Congress Eliminates Popular Social Security Planning Strategies - March 17, 2016

Citrin Cooperman & Company

Description

Alerts

Mar 17, 2016

Congress Eliminates Popular Social Security Planning Strategies

Planning for retirement? Congress recently eliminated three popular strategies that affect planning for Social Security retirement benefits. These new changes

could mean a loss in potential retirement income. These changes go into effect on May 1st so there is still time to use these strategies if you qualify and act

quickly. The suspended strategies, which are explained below, enabled retirees to increase their ultimate retirement benefits. In some cases, those retirees

and their spouses or dependents already utilizing these planning strategies will be grandfathered in. Some of these strategies are still available on a limited

basis.

General Rules for Claiming Social Security

An individual will receive 100% of his or her benefits if they file at full retirement age. If you were born between 1943 and 1954, your full retirement age is 66. For

those born between 1955 and 1959, full retirement age gradually increases until it reaches age 67 for anyone born in 1960 or later.

An individual may claim social security benefits as early as age 62. However, if an individual claims a benefit before full retirement age, the monthly payment

could be reduced by up to 25%. Similarly, an individual who defers payments passed full retirement age will receive an increase in monthly payments of eight

percent annually. This annual increase is only available up to age 70, the maximum retirement age.

Spousal Benefits

A person may claim benefits based upon his or her own earnings record or a spousal benefit. Spousal benefits are based upon the earnings record of a

spouse or, possibly, a former spouse. The spousal benefit could equal up to one-half of the spouse’s benefit at full retirement age, and the spouse must be

eligible for or receiving benefits.

Strategies Affected

File & Suspend Strategy- allowed a spouse to file for social security benefits at full retirement age and immediately suspend the benefits. This gave the

spouse access to spousal benefits, while the deferred benefits of the first spouse grew annually up to age 70.

The Restricted Application- allowed for a person of full retirement age to collect spousal benefits of their retirement age partner, while deferring their own full

benefits, which would grow annually up to age 70.

Retroactive Lump Sum- allowed for retirement age individuals who file and suspended their benefits, to un-suspend and collect a lump sum retroactive

payment at any time prior to 70. The new law still permits un-suspending, but trades the lump sum retroactive payment for deferred retirement credits.

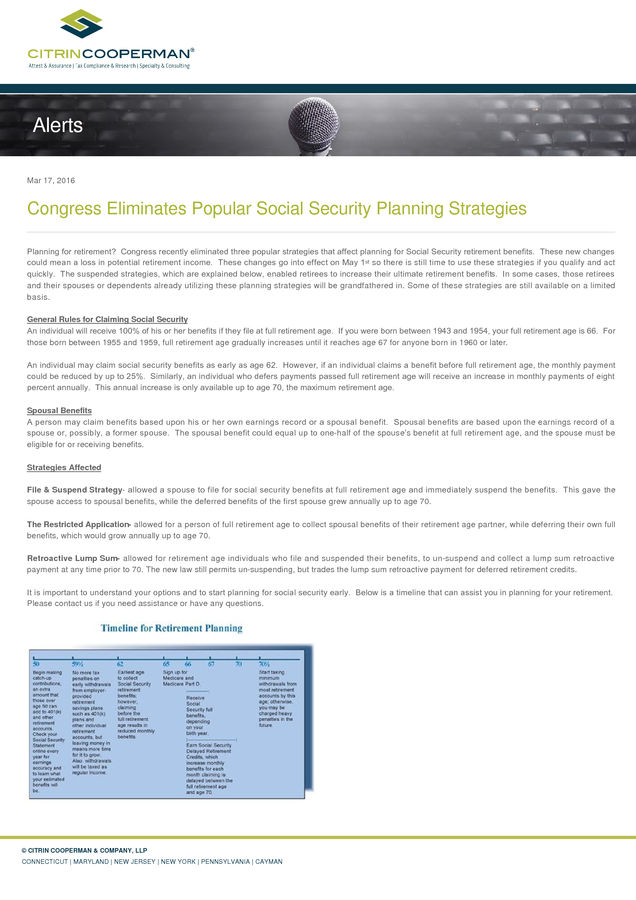

It is important to understand your options and to start planning for social security early. Below is a timeline that can assist you in planning for your retirement.

Please contact us if you need assistance or have any questions.

© CITRIN COOPERMAN & COMPANY, LLP

CONNECTICUT | MARYLAND | NEW JERSEY | NEW YORK | PENNSYLVANIA | CAYMAN

.