2013 US Staffing Industry Survey: Standing Strong Under Pressure – April 10, 2014

Citrin Cooperman & Company

Description

2013 Staffing Industry

Survey Highlights

ATTEST & ASSURANCE | TAX COMPLIANCE & RESEARCH | SPECIALTY & CONSULTING

. Survey Participation

The survey was distributed to over 500 staffing firms

across the U.S.

In excess of 100 participants responded, with the

majority from the Northeast.

Respondents ranged in size from less than $5 million to

more than $250 million in annual revenue.

2

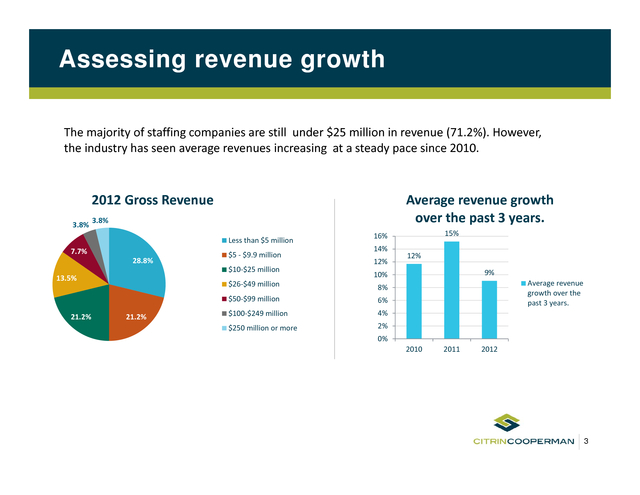

. Assessing revenue growth

The majority of staffing companies are still under $25 million in revenue (71.2%). However,

the industry has seen average revenues increasing at a steady pace since 2010.

2012 Gross Revenue

3.8%

Average revenue growth

over the past 3 years.

3.8%

Less than $5 million

7.7%

28.8%

$5 †$9.9 million

$10â€$25 million

13.5%

14%

12%

21.2%

12%

9%

10%

$26â€$49 million

6%

$100â€$249 million

4%

$250 million or more

Average revenue

growth over the

past 3 years.

8%

$50â€$99 million

21.2%

15%

16%

2%

0%

2010

2011

2012

3

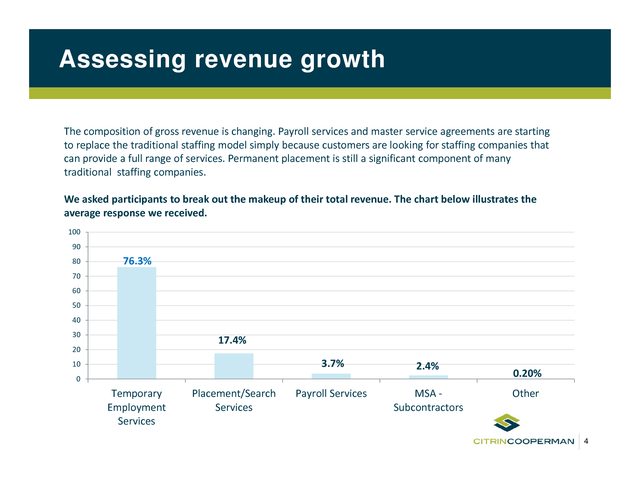

. Assessing revenue growth

The composition of gross revenue is changing. Payroll services and master service agreements are starting

to replace the traditional staffing model simply because customers are looking for staffing companies that

can provide a full range of services. Permanent placement is still a significant component of many

traditional staffing companies.

We asked participants to break out the makeup of their total revenue. The chart below illustrates the

average response we received.

100

90

80

76.3%

70

60

50

40

30

17.4%

20

3.7%

10

2.4%

Payroll Services

MSA â€

Subcontractors

0

Temporary

Employment

Services

Placement/Search

Services

0.20%

Other

4

. Companies are diversifying

In 2010*, we projected that most staffing firms would diversify into IT and Healthcare. The

2013 survey confirmed that 17.3% of respondents expanded into Healthcare and 11.5%

expanded into IT. This increase can be attributed to various factors, including the Affordable

Care Act (ACA), advances in global technology markets, compliance with regulatory matters,

and an aging population (baby boomers), among others.

Which industry sectors have

you diversified or expanded into?

Have not further diversified

51.9%

Healthcare

17.3%

Information Technology

11.5%

Clinical/Scientific

5.8%

Office/Clerical

3.8%

Industrial

3.8%

Finance/Accounting

3.8%

Engineering/Design

3.8%

Legal

1.9%

Marketing/Creative

1.9%

*Citrin Cooperman, Sowing the Seeds of Growth: 2010 Staffing Industry Survey

5

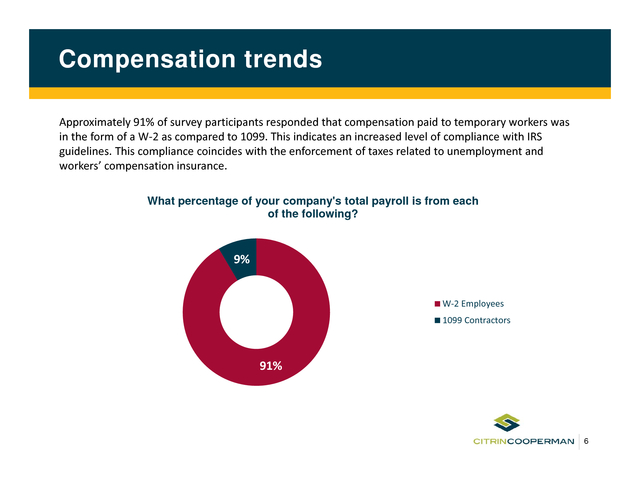

. Compensation trends

Approximately 91% of survey participants responded that compensation paid to temporary workers was

in the form of a Wâ€2 as compared to 1099. This indicates an increased level of compliance with IRS

guidelines. This compliance coincides with the enforcement of taxes related to unemployment and

workers’ compensation insurance.

What percentage of your company's total payroll is from each

of the following?

9%

Wâ€2 Employees

1099 Contractors

91%

6

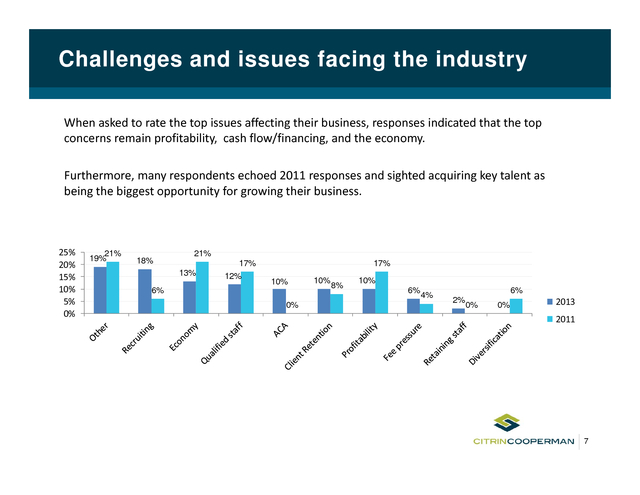

. Challenges and issues facing the industry

When asked to rate the top issues affecting their business, responses indicated that the top

concerns remain profitability, cash flow/financing, and the economy.

Furthermore, many respondents echoed 2011 responses and sighted acquiring key talent as

being the biggest opportunity for growing their business.

25%

20%

15%

10%

5%

0%

21%

19%

18%

21%

13%

17%

12%

17%

10%

6%

0%

10%

8%

10%

6%

4%

6%

2%

0%

0%

2013

2011

7

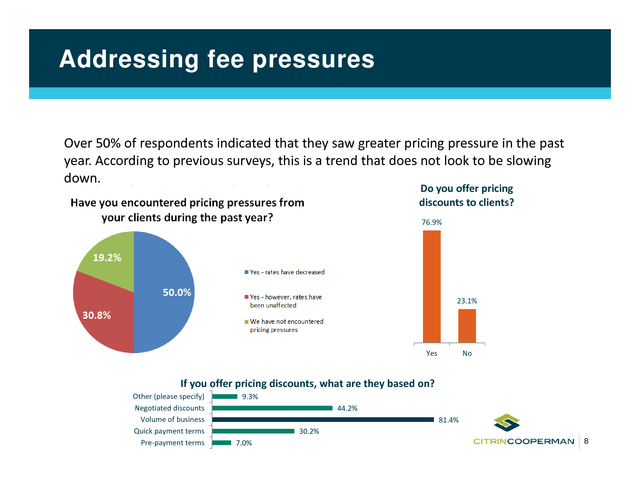

. Addressing fee pressures

Over 50% of respondents indicated that they saw greater pricing pressure in the past

year. According to previous surveys, this is a trend that does not look to be slowing

down.

Do you offer pricing

discounts to clients?

76.9%

23.1%

Yes

No

If you offer pricing discounts, what are they based on?

Other (please specify)

Negotiated discounts

Volume of business

Quick payment terms

Preâ€payment terms

9.3%

44.2%

81.4%

30.2%

7.0%

8

. Looking ahead

Over 65% of respondents are encouraged that they will see line revenue growth in 2014 and

beyond, but it will be slow and steady. Only 3.8% indicated that growth would decline.

3.8%

Industry will continue to grow at a

record pace

9.6%

21.2%

It will continue to take a slow and

steady approach to growth

It will remain stagnant

65.4%

It could decline

9

. Nick Florio, CPA

Partner and Staffing Industry Practice Leader

Image

212.697.1000

nflorio@citrincooperman.com

CITRIN COOPERMAN

529 Fifth Avenue, New York NY 10017

CONNECTICUT | NEW JERSEY | NEW YORK | PENNSYLVANIA

CITRINCOOPERMAN.COM

10

. CAYMAN | CONNECTICUT | NEW JERSEY | NEW YORK | PENNSYLVANIA

CITRINCOOPERMAN.COM

.