Steering Successful Growth: Value Capture in M&A Methodology Crowe commissioned Mergermarket to interview 100 U.S.-based senior corporate executives who had been directly involved in M&A decision-making to gain insight into how they approach value creation during successful and unsuccessful deals. All responses were anonymous and the results are presented in aggregate. Exhibit 15: Please confirm your company’s main industry. 5% 5% 5% Construction Chemicals 14% Healthcare Services Food, Commodities, Hospitality Agriculture, or 5% Beverage 14% 14% Research note: The scaling to determine successful and unsuccessful deals is 1-7 were deemed unsuccessful and 8-10 were deemed successful. Automotive 14% 5% 5% 14% Metals Retail Dealers Restaurant Technology Retail Exhibit 16: Since 2012, how many M&A deals has your organization conducted? 6% 4% 1 34% 13% 2 3 4 16% 5 >5 27% Exhibit 17: What was the dollar value of this deal? 9% 6% 1% 19% < $100 million $101 million-$250 million $251 million-$500 million $501 million-$1 billion 31% $1.1 billion-$5 billion 34% 30 > $5 billion 31 . Contact Information Marc Shaffer is a partner in M&A advisory services with Crowe Horwath LLP. He can be reached at +1 312.857.7512 or marc.shaffer@crowehorwath.com. Chris Nemeth is a director in M&A advisory services with Crowe. He can be reached at +1 312.899.8405 or chris.nemeth@crowehorwath.com. Some of the survey respondents' comments have been edited for clarity. www.crowehorwath.com Crowe Horwath LLP is an independent member of Crowe Horwath International, a Swiss verein. Each member firm of Crowe Horwath International is a separate and independent legal entity.

Crowe Horwath LLP and its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. This material is for informational purposes only and should not be construed as financial or legal advice.

Please seek guidance specific to your organization from qualified advisers in your jurisdiction. © 2015 Crowe Horwath LLP AS-16007-001 .

corporate executives about some of their most recent deals – looking in particular at what the acquiring companies set out to achieve, the processes they used, and whether they deemed the deals successful or unsuccessful in terms of capturing value. In this report, we use the collected data to identify some of the important differences between good and bad deals, and we provide some comments from the interviewed executives. 30 Deal-making levels will remain at record highs as long as companies are hungry for growth and have access to cheap cash. While these factors put pressure on management teams to do a deal, no business wants to turn a potentially big opportunity into a costly mistake.

Making a merger or acquisition successful is one of the toughest tasks in business today; in such a competitive environment, it is also one of the most crucial. While nobody can guarantee a successful deal, we hope that this report will provide insight into the paths taken by successful acquirers. We trust that you find this report helpful, and we welcome your feedback. Marc Shaffer Partner, Crowe Horwath LLP +1 312 857 7512 marc.shaffer@crowehorwath.com 2 Chris Nemeth Director, Crowe Horwath LLP +1 312 899 8405 chris.nemeth@crowehorwath.com 3 . Steering Successful Growth: Value Capture in M&A Executive Summary After a record 2014, deal-making continues to thrive this year. According to Mergermarket data, $719 billion worth of deals were made in the first quarter of 2015 – up 13.4 percent from the same period the previous year. This is the highest first-quarter value figure since 2007. Cross-border activity is also thriving, with a 12.2 percent year-on-year increase in M&A value. seeks to answer that question – in particular, how the characteristics of successful deals differ from those of less successful deals and why a specific deal either builds or loses value at particular points on the M&A transaction value chain as the deal moves toward completion. Following are some of the key findings of this survey. The growing appetite to spend, however, comes at a time when companies face major challenges. Macroeconomic factors – such as slow economic growth in Europe, a slowdown of emerging markets’ economies, and falling oil prices – have spurred consolidation in some sectors, making the realization of expected synergies more important than ever. In addition, the rise in the number of activist investors has increased the pressure on boards to maximize shareholder value through buybacks, dividends, and M&A.

Corporate executives who don’t respond adequately to this pressure could be grilled at annual shareholder meetings and even asked to resign. Also, increased business activity among countries brings with it an increase in the challenges often associated with cross-border transactions, such as regulatory issues and cultural differences. With so many factors in play, how can companies have a better chance of consistently creating value from their mergers and acquisitions? This report 4 Everyone can improve. The survey shows that even the most experienced deal-makers, by their own admission, are leaving substantial value on the table. There appears to be room for improvement at all stages of the M&A transaction value chain – from M&A strategy clarification, deal targeting, due diligence rigor, and integration execution. Strategic clarity and insight set the table for success.

The more successful deal-makers performed more value-clarification processes than the unsuccessful companies did. More time spent upfront on clarifying and understanding exactly how best to extract the value from a merger or acquisition is a hallmark of better deals. Synergies are not created equal. “Strategic” deals focused primarily on commercial synergies – including market and channel expansion, new product offerings, and cross-selling – proved to be substantially more challenging and problematic than deals focused on goals such as consolidation, removing production capacity from the market, and economies of scale. Contemporary due diligence transcends the financials. Expanded due diligence – incorporating areas like IT, operations, human resources, and culture – was reported to be in almost nine out of 10 of the successful deals cited by the respondents. Conversely, it occurred in just 59 percent of the unsuccessful deals. Integration is crucial – and a particular area of opportunity. Surprisingly, many of the otherwise experienced deal-makers responding to the survey indicated that they had inadvertently neglected or underestimated the integration aspect of the M&A transaction value chain and lost value as a result.

This finding holds for both pre-close integration planning and post-close integration execution. By almost every integration execution dimension surveyed, the more successful deal-makers seemed to invest more in the integration activity. For instance, half of successful deal-makers used an integration scorecard, compared to only 37 percent of unsuccessful ones. The percentages were similar when successful and unsuccessful respondents (54 percent and 35 percent, respectively) were asked whether they consulted external expertise for executing the integration.

In general, while most deal-makers seem to understand that integration is utterly critical to capturing value, integration is not consistently receiving the early attention and adequate resources necessary for the delivery of its full value. Good advice augments the internal team’s capability and drives results. Virtually across the board, using qualified external advisers enhanced the value of the deals. Eighty-eight percent of the respondents whose companies executed successful deals and used an external consultant during the due diligence process said that having the adviser onboard generated significant value. By contrast, those in the unsuccessful deal category unanimously said that their companies should have used advisers during due diligence, integration planning, negotiation, and/or process management. Deals abroad are even tougher. Perhaps not surprisingly, the survey indicates that cross-border transactions present far more challenges and risks than domestic deals do.

These issues are further compounded by companies’ inability or unwillingness to deploy qualified internal resources for these transactions and tendencies not to supplement their teams with local knowledge. 5 . Steering Successful Growth: Value Capture in M&A Capturing Value Across the M&A Transaction Value Chain Exhibit 1: The M&A Transaction Value Chain Marc Shaffer and Chris Nemeth discuss how proper focus throughout the M&A transaction value chain can help companies achieve greater acquisitions success. The nature of the deal market and deal execution is changing, and companies must continue to adapt if they hope to succeed in today’s competitive M&A market. “Historically, M&A has been treated as a kind of ad hoc activity,” said Chris Nemeth, director in M&A advisory services at Crowe. “It’s only recently, with the greater prevalence of M&A as a core growth strategy, that deal-making as a discipline has been formalized, with a more professional focus on the tactical, executional aspects like targeting, due diligence, valuation, and integration.” This raises the question of how, in the current M&A market, the deal process works and, specifically, how it should work to capture the best value. Looking at the deal process as a “value chain” can help executives properly understand how each stage of the acquisition functions and, ultimately, is connected. “The M&A transaction value chain model not only makes the steps of the deal explicit and clear,” said Nemeth, “but it also speaks to the fact that the ultimate value of the deal can be either supported or undermined at each stage.” The following list expands on each of the stages of what Crowe calls the “M&A transaction value chain” and examines why each is critical to capturing deal value. 1.

M&A Strategy Take time to understand and articulate the 6 deal rationale and its link to the underlying business strategy. “Companies typically have a ‘macro’ strategy but often not a specific M&A strategy,” said Nemeth. “Why is this important? For one, it’s all too easy to get caught up in the litany of transactional ‘table stakes’ issues and lose sight of the deal’s value drivers. Also, with respect to finding and pursuing targets, deal-making is usually best done proactively, and not just reacting to and chasing opportunistic targets.” Regarding the importance of strategic planning to his company’s deal, the vice president (VP) of corporate development at a chemicals company said that his team’s thorough planning of the preacquisition activity was remarkably valuable in terms of achieving the ultimate target. 2. Due Diligence Grasping the deal’s underlying value drivers – the variables that affect the actual value of a company – should be at the heart of any due diligence process, as well as the financials.

“Firms want to focus on the black-and-white stuff and not the value drivers,” said Marc Shaffer, a partner in M&A advisory services at Crowe. “You need to understand what is driving the business by looking at what is driving the business value, not just completing a checklist. Good due diligence will look at these drivers.” Moreover, the insight gained in this process can drive value further along the M&A transaction value chain.

“Often, the due diligence and integration teams rarely talk – and we try to change that,” said Shaffer. “If we include members of the integration team in the due diligence, the integration team can begin to plan ahead for the integration. 1 2 M&A STRATEGY DUE DILIGENCE 3 Getting this right can create a good deal and dynamic for both buyer and seller. Reflecting on his experience, one restaurant company corporate director said, “In order for both parties to have a fair deal, we used standardized valuation techniques. We were assisted by external valuation consultants to get accurate valuations.” CLOSE PHASE 2 7 CAPABILITY UPGRADE “All things equal, faster integration equals better results,” said Nemeth. “The one thing that virtually all deal-makers voice is that, irrespective of the specific deal or circumstance, they wish they could have integrated faster.” In particular, according to Nemeth, companies should focus on “bite-sizing” the integration into three basic areas: (1) vetting, prioritizing, and planning related to the key value drivers; (2) planning the functional transition in order to assume operational control and maintain operating continuity; and (3) laying out the change management and culture assimilation road map for the new, combined company. 4.

Integration Planning Despite having successfully navigated to this stage in the deal process, a company can irretrievably harm the deal’s value by neglecting to prepare for the integration. And to make matters even more challenging, time is of the essence. INTEGRATION PLANNING AGREEMENT LETTER OF INTENTION 3. Valuation In many cases, valuation is part art and part science.

As such, it can pay to work with an experienced, third-party specialist. “We’re trying to help the buyer understand where, why, and how they are getting value,” said Shaffer. “For example, if you want to get it from minimizing tax, it might be worth focusing on the country-by-country profitability.

If you’re more focused on quarterly pre-tax earnings, however, quick deductions from highly valued inventory turning into the P&L might not be desired.” 4 VALUATION 6 INCREMENTAL OPTIMIZATION into near-term integration execution issues versus longer-term optimization issues.” The near-term focus of the post-close integration is on quickly assuming control of the target company’s operation and workforce, stabilizing the operational environment, and protecting key customer relationships and the associated top-line performance. Nemeth said, “If you’re able to get meaningful traction on attacking the first wave of synergy projects, that’s great, but the immediate priority is stabilization – mitigating the critical risks and making sure the company is able to keep the lights on.” 6. Incremental Optimization 5.

Post-Close Execution “Even in modest integrations, there’s an awful lot of work that has to get done,” said Nemeth about this first of two integration stages. “So it’s very useful, in our experience, to rigorously separate and prioritize tasks The focus during this, the second postclose integration stage, is on attacking the deal’s synergies and value drivers. “Stage two is about allocating focus and resources to the areas with the highest potential value,” said Nemeth. “In most 5 POST-CLOSE EXECUTION deals, typically there are more projects with potential synergy than there are available internal resources – most of whom also have a ‘day job.’” Nemeth believes that “the most important step is prioritization of resources and efforts, and aligning resources accordingly. 7.

Capability Upgrade High-performing acquirers use each deal as a learning curve, working to incorporate those hard-won lessons into their M&A playbook. “Better acquirers see M&A as central to growth strategy, not just a onetime deal,” said Nemeth. “As such, they view M&A execution capability as critical, and thus continuously scrutinize, maintain, and use an M&A execution ‘playbook.’ This can help to minimize inefficiency, properly stage work steps and priorities, quickly bring new and inexperienced resources up to speed, avoid needing to ‘reinvent the wheel’ with each new deal, and more.” 7 .

Maximizing Value Capture The value chain presents tremendous opportunities and pitfalls for companies engaged in M&A. In this section, we outline what is separating good deals from unsuccessful ones. Spotlight on M&A Strategy One salient finding from the survey is that acquisitions focused on commercial synergies appear to be more difficult to undertake and complete successfully than those targeting operational synergies. In every case, the survey elements that are tied to commercial synergies – for example, incremental product or service offerings, the impact on gross margin, and access to new geographies, markets, or channels – had higher rates of failure than success. Exhibit 2: The Drivers of Value Creation UNSUCCESSFUL DEALS SUCCESSFUL DEALS Incremental product/service offerings 80% 74% Operational synergies/cost reduction/economies of scale 67% 63% Increased top line, market share 61% 67% Access to new human capital, skills, and capability 59% 61% Access to new geographies, markets, or channels 57% Conversely, the deals that were focused on operational synergies or cost-based elements – including the rationalization of combined product offerings and working capital requirements – had higher rates of success (Exhibit 2). See sidebar “For Good Reasons,” page 11. 52% Rationalization of combined product offerings 39% 46% Working capital requirements 26% 41% Impact on gross margin 28% 22% Elimination of a competitor 20% 13% “Our key decision-makers enforced good procedures to be followed during the whole deal cycle.

Their thorough planning with regard to the pre-post acquisition activity was remarkable in terms of achieving the target – in fact it turned out to be a value add to our whole deal. Capital allocations were more effective and we were able to focus on areas that needed more attention and improvements.” VP of Corporate Development, chemicals company 8 9 . Steering Successful Growth: Value Capture in M&A For Good Reasons Exhibit 3: Strategies Executed During a Transaction UNSUCCESSFUL DEALS Executing the Strategy SUCCESSFUL DEALS Expanded due diligence period focused beyond ï¬nancial to forward-looking operational/integration issues 59% 91% Prioritization of resources and effort around highest value-capture initiatives 67% 91% While the use of synergy capture plans is common for both the successful and the unsuccessful deals of the survey respondents, there was a marked difference in the successful acquirers’ ability to “walk the talk” and put some teeth into those plans. The successful deal-makers deployed a greater portfolio of execution strategies – including an expanded due diligence period, the careful prioritization of resources, increased internal accountability for deal results, an M&A playbook and toolkit, and the use of an integration scorecard – than did the unsuccessful deal-makers (Exhibit 3). Utilization of synergy capture plan for each signiï¬cant synergy 85% 76% Increased internal accountability for deal results 54% 63% Utilization of M&A playbook and toolkit 39% 54% Utilization of integration scorecard 37% 50% Use of incremental external resources 41% 41% Use of succinct deal summary to clarify deal thesis and key value drivers 37% 37% 91% 67% Prioritization of resources and effort around highest value-capture initiatives Utilization of synergy capture plan for each signiï¬cant synergy UNSUCCESSFUL DEALS Prioritization of resources and effort around highest value-capture initiatives 0% 85% 10 While having a solid strategy in place is paramount, it is all for nothing unless a deal is executed properly. As one retail executive pointed out, “The execution was the most crucial stage in shaping the success of the deal.” TO 100% 91% Expanded due diligence period focused beyond ï¬nancial to forward-looking operational/ integration issues R AT E G IES P ST 100% SUCCESSFUL DEALS Chris Nemeth and Marc Shaffer explore the challenges of commercial synergy value capture. M&A is clearly an attractive and accepted method for gaining access to new markets, channels, product and service offerings, customer segments, and the like. However, the survey respondents indicated that deals focusing on these commercial synergies are significantly more challenging than those targeting operational, cost-focused synergies. Perhaps one way to understand this is that, in a cost-synergy deal, many of the important variables are internal to the acquiring company and thus in the buyer’s control.

In essence, executives are asking their own people to do things differently in order for the company to realize the efficiency benefits. For commercial synergies, however, the buyer is faced with myriad external factors in addition to the internal factors. Not only are the internal stakeholders asked to do things differently, but the external stakeholders, such as customers and suppliers, are being asked to do things differently as well. The acquiring company asks its customers to buy new things, buy more things, accept different pricing, and/or interact with the newly combined company in new and different ways. It’s easy for an acquirer to underestimate the disruption and challenges these changes create for customers, suppliers, and others, so the acquiring company’s executives can be blindsided by subsequently flagging results.

In addition, in cases where the deal is taking a competitor out of the market, customers often feel the need to offset their increased supply risk by further diversifying their sources of supply and as a result buy less from the newly combined company. Even beyond these factors, there are additional myriad external market forces, such as the response of competitors, foreign exchange rates, the customers’ business cycle, general supply and demand issues, and more. Failure to think holistically and realistically about the assumptions made about commercial synergies can easily result in company performance that trails expectations. Following are some tenets that executives pursuing M&A for the commercial synergies should bear in mind to increase the chances of success. „„ Consider commercial diligence. Don’t fixate on the balance sheet or trailing financials. If the commercial side of the business is what drove you to acquire it, then also look to focus on and examine the commercial aspects, including both the risks and potential benefits. priorities but also work to heighten key customers’ confidence and build “relationship equity” in the combined company right out of the gate. „„ Risk equals reward.

Consider the retention of existing key customers to be equally as important as incremental synergy capture. As any executive who’s lived through customer fallout from a troubled deal process will attest, “re-earning” the trust and business of a damaged customer relationship is often even more difficult and costly than capturing new customer synergies. „„ Don’t overpromise. With so many external factors to consider, it is better to be conservative about external analysts’ forecasts of sales synergies. The age-old wisdom of “underpromise and overdeliver” is a prudent operating principle when it comes to forecasting and communicating commercial synergy capture. „„ Listen to your customers at closing. Meaningfully involving key customers in the integration planning process can not only help guide the integration 11 .

Spotlight on Due Diligence Due diligence was treated as a more holistic activity – both in terms of its breadth and its depth – in the successful deals more so than in the unsuccessful deals. The due diligence period of successful deal-makers was likely to be more prolonged and have a greater scope. The due diligence process of 91 percent of the successful deal-makers was expanded, focusing beyond the financial aspects of the deal, while just 59 percent of those who had unsuccessful deals used an expanded scope of diligence (Exhibit 3). It is important for corporate executives to have the right goals in mind with due diligence. “Due diligence was conducted with the intention of maximizing deal value,” said one finance director at a chemicals firm.

“Our specialists helped in the timely execution and monitoring of the activity. The deal enabled our business to transform and helped us explore key geographies.” A Wider Scope Successfully executed deals reported by the survey respondents encompassed a much broader range of due diligence tasks than the unsuccessful deals. In successful deals, there was a greater emphasis on detailed pre-acquisition analysis of profit contribution by product and customer (91 percent, compared with 70 percent for unsuccessful deals), development of combined working capital requirements (81 percent, compared with 61 percent), and 12 verification of cost savings assumptions (76 percent, compared with 61 percent). Almost all the respondents’ companies, whether their deals proved to be successful or not, established objective financial and operational metrics preand post-acquisition (Exhibit 4). For successful deal-makers, these components of thorough due diligence were vital.

“Information was gathered well in advance, so we were able to spend ample time in transforming them into actionable insights,” said the finance director at a beverage group. “Gaining a 360-degree perspective of the deal was one of the most important factors in conducting our due diligence processes.” 81% of successful deal-makers considered the development of working capital requirements in the due diligence process, compared with 61% of unsucessful ones. Exhibit 4: Facets of the Due Diligence Process UNSUCCESSFUL DEALS SUCCESSFUL DEALS Establishment of objective ï¬nancial and operational metrics pre- and post-acquisition 98% 96% Detailed pre-acquisition analysis of proï¬t contribution by product and customer 70% 91% Development of combined working capital requirements 61% 81% Veriï¬cation of input cost savings assumptions 61% 76% 13 . Steering Successful Growth: Value Capture in M&A 91% of successful deal-makers did detailed pre-acquisition analysis of profit contribution by product and customer as part of the due diligence process. Moreover, performing due diligence on a wider range of aspects can help maintain a deal’s value as it progresses along the value chain. “The most important aspect of due diligence for us was the development of combined working capital requirements and cost savings to increase the long-term value,” said a construction firm CFO. The due diligence process for unsuccessful deals relied heavily on establishing pre- and post-acquisition financial and operational metrics (98 percent). Longer-term factors, such as the development of combined working capital requirements (61 percent), were ignored much more often than they were in the successful deals’ processes. One automotive executive who had been involved in an unsuccessful acquisition acknowledged that “activities that led to the development of combined working capital requirements were skipped, as the acquired business had a reputation and global presence. Workforces were to be combined and [we thought] this would help us in becoming more robust and active toward market changes, risks, and opportunities.” This near-sighted focus with respect to due diligence can be costly to firms in the long run. Another automotive executive said shortsightedness might have destroyed value during the due diligence process for his company’s deal, which was ultimately unsuccessful.