Description

Wealth Management Guide

Reach your goals

This guide is designed for individuals, families, executives, business

owners, and retirees looking for financial guidance. We compiled our

wealth advisory articles to make it easy for you to gain insights on a

variety of related topics, including retirement, investing for the long

term, life insurance, estate and gift planning, business transitions,

risk management, and key tax information for 2014 and 2015.

CLAconnect.com/privateclient

©2015 CliftonLarsonAllen LLP

. Table of Contents

Page 1

Page 17

Page 2

Page 18

Planning for a Meaningful

Retirement Starts With a Vision

Using a Trust in Financial Planning:

Nonfinancial Questions to Consider

Achieve Your Retirement Vision:

Focus on What You Can Control

Income Tax Implications of Grantor

and Non-Grantor Trusts

Page 4

Page 20

Your Investment Portfolio, Market

Volatility, and the Sequence

of Returns

Make Use of the Gift Tax Exemption

With Spousal Access Trusts

Page 6

Page 21

Page 8

Page 24

How Domicile is a Wealth Factor

When You Retire to Another State

Credit Shelter Trusts Versus

Portability in Estate Planning

Retirement, Baseball, and the

Real Future of Social Security

You’ve Been Asked to be the

Executor for an Estate. Now What?

Page 25

Page 10

File and Suspend: Maximize Social

Security With Spousal Benefits

Avoid Some of the Pitfalls

of Sudden Wealth With

Proactive Tax Planning

Page 12

Page 27

Deferred Income Annuities Offer

Pension-Like Retirement Benefits

Helpful Steps to Consider

When Selling Your Business

Page 13

Page 29

Life Insurance: A Retirement

Strategy With Tax Savings

for High Earners

Leadership Transition Is a Risk

Management Issue

Page 30

Page 14

Connecting Your Estate

and Financial Plans

Legislation Extends Tax Provisions

for Individuals and Businesses

in 2014

Page 15

Page 32

Tax-Smart Tips for Handling

Your IRA and Estate Plan

Key Information for the

2015 Tax Year

Page 34

CLAconnect.com/privateclient

About CLA

Page 34

Disclosures

©2015 CliftonLarsonAllen LLP

. to continue working. Just “finding something to keep busy”

won’t do for those who have always been goal-oriented

and purposeful.

Choosing a path with a purpose

In order to help our clients start preparing for the next

chapter of their lives, we encourage them to make a list of

10 things they want to accomplish or achieve in their life.

These items do not necessarily have to be monetary; they

can be anything from setting up a nonprofit or foundation,

to learning a language, taking up golf or hunting, beginning

to knit or sew, or traveling.

If you have a partner, he/she should make a separate list.

After both are complete, create a third line-up of goals

you would like to reach together. When that’s done, share

your individual ideas and see where they are similar. The

exercise is designed to get you thinking about dreams that

you have put off because of time constraints or

other factors.

Planning for a

Meaningful Retirement

Begins With a Vision

It’s one thing to talk about what you would like to do in

retirement and another to write it down and hold yourself

accountable.

And there is always satisfaction in knowing that you have accomplished what you set out to do. Creating lists helps you build a framework for how you want to spend your time and ensures that your values align accordingly. The lists also provide guidance as you identify your desired spending needs in retirement. Clearly, traveling to Africa or Europe, or studying pottery in China will take more resources than learning a language or golf. Knowing your projected spending ahead of time allows you to prepare for the retirement you want and to make the necessary changes before it is too late. by Cheryl Starman-Coombs Nearly 10,000 Baby Boomers turn 65 every day, a trend that the Pew Research Center says will continue for the next 20 years.

By 2030, a full 18 percent of Americans will be at retirement age. Some Boomers are wondering if they can afford to leave the workforce; others are confident they have all the financial resources they need. But money is only part of the story. For members of both groups, the first step in achieving independence from a career or business is deciding what they want the years after retirement to look like.

Developing a vision for the future before addressing finances can lead down a more rewarding path. Of course, you’re not going to be able to hit all of the curve balls that life throws at you, so it’s best to keep your vision flexible. At some point your health or other factors may come into play, diverting you from your original course. Be willing to make adjustments, and seek advice to help make sure you’re on the right track.

The way we were The traditional view of aging in America has men and women working until they are in their early to mid-60s, then walking away from it all and beginning a life of leisure and freedom. But for some, reality can be quite different. Retirees often experience depression as they transition from business ownership or a successful career because their work defines a big part of who they are. It doesn’t matter that they have plenty of money; many are at a loss to decide who they want to become and what they want to do with the rest of their lives. What to do about the business By the time you leave full-time employment, you will have spent 40-plus years establishing a working legacy. Developing a vision for the post-career years won’t take nearly as long, but it’s going to take more than a few hours or even a few days.

We’re talking about the rest of your life, so thoughtfully weighing options is vital to drawing the right conclusions. Longer life expectancies are also challenging Boomers to paint a new picture of their golden years. In fact, it is common to hear men and women in their late 50s and early 60s say that they are not ready to leave work. This may not be out of necessity; it is often because they chose CLAconnect.com/privateclient When you begin the process, give yourself (and your partner) time to think about your future.

This is especially true if you are a business owner. In Dancing in the End Zone: The Business Owner’s Exit Planning Playbook, 1 ©2015 CliftonLarsonAllen LLP . author Patrick Ungashick estimates that about 9 million of America’s 15 million business owners were born in or before 1964. That means millions will soon be in a position to transfer business ownership. Unfortunately, Peter Christman, founder of the Exit Planning Institute, estimates that about 75 percent of business owners don’t have an exit plan. Business owners will have additional questions to consider regarding the transition of a business such as: • Sell it to family members, or a third party • Gift outright to family members • Create a plan that combines a sale and gift Achieve Your Retirement Vision: Focus on What You Can Control If you are contemplating a transition to family members, you should consider utilizing a trust. It is important that you consider the permanency and income tax implications of different types of trusts for yourself and the beneficiaries.

Understanding the cash flow from each of these options is critical, in addition to making a decision on how you will or will not stay involved in the business. You could remain the majority owner, but turn day-today operations over to a management team. Maybe you will work part time or as a consultant. These types of arrangements are a compromise between involvement and income, but may be the best route for you to achieve your goals. by Dale Skogstad and Andy Frye How much is enough to retire? This seems like a simple question and ideally there would be a tried-and-true method for coming up with a specific dollar amount that assures you many comfortable and productive postemployment years.

However, there are many variables outside your control that make this question much more difficult to answer, for example, investment returns, inflation, and monetary and fiscal policies. Looking forward with confidence Whether your idea of retirement includes working, volunteering, traveling, or some other activity, it will require a shift in the balance in your current life. Articulating your own unique vision is the first step forward. Once you have established a road map and understand the kind of lifestyle you want to retire to, you can build a financial plan that aligns with your retirement dreams. _____________________________________________ Instead of focusing on what you can’t control, it’s often better to focus on those things you can control. Our article titled “Planning for a Meaningful Retirement Begins With a Vision” discusses how Baby Boomers might address the qualitative issues relating to their retirement by answering questions about specific goals. The next step is to look at quantitative factors, or more specifically, determining how to turn your vision into reality.

This means employing planning and investment strategies that can help maximize your chances of providing for your retirement needs — regardless of what the uncertain future may bring. Cheryl Starman-Coombs, CPA, CFP®, Principal CliftonLarsonAllen Wealth Advisors, LLC cheryl.coombs@CLAconnect.com or 612-376-4520 Table of contents Live within your means Ensuring that your nest egg is able to support you during retirement means making sure you are living within your means. In other words, keep the withdrawals from your portfolio to a sustainable level. Studies suggest that by limiting annual withdrawals to 4 – 5 percent of a portfolio’s value, it is less likely that you will exhaust your assets during your lifetime. CLAconnect.com/privateclient 2 ©2015 CliftonLarsonAllen LLP .

Tax efficient distributions It’s also important that you distribute your investment assets in a tax-efficient manner. By managing the amount of distributions between your pre-tax investments (IRAs and 401(k)s) and after-tax investments, you may be able keep from pushing yourself into a higher tax bracket in any given year. This will help stretch your retirement assets further regardless of your investment returns. Having a mix of both pre-tax and after-tax investments provides you with flexibility to better manage your tax situation during retirement. Generally, this can be a way to gauge whether you are living within your means.

Reducing your expenses to a sustainable level may not be your first choice, but it’s at least something you can control. You’ll probably agree that the sacrifice is preferable to having anxiety about running out of money or taking more risk than you can afford, which could make the situation worse. Manage risk in your portfolio In constructing your investment portfolio, focus on diversification without taking on more risk than you are comfortable with or need. This is especially important in light of the historically low interest rates over the past few years. Maximize your Social Security benefits Many retirees are typically near the age of eligibility to begin collecting Social Security benefits.

Decisions regarding Social Security benefits can be among the most important that retirees control and should be thoughtfully considered. Generally, the most important decision revolves around when to begin taking benefits between age 62 and 70. For married couples, there are a number of sophisticated strategies to maximize benefits and potentially provide greater longevity protection for the surviving spouse. The lack of yields on cash and shorter term fixed income investments make it difficult to get reasonable yields without taking too much risk.

There is temptation to take on more risk than you otherwise might in order to generate returns. While this may be appropriate in some situations, risk should still be evaluated carefully so you don’t take on more than you are able to bear both mentally and financially. It’s also important to consider the impact of negative returns during retirement. In our article “Your Investment Portfolio, Market Volatility, and the Sequence of Returns,” we describe the effect that the timing of investment returns has on the value of a portfolio, especially during the distribution phase.

Unfortunately, investors cannot control the order in which returns are generated by capital markets. As noted in the article, significant negative market returns, especially in the early years of retirement, have a dramatic impact on how long a portfolio might last. A well-diversified, risk-managed portfolio will minimize your chances of this occurring. While the transition to retirement can be a challenge for some, being proactive about strategies you can control — and not focusing on a future you can’t control — should allow you to live your retirement vision with greater confidence. _____________________________________________ Dale Skogstad, CFA, CFP®, Senior Wealth Advisor CliftonLarsonAllen Wealth Advisors, LLC dale.skogstad@CLAconnect.com or 612-397-3105 Andy Frye, CPA, PFS, CFP®, Principal CliftonLarsonAllen Wealth Advisors, LLC andrew.frye@CLAconnect.com or 612-376-4533 Consider using annuities to transfer risk Annuities are a popular strategy that allow you to shift investment risk to an insurance company, and in return, receive a stream of payments for a set number of years or for life. Annuities are typically either fixed or variable. Table of contents With a fixed annuity the insurance company controls the investments and you get a predetermined stream of payments in return.

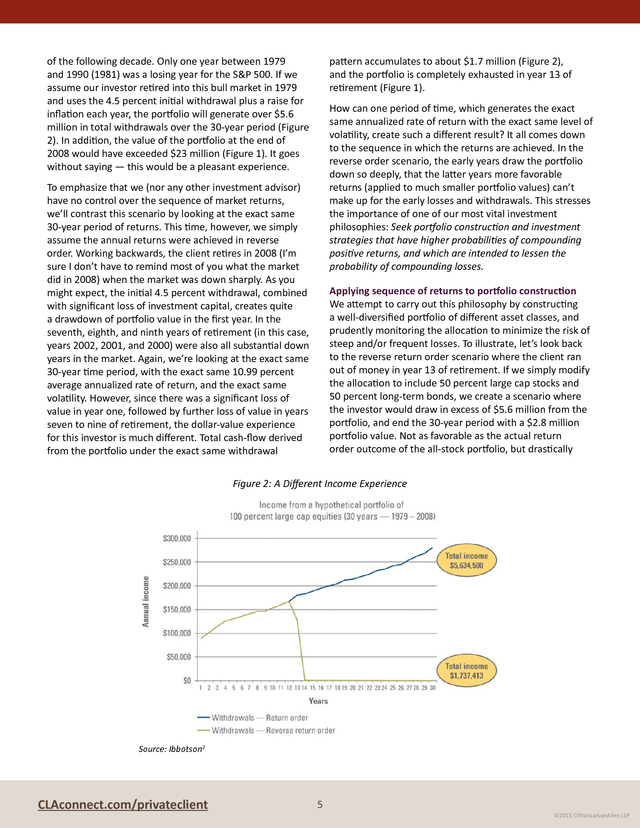

A variable annuity allows you to control the investments and the insurance company typically guarantees a minimum annuity payment. Although variable annuities can be expensive, they may be a good option for a portion of the retirement funds of retirees who want to invest in riskier securities, but still have some risk protection from the guaranteed annuity stream. CLAconnect.com/privateclient 3 ©2015 CliftonLarsonAllen LLP . managing their investments. However, through prudent portfolio construction we can attempt to produce more consistent returns with less volatility. This basic example demonstrates how a well-run, disciplined investment strategy can produce a favorable outcome by minimizing the risks associated with retiring into a bear market. A 30-year example of why the sequence of returns is critical Let’s start our example with a hypothetical portfolio of $2 million in year one of retirement (Figure 1). We will also pick a specific 30-year period of stock market history, 1979 – 2008, which is chosen to illustrate the importance of the sequence of returns.

In the first year, the client decides to take a 4.5 percent initial withdrawal (a modest and sustainable withdrawal rate according to some advisors). Your Investment Portfolio, Market Volatility, and the Sequence of Returns Each year in retirement, the individual will increase the annual distribution amount based on the prior year’s rate of inflation. For example, the second year withdrawal would be about $95,670 ($90,000 X 1.063 to account for 6.3 percent inflation in 1979). The third year withdrawal would be about $101,300 ($95,670 X 1.059).

This pattern continues throughout the 30 years of retirement. To emphasize the impact sequence of returns can have on an investor’s experience, let’s assume the individual decides to invest the entire value of the portfolio in the domestic large cap equity market. by Nate Kublank The impact of our investment policy is based on compounding positive returns and minimizing the frequency of losses. Unfortunately, investors have no control over the order in which the markets will generate returns.

This risk is especially concerning to investors who are in or near the distribution phase of From 1979 – 2008, the stock market (as measured by the S&P 500) returned 10.99 percent per year. As some may recall, 1979 was a good year in the market, as was most Figure 1: A Different Ending Value Experience Source: Ibbotson1 CLAconnect.com/privateclient 4 ©2015 CliftonLarsonAllen LLP . of the following decade. Only one year between 1979 and 1990 (1981) was a losing year for the S&P 500. If we assume our investor retired into this bull market in 1979 and uses the 4.5 percent initial withdrawal plus a raise for inflation each year, the portfolio will generate over $5.6 million in total withdrawals over the 30-year period (Figure 2). In addition, the value of the portfolio at the end of 2008 would have exceeded $23 million (Figure 1).

It goes without saying — this would be a pleasant experience. pattern accumulates to about $1.7 million (Figure 2), and the portfolio is completely exhausted in year 13 of retirement (Figure 1). How can one period of time, which generates the exact same annualized rate of return with the exact same level of volatility, create such a different result? It all comes down to the sequence in which the returns are achieved. In the reverse order scenario, the early years draw the portfolio down so deeply, that the latter years more favorable returns (applied to much smaller portfolio values) can’t make up for the early losses and withdrawals. This stresses the importance of one of our most vital investment philosophies: Seek portfolio construction and investment strategies that have higher probabilities of compounding positive returns, and which are intended to lessen the probability of compounding losses. To emphasize that we (nor any other investment advisor) have no control over the sequence of market returns, we’ll contrast this scenario by looking at the exact same 30-year period of returns.

This time, however, we simply assume the annual returns were achieved in reverse order. Working backwards, the client retires in 2008 (I’m sure I don’t have to remind most of you what the market did in 2008) when the market was down sharply. As you might expect, the initial 4.5 percent withdrawal, combined with significant loss of investment capital, creates quite a drawdown of portfolio value in the first year.

In the seventh, eighth, and ninth years of retirement (in this case, years 2002, 2001, and 2000) were also all substantial down years in the market. Again, we’re looking at the exact same 30-year time period, with the exact same 10.99 percent average annualized rate of return, and the exact same volatility. However, since there was a significant loss of value in year one, followed by further loss of value in years seven to nine of retirement, the dollar-value experience for this investor is much different.

Total cash-flow derived from the portfolio under the exact same withdrawal Applying sequence of returns to portfolio construction We attempt to carry out this philosophy by constructing a well-diversified portfolio of different asset classes, and prudently monitoring the allocation to minimize the risk of steep and/or frequent losses. To illustrate, let’s look back to the reverse return order scenario where the client ran out of money in year 13 of retirement. If we simply modify the allocation to include 50 percent large cap stocks and 50 percent long-term bonds, we create a scenario where the investor would draw in excess of $5.6 million from the portfolio, and end the 30-year period with a $2.8 million portfolio value.

Not as favorable as the actual return order outcome of the all-stock portfolio, but drastically Figure 2: A Different Income Experience Source: Ibbotson2 CLAconnect.com/privateclient 5 ©2015 CliftonLarsonAllen LLP . better than the reverse return order result of the all-stock portfolio — all by simply adding one additional asset class to the investment mix. Even more interesting is the fact that the 50/50 portfolio mix generated a lower annualized rate of return than the 100 percent stock portfolio. In this case, a lower, yet more stable annualized return stream produced a sustainable portfolio. Now imagine the impact of adding many different asset classes with disparate return streams intended to minimize losses. We feel that this disciplined approach to portfolio construction puts investors in the best possible position to weather unpredictable market return streams, creates more consistent results, and takes advantage of the longterm compounding of positive returns. How Domicile Is a Wealth Factor When You Retire to Another State How we can help The next time you’re attempting to evaluate the performance of several different investment managers, be sure to look beyond the annualized rate of return figures. The exact same average rate of return in one case can produce a vastly different outcome in another time period. This is precisely why we feel that you can mitigate the effects of a volatile market with a thoughtfully constructed portfolio and holistic financial planning in order to provide a high probability of meeting your future cash-flow needs and leaving a legacy for the next generation. by Kara Kessinger If you are considering retiring to a state other than where you currently live, understanding where you are a legal resident is critical to mapping out your financial plan. There are two key elements to residency: your domicile and where you actually spend your time.

Understanding these concepts impacts where you pay income tax and other personal financial matters. Reverse return order replicates a bear market followed by a bull market. Analysis occurs in hindsight, bull and bear markets cannot be predicted. Please see endnotes for information about this illustration. It is not possible to invest in an index.

Hypothetical examples are shown for illustrative and educational purposes only. Past performance is no guarantee of future results. 1 Domicile defined Domicile, also called your “state of legal residence,” is your true, fixed, permanent home. It is the place where you intend to return when you are away.

Even if you have more than one home, you will have only one domicile. You do not apply or register anywhere; it is based on facts and circumstances. The use of 4.5 percent for this illustration is not a recommendation of a particular rate; financial advisors and clients should determine the appropriate rate based on individual client situations. Reverse return order replicates a bear market followed by a bull market. Analysis occurs in hindsight, bull and bear markets cannot be predicted.

Please see endnotes for information about this illustration. It is not possible to invest in an index. Hypothetical examples are shown for illustrative and educational purposes only. Past performance is no guarantee of future results. 2 Nate Kublank CFP®, CPWA®, AEP®, Senior Wealth Advisor CliftonLarsonAllen Wealth Advisors, LLC nate.kublank@CLAconnect.com or 608-662-8647 Your domicile is the first factor that determines your residency.

If you are domiciled in a state, you are a resident of that state. Therefore if you are trying to change your residency, know the facts and circumstances that drive your state of domicile and put them in place as soon as possible. Table of contents Your domicile affects the following: _____________________________________________ 1. Your liability for state income taxes 2. Your eligibility for certain state benefits, such as in-state tuition rates, disability benefits, and Medicaid benefits 3. The jurisdiction where your will is probated CLAconnect.com/privateclient 6 ©2015 CliftonLarsonAllen LLP . Domicile requirements There are two residency requirements: you must be physically present in the state, even though you aren’t mandated to be there for a specified length of time; and you must aim to make the state your permanent home. Some states have an exception to the physical presence requirement. If you marry a person domiciled in another state, you may be able to claim your spouse’s state of domicile as your own, even if you never go there. Because the intent to reside in any state is subjective, only you can know your true intentions. Your actions and conduct can demonstrate to others whether you have shown intent. The U.S.

Supreme Court has suggested to other courts that are deciding on domicile issues to consider the following factors: • Maintain records of where you spend your time during the year. • Register to vote in your new state. • Transfer your vehicle titles and get a driver’s license in the new state. • Establish bank accounts in your new state. • Update your estate planning documents to reflect your new state of domicile. Income tax return considerations In addition, for income tax purposes, most states have rules based on specific statutory criteria whereby you are considered a “resident” if you have been physically present in the state for a certain number of days (often greater than 183 days) and/or if you own a place of abode in their state. You can meet the test for residency in dual states by having a domicile in one state but meeting the statutory rules for residency in another state. • Current residence • Voting registration and voting practices • Location of spouse and family • Location of personal and real property • Location of brokerage and bank accounts • Memberships in churches, clubs, unions, and other organizations • Location of your physician, lawyer, accountant, dentist, and stockbroker • Place of employment or business • Driver’s license and automobile registration • Payment of taxes Your income may be taxed in your state of domicile, the state where you earned it, or both. If you relocate on a date other than January 1, you will probably have to file part-year income tax returns in both states if they both have income taxes.

In some states, if you’re physically present for a certain period of time, you’re liable for income taxes in that state regardless of domicile. The most important point to remember when claiming a state as your domicile is to be consistent. Inconsistency is the single biggest mistake you can make regarding domicile. Additional factors to include: Any state will take you.

It’s the state you are leaving that doesn’t want to give you up. If you want to change your domicile, be prepared to convince the authorities of any state that may be negatively affected by your move that you have truly changed your state of legal residence. For instance, if you move from a state with income and/or estate taxes to a state that doesn’t have those taxes, you may be asked by your former state to prove that you have legitimately changed your domicile. The state will review the quality and not the quantity of your facts and circumstances to determine the validity of your claim.

Most states aggressively audit a change in residency when you are leaving a state that imposes income tax and moving to a state that does not. These audits require you to provide extensive documentation on your whereabouts, including detailed credit card bills, bank statements, travel logs, and cell phone bills. • Where you spend the most time with family and friends • Citation in wills, testaments, and other legal documents • Location of safe deposit boxes used for family records and valuables • Location of your autos, boats, and/or airplanes and their registrations • Location of the items that you consider near and dear (jewelry, family heirlooms, works of art, etc.) • Telephone services at each residence, including the nature of the listing, the activity, and the service features • Relative size of the home in your new domicile versus your home in another location Things to do to establish legal residence • Change your permanent address to the new state and use it for every form you fill out. • Stop claiming any benefits to which you were entitled in your former state of residency. • Sell your former residence in the other state. If you want to maintain a place to stay where you used to live, consider leasing or purchasing a smaller residence than the one in your new state. CLAconnect.com/privateclient While residency is a factor when considering your retirement, think broader and compare the overall tax scenarios of the states for domicile consideration.

In addition, review the gift, estate, and inheritance taxes. But in no case should taxes be the sole motivating reason. 7 ©2015 CliftonLarsonAllen LLP . Focus on what you can control in retirement, and think about your health and the health of your spouse, your finances and financial commitments, and your desired lifestyle. If your new location does not address these three areas of concern, then you should consider your alternatives. Unless some unforeseen disaster befalls the government or the Social Security tax is repealed, benefits are going to continue in one form or another. Some modifications might be needed to keep the program’s existing promises, but chances are good that there will be something there when you retire. How we can help The residency rules are complex and this issue is often contested by state taxing authorities. If a move is part of your retirement plan, know the factors involved with changing your state of residency and the time it takes to put it all in place.

Contact your advisor to understand these rules and review your plans. _____________________________________________ Few people will dispute the popularity of this Depressionera program. A 2013 survey by the National Academy of Social Insurance (NASI) showed that 96 percent of those currently receiving benefits say it is important to their monthly income; 72 percent say that without Social Security they would have to make significant sacrifices. But 57 percent of those same survey respondents say they are not confident in the system, and 69 percent of those not yet receiving benefits say they are not confident that all of the future benefits they are supposed to receive will be available to them. Kara Kessinger, CPA, Principal, Private Client Tax kara.kessinger@CLAconnect.com or 267-419-1634 Table of contents I think a few more Yogi-isms would be a great way to guide us as we look at the finances and future of Social Security and why it should be a part of your retirement planning. “A nickel ain’t worth a dime anymore.” The Social Security trust fund is intended to cover the benefits promised to those who pay into it. The fund is invested in special U.S.

Treasury bonds issued when the trust’s funds are loaned to other parts of the government. The trust fund collects interest on those loans. Since Social Security is a pay-as-you-go program, it can finance its costs through a combination of dedicated revenue and trust fund assets that are a distinct entity within the federal budget and can be considered an independent (off-budget) program. In the Social Security Administration’s 2013 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, the trustees project that trust fund reserves will continue to increase for the next several years, growing from $2.7 trillion at the beginning of 2013 to $2.9 trillion at the beginning of 2021. By 2021, annual costs will begin to exceed total income, and trust fund reserves will begin to decline.

By 2033, the trust fund will be exhausted. At that time income into the program via Social Security taxes would only be sufficient to pay 77 percent of benefits promised, and 72 percent of benefits promised by the end of 2087. Retirement, Baseball, and the Real Future of Social Security by James Clemensen Baseball sage Yogi Berra is quoted as saying, “Half the lies they tell about me aren’t true.” You could say the same about Social Security. Some critics seem to only choose statistics that support their notion that Social Security is a government boondoggle facing imminent failure.

The truth is, at the venerable age of 79, Social Security is financially sound enough to stay viable in some capacity in perpetuity. “If you don’t know where you’re going, you might not get there.” So even if the trust fund were to be depleted and Social Security could only pay out what taxes bring in, retirees would continue to receive significant benefits. And the changes to keep Social Security viable in its current form What this means to someone planning for retirement is that Social Security should be here when you need it. CLAconnect.com/privateclient 8 ©2015 CliftonLarsonAllen LLP . “It ain’t over till it’s over.” The best time to secure Social Security is now; trustees say that the sooner changes are enacted the less painful they will be. For example, a combined Social Security tax rate increase to 15.12 percent now would close the actuarial deficit, but the Social Security tax rate increase would have to jump to 16.50 percent if postponed until 2033 and 17.17 percent if postponed to 2087. are much more realistic than generally made known. For example, trustees have calculated that a Social Security tax increase alone, from the traditional 12.4 percent (employers and employees each pay 6.2 percent) to a combined rate of 15.12 percent, would provide the funding necessary to pay projected benefits for the next 75 years. In addition, there are many small changes that would bring Social Security into actuarial balance, though each change individually resolves only a fraction of the deficit. Strategy Impact Index full retirement age to longevity The issue may be forced to the forefront by a projected 2016 shortfall in the disability insurance (DI) component of Social Security; Congress will need to reallocate revenue between old-age and survivors insurance (OASI) and DI as it has done 11 times in the past. This may be lawmakers’ next opportunity to address long-term problems and demonstrate that the rumors of Social Security’s demise have been greatly exaggerated. Covers about one-fifth of the actuarial deficit Index cost of living adjustments (COLAs) to the chained consumer price index (which reflects substitutions that consumers make within COLA) Covers about one-fifth of the actuarial deficit Subject 90 percent of wages to the Social Security tax, which would increase the taxable earnings limit Covers about one-third of the actuarial deficit It appears that Social Security will remain a cornerstone of the financial plans of most Americans.

That seems perfectly logical since the present value of a couple’s Social Security benefits can be worth well over $1 million and provide an annuity stream that protects against the risk of outliving your money. But Social Security remains one of those things that is beyond your individual control. To achieve your retirement vision, it’s often better to focus your attention on those things that you can control, like living within your means, tax planning, and your investment portfolio. The most practical changes to present law can be reviewed with a calculator created by the Committee for a Responsible Federal Budget. “When you come to a fork in the road, take it.” According to the NASI survey, factual information can change a person’s concerns about the future of Social Security.

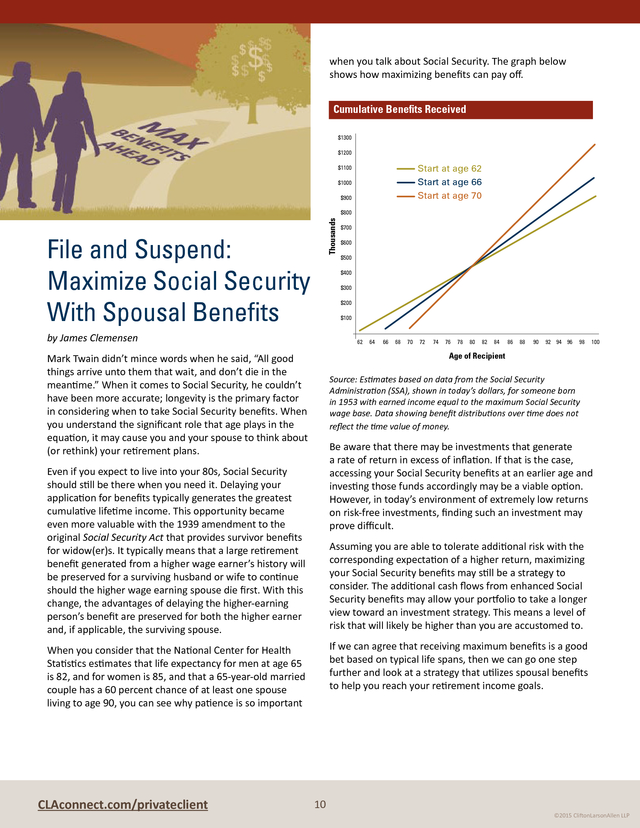

Just 18 percent of respondents knew that Social Security would still be able to pay a reduced benefit in 2033. After learning that an increase in Social Security taxes would ensure that the program could pay full benefits for 75 years, the number of survey participants who think Social Security financing is in a crisis dropped by half, while those who think it is a manageable problem increased by two-thirds. Yogi had it right when he said, “The future ain’t what it used to be.” But if we can agree that your future will likely include Social Security, then the next thing you need to do is come up with a strategy for when to take it. _____________________________________________ James Clemensen, CFP®, Wealth Advisor CliftonLarsonAllen Wealth Advisors, LLC james.clemensen@CLAconnect.com or 612-373-1404 Greater education will help people understand that Social Security is sustainable, and is likely to be supported in the voting booths judging by the high percentage of Americans who agree with these statements: Table of contents • “I don’t mind paying Social Security taxes because it provides security and stability to millions.” (84 percent) • “It is critical that we preserve Social Security even if it means increasing the Social Security tax paid by working Americans.” (82 percent) • “We should consider increasing Social Security benefits.” (75 percent) • “Do not means-test eligibility for Social Security benefits.” (74 percent) CLAconnect.com/privateclient 9 ©2015 CliftonLarsonAllen LLP . when you talk about Social Security. The graph below shows how maximizing benefits can pay off. Cumulative Benefits Received $1300 $1200 Start at age 62 Start at age 66 Start at age 70 $1100 $1000 $900 Thousands $800 File and Suspend: Maximize Social Security With Spousal Benefits $600 $500 $400 $300 $200 $100 by James Clemensen 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 100 Age of Recipient Mark Twain didn’t mince words when he said, “All good things arrive unto them that wait, and don’t die in the meantime.” When it comes to Social Security, he couldn’t have been more accurate; longevity is the primary factor in considering when to take Social Security benefits. When you understand the significant role that age plays in the equation, it may cause you and your spouse to think about (or rethink) your retirement plans. Source: Estimates based on data from the Social Security Administration (SSA), shown in today’s dollars, for someone born in 1953 with earned income equal to the maximum Social Security wage base. Data showing benefit distributions over time does not reflect the time value of money. Be aware that there may be investments that generate a rate of return in excess of inflation.

If that is the case, accessing your Social Security benefits at an earlier age and investing those funds accordingly may be a viable option. However, in today’s environment of extremely low returns on risk-free investments, finding such an investment may prove difficult. Even if you expect to live into your 80s, Social Security should still be there when you need it. Delaying your application for benefits typically generates the greatest cumulative lifetime income. This opportunity became even more valuable with the 1939 amendment to the original Social Security Act that provides survivor benefits for widow(er)s.

It typically means that a large retirement benefit generated from a higher wage earner’s history will be preserved for a surviving husband or wife to continue should the higher wage earning spouse die first. With this change, the advantages of delaying the higher-earning person’s benefit are preserved for both the higher earner and, if applicable, the surviving spouse. Assuming you are able to tolerate additional risk with the corresponding expectation of a higher return, maximizing your Social Security benefits may still be a strategy to consider. The additional cash flows from enhanced Social Security benefits may allow your portfolio to take a longer view toward an investment strategy.

This means a level of risk that will likely be higher than you are accustomed to. If we can agree that receiving maximum benefits is a good bet based on typical life spans, then we can go one step further and look at a strategy that utilizes spousal benefits to help you reach your retirement income goals. When you consider that the National Center for Health Statistics estimates that life expectancy for men at age 65 is 82, and for women is 85, and that a 65-year-old married couple has a 60 percent chance of at least one spouse living to age 90, you can see why patience is so important CLAconnect.com/privateclient $700 10 ©2015 CliftonLarsonAllen LLP . What are spousal benefits? Spousal benefits may be paid to the husband or wife of an individual who is entitled to Social Security retirement benefits based on the worker’s highest 35 years of Social Security taxable wages. This means that one spouse may apply for a benefit equal to 50 percent of the other spouse’s full retirement age (FRA) benefit. But to access benefits based on the employment record of your spouse, the other person must have already filed an application for his or her own retirement benefits. This may seem counter-intuitive, but it’s the foundation of the file and suspend strategy (also known as voluntary suspension or claim and suspend). Filing and suspending can also be useful if Jane is too impatient for benefits to start at 66.

If she begins receiving benefits at age 62 the amount would be based on her own employment record. Her husband is able to file and suspend at his FRA of 66, so she would only access her $800 benefit and this amount would be penalized down 25 percent ($200) to $600 due to her early application. Four years later, Jack may still file and suspend to give Jane access to spousal benefits, although her $200 penalty would continue and $1,321 would only be $1,121. With both scenarios the suspension of Jack’s benefits also allows Jack the flexibility of a subsequent filing for retroactive benefits going all the way back to the date of the suspension. Jack then has the ability to change his mind and receive a lump sum for all of the benefits he has waited on at any time between his FRA (66) and age 70.

The full 48 months of $2,642 deposits would equal $126,816. How the file and suspend strategy works The file and suspend strategy, made possible by the Senior Citizens’ Freedom to Work Act of 2000, adds a wrinkle to collecting spousal benefits. It works like this: • An individual whose wages will be the basis for spousal payments applies for his or her own retirement benefits at the FRA of 66. • That person then immediately suspends benefits without ever receiving a retirement benefit deposit from Social Security. • By applying, the higher-earning spouse makes it possible for his or her partner to begin receiving spousal benefits, while leaving his or her own retirement benefit unaffected and growing until as late as age 70. Never put off until tomorrow… Mark Twain burnished his credentials as a procrastinator when he said, “Never put off until tomorrow what you can do the day after tomorrow.” Like his earlier advice, this wisdom may also be applied to the question of when is the best time to begin receiving the Social Security payments to which you and your spouse are entitled. There are other strategies for maximizing your Social Security benefits. In future articles on this topic, we’ll look at one called “claim now, claim more later” and another that combines that strategy with file and suspend.

Always consult an investment advisor and tax professional to assist in analyzing your needs and corresponding risks. _____________________________________________ File and suspend works best when the lower-earning spouse has a retirement benefit that is less than one-third of the higher-earning spouse’s. An example of the file and suspend strategy Jack has an FRA benefit of $2,642 (the maximum) and his wife, Jane, has a benefit of $800. They are the same age. At his full retirement age of 66, Jack applies for retirement benefits, but then suspends his benefits before receiving any payments. Simply by applying for benefits, Jack allows Jane to begin a $1,321 spousal benefit (which is equal to half of Jack’s retirement benefit) rather than only $800 that Jane would get based on her own work history.

Jack’s own retirement benefit continues to grow until it is $3,487 at age 70. James Clemensen, CFP®, Wealth Advisor CliftonLarsonAllen Wealth Advisors, LLC james.clemensen@CLAconnect.com or 612-373-1404 Table of contents Unlike retirement benefits, which can grow through age 70, spousal benefits only grow until FRA. If Jane chooses the spousal benefit, it will be larger than her own maximized benefit. File and suspend bumps her monthly check from $800 to $1,321 four years ahead of schedule, bringing her an extra $25,008 that would have been lost had she put off receiving spousal payments until Jack began receiving his individual retirement benefit. CLAconnect.com/privateclient 11 ©2015 CliftonLarsonAllen LLP .

Consider this example of a hypothetical 60-year-old man comparing the differences between an investment in a deferred income annuity versus an immediate annuity. Potential advantages of deferred income annuities Nash is 60 years old and nearing retirement. He expects to follow in his parents’ footsteps and live into his 90s. Nash decides to invest $100,000 in a DIA, and he wants the payments to start at age 80. At the time of this writing, after the 20-year deferral period, Nash will be able to withdraw around $42,000 per year for the rest of his life. So, if he lives to age 95, he will have received $630,000 in income from his initial $100,000 investment. Now, what if Nash decides to wait until he is 80 years old and he invests in an immediate annuity? Let’s assume that the $100,000 he had at age 60 was put into conservative investments yielding 3 percent interest per year for that 20 years. By age 80, he would have about $180,000.

An 80-year-old investing $180,000 in an immediate annuity will receive about $1,500 per month, or about $18,000 per year. So, if Nash lives to age 95, he will receive about $270,000 in income. Deferred Income Annuities Offer PensionLike Retirement Benefits by Frank Zawlocki Many retirees no longer have the benefits of a traditional pension plan and its guaranteed lifetime income. Even so, people continue looking for methods to create a pensionlike benefit.

Those who have accumulated a sum of money over time may have looked to an immediate annuity to provide the income stream they desire. Now the insurance industry has created an alternative solution: a deferred income annuity (DIA). In this scenario, the advantages of a deferred income annuity are clear. Of course, this example is hypothetical and actual payout amounts will vary based on age, deferral period, and interest rates at the time of purchase. A caveat about your principal With most deferred income annuity-based products, the holder forfeits the principal in exchange for the guarantee of future payments.

In order to pass the investment on to heirs in the event of the holder’s death, some insurance companies offer optional riders. Another option adjusts for annual inflation and provides larger payments. Sometimes referred to as a longevity annuity, a DIA works much like conventional annuity products except the payments do not start right away. The holder provides a lump-sum payment to the insurance company in exchange for guaranteed lifetime income that begins at a future date, sometimes up to 30 or more years down the road. Deferred income annuities are just one of many options to consider when planning retirement income.

The best way to formulate a personalized solution is to talk to a qualified financial advisor. _____________________________________________ Although DIAs are sold by insurance companies, they should not be confused with a cash value life insurance policy, which can also offer benefits in retirement planning, including tax savings for high income earners. Frank Zawlocki, Director of Insurance Services CliftonLarsonAllen Wealth Advisors, LLC frank.zawlocki@CLAconnect.com or 608-662-9149 How a deferred income annuity works When a person purchases a deferred income annuity contract, the payout date is determined and the insurance company guarantees a set amount. It is important to note that DIAs are not liquid investments. When you invest in one, you completely forfeit the initial premium.

Several products have some liquidity options, but they can be difficult to invoke and are often subject to surrender fees. Table of contents Deferred income annuities offer significantly higher payouts than their immediate annuity counterparts. CLAconnect.com/privateclient 12 ©2015 CliftonLarsonAllen LLP . of their salary and bonuses to fill the retirement funding gap. The only trouble is, as the owner of the business, you may not be able to participate due to the tax treatment of your business entity. An employer-sponsored cash balance retirement plan also offers some attractive benefits for employees and for the business. As income tax rates increase, retirement investors are looking for solutions that allow them to make aftertax contributions that defer or eliminate future tax on those monies. They should also consider how the gain (or interest) and distributions are taxed.

A Roth IRA is one solution that provides tax deferral and tax-free distributions, but there are income and contribution limits on these plans. A married couple with income greater than $191,000 is ineligible. Even those who are eligible are limited to $5,500 in annual contributions. Life Insurance: A Retirement Strategy With Tax Savings for High Earners This is where life insurance comes in. A Roth IRA compared to life insurance High income individuals may be able to supplement retirement income and attempt to achieve tax efficiency with life insurance.

Take a look at this comparison of the Roth IRA and a cash value life insurance policy. by Frank Zawlocki and Mark Wyzgowski There are almost as many ways to save and invest for retirement as there are retirees. But all of the options are not created equal, and there is one that may not always enter the conversation: life insurance. Including a cash value life policy in the mix can alleviate the drawbacks of some of the more common options, while still providing flexibility, tax-efficient growth, and income. Feature No Yes Yes Tax-deferred accumulations Yes Yes Tax-free death benefit No Yes Penalty for early withdrawal Yes Possibly Cost of insurance charges No Yes Market risk Possibly Possibly Life insurance allows the policy owner to contribute amounts up to an insurance company limit, or limits that would cause the policy to be considered a modified endowment contract, which is taxable under federal law. The cash value of the policy grows tax deferred, and when the income is needed, the policy owner can make taxfree withdrawals of the reportable cost basis.

With many policies, the policy owner can also take loans against any gains. The loans are not taxable at the time they are taken, but will reduce the death benefit by the amount of the loan, plus any interest. The solution may be to create your own retirement income plan. This can be accomplished by accumulating cash, investing in public or private offerings (such as stocks, bonds, and mutual funds), or contributing to a life insurance policy.

In recent years, more have been choosing deferred income annuities for the pension-like benefits they can produce. Each of these options comes with costs and benefits; one of the most important considerations is the tax treatment. One pitfall to this strategy is that if the policy owner takes out all the cash value of the contract and the policy lapses, all of the loans will be taxable in the year the policy ends. To compensate for that risk, the insurance industry has created riders to limit the amount of contract values that If you are a business owner, you can create a nonqualified deferred compensation plan that allows highly compensated employees to defer an unlimited amount CLAconnect.com/privateclient Life Insurance Yes Tax-favored withdrawals Limitations of 401(k)s and IRAs Many people rely on qualified plans, such as 401(k)s and individual retirement accounts (IRAs), for their retirement savings due to the tax advantages they offer. However, these tried and true accounts come with strict limits on income and contributions, which can result in inadequate retirement savings, especially for high income earners. Roth IRA Contribution limits 13 ©2015 CliftonLarsonAllen LLP .

can be taken out as loans. These features will essentially freeze the policy, but still allow it to stay in force until the death of the insured. Collecting the life insurance death benefit The death benefit of a life insurance policy can be the selfcompleting mechanism of the retirement income plan if the insured person passes away. The death benefit will be greater than the cash value of the contract for the majority of the policy’s lifetime. If the death benefit is exercised, the proceeds can provide retirement income to the surviving spouse and family, and additional dollars to assist with current financial needs. Connecting Your Estate and Financial Plans Another planning consideration is who to insure.

In many cases, it is appropriate to have both spouses insured on separate policies. However, in some cases, covering husband and wife together may create the greatest policy efficiency and enhance the income potential. Ownership of a policy is an important consideration since an individually owned policy could be included in your taxable estate. Even so, in most states, some or all of a life insurance policy’s cash value and death benefit may be protected from creditors. by Mike Prinzo A client recently asked me whether he should implement a complex estate planning tool because one of his sibling’s advisors recommended the idea.

The question captured what many people struggle with when they think about estate planning: an item on a “to-do list” that should be crossed off as quickly and efficiently as possible. Unfortunately, no amount of bells and whistles can magically short cut your real mission: thoughtful planning for the future. Filling the retirement funding gap It’s important to look at each individual situation carefully to determine if life insurance planning is a good way to address a void in retirement funding, and if it can be crafted to provide income and tax efficiencies. Of course, you should always start with a vision of what you want to do in your retirement, and a careful assessment of your financial situation. Consult an investment advisor and tax consultant to analyze your needs and the corresponding risks. _____________________________________________ The to-do list approach is contrary to the very purpose of estate planning and is likely due in part to the ever changing estate tax exemption that confused taxpayers over the past decade.

However, in January 2013, the American Tax Relief Act of 2012 (ATRA) was signed into law. It created some certainty for taxpayers who engage in estate planning, including an increased estate tax exemption that is indexed for inflation each year and is $5.34 million per person in 2014. Frank Zawlocki, Director of Insurance Services CliftonLarsonAllen Wealth Advisors, LLC frank.zawlocki@CLAconnect.com or 608-662-9149 Think of it as life planning An estate plan, although important, should be a piece of your overall financial plan. A successful plan for the future uses a goals-based approach that helps you identify, implement, and achieve your big picture dreams.

Just like your dreams evolve, your financial and estate plan should evolve to help you stay on track. Estate planning, when performed within an overall financial plan, can dramatically impact the following areas: Mark Wyzgowski, Managing Principal mark.wyzgowski@CLAconnect.com or 515-346-3673 Table of contents • Cash flow • Harvesting potential income tax benefits • Balancing complexity versus cost CLAconnect.com/privateclient 14 ©2015 CliftonLarsonAllen LLP . Trusts, cash flow, and income tax Business owners, retirees, and soccer moms all would agree that the last five years have demonstrated the importance of cash flow to the survival of businesses, second homes — and family budgets. Many commonly used estate planning vehicles, such as intentionally defective grantor trusts (IDGTs), self-cancelling installment notes (SCINs), and spousal lifetime access trusts (SLATs) can positively or negatively impact cash flow. the trust, and to remit this information to the beneficiary of the trust. Whether you are subject to estate taxes or not, estate planning is an important process and should be investigated by nearly everyone. Whether you want to plan a meaningful retirement, cement a lasting legacy, or pass your wealth to heirs (or all three), estate planning gives you the best opportunity for accomplishing your goals. _____________________________________________ For example, an IDGT is a grantor trust that can be utilized in an estate plan to transfer wealth (often at a discount) from one individual to another. However, the creator of the trust retains the responsibility for paying any income tax associated with assets owned by the IDGT.

Therefore, be sure to understand and incorporate the cash flow implications of an IDGT with your financial advisor, so that the estate plan does not create unexpected, and undesirable, cash flow issues. Mike Prinzo, CPA, Principal, Private Client Tax michael.prinzo@CLAconnect.com or 505-222-3517 Table of contents In many cases, estate planning vehicles not only affect your estate, but can also create income tax implications. For example, a charitable remainder trust (CRT) is commonly used to include philanthropic goals in your plan. A CRT lets you retain a cash flow stream that is paid over a period of years, while allowing the assets inside the CRT to transfer to a charity at some point in the future. A CRT can be a helpful because it gives you cash flow, reduces the value of the estate and/or estate tax upon an individual’s passing, and fulfills your charitable legacy goals.

Contributions to a properly structured CRT can also lower your income tax burden because they become an immediate charitable contribution deduction. A smaller tax bill can influence your financial plan in a number of ways, such as: Tax-Smart Tips for Handling Your IRA and Estate Plan • Reducing the cash distribution needs from a portfolio • Creating additional resources that can be invested in a portfolio • Providing the option to reduce or eliminate outstanding debt obligations by Nicholas Houle Most people have some type of qualified retirement account as part of their personal net worth. Some common retirement savings vehicles include, among other things, profit-sharing plans, 401k plans, pension plans, and individual retirement accounts (IRAs).

This article will point out some tips to consider when planning to maximize the benefits of these accounts in your estate plan. The cost of complexity When estate planning is performed without regard to your life as a whole, the implementation and annual costs of an estate plan can be overlooked. Many estate planning vehicles have additional costs and professional fees, such as valuation requirements, annual income tax returns for new entities created as a result of the planning process, and in some cases, more complicated income tax returns. And while a CRT can yield many benefits, as discussed above, it will require you to file an annual income tax return to report the income and deductions generated by CLAconnect.com/privateclient Following the general rule, most qualified retirement account owners must begin annual required minimum distributions (RMDs) when they turn 70.5. For some couples, this is a source of retirement cash flow while 15 ©2015 CliftonLarsonAllen LLP .

others don’t consider annual distributions a necessity. But Congress decided the taxation of these accounts must occur at some point, hence the RMD rules. level of complexity that may not be needed. Review your objectives for your retirement plan assets before setting up these complex strategies. Be aware of the income tax implications of common estate planning strategies during your review (e.g., non-grantor trusts), along with the nonfinancial planning aspects of a trust. If you don’t need the cash flow from the annual distributions, consider converting some or all of your account to a Roth before your RMD date. A Roth allows you to set aside after-tax income, and there are two main benefits to this retirement approach: Charitable giving and contingent beneficiaries A charity can be a perfect beneficiary for some or all of a retirement account (other than a Roth IRA). Assets that go directly to aid charitable organizations are not taxable for income tax purposes or taxable for estate tax purposes. For those with larger estates and retirement plan accounts, having a tax exempt entity as the beneficiary of a portion of the account can be very tax efficient. 1. Roth IRAs do not have a RMD during the owner’s lifetime; and 2. When the owner converts a retirement plan to a Roth and pays the conversion income tax from other fund sources, the Roth IRA continues to grow tax free. The designated beneficiaries (e.g., children and grandchildren) must start RMDs after your death but generally NONE of the distributions are taxable income. A word of caution: If your favorite charity is a partial beneficiary of a retirement account, it is important the charitable portion be paid out in a defined time period after the account owner’s death.

That way, individual beneficiaries may have the benefit of “stretching” the retirement account balances over their lifetimes. Beneficiary designations could hinder or help Certain beneficiary choices can unnecessarily accelerate distributions and related income tax, so be sure to review your designations with a professional advisor. Naming your loved ones as beneficiaries allows for the best options to defer taxation of benefits by “stretching” the retirement plan money over their life expectancy. Finally, check your contingent beneficiary designations to allow for disclaimer planning and to prevent an estate from becoming a beneficiary by default. How we can help This article only touches on a few concepts for retirement accounts and estate planning. We encourage you to consult with your CPA and/or wealth advisor for a more thorough review of options and opportunities as part of a well balanced estate plan. _____________________________________________ That rule changes if an estate or non-qualifying trust is a designated beneficiary of your account.

In that case, a special rule requires the benefits to be entirely distributed within five years of the account holder’s death, expediting the taxation of those dollars. Speeding up the taxation of the account’s accumulated benefits can needlessly increase income tax costs and perhaps push recipients into higher tax brackets. Nicholas J. Houle, CPA, Principal, Private Client Tax nicholas.houle@CLAconnect.com or 612-376-4760 Generally naming your estate as beneficiary of your retirement account will cause acceleration of distributions and taxation of your benefits over a five year period or less.

And naming your revocable trust as beneficiary may not necessarily get you the answer you are looking for. Table of contents Qualified trusts Qualified trusts are a bit of a different story. Certain trusts can qualify as a designated beneficiary for the “stretch” period of distributions if they meet the following criteria: • the trust is valid under local law; • the trust is irrevocable or will, by its terms, become irrevocable upon the death of the individual; and • the trust beneficiaries are all individuals who are identifiable from the trust document. Generally, the oldest individual trust beneficiary’s life will set the period for the distributions from the retirement account. Trusts can be useful for certain goals but do add a CLAconnect.com/privateclient 16 ©2015 CliftonLarsonAllen LLP .

Beneficiaries are usually people, but sometimes they are institutions, such as schools, hospitals, or foundations. If you want to create a trust, the hardest thing may be to find a person or entity willing to serve as trustee and abide by your wishes. For a trustee, the most difficult task is to fulfill the stated wishes of the trust creator while maintaining the proper asset allocation to satisfy the interests of two types of beneficiaries: an income beneficiary and a remainder beneficiary. The income beneficiary wants income to enjoy for as long as his or her interest lasts. However, the trustee must balance the desire to provide current income with the notion that the assets of the trust must continue to grow in order to fulfill the remainder beneficiary’s needs. Using a Trust in Financial Planning: Nonfinancial Questions and Choices to Consider It’s a task that is simple in design, but exceedingly difficult to execute. The importance of financial maturity When contemplating the design of a trust, some of the most important decisions are nonfinancial.

So it is critical for a conversation about creating a trust to begin with questions related to the financial maturity of the beneficiaries. by Dominic Zamora There are many examples where someone is given a windfall, only to have it destroy his or her life. We need look no further than many lottery winners to see the pitfalls and adversity often created by unexpected wealth. In many of life’s experiences we look for simplicity, because in simplicity, we find elegance. In the world of strategic financial planning, trusts are simple and elegant, yet there are so many variations that they are among the most misunderstood financial planning vehicles. One of the most frequently posed questions is something like, “What would happen if Liam Littlebucks were to receive Daddy Bigbucks’ fortune?” Many would respond with a not-too-surprising answer: Liam has a gleam in his eye for a red Corvette, a little Mini Cooper, or some other material item with little lasting value.

The solution is often to design a trust that reduces the opportunity for Liam to squander his newfound wealth. For instance, the trust might be designed to match Liam’s regular income until he reaches the age of 30. A planner might also consider the use of a staggered inheritance. This article highlights some of the issues associated with using a trust to transfer wealth, and provides insight into the opportunities for producing particular outcomes. Discussions about use of a trust should nearly always be accompanied by nonfinancial questions; the answers often drive the solution. What is a trust? Webster’s New Collegiate Dictionary says a trust is, “… a property interest held by one person for the benefit of another.” That property interest could be land, but it could just as easily be interests in chemical formulas, or anything else that has value.

Holding that interest by one person for the benefit of another is the essence of what it means to have a trust. Transferring assets over time In creating many modern trusts, we discuss the concept of transferring the underlying assets in a trust over a period of time. Suppose Liam is 30 years old when his parents pass away. Due to the nature of Liam’s personality (and his well-known infatuation with the red Corvette), Daddy Bigbucks created a trust where Liam gets income from the trust until he’s 45.

At that point, Liam receives a distribution equal to 50 percent of the trust’s value. He then receives the final 50 percent of the trust when he reaches 55. A trustee is often appointed to provide guidance and due care over the trust property. The trustee’s job is to provide a “benefit” derived from the trust property and distribute it to the beneficiaries of the trust.

In most instances the benefit comes in the form of income, but it can also mean distributions of trust assets at a specified point in time. CLAconnect.com/privateclient 17 ©2015 CliftonLarsonAllen LLP . An increasing number of clients are considering establishing “dynasty trusts” that have a perpetual life. Not only does the current generation enjoy the benefit of the trust assets, but future generations will as well. Those who desire this form of trust must consider many complex issues pertaining to taxation and state laws related to trusts of this nature. Suffice it to say that when the issues can be resolved satisfactorily, these trusts can be quite valuable. It is important to understand the different types of trusts and how the latest income tax rules affect the trust and its beneficiaries. Grantor trusts There is a good chance that you set up a grantor trust for income tax purposes, as grantor trusts are incorporated into many effective estate planning strategies. Spousal access trusts, grantor retained annuity trusts (GRAT), defective grantor trusts (e.g., an IDGT or DIGIT), and most irrevocable life insurance trusts (ILITs) are grantor trusts. Dynasty trusts can also be structured as grantor trusts. The solutions to age-old difficulties surrounding trusts often lie in the planning capabilities of your advisors. Choose your advisors wisely and make sure you cover all of the bases. _____________________________________________ A grantor trust means that you, as the grantor (the person who established the trust by gift or grant), retain certain powers over the trust that result in you continuing to pay income tax on the trust assets. This can be the income tax result even though you established an irrevocable trust and made a completed gift to the trust.

For example, the power of substitution (i.e., the power to swap assets with the trust) is one of the most popular powers used for grantor trusts. Dominic Zamora, JD, CPA, Principal CliftonLarsonAllen Wealth Advisors, LLC dominic.zamora@CLAconnect.com or 509-363-6345 Table of contents A grantor trust is considered a disregarded entity for income tax purposes. Therefore, any taxable income or deduction earned by the trust will be taxed on the grantor’s tax return. In most cases, there will not even be a requirement to file a trust income tax return, as the income of the trust assets can be reported with your social security number. Tax advantages Establishing a grantor trust has a number of tax advantages.

For example, you can sell assets to the trust without recognizing the gain on the sale. You can also loan money to the trust, and although the trust must pay you at least a minimum IRS-prescribed interest rate (called the applicable federal rate [AFR]), the interest income is not taxable to you. In addition, your trust’s income tax, paid by you as the grantor, is not considered an additional gift to the trust.

Basically, the trust assets can grow for the benefit of the beneficiaries, without the economic burden of paying income tax. In essence, this is a tax-free gift. Income Tax Implications of Grantor and Non-Grantor Trusts However, at some point you may realize that the trust has sufficient assets for its intended beneficiaries — perhaps your children and grandchildren. Or you may no longer find it economical to your personal finances to pay the trust’s income taxes.

In these circumstances, it may be possible to give up or waive the grantor trust powers, which would then convert the grantor trust to a non-grantor trust. Also, after the death of the grantor, the trust will become a nongrantor trust. by Sue Clark So, you set up a trust as part of your estate planning. But do you know how the trust’s income will be taxed? And how does the American Taxpayer Relief Act of 2012 (ATRA), which increased income tax rates and added the new net investment income tax (NIIT), affect the taxation of trusts? CLAconnect.com/privateclient 18 ©2015 CliftonLarsonAllen LLP . Non-grantor trusts A non-grantor trust pays income tax at the trust level on any taxable income retained by the trust. There is a good chance that beneficiaries are in lower income tax brackets. However, keep in mind the estate planning and asset protection objectives of the trust. To the extent that income is distributed from a trust, the income will be included in the beneficiary’s estate, and will also be subject to beneficiary’s creditors, contrary to the original objectives of the trust. Therefore, the trustee should carefully consider discretionary distribution in light of all of the facts and circumstances. If a trust makes a distribution to a beneficiary, such distribution will pass the taxable ordinary income (but generally not capital gains) to the beneficiary, to be taxed on the beneficiary’s personal income tax return.

The trustee must complete Form 1041 and issue a Schedule K-1 to the beneficiary, showing the amount and type of income from the trust to be included on his/her individual tax return. Note that ATRA also made the federal estate tax exclusion $5 million, which permanently indexed it for inflation. The exclusion is $5.34 million for 2014. This legislation will reduce the number of taxpayers subject to federal estate tax.

Therefore income tax planning may be more important that estate tax planning for most taxpayers. Effect of ATRA The ATRA was not kind to trusts, and especially to those that accumulate income. A trust’s income taxation is similar to individuals, but the tax brackets are very compressed. For 2014, a trust will pay income tax at the 39.6 percent tax rate when taxable income is more than $12,150.

Compare this with an individual, where the same income tax bracket kicks in at $406,750 of taxable income ($457,600 for married couples filing jointly). Most trusts can also make distributions within 65 days of the end of the year and elect to consider such distribution as occurring on December 31 of the preceding year. This allows a trustee the flexibility to manage the trust’s taxable income and make a distribution decision based on trust income after gathering all of the information for the tax year. Trusts are eligible for the special income tax rate on longterm capital gains and qualified dividends; in 2014, the 20 percent capital gains rate will apply when trust taxable income exceeds $12,150. The 15 percent and 0 percent capital gains rates also apply to trusts in lower tax brackets. Tax considerations The trust that you established for estate planning purposes may have some interesting income tax considerations.

Be aware of who pays the income tax on the trust income, the opportunities with grantor trust planning, and the income tax effect and distribution planning opportunities for nongrantor trusts. Net investment income Also, the new NIIT of 3.8 percent applies to certain income retained by trusts and estates if taxable income exceeds $12,150. Net investment income includes interest and dividend income and capital gains, but also includes passive income from rental and business activities, and from pass-through entities such as partnerships, limited liability companies (LLCs), and S corporations.* As a result, many trusts and estates will be taxed in 2014 at 43.4 percent on ordinary income and 23.8 percent on qualified dividends and long-term capital gains, plus state level income taxes. *A trust that holds S corporation stock will need special handling! A grantor trust is an eligible S corporation shareholder; however, other trusts will need to meet special requirements and must make a timely election as a qualified subchapter S trust (QSST) or an electing small business trust (ESBT) to own S corporation stock. QSSTs and ESBTs have income taxation unique to their specific status. _____________________________________________ Sue Clark, CPA, Principal, Private Client Tax susan.clark@CLAconnect.com or 612-376-4725 Individual beneficiaries may be eligible for lower tax brackets.

The NIIT does not affect single beneficiaries unless their Adjusted Gross Income (AGI) exceeds $200,000 or beneficiaries who are married filing jointly with AGI exceeding $250,000. Table of contents Managing taxable income This difference in income tax brackets between trusts and individual beneficiaries presents an opportunity to effectively manage the trust’s taxable income. If the trust’s distribution provisions allow discretionary distributions, a trust distribution will result in income taxed at the beneficiary level. CLAconnect.com/privateclient 19 ©2015 CliftonLarsonAllen LLP . those funds first rather than making regular distributions to the spouse. Distributions from the trust to the spouse reduce its effectiveness. Using a SLAT to hedge against a downturn As an example, let’s assume that Sally, who is an executive, would like to make a gift of $5.43 million to use her entire gift tax exclusion in 2015. She and her husband, Fred, own their home jointly and have a joint brokerage account worth $2 million. In addition, Sally has $7 million in an account in her own name.

She is concerned that she and her husband may have a future need for some of the gifted funds, particularly if there is another economic downturn. Make Use of the Gift Tax Exemption With Spousal Access Trusts Sally could establish a spousal limited access trust for Fred’s benefit and transfer $5.43 million from her individual account to the trust. The trust could provide distributions to Fred for his needs and their children’s needs. The intent would be for the funds to stay in the trust but Fred would have access to it if he needed more money.

The trust could be distributed to their children at some point in the future, for example after both Sally and Fred have passed away, or it could stay in trust for future generations. by Lori A. Peterson You may have heard that after more than a decade of changing estate tax exemptions, we finally have permanent law. The American Taxpayer Relief Act of 2012 (ATRA) sets the gift and estate tax exclusion at $5 million, and indexes that amount for inflation beginning in 2012.

For 2014, that gives individuals an exclusion amount of $5.34 million and for 2015, $5.43 million. Although technically permanent, it’s only as permanent as any other tax law, which means it could change in the future. SLAT income tax implications A spousal limited access trust is usually a grantor trust for income tax purposes. This means if you establish a SLAT for the benefit of your spouse, you will report the trust’s taxable income and deductions on your personal income tax return.

A grantor trust is disregarded for income tax purposes, so the trust will not pay taxes. This can be advantageous because it allows the trust to grow without the burden of income taxes. Upon the death of the grantor, the trust will no longer be a grantor trust and will then have to pay income taxes. You might be considering making large gifts in 2014 or 2015 to use your gift tax exclusion while it’s still here.

But you may also be concerned about giving away such a large amount. Wouldn’t it be nice to give it away but still have some ability to access it if something unforeseen happens? A spousal limited access trust may be a solution. For example, Bob is the owner of a car dealership. In 2015, he transfers $5.43 million of nonvoting dealership stock to a spousal limited access trust for the benefit of his wife, Cindy.