Description

MOMENTUM 2016

Technology Outlook:

Sustaining Growth in

an Environment

of Rapid Change

A 2016 CohnReznick LLP Report

. Regulatory Issues...

6

mo • men • tum

noun: impetus and driving force gained by the

development of a process or course of events

. Table of

Contents

..

Sustaining Growth in an Environment of Rapid Change .......1

• Capital Raising ...................................................................................... 1

• Business Strategy ................................................................................... 3

• Is Now the Time to Acquire Another Company? .............................. 7

Legislative Updates .....................................................................9

Conclusion .................................................................................12

@CR_TechInd

A CohnReznick Report

3

.

Preface To grow at a sustainable level, a company needs more than the execution of an innovative idea. It requires focus on key issues like accessing growth capital, cash management, building a strong management team, designing efficient operating systems, and paying careful attention to compliance issues. While new and innovative technology is critical for a company’s success, we cannot minimize the importance of building a solid foundation to support sustainable growth. Having the right people, systems, and processes in place also puts a company in a position of strength when the time is right to evaluate and potentially pursue a liquidity event. While 2016 may turn out to be the year that technology firms say goodbye to sky-high valuations and limitless options for capital raising, it may still be a time of remarkable opportunity. Despite an IPO market that has all but dried up, strong, well-positioned companies will continue to be funded or viewed as prized acquisition targets. M&A activity should remain at a robust pace.

The investors are still out there—with capital available for the right opportunity. To this end, the 2016 edition of Momentum: Technology Outlook focuses on some of the key issues and recommended strategies in fundraising and business strategy, as well as new legislative developments that will impact the way technology companies do business. These are among the things that need to be on your agenda in the year ahead. We hope you find this document, which represents the collective insights of the members of CohnReznick’s Technology Practice, to be a thought-provoking commentary on the state of the industry and helpful to you as you seek to plot your own course. We look forward to your thoughts and to discussing the issues it raises. Alex Castelli, CPA Partner Technology Industry Practice Leader March 2016 Alex Castelli . Sustaining Growth in an Environment of Rapid Change Capital Raising In 2015, capital raising activities in the public markets There is no doubt that, within the technology industry, were strongly influenced by increasing volatility and a the giddiness of the last few years has evaporated. But lack of investor confidence. Unfortunately, these same this is not a bad thing—exuberance is hard to sustain conditions have followed us into 2016. We are hopeful and, in any event, makes for poor strategy.

More that, as the year progresses, stability and investor importantly, three fundamental drivers remain intact: confidence return to the markets. When they do, the number of capital raising opportunities for • The infiltration of technology into every aspect growth-oriented companies will certainly increase. of our businesses and our lives—from managing For now, market conditions continue to be volatile. unabated, having long ago reached a momentum The IPO window, although not formally closed, that feeds on itself. certainly seems that way. And despite the fact that middle market technology companies have become increasingly less dependent on the IPO as a source of capital, the level of IPO activity has broad market implications.

It impacts both valuations and M&A transaction activity. Three months into 2016, we still supply chains to ordering dinner—continues to grow • The readiness of mature technology companies to turn to acquisition continues, either as a growth strategy when they cannot maintain a healthy growth rate organically, or as part of a strategic plan to enter or dominate markets. await the first technology sector IPO. A CohnReznick Report 1 . • The reduced number of investment options for financial and strategic investors in the low interest rate environment, combined with large cash reserves, means that sound technology companies will remain attractive investments, even if at more modest valuations. For our clients, this environment brings several clear directives. Companies must turn their focus inward, away from valuations and exit strategies and toward controlling costs, optimizing operations, and solidifying their customer base. The default stance toward raising capital in 2016 needs to be “How much do we really need?” rather than, as in prior years, “How much can we get?” But this refocusing on long-term strategy is not a retreat, or even necessarily a slowing down. “When raising capital in 2016, companies should ask ‘How much do we really need?’—not ‘How much can we get?’” Alex Castelli, Partner Technology Industry Practice Leader Indeed, it may be that a company’s strategy for growth in this changing environment requires it to become more aggressive in its business strategy—perhaps even becoming an acquirer rather than a target. However, before an enterprise decides to move forward, it is important that it build a solid foundation to support its strategic plan. This may involve the examination of a variety of issues and options such as evaluating gaps in your management team, reviewing your corporate structure, and analyzing your tax strategy.

A failure to address these matters can have significant implications down the line. 2 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change . Sustaining Growth in an Environment of Rapid Change Business Strategy Digital Transformation— Eating Your Own Dog Food The less-heady reality of 2016 demands that companies increase focus on their current businesses. But what is true for a technology company’s clients is true for the tech space in general. In today’s world, the traditional five-year strategic business plan has been replaced by a five-month plan that is constantly Fortunately, while managing the process of customer conversion and operations optimization has become much more complex, the analytic tools available to generate insights, drive business strategy, and improve every aspect of the customer experience have more than kept pace. Companies, therefore, should view digital transformation as an exciting opportunity to bring an innovation orientation to all that they do. being revised in the face of changing markets, But the fact is that the process of digital transformation better informed customers, new opportunities, and can be easy to do incorrectly, even for technology new threats. While many companies have adopted companies.

Digital transformation requires enterprises an agile mindset in application development, their to rethink at a very fundamental level what it is they approach to key functions like marketing, customer are trying to accomplish and why—especially when retention, and operations is often stuck in the analog the default approach in business often is to focus era. To reprise a saying from the early dot-com days, immediately on how to get something done. The technology companies need to make sure they are result is a great deal of effort on traditional initiatives eating their own dog food. like upgrading ERP and CRM platforms with very little A CohnReznick Report 3 .

“Businesses with a digital purpose will outperform those focused solely on the bottom line.” Paul Gulbin, Managing Director, Digital and Innovation Services When a consumer is offered the opportunity to log onto a company website using a LinkedIn profile instead of typing in a username and password, the company is granted permission to access a wealth of information about that consumer. What is their current employment position? Which associations do they belong to? What kinds of jobs have they had? By gaining access to this kind of lifestyle information, companies can better target their product and service offerings to the consumer’s specific background and degree of influence at the company. This information also gives companies critical information to develop new products and energy given to underlying questions such as how services designed to better address these needs. the lives and expectations of customer personas are Companies such as Salesforce.com changing and which digital strategies can bring us and Gigya are enjoying new levels of success using closer to becoming a critical part of the customer these approaches. experience in real time. The second “customer first” strategy is the use of These questions are important to answer because omnichannel digital commerce to build lasting brand they point toward strategic opportunities, uncover relationships with customers. Digital commerce once inefficiencies, and help mitigate risks.

Take the meant shopping cart conversion, e-coupons, and customer conversion example. The enterprise online payment tools. Today, digital commerce reporting systems for technology companies can has evolved into creating and fostering online provide a false sense of security regarding their communities with customers, using tools such as customer base.

Since ERP and basic CRM do video chat for assisted selling, social network product not harness enough information to understand a reviews and brand advocacy, and service taking on a customer’s interests, likes, and specific attributes, a role in multi-channel lead management. Omnichannel seamless customer experience with the brand will 2.0 is about using digital commerce as a means to remain out of reach. In short, digital transformation help companies generate revenue by enabling them requires “customer first” type of thinking that keeps to build meaningful, two-way relationships with their organizations prioritized on the things that will actually consumers or business customers.

These relationships drive conversion, loyalty, or both. are fostered across multiple retail, wholesale, mobile, There are two significant “customer first” digital strategies that smart companies are now employing. and direct/indirect sales channels, through call centers, and through other digital platforms. The first is personalization. With the continued rise of Companies such as Burberry and Leviev Jewelry are Facebook, LinkedIn, and other social media outlets, growing and outperforming their competitors using consumers are taking a more proactive approach personalization and omnichannel 2.0 digital strategies in sharing certain types of personal data with each to create lasting relationships with their customers. other and with the companies they do business with. These and other innovative companies are leveraging In response, companies have begun to execute digital transformation at the highest level—reinventing permission-based data collection protocols on their the way companies sell to, and retain, their customers. websites and other digital communication tools. 4 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change . While each enterprise’s path toward digital transformation will be different, our experience in helping companies achieve digital leadership suggests that there are three fundamental requirements: A strong vision: Being an agile enterprise demands a great deal of comfort with uncertainty, as strategies get revised in the face of new information and market changes. This makes it all the more important for management to have a strong vision for the company’s products—not in terms of the specifics, which will change over time, but for the problems the products will solve and the value they will add. Freedom from legacy silos: Digitally agile organizations are able to routinely innovate because they continually combine insights and perspectives from across the organization. Similarly, they are able to create holistic experiences because they are always focused on the big picture. In practice, this means that marketing, product development, sales, and other functions are not merely exchanging information but working as part of front-line operational teams. Constant feedback and learning: This is at the heart of digital transformation.

It means, for example, not just having excellent customer service, but using it as an intelligence tool to gather ongoing insight for product development. It means not just creating a robust social media presence, but monitoring and analyzing traffic and then becoming part of the conversation. Above all, digital transformation requires the structure and culture necessary to support this torrent of inputs and the discussions and recalibrations that follow. Cybersecurity: Everyone Is a Target The continued digital disruption of almost all industries, combined with increased interconnectivity between individuals and between organizations, has made cybersecurity an ongoing strategic issue for nearly every enterprise.

Technology companies, however, have an additional layer of concern because of the role their products play within the digital ecosystem. “Many companies think of cybersecurity in terms of ï¬rewalls and encryption protocols— while it is actually a broader business risk issue.” After all, cybercriminals who can breach a technology platform or device can often gain access to an entire organization’s data, and also quite possibly the data of every organization Jim Ambrosini, Managing Director Cybersecurity that uses those products. A CohnReznick Report 5 . While many companies understand this in theory, we have found that mid-market technology companies—those at the front lines of entrepreneurialism and innovation—can sometimes be less savvy in protecting their own data. These companies often think of cybersecurity in a fragmented way—having the right firewalls, encryption protocols, and so forth—rather than having a broader, enterprise cyber program and strategy. Because of their inherent tech savviness, it is easy for them to be strong on the infrastructure side of data protection. The fact is, however, that having technology controls is only one element of the cybersecurity process. There is also the organizational component, covering the security of the network of business partners and developing a comprehensive breach response plan.

And there is a strategic component which includes understanding how cybersecurity integrates with the business and accurately assesses the organization’s threat profile. It is here where technology companies can find their cybersecurity program lacking. In order to ensure cybersecurity preparedness, companies need to take these three steps: Look across your product development chain. Best practice cybersecurity is part of product development lifecycle from coding to delivery.

This means assessing both security within the product itself and in how the product is developed and distributed—particularly if your organization uses a third-party as part of the process. Know your Information assets. The first step in any cybersecurity program is to make sure you have an inventory of your information systems (servers, databases) and an understanding of the type of data that the systems contain (corporate data, personal data, intellectual property, etc.). From here, your company can then build a robust cyber program that includes not only protecting its data, but having the ability to identify threats proactively as well as being able to properly respond to and recover from a data breach. Know your risks and create your cyber program accordingly. Ultimately, cybersecurity is a business risk decision.

A company needs to understand who wants to attack it and the likely ways in which an attacker could access data. Then, the company must align its cybersecurity program to the risk it is willing to accept. Too often, organizations may invest in a cybersecurity solution that is not aligned to the threats they face, or worse, they have underdeveloped, or incomplete programs. 6 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change . Sustaining Growth in an Environment of Rapid Change Is Now the Time to Acquire Another Company? Companies that sit on the other side of the M&A table its competitors, suppliers, and others. In fact, the need to be aware that making an acquisition is likely conversations and interactions you have with other to require new capabilities. After all, they will now firms can provide a good opportunity to segue into be competing against both strategic and financial corporate development discussions. Acquiring a investors with a great deal of experience.

Breaking into business process, people, or product from another the acquirer class requires several things, including: company may to be the ideal strategy in taking your Clearly establishing your objective. It is critical that company to the next level. you have a clearly set goal for the acquisition based Conducting rigorous due diligence. As an acquirer, on your company’s growth objectives.

You must a company needs the intelligence to make informed understand the potential of the acquisition and how risk/reward decisions. Each acquisition will require it will fit into your company’s vision. Will a particular a comprehensive evaluation of historic financial acquisition help you become a dominant player in a performance, key business drivers, profitability trends, particular industry or sector, or is the acquisition meant and areas of potential risk for the target.

This process is to diversify your company’s portfolio? Are you primarily most critical when the target is smaller or less mature. interested in acquiring specific assets (trademarks, Their financial and internal control systems may be less intellectual property, patents, etc.) from the other sophisticated and the information provided may be company or is the acquisition intended to make better less transparent. use of your own internal intellectual property? There are a number of other key factors related to the Identifying the universe of potential targets. In assessing acquisition target that should be reviewed as part of targets, your company may have a solid grasp of the due diligence process. These include: A CohnReznick Report 7 .

• Reputation: You need to understand how the target company is perceived in the industry and which “intangibles” are associated with the current organization, its owners, its product line, etc. If your acquisition target is an “unknown” entity with a good product, you will need to understand where monies may need to be spent in creating brand name recognition (this may not be critical if your company already has strong brand recognition in the marketplace). “A company must clearly establish its goal for an acquisition and understand how it ï¬ts into the overall vision.” Mario Pompeo, Partner CFO Advisory Practice Leader • Management team: Does the target company have a strong management team and have you gotten to know them during the merger / acquisition process? Also, avoid getting get caught up in the “auction You also need to assess whether your existing team frenzy” that can occur for a prized acquisition target. is prepared to assume responsibility for running the Savvy sellers and/or their investors will often behave in target company’s operations unless you are actually a way to drive up the price, causing potential buyers to acquiring the “know how” of the organization. care more about winning the deal than the economics You also need to determine if the company’s of the deal. You should establish price parameters and management team’s skills are complementary to, stick to them. or symbiotic with, your own internal management’s strengths. Lastly, the personal chemistry between the buyer and seller is often a key indicator of the ultimate success of the acquisition.

This is especially true if any of the acquired company’s management team is being retained after the deal closes. • Foreign vs. domestic targets: If you are considering the Establishing the purchase price and financing the deal are two critical considerations. You will need to consider a number of factors including financing terms (i.e., purchase price plus an earn out, etc.), and the acquisition company’s current EBITDA or other multiples for targets in similar industries.

Especially in cases where you can’t agree on a price with the seller, you should consider acquisition of a foreign company, you must be aware using earn-outs to defer payments if the potential that there may be differences in accounting standards, acquisition target does not perform as promised. labor laws, environmental laws (if applicable), etc. You will also need to consider the implications of transfer pricing laws and international laws dictating the use of/sharing of data across borders. • R&D cost beneï¬ts: The acquisition target may hold The ability to successfully integrate the assets. History shows that integration can be the toughest hurdle to clear, tripping up even highly experienced companies. Not only must the acquired assets be woven into existing operations, but people, company appeal based on the cost benefits it can deliver from cultures, financial reporting, infrastructure, and other an R&D perspective. The acquisition may allow you components need to be combined as well.

Even under to spread your R&D costs across a broader product/ ideal circumstances, integration places significant stress earnings base or purchase a specific set of R&D on organizational systems. opportunities/pipeline. Estimates suggest that 50 to 80% of all acquisitions that Selecting the right ï¬nancing strategy. Sometimes, fail do so because the companies are not well integrated. financing acquisitions directly from operations Given this, the acquiring company needs to focus on the makes perfect sense. However, there may be more integration process very early on, and well before the beneficial alternatives.

Financing transactions is best acquisition. From the moment the deal closes, the business accomplished by people who have successfully done needs to be able to start running on a combined basis. it. Don’t have the bench-strength to tap the capital markets? Consider outsourcing it. 8 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change .

Legislative Updates Key Extensions in the PATH Act The budget agreement signed by the president at Companies with employees developing new products the close of 2015 (the “Protecting Americans from Tax or processes in the United States can be eligible for Hikes Act of 2015”) included the permanent extension the R&D credit. For example, companies that have of two tax credits that are particularly relevant to improved their products (new functionality, higher technology companies. The first is the research and quality, better performance), created new products development tax credit. This tax credit is equal to (or software), or automated their manufacturing the difference between the current year’s qualified lines may be eligible to take this credit.

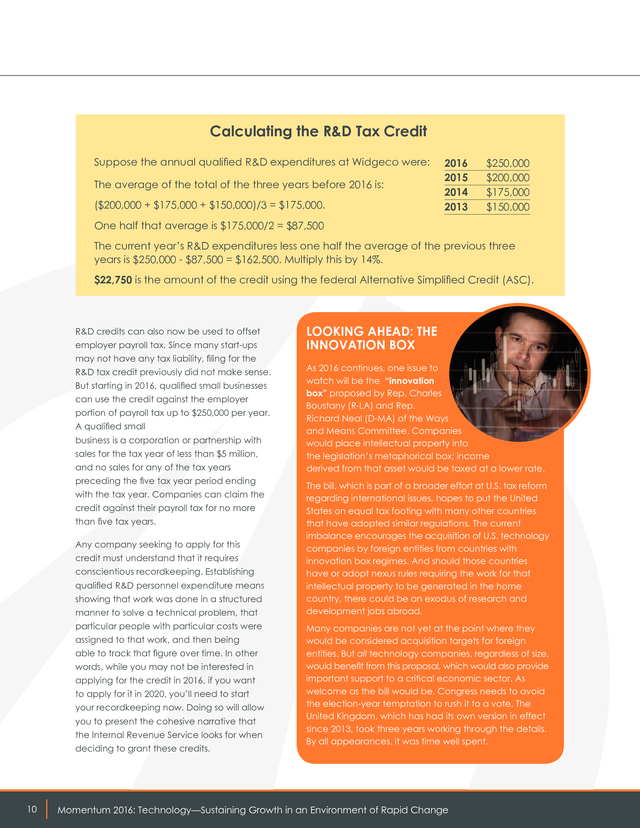

Eligible costs expenditure on R&D personnel and supplies and include wages of those employees, supplies, and costs one-half the average of the R&D expenditure of the related to contract research. Two basic forms of the previous three years (see box for example on the next credit exist—the regular credit and the alternative page). In addition, non-public companies with less simplified credit (ASC).

A company can select the than an average of $50 million in revenue over the ASC computation when the traditional R&D tax credit last three years can also use the credit against the computation excludes it from receiving tax credits. alternative minimum tax. There are two significant enhancements to the R&D This tax credit is a great help for any company credit in 2016 that companies should be aware of. focused on innovation or process improvement. As discussed, many small businesses can now use the Making it permanent removes the uncertainty that R&D credit against the alternative minimum tax (AMT). made it difficult for companies to incorporate this Eligible businesses are non-publicly traded companies credit into long-term planning and budgeting. with less than $50 million in sales averaged over the prior three years. A CohnReznick Report 9 . Calculating the R&D Tax Credit Suppose the annual qualified R&D expenditures at Widgeco were: The average of the total of the three years before 2016 is: ($200,000 + $175,000 + $150,000)/3 = $175,000. 2016 $250,000 2015 $200,000 2014 $175,000 2013 $150,000 One half that average is $175,000/2 = $87,500 The current year’s R&D expenditures less one half the average of the previous three years is $250,000 - $87,500 = $162,500. Multiply this by 14%. $22,750 is the amount of the credit using the federal Alternative Simplified Credit (ASC). R&D credits can also now be used to offset employer payroll tax. Since many start-ups may not have any tax liability, filing for the R&D tax credit previously did not make sense. But starting in 2016, qualified small businesses can use the credit against the employer portion of payroll tax up to $250,000 per year. A qualified small business is a corporation or partnership with sales for the tax year of less than $5 million, and no sales for any of the tax years preceding the five tax year period ending with the tax year. Companies can claim the credit against their payroll tax for no more than five tax years. Any company seeking to apply for this credit must understand that it requires conscientious recordkeeping.

Establishing qualified R&D personnel expenditure means showing that work was done in a structured manner to solve a technical problem, that particular people with particular costs were assigned to that work, and then being able to track that figure over time. In other words, while you may not be interested in applying for the credit in 2016, if you want to apply for it in 2020, you’ll need to start your recordkeeping now. Doing so will allow you to present the cohesive narrative that the Internal Revenue Service looks for when deciding to grant these credits. 10 LOOKING AHEAD: THE INNOVATION BOX As 2016 continues, one issue to watch will be the “innovation box” proposed by Rep.

Charles Boustany (R-LA) and Rep. Richard Neal (D-MA) of the Ways and Means Committee. Companies would place intellectual property into the legislation’s metaphorical box; income derived from that asset would be taxed at a lower rate. The bill, which is part of a broader effort at U.S. tax reform regarding international issues, hopes to put the United States on equal tax footing with many other countries that have adopted similar regulations.

The current imbalance encourages the acquisition of U.S. technology companies by foreign entities from countries with innovation box regimes. And should those countries have or adopt nexus rules requiring the work for that intellectual property to be generated in the home country, there could be an exodus of research and development jobs abroad. Many companies are not yet at the point where they would be considered acquisition targets for foreign entities.

But all technology companies, regardless of size, would benefit from this proposal, which would also provide important support to a critical economic sector. As welcome as the bill would be, Congress needs to avoid the election-year temptation to rush it to a vote. The United Kingdom, which has had its own version in effect since 2013, took three years working through the details. By all appearances, it was time well spent. Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change .

Another permanent extension included in the budget bill provides a 100 percent tax exemption from gains from the sale of Qualiï¬ed Small Business Stock (“QSBS” or “Section 1202”). This makes taking equity investments in new ventures and small businesses more attractive. As compelling as this provision is, it does require some forethought and decision making. For example, since the investment must be in C Corporation, entrepreneurs will have another issue to weigh in terms of the tax implications of corporate formation. Specifically, establishing the company as a “pass-through” (e.g.

partnerships, LLCs or S corporations) may not be as attractive if the main focus is ultimate tax savings upon exit since formation as a C-corporation could save millions of dollars in capital gains taxes when company stock is sold. (Note, there is a limit to the amount that is excluded from tax. It is the greater of $10 million or 10 times the original cost basis of the investment.) It is also important for investors to be informed about the benefits available to them under Section 1202 as it can significantly affect investment decisions. Prior to the PATH ACT, some investors were hesitant to pursue this type of investment due to the uncertainty on whether the provision would be extended.

With the passage of the PATH Act, it may be more advantageous to pursue an equity transaction rather than a debt transaction. For example, imagine an investor is issued preferred stock in exchange for a $3 million investment in a QSB. The investor meets the requisite holding period, and then sells the stock for $30 million.

Eligibility for the 100% capital gains exclusion under Section 1202 could result in tax savings in excess of $7 million. However, if the same investor is issued convertible debt in exchange for the same $3 million initial investment, a minimum selling price of at least $36 million would be required to achieve the same return on investment. There are also noteworthy implications for company employees. For example, a software developer is granted QSBS for services performed, meets the requisite holding period, and then sells the stock for $10 million. The developer may also be eligible for the 100% capital gains exclusion under Section 1202.

This effectively could mean more than $2.5 million in tax savings. On the other hand, if the same employee was granted stock options that remained un-exercised until the date of the stock sale, the gain would be subject to the ordinary “The PATH Act removed a longstanding road block that prevented small businesses from using the R&D tax credit.” Scott Hamilton, Partner Research and Development Group income tax rate. The R&D and Section 1202 tax credits are not for everyone. However, company decision makers need to be fully educated regarding the options to avoid regretting not taking an optimal path that required advance planning. A CohnReznick Report 11 . Conclusion The past several years have been very good for the technology sector. We see no reason that this will not continue through the remainder of 2016. While capital raising opportunities should remain plentiful, investors will be more discerning at all levels of the capital stack. Technology companies should respond by redoubling their efforts to unglamorous but essential tasks—ensuring that they continue to build a strong foundation for growth, strengthen their management teams, have rigorous and scalable compliance mechanisms, and take an appropriately strategic—not just technological—approach to leveraging digital capabilities and cybersecurity programs.

2016 may also be an opportune time to evaluate accelerating growth or strengthening your company through the acquisition of a key competitor. Companies that make investments while conditions are relatively positive will be in a position to ride out uncertainties that might arise in 2016 and beyond. Just as important, they will be building a foundation that will allow them to keep their focus on where it needs to be: refining and executing their vision. Build it and they will come. But build it strong and sustainable, and they will come in droves. 12 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change .

About CohnReznick’s Technology Practice Members of CohnReznick’s Technology Industry Practice Leadership team include: Jeffrey Bobrosky 818-205-2640 Jeffrey.Bobrosky@CohnReznick.com Alex Castelli 703-744-6708 Alex.Castelli@CohnReznick.com Mark Hooley 858-300-3420 Mark.Hooley@CohnReznick.com Stephen Jackson 959-200-7112 Stephen.Jackson@CohnReznick.com Asael Meir 516-336-5515 Asael.Meir@CohnReznick.com Ravi Raghunathan 973-364-7826 Ravi.Raghunathan@CohnReznick.com About CohnReznick’s Technology Industry Practice CohnReznick’s Technology Industry Practice assists private, public, and investor-backed companies at each stage of their lifecycles. Technology clients are served by a team of partner-led professionals who have extensive knowledge of industry-specific accounting and tax issues. As such, we are instrumental in helping clients understand the financial and operational risks and rewards inherent in most business decisions. With contacts throughout the investment and banking communities, CohnReznick can help make introductions to venture capital firms, private equity groups, and strategic investors. CohnReznick Advantage for the Technology Industry • Industry Insights, Optimized Solutions – We understand the accounting, tax, and business issues facing technology companies through start-up, growth, and late stage development and offer solutions, best practices, and ideas to help attract investors, minimize risks, and identify and maximize opportunity. • Transformative Advice – Timely and proactive observations are introduced concerning technology industry trends and technical accounting and tax issues, such as raising venture capital, crowdfunding, internet sales tax regulations, and others tailored to growing technology companies. • Responsive Culture – To keep pace with the speed of the industry, our partners are accessible and appreciate the need for timely and efficient responses to founder, investor, and management requests. • Capital Markets Dexterity – We help clients understand, prepare for, and maximize value from a liquidity event or capital raise.

We can introduce them to the appropriate funding sources, including venture capital, private equity, and strategic investors. • Proactive, Resourceful Service – Partner-led service teams understand the unique nature of the technology industry offering value-added resources throughout the engagement. • National with Global Reach – Companies with international interests are served seamlessly and cost-efficiently through our affiliation with Nexia International, a top 10 worldwide network of accounting firms. A CohnReznick Report 13 . About CohnReznick CohnReznick LLP is one of the top accounting, tax, and advisory firms in the United States, combining the resources and technical expertise of a national firm with the hands-on, entrepreneurial approach that today’s dynamic business environment demands. Headquartered in New York, NY, and with offices nationwide, CohnReznick serves a large number of diverse industries and offers specialized services for middle market and Fortune 1000 companies, private equity and financial services firms, technology companies, government agencies, life sciences companies, and not-for-profit organizations. The Firm, with origins dating back to 1919, has more than 2,700 employees including nearly 300 partners and is a member of Nexia International, a global network of independent accountancy, tax, and business advisors. 14 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change . @CR_TechInd 1301 Avenue of the Americas New York, NY 10019 212-297-0400 www.cohnreznick.com CohnReznick is an independent member of Nexia International CohnReznick LLP © 2016 Any advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues. Nor is it sufficient to avoid tax-related penalties. This has been prepared for information purposes and general guidance only and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is made as to the accuracy or completeness of the information contained in this publication, and CohnReznick LLP, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. .

Preface To grow at a sustainable level, a company needs more than the execution of an innovative idea. It requires focus on key issues like accessing growth capital, cash management, building a strong management team, designing efficient operating systems, and paying careful attention to compliance issues. While new and innovative technology is critical for a company’s success, we cannot minimize the importance of building a solid foundation to support sustainable growth. Having the right people, systems, and processes in place also puts a company in a position of strength when the time is right to evaluate and potentially pursue a liquidity event. While 2016 may turn out to be the year that technology firms say goodbye to sky-high valuations and limitless options for capital raising, it may still be a time of remarkable opportunity. Despite an IPO market that has all but dried up, strong, well-positioned companies will continue to be funded or viewed as prized acquisition targets. M&A activity should remain at a robust pace.

The investors are still out there—with capital available for the right opportunity. To this end, the 2016 edition of Momentum: Technology Outlook focuses on some of the key issues and recommended strategies in fundraising and business strategy, as well as new legislative developments that will impact the way technology companies do business. These are among the things that need to be on your agenda in the year ahead. We hope you find this document, which represents the collective insights of the members of CohnReznick’s Technology Practice, to be a thought-provoking commentary on the state of the industry and helpful to you as you seek to plot your own course. We look forward to your thoughts and to discussing the issues it raises. Alex Castelli, CPA Partner Technology Industry Practice Leader March 2016 Alex Castelli . Sustaining Growth in an Environment of Rapid Change Capital Raising In 2015, capital raising activities in the public markets There is no doubt that, within the technology industry, were strongly influenced by increasing volatility and a the giddiness of the last few years has evaporated. But lack of investor confidence. Unfortunately, these same this is not a bad thing—exuberance is hard to sustain conditions have followed us into 2016. We are hopeful and, in any event, makes for poor strategy.

More that, as the year progresses, stability and investor importantly, three fundamental drivers remain intact: confidence return to the markets. When they do, the number of capital raising opportunities for • The infiltration of technology into every aspect growth-oriented companies will certainly increase. of our businesses and our lives—from managing For now, market conditions continue to be volatile. unabated, having long ago reached a momentum The IPO window, although not formally closed, that feeds on itself. certainly seems that way. And despite the fact that middle market technology companies have become increasingly less dependent on the IPO as a source of capital, the level of IPO activity has broad market implications.

It impacts both valuations and M&A transaction activity. Three months into 2016, we still supply chains to ordering dinner—continues to grow • The readiness of mature technology companies to turn to acquisition continues, either as a growth strategy when they cannot maintain a healthy growth rate organically, or as part of a strategic plan to enter or dominate markets. await the first technology sector IPO. A CohnReznick Report 1 . • The reduced number of investment options for financial and strategic investors in the low interest rate environment, combined with large cash reserves, means that sound technology companies will remain attractive investments, even if at more modest valuations. For our clients, this environment brings several clear directives. Companies must turn their focus inward, away from valuations and exit strategies and toward controlling costs, optimizing operations, and solidifying their customer base. The default stance toward raising capital in 2016 needs to be “How much do we really need?” rather than, as in prior years, “How much can we get?” But this refocusing on long-term strategy is not a retreat, or even necessarily a slowing down. “When raising capital in 2016, companies should ask ‘How much do we really need?’—not ‘How much can we get?’” Alex Castelli, Partner Technology Industry Practice Leader Indeed, it may be that a company’s strategy for growth in this changing environment requires it to become more aggressive in its business strategy—perhaps even becoming an acquirer rather than a target. However, before an enterprise decides to move forward, it is important that it build a solid foundation to support its strategic plan. This may involve the examination of a variety of issues and options such as evaluating gaps in your management team, reviewing your corporate structure, and analyzing your tax strategy.

A failure to address these matters can have significant implications down the line. 2 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change . Sustaining Growth in an Environment of Rapid Change Business Strategy Digital Transformation— Eating Your Own Dog Food The less-heady reality of 2016 demands that companies increase focus on their current businesses. But what is true for a technology company’s clients is true for the tech space in general. In today’s world, the traditional five-year strategic business plan has been replaced by a five-month plan that is constantly Fortunately, while managing the process of customer conversion and operations optimization has become much more complex, the analytic tools available to generate insights, drive business strategy, and improve every aspect of the customer experience have more than kept pace. Companies, therefore, should view digital transformation as an exciting opportunity to bring an innovation orientation to all that they do. being revised in the face of changing markets, But the fact is that the process of digital transformation better informed customers, new opportunities, and can be easy to do incorrectly, even for technology new threats. While many companies have adopted companies.

Digital transformation requires enterprises an agile mindset in application development, their to rethink at a very fundamental level what it is they approach to key functions like marketing, customer are trying to accomplish and why—especially when retention, and operations is often stuck in the analog the default approach in business often is to focus era. To reprise a saying from the early dot-com days, immediately on how to get something done. The technology companies need to make sure they are result is a great deal of effort on traditional initiatives eating their own dog food. like upgrading ERP and CRM platforms with very little A CohnReznick Report 3 .

“Businesses with a digital purpose will outperform those focused solely on the bottom line.” Paul Gulbin, Managing Director, Digital and Innovation Services When a consumer is offered the opportunity to log onto a company website using a LinkedIn profile instead of typing in a username and password, the company is granted permission to access a wealth of information about that consumer. What is their current employment position? Which associations do they belong to? What kinds of jobs have they had? By gaining access to this kind of lifestyle information, companies can better target their product and service offerings to the consumer’s specific background and degree of influence at the company. This information also gives companies critical information to develop new products and energy given to underlying questions such as how services designed to better address these needs. the lives and expectations of customer personas are Companies such as Salesforce.com changing and which digital strategies can bring us and Gigya are enjoying new levels of success using closer to becoming a critical part of the customer these approaches. experience in real time. The second “customer first” strategy is the use of These questions are important to answer because omnichannel digital commerce to build lasting brand they point toward strategic opportunities, uncover relationships with customers. Digital commerce once inefficiencies, and help mitigate risks.

Take the meant shopping cart conversion, e-coupons, and customer conversion example. The enterprise online payment tools. Today, digital commerce reporting systems for technology companies can has evolved into creating and fostering online provide a false sense of security regarding their communities with customers, using tools such as customer base.

Since ERP and basic CRM do video chat for assisted selling, social network product not harness enough information to understand a reviews and brand advocacy, and service taking on a customer’s interests, likes, and specific attributes, a role in multi-channel lead management. Omnichannel seamless customer experience with the brand will 2.0 is about using digital commerce as a means to remain out of reach. In short, digital transformation help companies generate revenue by enabling them requires “customer first” type of thinking that keeps to build meaningful, two-way relationships with their organizations prioritized on the things that will actually consumers or business customers.

These relationships drive conversion, loyalty, or both. are fostered across multiple retail, wholesale, mobile, There are two significant “customer first” digital strategies that smart companies are now employing. and direct/indirect sales channels, through call centers, and through other digital platforms. The first is personalization. With the continued rise of Companies such as Burberry and Leviev Jewelry are Facebook, LinkedIn, and other social media outlets, growing and outperforming their competitors using consumers are taking a more proactive approach personalization and omnichannel 2.0 digital strategies in sharing certain types of personal data with each to create lasting relationships with their customers. other and with the companies they do business with. These and other innovative companies are leveraging In response, companies have begun to execute digital transformation at the highest level—reinventing permission-based data collection protocols on their the way companies sell to, and retain, their customers. websites and other digital communication tools. 4 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change . While each enterprise’s path toward digital transformation will be different, our experience in helping companies achieve digital leadership suggests that there are three fundamental requirements: A strong vision: Being an agile enterprise demands a great deal of comfort with uncertainty, as strategies get revised in the face of new information and market changes. This makes it all the more important for management to have a strong vision for the company’s products—not in terms of the specifics, which will change over time, but for the problems the products will solve and the value they will add. Freedom from legacy silos: Digitally agile organizations are able to routinely innovate because they continually combine insights and perspectives from across the organization. Similarly, they are able to create holistic experiences because they are always focused on the big picture. In practice, this means that marketing, product development, sales, and other functions are not merely exchanging information but working as part of front-line operational teams. Constant feedback and learning: This is at the heart of digital transformation.

It means, for example, not just having excellent customer service, but using it as an intelligence tool to gather ongoing insight for product development. It means not just creating a robust social media presence, but monitoring and analyzing traffic and then becoming part of the conversation. Above all, digital transformation requires the structure and culture necessary to support this torrent of inputs and the discussions and recalibrations that follow. Cybersecurity: Everyone Is a Target The continued digital disruption of almost all industries, combined with increased interconnectivity between individuals and between organizations, has made cybersecurity an ongoing strategic issue for nearly every enterprise.

Technology companies, however, have an additional layer of concern because of the role their products play within the digital ecosystem. “Many companies think of cybersecurity in terms of ï¬rewalls and encryption protocols— while it is actually a broader business risk issue.” After all, cybercriminals who can breach a technology platform or device can often gain access to an entire organization’s data, and also quite possibly the data of every organization Jim Ambrosini, Managing Director Cybersecurity that uses those products. A CohnReznick Report 5 . While many companies understand this in theory, we have found that mid-market technology companies—those at the front lines of entrepreneurialism and innovation—can sometimes be less savvy in protecting their own data. These companies often think of cybersecurity in a fragmented way—having the right firewalls, encryption protocols, and so forth—rather than having a broader, enterprise cyber program and strategy. Because of their inherent tech savviness, it is easy for them to be strong on the infrastructure side of data protection. The fact is, however, that having technology controls is only one element of the cybersecurity process. There is also the organizational component, covering the security of the network of business partners and developing a comprehensive breach response plan.

And there is a strategic component which includes understanding how cybersecurity integrates with the business and accurately assesses the organization’s threat profile. It is here where technology companies can find their cybersecurity program lacking. In order to ensure cybersecurity preparedness, companies need to take these three steps: Look across your product development chain. Best practice cybersecurity is part of product development lifecycle from coding to delivery.

This means assessing both security within the product itself and in how the product is developed and distributed—particularly if your organization uses a third-party as part of the process. Know your Information assets. The first step in any cybersecurity program is to make sure you have an inventory of your information systems (servers, databases) and an understanding of the type of data that the systems contain (corporate data, personal data, intellectual property, etc.). From here, your company can then build a robust cyber program that includes not only protecting its data, but having the ability to identify threats proactively as well as being able to properly respond to and recover from a data breach. Know your risks and create your cyber program accordingly. Ultimately, cybersecurity is a business risk decision.

A company needs to understand who wants to attack it and the likely ways in which an attacker could access data. Then, the company must align its cybersecurity program to the risk it is willing to accept. Too often, organizations may invest in a cybersecurity solution that is not aligned to the threats they face, or worse, they have underdeveloped, or incomplete programs. 6 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change . Sustaining Growth in an Environment of Rapid Change Is Now the Time to Acquire Another Company? Companies that sit on the other side of the M&A table its competitors, suppliers, and others. In fact, the need to be aware that making an acquisition is likely conversations and interactions you have with other to require new capabilities. After all, they will now firms can provide a good opportunity to segue into be competing against both strategic and financial corporate development discussions. Acquiring a investors with a great deal of experience.

Breaking into business process, people, or product from another the acquirer class requires several things, including: company may to be the ideal strategy in taking your Clearly establishing your objective. It is critical that company to the next level. you have a clearly set goal for the acquisition based Conducting rigorous due diligence. As an acquirer, on your company’s growth objectives.

You must a company needs the intelligence to make informed understand the potential of the acquisition and how risk/reward decisions. Each acquisition will require it will fit into your company’s vision. Will a particular a comprehensive evaluation of historic financial acquisition help you become a dominant player in a performance, key business drivers, profitability trends, particular industry or sector, or is the acquisition meant and areas of potential risk for the target.

This process is to diversify your company’s portfolio? Are you primarily most critical when the target is smaller or less mature. interested in acquiring specific assets (trademarks, Their financial and internal control systems may be less intellectual property, patents, etc.) from the other sophisticated and the information provided may be company or is the acquisition intended to make better less transparent. use of your own internal intellectual property? There are a number of other key factors related to the Identifying the universe of potential targets. In assessing acquisition target that should be reviewed as part of targets, your company may have a solid grasp of the due diligence process. These include: A CohnReznick Report 7 .

• Reputation: You need to understand how the target company is perceived in the industry and which “intangibles” are associated with the current organization, its owners, its product line, etc. If your acquisition target is an “unknown” entity with a good product, you will need to understand where monies may need to be spent in creating brand name recognition (this may not be critical if your company already has strong brand recognition in the marketplace). “A company must clearly establish its goal for an acquisition and understand how it ï¬ts into the overall vision.” Mario Pompeo, Partner CFO Advisory Practice Leader • Management team: Does the target company have a strong management team and have you gotten to know them during the merger / acquisition process? Also, avoid getting get caught up in the “auction You also need to assess whether your existing team frenzy” that can occur for a prized acquisition target. is prepared to assume responsibility for running the Savvy sellers and/or their investors will often behave in target company’s operations unless you are actually a way to drive up the price, causing potential buyers to acquiring the “know how” of the organization. care more about winning the deal than the economics You also need to determine if the company’s of the deal. You should establish price parameters and management team’s skills are complementary to, stick to them. or symbiotic with, your own internal management’s strengths. Lastly, the personal chemistry between the buyer and seller is often a key indicator of the ultimate success of the acquisition.

This is especially true if any of the acquired company’s management team is being retained after the deal closes. • Foreign vs. domestic targets: If you are considering the Establishing the purchase price and financing the deal are two critical considerations. You will need to consider a number of factors including financing terms (i.e., purchase price plus an earn out, etc.), and the acquisition company’s current EBITDA or other multiples for targets in similar industries.

Especially in cases where you can’t agree on a price with the seller, you should consider acquisition of a foreign company, you must be aware using earn-outs to defer payments if the potential that there may be differences in accounting standards, acquisition target does not perform as promised. labor laws, environmental laws (if applicable), etc. You will also need to consider the implications of transfer pricing laws and international laws dictating the use of/sharing of data across borders. • R&D cost beneï¬ts: The acquisition target may hold The ability to successfully integrate the assets. History shows that integration can be the toughest hurdle to clear, tripping up even highly experienced companies. Not only must the acquired assets be woven into existing operations, but people, company appeal based on the cost benefits it can deliver from cultures, financial reporting, infrastructure, and other an R&D perspective. The acquisition may allow you components need to be combined as well.

Even under to spread your R&D costs across a broader product/ ideal circumstances, integration places significant stress earnings base or purchase a specific set of R&D on organizational systems. opportunities/pipeline. Estimates suggest that 50 to 80% of all acquisitions that Selecting the right ï¬nancing strategy. Sometimes, fail do so because the companies are not well integrated. financing acquisitions directly from operations Given this, the acquiring company needs to focus on the makes perfect sense. However, there may be more integration process very early on, and well before the beneficial alternatives.

Financing transactions is best acquisition. From the moment the deal closes, the business accomplished by people who have successfully done needs to be able to start running on a combined basis. it. Don’t have the bench-strength to tap the capital markets? Consider outsourcing it. 8 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change .

Legislative Updates Key Extensions in the PATH Act The budget agreement signed by the president at Companies with employees developing new products the close of 2015 (the “Protecting Americans from Tax or processes in the United States can be eligible for Hikes Act of 2015”) included the permanent extension the R&D credit. For example, companies that have of two tax credits that are particularly relevant to improved their products (new functionality, higher technology companies. The first is the research and quality, better performance), created new products development tax credit. This tax credit is equal to (or software), or automated their manufacturing the difference between the current year’s qualified lines may be eligible to take this credit.

Eligible costs expenditure on R&D personnel and supplies and include wages of those employees, supplies, and costs one-half the average of the R&D expenditure of the related to contract research. Two basic forms of the previous three years (see box for example on the next credit exist—the regular credit and the alternative page). In addition, non-public companies with less simplified credit (ASC).

A company can select the than an average of $50 million in revenue over the ASC computation when the traditional R&D tax credit last three years can also use the credit against the computation excludes it from receiving tax credits. alternative minimum tax. There are two significant enhancements to the R&D This tax credit is a great help for any company credit in 2016 that companies should be aware of. focused on innovation or process improvement. As discussed, many small businesses can now use the Making it permanent removes the uncertainty that R&D credit against the alternative minimum tax (AMT). made it difficult for companies to incorporate this Eligible businesses are non-publicly traded companies credit into long-term planning and budgeting. with less than $50 million in sales averaged over the prior three years. A CohnReznick Report 9 . Calculating the R&D Tax Credit Suppose the annual qualified R&D expenditures at Widgeco were: The average of the total of the three years before 2016 is: ($200,000 + $175,000 + $150,000)/3 = $175,000. 2016 $250,000 2015 $200,000 2014 $175,000 2013 $150,000 One half that average is $175,000/2 = $87,500 The current year’s R&D expenditures less one half the average of the previous three years is $250,000 - $87,500 = $162,500. Multiply this by 14%. $22,750 is the amount of the credit using the federal Alternative Simplified Credit (ASC). R&D credits can also now be used to offset employer payroll tax. Since many start-ups may not have any tax liability, filing for the R&D tax credit previously did not make sense. But starting in 2016, qualified small businesses can use the credit against the employer portion of payroll tax up to $250,000 per year. A qualified small business is a corporation or partnership with sales for the tax year of less than $5 million, and no sales for any of the tax years preceding the five tax year period ending with the tax year. Companies can claim the credit against their payroll tax for no more than five tax years. Any company seeking to apply for this credit must understand that it requires conscientious recordkeeping.

Establishing qualified R&D personnel expenditure means showing that work was done in a structured manner to solve a technical problem, that particular people with particular costs were assigned to that work, and then being able to track that figure over time. In other words, while you may not be interested in applying for the credit in 2016, if you want to apply for it in 2020, you’ll need to start your recordkeeping now. Doing so will allow you to present the cohesive narrative that the Internal Revenue Service looks for when deciding to grant these credits. 10 LOOKING AHEAD: THE INNOVATION BOX As 2016 continues, one issue to watch will be the “innovation box” proposed by Rep.

Charles Boustany (R-LA) and Rep. Richard Neal (D-MA) of the Ways and Means Committee. Companies would place intellectual property into the legislation’s metaphorical box; income derived from that asset would be taxed at a lower rate. The bill, which is part of a broader effort at U.S. tax reform regarding international issues, hopes to put the United States on equal tax footing with many other countries that have adopted similar regulations.

The current imbalance encourages the acquisition of U.S. technology companies by foreign entities from countries with innovation box regimes. And should those countries have or adopt nexus rules requiring the work for that intellectual property to be generated in the home country, there could be an exodus of research and development jobs abroad. Many companies are not yet at the point where they would be considered acquisition targets for foreign entities.

But all technology companies, regardless of size, would benefit from this proposal, which would also provide important support to a critical economic sector. As welcome as the bill would be, Congress needs to avoid the election-year temptation to rush it to a vote. The United Kingdom, which has had its own version in effect since 2013, took three years working through the details. By all appearances, it was time well spent. Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change .

Another permanent extension included in the budget bill provides a 100 percent tax exemption from gains from the sale of Qualiï¬ed Small Business Stock (“QSBS” or “Section 1202”). This makes taking equity investments in new ventures and small businesses more attractive. As compelling as this provision is, it does require some forethought and decision making. For example, since the investment must be in C Corporation, entrepreneurs will have another issue to weigh in terms of the tax implications of corporate formation. Specifically, establishing the company as a “pass-through” (e.g.

partnerships, LLCs or S corporations) may not be as attractive if the main focus is ultimate tax savings upon exit since formation as a C-corporation could save millions of dollars in capital gains taxes when company stock is sold. (Note, there is a limit to the amount that is excluded from tax. It is the greater of $10 million or 10 times the original cost basis of the investment.) It is also important for investors to be informed about the benefits available to them under Section 1202 as it can significantly affect investment decisions. Prior to the PATH ACT, some investors were hesitant to pursue this type of investment due to the uncertainty on whether the provision would be extended.

With the passage of the PATH Act, it may be more advantageous to pursue an equity transaction rather than a debt transaction. For example, imagine an investor is issued preferred stock in exchange for a $3 million investment in a QSB. The investor meets the requisite holding period, and then sells the stock for $30 million.

Eligibility for the 100% capital gains exclusion under Section 1202 could result in tax savings in excess of $7 million. However, if the same investor is issued convertible debt in exchange for the same $3 million initial investment, a minimum selling price of at least $36 million would be required to achieve the same return on investment. There are also noteworthy implications for company employees. For example, a software developer is granted QSBS for services performed, meets the requisite holding period, and then sells the stock for $10 million. The developer may also be eligible for the 100% capital gains exclusion under Section 1202.

This effectively could mean more than $2.5 million in tax savings. On the other hand, if the same employee was granted stock options that remained un-exercised until the date of the stock sale, the gain would be subject to the ordinary “The PATH Act removed a longstanding road block that prevented small businesses from using the R&D tax credit.” Scott Hamilton, Partner Research and Development Group income tax rate. The R&D and Section 1202 tax credits are not for everyone. However, company decision makers need to be fully educated regarding the options to avoid regretting not taking an optimal path that required advance planning. A CohnReznick Report 11 . Conclusion The past several years have been very good for the technology sector. We see no reason that this will not continue through the remainder of 2016. While capital raising opportunities should remain plentiful, investors will be more discerning at all levels of the capital stack. Technology companies should respond by redoubling their efforts to unglamorous but essential tasks—ensuring that they continue to build a strong foundation for growth, strengthen their management teams, have rigorous and scalable compliance mechanisms, and take an appropriately strategic—not just technological—approach to leveraging digital capabilities and cybersecurity programs.

2016 may also be an opportune time to evaluate accelerating growth or strengthening your company through the acquisition of a key competitor. Companies that make investments while conditions are relatively positive will be in a position to ride out uncertainties that might arise in 2016 and beyond. Just as important, they will be building a foundation that will allow them to keep their focus on where it needs to be: refining and executing their vision. Build it and they will come. But build it strong and sustainable, and they will come in droves. 12 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change .

About CohnReznick’s Technology Practice Members of CohnReznick’s Technology Industry Practice Leadership team include: Jeffrey Bobrosky 818-205-2640 Jeffrey.Bobrosky@CohnReznick.com Alex Castelli 703-744-6708 Alex.Castelli@CohnReznick.com Mark Hooley 858-300-3420 Mark.Hooley@CohnReznick.com Stephen Jackson 959-200-7112 Stephen.Jackson@CohnReznick.com Asael Meir 516-336-5515 Asael.Meir@CohnReznick.com Ravi Raghunathan 973-364-7826 Ravi.Raghunathan@CohnReznick.com About CohnReznick’s Technology Industry Practice CohnReznick’s Technology Industry Practice assists private, public, and investor-backed companies at each stage of their lifecycles. Technology clients are served by a team of partner-led professionals who have extensive knowledge of industry-specific accounting and tax issues. As such, we are instrumental in helping clients understand the financial and operational risks and rewards inherent in most business decisions. With contacts throughout the investment and banking communities, CohnReznick can help make introductions to venture capital firms, private equity groups, and strategic investors. CohnReznick Advantage for the Technology Industry • Industry Insights, Optimized Solutions – We understand the accounting, tax, and business issues facing technology companies through start-up, growth, and late stage development and offer solutions, best practices, and ideas to help attract investors, minimize risks, and identify and maximize opportunity. • Transformative Advice – Timely and proactive observations are introduced concerning technology industry trends and technical accounting and tax issues, such as raising venture capital, crowdfunding, internet sales tax regulations, and others tailored to growing technology companies. • Responsive Culture – To keep pace with the speed of the industry, our partners are accessible and appreciate the need for timely and efficient responses to founder, investor, and management requests. • Capital Markets Dexterity – We help clients understand, prepare for, and maximize value from a liquidity event or capital raise.

We can introduce them to the appropriate funding sources, including venture capital, private equity, and strategic investors. • Proactive, Resourceful Service – Partner-led service teams understand the unique nature of the technology industry offering value-added resources throughout the engagement. • National with Global Reach – Companies with international interests are served seamlessly and cost-efficiently through our affiliation with Nexia International, a top 10 worldwide network of accounting firms. A CohnReznick Report 13 . About CohnReznick CohnReznick LLP is one of the top accounting, tax, and advisory firms in the United States, combining the resources and technical expertise of a national firm with the hands-on, entrepreneurial approach that today’s dynamic business environment demands. Headquartered in New York, NY, and with offices nationwide, CohnReznick serves a large number of diverse industries and offers specialized services for middle market and Fortune 1000 companies, private equity and financial services firms, technology companies, government agencies, life sciences companies, and not-for-profit organizations. The Firm, with origins dating back to 1919, has more than 2,700 employees including nearly 300 partners and is a member of Nexia International, a global network of independent accountancy, tax, and business advisors. 14 Momentum 2016: Technology—Sustaining Growth in an Environment of Rapid Change . @CR_TechInd 1301 Avenue of the Americas New York, NY 10019 212-297-0400 www.cohnreznick.com CohnReznick is an independent member of Nexia International CohnReznick LLP © 2016 Any advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues. Nor is it sufficient to avoid tax-related penalties. This has been prepared for information purposes and general guidance only and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is made as to the accuracy or completeness of the information contained in this publication, and CohnReznick LLP, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. .