Citi Energy Whitepaper, "Lower for Longer" and “Building a Resilient Treasury” - January 2016

Citigroup

Description

Lower for Longer:

How Companies Are Adapting

and Embedding Resilience

An Energy Industry Perspective

This client report has been prepared by members of Citi’s Corporate and Investment Banking division. This is not a

research report and does not constitute advice on investments or a solicitation to buy or sell any financial instrument.

Institutional Clients Group

. 2

Institutional Clients Group

With expectations that the oil and gas prices will remain lower for longer,

the energy industry is undergoing a drastic restructuring. How will companies

weather the impact and adapt? What is the financial optionality as capital

tightens? How can risks from changes in local regulations be mitigated?

Enclosed are two related articles discussing how Chief Financial Officers and Treasurers

are adapting to these changes and working closely with their banks to embed resilience

into their global strategy.

We hope you will find these pieces to be informative and insightful. As you read the

articles, we invite you to let us know how we can deepen our relationship to support your

financing and treasury goals and objectives.

. Lower for Longer: How Companies Are Adapting and Embedding Resilience | About the Authors

About the Authors

Mr. Reilly is Vice Chairman and Global Head of Energy Corporate Banking, with oversight for

the entirety of our Corporate Banking activities with energy clients worldwide. Corporate

Banking at Citi includes Lending, Structured Finance, Debt Capital Markets, Trade Finance,

Commodities, FX and Financial Derivatives and Operating/Transaction Services. He is

responsible for relationships with corporations involved in all phases of the energy industry

around the globe, including the upstream, midstream/transportation, refining/marketing, and

service/supply and drilling segments.

Jim Reilly

Vice Chairman

and Global Head of

Energy Corporate

Banking, Citi

In addition, he is charged with the coordination and networking of our corporate bankers

around the world who cover clients in the energy industry.

Mr. Reilly is a member of the Global Operating Committee of the Corporate Bank and of the U.S. Management Committee of the Corporate and Investment Bank.

He is the Business Senior Credit Officer Level 2, Business Industry Specialist for Energy and the Global Coordinator/Americas Regional Head for Capital Approval/Allocation for Energy. Mr. Reilly has a Bachelor’s of Science in Business Administration from Villanova University in Pennsylvania and a Masters of Business Administration in Finance from The American University in Washington, D.C. Mr. Langshaw is responsible for executing a global sales strategy that delivers solutions for the treasury and working capital needs of energy clients worldwide for Citi’s TTS business.

He has held various senior international management positions at country, regional and global levels across five different continents. Prior to joining Citi, he worked internationally for eight years for a large U.S. international oilfield service company, which culminated in being appointed as Base Manager in Brunei with full profit and loss (P&L) responsibility, overseeing three countries. Peter Langshaw Managing Director, Global Sector Sales Head for Energy, Power, Chemicals & Metals and Mining, Treasury and Trade Solutions, Citi Mr.

Langshaw joined Citi’s Pan-European cash management team and was later based in Singapore, pioneering regional treasury structures in Asia. He then transitioned into Corporate Banking as the subsidiaries Banking Head in Singapore, where he launched and ran the Regional Account Management (RAM) banking team covering Southeast Asia. He was later appointed Corporate Bank Head and Acting Country Head in Vietnam.

After being promoted as Corporate and Bank Head and Market Manager for the Southern Region in Australia, he took up the post of Corporate and Investment Bank Head for Saudi Arabia (Central Region). In 2004, he accepted a position as Director of Multinationals and Transactional Banking for Africa and Middle East region with Barclays. In 2006, he returned to Citi as the Regional TTS Industry Head for Energy, Power, Chemicals and Mining. Later he was appointed Global Sector Sales Head based in Brazil.

He now works in the USA, where, in addition to his global role, he has extended responsibilities for Industrial clients in Latin America. Peter holds an MBA from Manchester Business School and a BA (Hons.) from the University of Nottingham in the UK. He has also attended an Executive Education Program at Harvard Business School. 3 . 4 Institutional Clients Group Adapting to “Lower for Longer” Low commodity prices in 2015 prompted energy companies to drastically revise their operational, capital expenditure, finance and risk management plans. Industry-wide, capital expenditures fell an estimated 45% in 2015 versus 2014. For 2016, the outlook suggests continuing frugality as the prevailing industry view is for oil and gas prices to remain “lower for longer.” As one way to partially address these challenges, companies can seek support and advice from their banks, writes Jim Reilly, Vice Chairman and Global Head of Energy Corporate Banking at Citi. Jim Reilly Vice Chairman and Global Head of Energy Corporate Banking, Citi The dramatic fall in commodity prices since the fourth quarter of 2014 has rewritten the playbook for energy companies. While the upstream and oilfield service segments of the industry have been the most severely impacted, no segment has escaped pain. The WTI and Brent benchmark oil prices finished 2015 at roughly $37 per barrel.

Most observers expect WTI to average between $39 and $49 per barrel in the coming year, with Brent running $3-$5 per barrel higher. At the bullish end of that range, oil prices would firm up in the second half of 2016; at the bearish end, strength would come instead in 2017. Henry Hub natural gas prices were similarly depressed at year-end. With a huge resource base, high inventories and unseasonably warm weather this winter, neither the immediate nor the long-term outlook is bullish for natural gas pricing.

In concert, demand for drilling rigs, oilfield services and equipment and labor has plummeted. In such an environment, both large and small companies face significant challenges. Some weaker oil and gas players have already filed for bankruptcy, and credit ratings and outlooks across the industry have been broadly reduced. All companies are reconsidering how they manage their cash and liquidity and capital programs, as well as the most efficient manner to fund them. While energy companies will undoubtedly experience challenges in the coming months, it is important to recognize that support and advice are available.

As cash becomes tighter, Citi can help corporates manage their liquidity with a wide range of solutions. Moreover, while the backdrop of low commodity prices makes it harder to raise financing, there are a number of alternatives available. A prolonged period of low oil prices The current low oil price, which is expected to rise only moderately in 2016 and 2017, has a number of supply and demand drivers – none of which are likely to disappear in the short term. The American shale revolution fundamentally changed the oil supply equation, as it had done earlier with natural gas, with the United States now among the top oil producers globally. Supply has also increased from Canada, Russia, Iraq, Kuwait, Saudi Arabia and deep-water sources, and it may soon be augmented by exports from Iran. Unlike times in the recent past, OPEC – or, really, Saudi Arabia – has refused to cut production to rebalance the market.

At the same time, modest growth in the United States, and sluggish economies in Europe and Latin America have led to lower . Lower for Longer: How Companies Are Adapting and Embedding Resilience | Adapting to “Lower for Longer” demand. And in China, where the economy is still expanding faster than in the rest of the world, energy demand is lower than anticipated even a year ago. The result is that the world is currently producing over a million barrels of oil per day more than is being consumed. While this oversupply is unlikely to change dramatically in the near term, there are several significant variables in the medium term: U.S. production decline, already underway, is likely to accelerate; Saudi Arabia may decide that lower production is a price worth paying to buoy prices; demand in China could pick up if the economic growth rate increases; and, in the background, the prospect of geopolitical shock remains. The implications of lower prices At current production volumes, the oil price fall has led to a drop in revenues across the industry of around $1.5 trillion a year. While falling revenues have been cushioned by lower service costs, the meticulous management of expenses, and productivity gains, this represents only a fraction of lost revenues.

The resulting drop in operating cash flows has prompted a steep decline in capital expenditures among upstream companies. Larger oil and gas producers are necessarily better placed to weather the decline in revenues. Smaller producers, many of which are backed by private equity firms and are highly leveraged, will face greater challenges as their capital structures were predicated on high oil and gas prices. At current prices, many companies are not viable – already, a number of bankruptcies of small companies have occurred in the United States.

Along with producers, the impact of lower commodity prices has hit the oilfield services segment the hardest. To date, midstream and downstream companies have fared reasonably well. Small and medium-sized producers typically borrow via Reserve-Based Lending (RBL) bank facilities, a type of secured financing specific to the oil and gas business. Financing terms for the following six months are reset based on current oil prices and production outlooks.

The 2015 resets reduced funding availability by 1525%, on average. Most companies were able to absorb that liquidity decrease via reduced expenditures and, in some cases, other debt and/or equity financing. However, lower prices will mean even further reductions in borrowing availability.

With a historically low percentage of production hedged, there will be few gains to offset low prices. Many companies could face a liquidity shortfall, which may accelerate industry consolidation and increase the number of bankruptcies. In the liquefied natural gas (LNG) industry, the impact of lower oil prices is more nuanced. LNG prices are typically linked to a basket of oil prices under long-term supply agreements. Therefore, the slump in oil prices has dragged down LNG prices. Unlike oil, natural gas trades at different prices around the world.

The arbitrage between U.S. and Asian and European LNG prices offsets the cost of specialized facilities and ships. However, the decline in oil prices has resulted in this arbitrage shrinking, undermining the viability of the market. The cost of LNG facilities and ships is immense and these projects can take years to build, with cost overruns being a common problem.

The elimination of a comfortable arbitrage between U.S. and Asian and European gas prices introduces significant risk into the LNG market that may stifle investment, at least in the short term. While declines in LNG prices will undoubtedly cause disruption, the impact of price changes will be lessened to some extent by the predicted long-term growth in LNG demand and the inevitable reduction in development costs driven by lower near-term demand. LNG is seen as a source of cleaner energy and has therefore been prioritized by governments over more polluting fossil fuels, such as coal.

As a result of this anticipated long-term demand, many planned liquefaction and transportation facilities will be built, although the timescale for their completion is likely to be pushed out. 5 The world is currently producing over a million barrels of oil per day more than is being consumed. While this oversupply is unlikely to change dramatically in the near term, there are several significant variables in the medium term. . 6 Institutional Clients Group Adapting to weaker revenues The sharp fall in revenues has increased companies’ focus on liquidity. The largest firms have the greatest flexibility and many have already increased the size of their banking facilities or tapped the investment grade bond market. Before markets stalled, smaller companies accessed high yield, second lien, and equity markets in order to augment liquidity. As financing conditions become tougher, and traditional sources of finance such as the bank, bond and equity markets become harder to access, energy companies are increasingly turning to alternative sources of finance, which can take into account their capital structures, improve their credit profiles, and support greater financial flexibility. Alternative sources of capital include volumetric production payments, project finance, export agency finance, supplier finance and asset-based lending, the latter typically against receivables and inventory. Strategic alternatives, although made more difficult by an uncertain market, also provide a capital source; these include divestitures, corporate spinoffs, and subsidiary IPOs such as master limited partnerships (MLPs).

Even larger companies are innovating: an oil major raised billions by issuing a hybrid bond; a national oil company sold a “century bond” with a hundred-year maturity; several large-cap independents monetized their royalty interests in the public equity market. Improving cash management and managing volatility Given the current environment, companies are also seeking to improve their working capital management. One large oil company, which is a large user of the commercial paper (CP) market, significantly reduced its historically high cash balance by using it to fund a committed capital expenditure program. To ensure sufficient liquidity should the CP market fail to deliver funding at an attractive price, they have established sizable overnight lines with their cash banks. Companies are also focusing on their cash management and are seeking to gain real-time visibility into where their cash is, how fast it is concentrated and how it is invested. Consequently, companies are increasingly fine-tuning their cash management structures to unlock valuable internal sources of liquidity. Until oil and gas prices improve, commodity hedging will be stagnant.

However, when activity returns, larger energy names will reconsider their approach to hedging in order to reduce their revenue volatility and potentially boost their share prices. Consequently, while smaller companies will remain the most active, large cap producers are expected to increase their hedging in the future. . Lower for Longer: How Companies Are Adapting and Embedding Resilience | Adapting to “Lower for Longer” On a selective basis, some LNG buyers and producers are now considering hedging strategies in order to minimize volatility. Several have already executed LNG price hedges. As a market for LNG hedging emerges, companies need to be confident in the strength of their counterparties, particularly given the scale and tenor of LNG projects. As a LNG cargo trader, Citi brings insight into LNG market dynamics and provides additional liquidity to this emerging market. Working with a trusted advisor Companies active in the energy sector face challenging times and will have to make many tough investment decisions if prices remain low for a prolonged period, as is expected. Not all challenges are financial, of course.

Still, there is value in companies investigating their financing options and focusing on improving their cash and liquidity management. Citi is an important player in both energy finance and transaction services and understands the issues that companies must address. Most significantly, Citi has an energy industry-dedicated team with experience, expertise, tools and solutions to help companies overcome specific challenges. By working with a trusted advisor, companies can navigate the difficult times ahead and ensure they remain on track to meet their strategic objectives. 7 As a LNG cargo trader, Citi brings insight into LNG market dynamics and provides additional liquidity to this emerging market. Citi is an important player in both energy finance and transaction services and understands the issues that companies must address. .

8 Institutional Clients Group Building a Resilient Treasury for 2016 At a time when energy companies are already undertaking major cost and portfolio restructuring due to the collapse of oil prices, the pace of regulatory, tax, economic and geopolitical changes are creating new headwinds. Peter Langshaw Managing Director, Global Sector Sales Head for Energy, Power, Chemicals & Metals and Mining, Treasury and Trade Solutions, Citi Treasurers are having to play a major role in steering the business through choppy regulatory and economic waters. In particular, the numerous regulatory changes occurring across geographies, which are not always synchronized, are affecting the ability of companies to optimize their organization’s global treasury strategy. Furthermore, the ‘Balkanization’ of financial markets is also reshaping how banks interact with their clients. In response, treasurers are quickly becoming more market/regulatory-oriented and flexible to embed resilience into their treasury strategy, writes Peter Langshaw, Managing Director, Global Sector Sales Head for Energy, Power, Chemicals & Metals and Mining, Citi Treasury and Trade Solutions. Changing Regulatory and Environmental Forces: A Treasurer’s Dilemma Over the past decade, treasurers have put in place fixed strategies to rationalize, centralize and standardize cash management processes to improve liquidity, operational efficiency, enhance working capital and mitigate risks. These efforts have provided a solid foundation for treasury management and continue to be best practices globally.

Indeed, these efforts have been intensified in recent months, driven by the need to drastically cut capital expenditure (CAPEX) and operating expenses (OPEX) to reduce cost and debt. More recently, companies are facing an unintended new set of cross-border business challenges derived from market shifts, government and policy intervention. Basel III and Dodd-Frank, for example, are having a significant impact on how companies manage their traditional bank relationships and investment strategies. Under Basel III, banks now compete for companies’ cash flow operating accounts to improve risk-returns, therefore enabling them to maximize the interest yield they can return to treasurers. A large oil company operating in Latin America, for instance, has had to re-categorize their operating accounts and apportion them to their major deposit taking global banks to receive the highest possible returns under the new regulatory regime.

In other cases, monetary policy changes in Europe have resulted in negative interest rates for certain currencies. Basel III is redefining how banks are managing their financing efforts. Alternative funding sources and the flexibility to leverage other liquidity techniques, such as pre-export financing, commodity trade finance, export agency financing and structured trade finance, are becoming increasingly important, especially as the traditional debt capital markets tighten and bond spreads widen. Certain banks have developed designated oil programs to help finance using the trade flows, including discounting future cash flows from captive and third-party trading companies.

Additionally, the implementation of Basel III has different impacts on different markets. For example, in relation to European banks, some pooling providers, including EU-based banks, will be strongly affected by recent regulatory capital rules. Due to these capital requirement constraints, some banks may decide not to offer notional pooling in Europe. New regulations in Europe, which have the objective of increasing transparency in financial markets and clamping down on speculation and reduce systemic risk, are also coming into play. For instance, non-financial companies used to be exempt from the Markets in Financial Instruments Directive 1 (or MiFID I), but this has now changed under MiFID II.

This new . Lower for Longer: How Companies Are Adapting and Embedding Resilience | Building a Resilient Treasury for 2016 regulation is bringing many commodity trading companies into full regulatory scope; which requires them to hold regulatory capital and liquidity and be subject to regulatory oversight by their local authorities. There are caveats and exemptions to this, depending on the specific activities of these firms and a detailed review will be needed to establish what will be required. At the same time, companies will have to restructure their financial processes globally in order to successfully navigate between the U.S. Dodd-Frank and the European rules about derivatives trading and reporting. Alternative funding sources and the flexibility to leverage other liquidity techniques, such as pre-export financing and structured trade finance, are becoming increasingly important. Another global trend is playing out in the context of tax transparency.

This is being driven by the Organization for Economic Co-operation and Development (OECD) Base Erosion and Profit Shifting (BEPS) initiative as well as the OECD’s Common Reporting and Due Diligence Standard (CRS) and will require corporates to revisit the way they operate their tax and liquidity structures to allow countries to tax local profits. Diagram 1: Changing Environmental Forces Geopolitical Markets Economic Currency Fluctuations Global Treasury Strategy Taxes Subsidies Regulatory Commodities Price Fiscal Creep Globally Resilient Treasury 9 . 10 Institutional Clients Group Changing Local Landscapes In the same vein, at the local country level, fast changing landscapes have become the norm, especially in the emerging markets – where many countries are facing significant economic slowdown, local currency devaluation and regulatory and fiscal reforms. These changing local landscapes can create new business opportunities or challenges for corporations. In Brazil, for example, there have been both prizes and pitfalls from a treasury standpoint. On one hand, Brazil is now offering attractive investment opportunities for investors, with over $13 billion of Petrobras assets for sale started in 2015 and continuing into 2016. On the other, the corporate income tax system is now having new implications for the financial revenues of non-financial companies.

In Argentina, the recently elected government ended four years of foreign exchange (FX) controls with the aims of streamlining imports/exports and increasing investors’ confidence in the economy. From a treasury perspective, this measure is expected to facilitate the repatriation of capital. In the United States, the Federal Reserve raised the interest rate for the first time in a decade. This rate increase and the likelihood of additional increases in 2016 will generate additional challenges for corporations with significant exposure to emerging markets, as profits will be impacted by the raise of the value of the U.S.

dollar against emerging markets’ local currencies. In Mexico, the passing of the landmark Energy Reform in December 2013 ended the Mexican government’s monopoly on the oil, petrochemical and power generation sectors. These structural reforms are aimed at increasing productivity and the efficiency of the energy sector by attracting private investment.

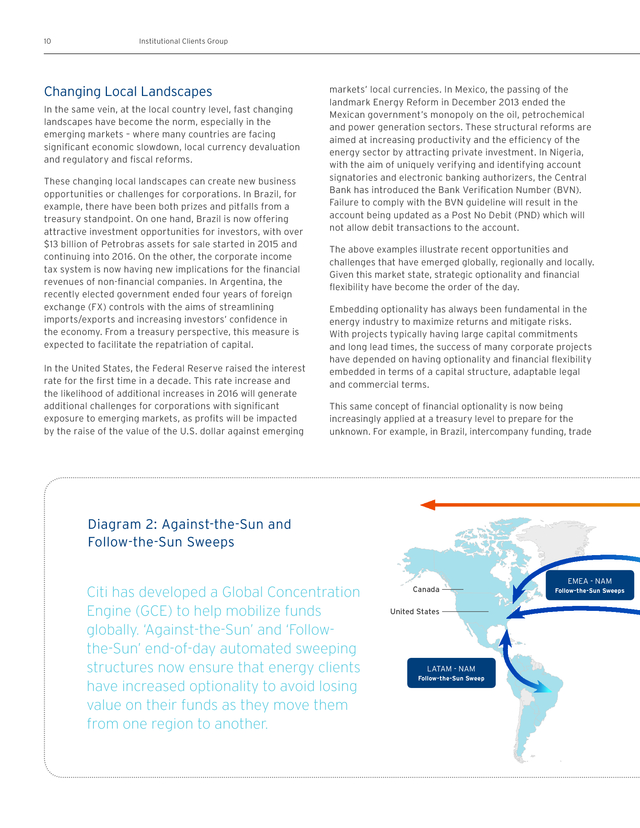

In Nigeria, with the aim of uniquely verifying and identifying account signatories and electronic banking authorizers, the Central Bank has introduced the Bank Verification Number (BVN). Failure to comply with the BVN guideline will result in the account being updated as a Post No Debit (PND) which will not allow debit transactions to the account. The above examples illustrate recent opportunities and challenges that have emerged globally, regionally and locally. Given this market state, strategic optionality and financial flexibility have become the order of the day. Embedding optionality has always been fundamental in the energy industry to maximize returns and mitigate risks. With projects typically having large capital commitments and long lead times, the success of many corporate projects have depended on having optionality and financial flexibility embedded in terms of a capital structure, adaptable legal and commercial terms. This same concept of financial optionality is now being increasingly applied at a treasury level to prepare for the unknown. For example, in Brazil, intercompany funding, trade Diagram 2: Against-the-Sun and Follow-the-Sun Sweeps Citi has developed a Global Concentration Engine (GCE) to help mobilize funds globally. ‘Against-the-Sun’ and ‘Followthe-Sun’ end-of-day automated sweeping structures now ensure that energy clients have increased optionality to avoid losing value on their funds as they move them from one region to another. Canada United States LATAM - NAM Follow-the-Sun Sweep EMEA - NAM Follow-the-Sun Sweeps .

Lower for Longer: How Companies Are Adapting and Embedding Resilience | Building a Resilient Treasury for 2016 finance techniques (pre-export financing or discounting of international receivables) or FDIC (Fundos de Investimento em Direitos Creditórios) structures all provide different liquidity options with major contractual implications. By partnering with global banks with strong local capabilities, treasurers can increase their strategic flexibility and leverage them as their ’eyes and ears’ on the ground. cash techniques such as interest optimization assures companies are maximizing returns globally. While gaining control over global cash is important, having in place a flexible global cash management structure that can quickly be adapted to changing market conditions, and is therefore more resilient to changing regulatory landscapes, is critical. Discounting of trade receivables and risk participation have also been widely used to boost liquidity. 2. Focus on Restructuring and Operational Efficiency Treasury Techniques for Increasing Resilience 1. Optimizing Visibility and Control over Global Cash Faced with significant currency devaluations in the emerging markets, many treasurers are responding by holding their liquidity and operating accounts offshore in U.S. dollars and relying less on local currency accounts. Energy companies have been relentless in seeking visibility and control of global cash so that they can mobilize it to where it is most needed and optimize returns for the company.

To help with this quest, Citi has developed a Global Concentration Engine (GCE) to help mobilize funds globally. ‘Against-the-Sun’ and ‘Follow-the-Sun’ end-of-day automated sweeping structures now ensure that energy clients have increased optionality to avoid losing value on their funds as they move them from one region to another. This is becoming increasingly important as investment and oil trading patterns change more directionally from West to East.

In addition, trapped Many companies have re-engineered their key end-toend financial processes to drive operational excellence and straight-through processing (STP) across their key financial processes. This has helped release important cash flows by improving general administrative expenses (G&As) and working capital efficiencies. Where trading models allow, a greater adoption of shared service centers (SSC) continue to be an important method to drive down OPEX.

‘Offshoring’ (i.e. outsourcing) and restructuring less critical processes and roles has also been at the forefront of reducing costs through reduced headcount and overhead. Rationalizing banking relationships and the use of efficient payment methods continues.

Furthermore, since Travel and Entertainment normally represents the third largest controllable expense, energy companies are looking to adopt a single global commercial card platform, which can be leveraged to significantly reduce payment and administrative costs. Shell, for example, operates on England Citi presence EMEA Follow-the-Sun Sweep Direction of the Sun Japan (east to west) Hong Kong Follow-the-Sun sweep (east to west) Dubai EMEA - APAC Against-the-Sun Sweep Singapore Against-the-Sun sweep (west to east) 11 . 12 Energy companies continue to reduce assets and debt in order to reshape portfolios and to safeguard ratings and profitability. Institutional Clients Group one global card platform in over 40 countries with over 50,000 cardholders. Over 10,000 man days have been saved by implementing this platform. Moreover, they have been able to determine the suppliers global spend to renegotiate prices, leverage process benefits and economies of scale. 3. Leveraging Bank Connectivity and Digitalization Bank integration needs are evolving quickly as treasurers are looking to do more with less and adapt global market standards and bank agnostic solutions which provide more flexibility.

More specifically, they are looking to optimize investments already made in technology and software solutions. With banking and treasury technology solutions advancing daily, treasurers are selecting platforms that are truly global in nature and can deliver a consistent, standardized and automated experience across all geographies and superior reconciliation capabilities. Two such examples include: 1) Alliance Lite2 service which SWIFT has developed.

This facilitates connectivity and integration with multiple banks through a single connection, and; 2) The emergence of a global market standard for formats such as ISO 20022 XML which provides richer information for streamlining reconciliations and facilitating straight-through processing between banks. Where treasury resources are at premium, mobile technology including tablets and smart phones are on the rise and are now being increasingly used to access banking services on the go. For instance, mobile users with Citi have approved US$800 billion worth of transactions since 2011. Streamlining bank analytics is another widely used tool in this environment to automate and simplify reporting with the view of moving towards a real-time balance sheet. Global solutions that simplify and accelerate bank integration are helping energy companies significantly reduce the costs, time and technology resources required to implement bank connectivity.

Indeed, projects that typically took 12 to 18 months to implement now often take two to three months. Some of these important advances around implementation tools designed to accelerate and streamline implementation include Citi’s ERP Integrator, which physically extracts files and has a hard code that helps standardize and reduce the need for writing codes to effect the integration. At an industry level, the Financial Services Network has been launched by SAP to enable integration between a SAP system and banks. More recently, SWIFT’s MyStandards is a service which has been designed and developed with the guidance and insight from Citi and other firms. It provides an artificial test environment through the Readiness Portal to validate test files and messages online and receive instant feedback.

All these solutions mitigate the need for complex technical projects and accelerate project completion time compared to traditional integration projects and helps standards adoption and end-to-end digitalization. 4. Improving Working Capital With the price of oil plummeting, working capital has naturally reduced too. Nonetheless, improving working capital efficiency remains extremely important to provide cash flows. Renegotiating input costs with suppliers has been a key strategy for energy companies.

At the same time, they are looking to help strategic suppliers weather the storm through supplier financing programs managed by banks. Citi has developed tailored global supplier finance programs to support oil companies and oil trading companies. One variation is Dynamic Discounting whereby buyers can use their own balance sheet or excess cash to generate additional purchasing discount and yield; whilst supporting sellers to reduce working capital and get paid earlier.

Another technique that is quickly being adopted by oil companies to reduce bank costs is the deployment of global umbrella credit facilities and pricing for guarantee facilities. Aside from lowering the cost of guarantees, these facilities help to improve liquidity and manage counterparty risk. Another key focus has been monetizing receivables to increase liquidity. 5.

Mitigating Risk and Alternative Financing Energy companies continue to reduce assets and debt in order to reshape portfolios and to safeguard ratings and profitability. Banks are helping post-merger and acquisition . Lower for Longer: How Companies Are Adapting and Embedding Resilience | Building a Resilient Treasury for 2016 integration by using Agency and Trust services. They are also providing important alternative debt financing structures, such as reservebased lending and commodity trade finance. An example of the latter is the $8.32 billion prepayment financing for Glencore and Vitol’s long-term crude oil purchases from one of Russia’s top crude oil producers. This was a landmark transaction for the energy sector and, since then, smaller financing structures are actively being pursued by some refiners. Off-balance sheet trade finance structures are also gaining interest. For example, Vivo Energy, a JV with Shell in Uganda with over 100 service stations, has greatly improved their cash flow and working capital. They have achieved this by securing early payments at no extra cost to Vivo through a structured bills discounting program.

As a result, the company can now potentially increase sales. Export Credit Agency (ECA) financing is a valuable way of diversifying funding sources and preserving bank lines and traditional debt capital markets. Typically, the agency may guarantee between 50% to 100% of the total financing and such facilities may not count against bank lines. In addition, governments, like Japan and China, have relied on ECAs to secure the supply of commodities, such as oil, through pre-export financing structures (relying on guarantees and co-lending from such agencies as Japan Bank for International Cooperation (JBIC) and Development Bank of Japan).

These programs are expected to expand in the future. As the emerging market economies are slowing, with some going into recession, the International Finance Corporation (IFC), a member of the World Bank Group, and Citi recently announced the signing of a $1.2 billion risk-sharing facility to help stimulate the growth of trade in these markets and to support economic development. IFC and Citi will use the funding to expand the availability of trade credit for companies, thereby supporting additional trade flows of more than $6 billion through 2019. 13 Leveraging Citi’s Globally Powered Network In summary, it is difficult to predict when and where the next regulatory and market challenges will occur. However, continuing to have a disciplined market-oriented approach and a global banking partner that can deliver seamless and flexible solutions, locally, regionally and globally, is critical. This helps avoid treasury strategies from becoming fragmented and sub-optimal, as the Balkanization of financial and banking regulations continues. Citi’s presence in over 100 countries, coupled with our local industry expertise, can help treasurers build a resilient treasury for the future. By partnering with global banks with strong local capabilities, treasurers can increase their resilience and leverage them as their ‘eyes and ears’ on the ground. .

. . IMPORTANT DISCLOSURES Citigroup Global Markets Inc. (“Citi”) is a registered broker-dealer in the United States. It is a member of Citigroup Inc. and is affiliated with Citibank, N.A.

and its subsidiaries and branches worldwide (collectively “Citibank”). Despite those affiliations, securities recommended, offered, sold by, or held at, Citi: (i) are not insured by the Federal Deposit Insurance Corporation; (ii) are not deposits or other obligations of any insured depository institution (including Citibank); and (iii) are subject to investment risks, including the possible loss of the principal amount invested. This material has been prepared by members of Citi’s Investment Banking Department and may include excerpts of other materials which have been previously been made available to other third parties. Although this publication may make reference to research reports that have been prepared and distributed by Citi and/or its affiliates, this publication has not been prepared by research personnel and the information provided herein is not intended to constitute “research” as that term is defined by applicable regulatory authorities.

The information contained in this publication is based on generally available information and, although obtained from sources believed to be reliable, its accuracy and completeness is not guaranteed. This material has been provided for informational purposes only, without regard to any particular user’s investment objectives, financial situation, or means. It does not constitute advice on investments or an offer or solicitation to purchase or sell any financial instruments.

Certain transactions and trading strategies, including those involving futures, options, and high-yield securities, give rise to substantial risk and are not suitable for all investors. No liability whatsoever is accepted for any loss (whether direct, indirect or consequential) that may arise from any use of the information contained in or derived from this publication. Past performance is not an indication of future returns. This publication is proprietary to Citi and any copying or distribution to a third party without the prior written consent of Citi and without the inclusion of the appropriate disclaimers as approved by Citi’s internal legal counsel is strictly prohibited. Citi does not provide tax or legal advice.

Any discussion of tax matters in this publication (i) is not intended to be used, and cannot be used or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the “promotion or marketing” of the matters discussed herein. Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor. Citi may have a role in connection with some of the transactions mentioned in this report. Institutional Clients Group icg.citi.com © 2016 Citigroup Global Markets Inc.

All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world. 1383308 GTS26553 01/16 .

Mr. Reilly is a member of the Global Operating Committee of the Corporate Bank and of the U.S. Management Committee of the Corporate and Investment Bank.

He is the Business Senior Credit Officer Level 2, Business Industry Specialist for Energy and the Global Coordinator/Americas Regional Head for Capital Approval/Allocation for Energy. Mr. Reilly has a Bachelor’s of Science in Business Administration from Villanova University in Pennsylvania and a Masters of Business Administration in Finance from The American University in Washington, D.C. Mr. Langshaw is responsible for executing a global sales strategy that delivers solutions for the treasury and working capital needs of energy clients worldwide for Citi’s TTS business.

He has held various senior international management positions at country, regional and global levels across five different continents. Prior to joining Citi, he worked internationally for eight years for a large U.S. international oilfield service company, which culminated in being appointed as Base Manager in Brunei with full profit and loss (P&L) responsibility, overseeing three countries. Peter Langshaw Managing Director, Global Sector Sales Head for Energy, Power, Chemicals & Metals and Mining, Treasury and Trade Solutions, Citi Mr.

Langshaw joined Citi’s Pan-European cash management team and was later based in Singapore, pioneering regional treasury structures in Asia. He then transitioned into Corporate Banking as the subsidiaries Banking Head in Singapore, where he launched and ran the Regional Account Management (RAM) banking team covering Southeast Asia. He was later appointed Corporate Bank Head and Acting Country Head in Vietnam.

After being promoted as Corporate and Bank Head and Market Manager for the Southern Region in Australia, he took up the post of Corporate and Investment Bank Head for Saudi Arabia (Central Region). In 2004, he accepted a position as Director of Multinationals and Transactional Banking for Africa and Middle East region with Barclays. In 2006, he returned to Citi as the Regional TTS Industry Head for Energy, Power, Chemicals and Mining. Later he was appointed Global Sector Sales Head based in Brazil.

He now works in the USA, where, in addition to his global role, he has extended responsibilities for Industrial clients in Latin America. Peter holds an MBA from Manchester Business School and a BA (Hons.) from the University of Nottingham in the UK. He has also attended an Executive Education Program at Harvard Business School. 3 . 4 Institutional Clients Group Adapting to “Lower for Longer” Low commodity prices in 2015 prompted energy companies to drastically revise their operational, capital expenditure, finance and risk management plans. Industry-wide, capital expenditures fell an estimated 45% in 2015 versus 2014. For 2016, the outlook suggests continuing frugality as the prevailing industry view is for oil and gas prices to remain “lower for longer.” As one way to partially address these challenges, companies can seek support and advice from their banks, writes Jim Reilly, Vice Chairman and Global Head of Energy Corporate Banking at Citi. Jim Reilly Vice Chairman and Global Head of Energy Corporate Banking, Citi The dramatic fall in commodity prices since the fourth quarter of 2014 has rewritten the playbook for energy companies. While the upstream and oilfield service segments of the industry have been the most severely impacted, no segment has escaped pain. The WTI and Brent benchmark oil prices finished 2015 at roughly $37 per barrel.

Most observers expect WTI to average between $39 and $49 per barrel in the coming year, with Brent running $3-$5 per barrel higher. At the bullish end of that range, oil prices would firm up in the second half of 2016; at the bearish end, strength would come instead in 2017. Henry Hub natural gas prices were similarly depressed at year-end. With a huge resource base, high inventories and unseasonably warm weather this winter, neither the immediate nor the long-term outlook is bullish for natural gas pricing.

In concert, demand for drilling rigs, oilfield services and equipment and labor has plummeted. In such an environment, both large and small companies face significant challenges. Some weaker oil and gas players have already filed for bankruptcy, and credit ratings and outlooks across the industry have been broadly reduced. All companies are reconsidering how they manage their cash and liquidity and capital programs, as well as the most efficient manner to fund them. While energy companies will undoubtedly experience challenges in the coming months, it is important to recognize that support and advice are available.

As cash becomes tighter, Citi can help corporates manage their liquidity with a wide range of solutions. Moreover, while the backdrop of low commodity prices makes it harder to raise financing, there are a number of alternatives available. A prolonged period of low oil prices The current low oil price, which is expected to rise only moderately in 2016 and 2017, has a number of supply and demand drivers – none of which are likely to disappear in the short term. The American shale revolution fundamentally changed the oil supply equation, as it had done earlier with natural gas, with the United States now among the top oil producers globally. Supply has also increased from Canada, Russia, Iraq, Kuwait, Saudi Arabia and deep-water sources, and it may soon be augmented by exports from Iran. Unlike times in the recent past, OPEC – or, really, Saudi Arabia – has refused to cut production to rebalance the market.

At the same time, modest growth in the United States, and sluggish economies in Europe and Latin America have led to lower . Lower for Longer: How Companies Are Adapting and Embedding Resilience | Adapting to “Lower for Longer” demand. And in China, where the economy is still expanding faster than in the rest of the world, energy demand is lower than anticipated even a year ago. The result is that the world is currently producing over a million barrels of oil per day more than is being consumed. While this oversupply is unlikely to change dramatically in the near term, there are several significant variables in the medium term: U.S. production decline, already underway, is likely to accelerate; Saudi Arabia may decide that lower production is a price worth paying to buoy prices; demand in China could pick up if the economic growth rate increases; and, in the background, the prospect of geopolitical shock remains. The implications of lower prices At current production volumes, the oil price fall has led to a drop in revenues across the industry of around $1.5 trillion a year. While falling revenues have been cushioned by lower service costs, the meticulous management of expenses, and productivity gains, this represents only a fraction of lost revenues.

The resulting drop in operating cash flows has prompted a steep decline in capital expenditures among upstream companies. Larger oil and gas producers are necessarily better placed to weather the decline in revenues. Smaller producers, many of which are backed by private equity firms and are highly leveraged, will face greater challenges as their capital structures were predicated on high oil and gas prices. At current prices, many companies are not viable – already, a number of bankruptcies of small companies have occurred in the United States.

Along with producers, the impact of lower commodity prices has hit the oilfield services segment the hardest. To date, midstream and downstream companies have fared reasonably well. Small and medium-sized producers typically borrow via Reserve-Based Lending (RBL) bank facilities, a type of secured financing specific to the oil and gas business. Financing terms for the following six months are reset based on current oil prices and production outlooks.

The 2015 resets reduced funding availability by 1525%, on average. Most companies were able to absorb that liquidity decrease via reduced expenditures and, in some cases, other debt and/or equity financing. However, lower prices will mean even further reductions in borrowing availability.

With a historically low percentage of production hedged, there will be few gains to offset low prices. Many companies could face a liquidity shortfall, which may accelerate industry consolidation and increase the number of bankruptcies. In the liquefied natural gas (LNG) industry, the impact of lower oil prices is more nuanced. LNG prices are typically linked to a basket of oil prices under long-term supply agreements. Therefore, the slump in oil prices has dragged down LNG prices. Unlike oil, natural gas trades at different prices around the world.

The arbitrage between U.S. and Asian and European LNG prices offsets the cost of specialized facilities and ships. However, the decline in oil prices has resulted in this arbitrage shrinking, undermining the viability of the market. The cost of LNG facilities and ships is immense and these projects can take years to build, with cost overruns being a common problem.

The elimination of a comfortable arbitrage between U.S. and Asian and European gas prices introduces significant risk into the LNG market that may stifle investment, at least in the short term. While declines in LNG prices will undoubtedly cause disruption, the impact of price changes will be lessened to some extent by the predicted long-term growth in LNG demand and the inevitable reduction in development costs driven by lower near-term demand. LNG is seen as a source of cleaner energy and has therefore been prioritized by governments over more polluting fossil fuels, such as coal.

As a result of this anticipated long-term demand, many planned liquefaction and transportation facilities will be built, although the timescale for their completion is likely to be pushed out. 5 The world is currently producing over a million barrels of oil per day more than is being consumed. While this oversupply is unlikely to change dramatically in the near term, there are several significant variables in the medium term. . 6 Institutional Clients Group Adapting to weaker revenues The sharp fall in revenues has increased companies’ focus on liquidity. The largest firms have the greatest flexibility and many have already increased the size of their banking facilities or tapped the investment grade bond market. Before markets stalled, smaller companies accessed high yield, second lien, and equity markets in order to augment liquidity. As financing conditions become tougher, and traditional sources of finance such as the bank, bond and equity markets become harder to access, energy companies are increasingly turning to alternative sources of finance, which can take into account their capital structures, improve their credit profiles, and support greater financial flexibility. Alternative sources of capital include volumetric production payments, project finance, export agency finance, supplier finance and asset-based lending, the latter typically against receivables and inventory. Strategic alternatives, although made more difficult by an uncertain market, also provide a capital source; these include divestitures, corporate spinoffs, and subsidiary IPOs such as master limited partnerships (MLPs).

Even larger companies are innovating: an oil major raised billions by issuing a hybrid bond; a national oil company sold a “century bond” with a hundred-year maturity; several large-cap independents monetized their royalty interests in the public equity market. Improving cash management and managing volatility Given the current environment, companies are also seeking to improve their working capital management. One large oil company, which is a large user of the commercial paper (CP) market, significantly reduced its historically high cash balance by using it to fund a committed capital expenditure program. To ensure sufficient liquidity should the CP market fail to deliver funding at an attractive price, they have established sizable overnight lines with their cash banks. Companies are also focusing on their cash management and are seeking to gain real-time visibility into where their cash is, how fast it is concentrated and how it is invested. Consequently, companies are increasingly fine-tuning their cash management structures to unlock valuable internal sources of liquidity. Until oil and gas prices improve, commodity hedging will be stagnant.

However, when activity returns, larger energy names will reconsider their approach to hedging in order to reduce their revenue volatility and potentially boost their share prices. Consequently, while smaller companies will remain the most active, large cap producers are expected to increase their hedging in the future. . Lower for Longer: How Companies Are Adapting and Embedding Resilience | Adapting to “Lower for Longer” On a selective basis, some LNG buyers and producers are now considering hedging strategies in order to minimize volatility. Several have already executed LNG price hedges. As a market for LNG hedging emerges, companies need to be confident in the strength of their counterparties, particularly given the scale and tenor of LNG projects. As a LNG cargo trader, Citi brings insight into LNG market dynamics and provides additional liquidity to this emerging market. Working with a trusted advisor Companies active in the energy sector face challenging times and will have to make many tough investment decisions if prices remain low for a prolonged period, as is expected. Not all challenges are financial, of course.

Still, there is value in companies investigating their financing options and focusing on improving their cash and liquidity management. Citi is an important player in both energy finance and transaction services and understands the issues that companies must address. Most significantly, Citi has an energy industry-dedicated team with experience, expertise, tools and solutions to help companies overcome specific challenges. By working with a trusted advisor, companies can navigate the difficult times ahead and ensure they remain on track to meet their strategic objectives. 7 As a LNG cargo trader, Citi brings insight into LNG market dynamics and provides additional liquidity to this emerging market. Citi is an important player in both energy finance and transaction services and understands the issues that companies must address. .

8 Institutional Clients Group Building a Resilient Treasury for 2016 At a time when energy companies are already undertaking major cost and portfolio restructuring due to the collapse of oil prices, the pace of regulatory, tax, economic and geopolitical changes are creating new headwinds. Peter Langshaw Managing Director, Global Sector Sales Head for Energy, Power, Chemicals & Metals and Mining, Treasury and Trade Solutions, Citi Treasurers are having to play a major role in steering the business through choppy regulatory and economic waters. In particular, the numerous regulatory changes occurring across geographies, which are not always synchronized, are affecting the ability of companies to optimize their organization’s global treasury strategy. Furthermore, the ‘Balkanization’ of financial markets is also reshaping how banks interact with their clients. In response, treasurers are quickly becoming more market/regulatory-oriented and flexible to embed resilience into their treasury strategy, writes Peter Langshaw, Managing Director, Global Sector Sales Head for Energy, Power, Chemicals & Metals and Mining, Citi Treasury and Trade Solutions. Changing Regulatory and Environmental Forces: A Treasurer’s Dilemma Over the past decade, treasurers have put in place fixed strategies to rationalize, centralize and standardize cash management processes to improve liquidity, operational efficiency, enhance working capital and mitigate risks. These efforts have provided a solid foundation for treasury management and continue to be best practices globally.

Indeed, these efforts have been intensified in recent months, driven by the need to drastically cut capital expenditure (CAPEX) and operating expenses (OPEX) to reduce cost and debt. More recently, companies are facing an unintended new set of cross-border business challenges derived from market shifts, government and policy intervention. Basel III and Dodd-Frank, for example, are having a significant impact on how companies manage their traditional bank relationships and investment strategies. Under Basel III, banks now compete for companies’ cash flow operating accounts to improve risk-returns, therefore enabling them to maximize the interest yield they can return to treasurers. A large oil company operating in Latin America, for instance, has had to re-categorize their operating accounts and apportion them to their major deposit taking global banks to receive the highest possible returns under the new regulatory regime.

In other cases, monetary policy changes in Europe have resulted in negative interest rates for certain currencies. Basel III is redefining how banks are managing their financing efforts. Alternative funding sources and the flexibility to leverage other liquidity techniques, such as pre-export financing, commodity trade finance, export agency financing and structured trade finance, are becoming increasingly important, especially as the traditional debt capital markets tighten and bond spreads widen. Certain banks have developed designated oil programs to help finance using the trade flows, including discounting future cash flows from captive and third-party trading companies.

Additionally, the implementation of Basel III has different impacts on different markets. For example, in relation to European banks, some pooling providers, including EU-based banks, will be strongly affected by recent regulatory capital rules. Due to these capital requirement constraints, some banks may decide not to offer notional pooling in Europe. New regulations in Europe, which have the objective of increasing transparency in financial markets and clamping down on speculation and reduce systemic risk, are also coming into play. For instance, non-financial companies used to be exempt from the Markets in Financial Instruments Directive 1 (or MiFID I), but this has now changed under MiFID II.

This new . Lower for Longer: How Companies Are Adapting and Embedding Resilience | Building a Resilient Treasury for 2016 regulation is bringing many commodity trading companies into full regulatory scope; which requires them to hold regulatory capital and liquidity and be subject to regulatory oversight by their local authorities. There are caveats and exemptions to this, depending on the specific activities of these firms and a detailed review will be needed to establish what will be required. At the same time, companies will have to restructure their financial processes globally in order to successfully navigate between the U.S. Dodd-Frank and the European rules about derivatives trading and reporting. Alternative funding sources and the flexibility to leverage other liquidity techniques, such as pre-export financing and structured trade finance, are becoming increasingly important. Another global trend is playing out in the context of tax transparency.

This is being driven by the Organization for Economic Co-operation and Development (OECD) Base Erosion and Profit Shifting (BEPS) initiative as well as the OECD’s Common Reporting and Due Diligence Standard (CRS) and will require corporates to revisit the way they operate their tax and liquidity structures to allow countries to tax local profits. Diagram 1: Changing Environmental Forces Geopolitical Markets Economic Currency Fluctuations Global Treasury Strategy Taxes Subsidies Regulatory Commodities Price Fiscal Creep Globally Resilient Treasury 9 . 10 Institutional Clients Group Changing Local Landscapes In the same vein, at the local country level, fast changing landscapes have become the norm, especially in the emerging markets – where many countries are facing significant economic slowdown, local currency devaluation and regulatory and fiscal reforms. These changing local landscapes can create new business opportunities or challenges for corporations. In Brazil, for example, there have been both prizes and pitfalls from a treasury standpoint. On one hand, Brazil is now offering attractive investment opportunities for investors, with over $13 billion of Petrobras assets for sale started in 2015 and continuing into 2016. On the other, the corporate income tax system is now having new implications for the financial revenues of non-financial companies.

In Argentina, the recently elected government ended four years of foreign exchange (FX) controls with the aims of streamlining imports/exports and increasing investors’ confidence in the economy. From a treasury perspective, this measure is expected to facilitate the repatriation of capital. In the United States, the Federal Reserve raised the interest rate for the first time in a decade. This rate increase and the likelihood of additional increases in 2016 will generate additional challenges for corporations with significant exposure to emerging markets, as profits will be impacted by the raise of the value of the U.S.

dollar against emerging markets’ local currencies. In Mexico, the passing of the landmark Energy Reform in December 2013 ended the Mexican government’s monopoly on the oil, petrochemical and power generation sectors. These structural reforms are aimed at increasing productivity and the efficiency of the energy sector by attracting private investment.

In Nigeria, with the aim of uniquely verifying and identifying account signatories and electronic banking authorizers, the Central Bank has introduced the Bank Verification Number (BVN). Failure to comply with the BVN guideline will result in the account being updated as a Post No Debit (PND) which will not allow debit transactions to the account. The above examples illustrate recent opportunities and challenges that have emerged globally, regionally and locally. Given this market state, strategic optionality and financial flexibility have become the order of the day. Embedding optionality has always been fundamental in the energy industry to maximize returns and mitigate risks. With projects typically having large capital commitments and long lead times, the success of many corporate projects have depended on having optionality and financial flexibility embedded in terms of a capital structure, adaptable legal and commercial terms. This same concept of financial optionality is now being increasingly applied at a treasury level to prepare for the unknown. For example, in Brazil, intercompany funding, trade Diagram 2: Against-the-Sun and Follow-the-Sun Sweeps Citi has developed a Global Concentration Engine (GCE) to help mobilize funds globally. ‘Against-the-Sun’ and ‘Followthe-Sun’ end-of-day automated sweeping structures now ensure that energy clients have increased optionality to avoid losing value on their funds as they move them from one region to another. Canada United States LATAM - NAM Follow-the-Sun Sweep EMEA - NAM Follow-the-Sun Sweeps .

Lower for Longer: How Companies Are Adapting and Embedding Resilience | Building a Resilient Treasury for 2016 finance techniques (pre-export financing or discounting of international receivables) or FDIC (Fundos de Investimento em Direitos Creditórios) structures all provide different liquidity options with major contractual implications. By partnering with global banks with strong local capabilities, treasurers can increase their strategic flexibility and leverage them as their ’eyes and ears’ on the ground. cash techniques such as interest optimization assures companies are maximizing returns globally. While gaining control over global cash is important, having in place a flexible global cash management structure that can quickly be adapted to changing market conditions, and is therefore more resilient to changing regulatory landscapes, is critical. Discounting of trade receivables and risk participation have also been widely used to boost liquidity. 2. Focus on Restructuring and Operational Efficiency Treasury Techniques for Increasing Resilience 1. Optimizing Visibility and Control over Global Cash Faced with significant currency devaluations in the emerging markets, many treasurers are responding by holding their liquidity and operating accounts offshore in U.S. dollars and relying less on local currency accounts. Energy companies have been relentless in seeking visibility and control of global cash so that they can mobilize it to where it is most needed and optimize returns for the company.

To help with this quest, Citi has developed a Global Concentration Engine (GCE) to help mobilize funds globally. ‘Against-the-Sun’ and ‘Follow-the-Sun’ end-of-day automated sweeping structures now ensure that energy clients have increased optionality to avoid losing value on their funds as they move them from one region to another. This is becoming increasingly important as investment and oil trading patterns change more directionally from West to East.

In addition, trapped Many companies have re-engineered their key end-toend financial processes to drive operational excellence and straight-through processing (STP) across their key financial processes. This has helped release important cash flows by improving general administrative expenses (G&As) and working capital efficiencies. Where trading models allow, a greater adoption of shared service centers (SSC) continue to be an important method to drive down OPEX.

‘Offshoring’ (i.e. outsourcing) and restructuring less critical processes and roles has also been at the forefront of reducing costs through reduced headcount and overhead. Rationalizing banking relationships and the use of efficient payment methods continues.

Furthermore, since Travel and Entertainment normally represents the third largest controllable expense, energy companies are looking to adopt a single global commercial card platform, which can be leveraged to significantly reduce payment and administrative costs. Shell, for example, operates on England Citi presence EMEA Follow-the-Sun Sweep Direction of the Sun Japan (east to west) Hong Kong Follow-the-Sun sweep (east to west) Dubai EMEA - APAC Against-the-Sun Sweep Singapore Against-the-Sun sweep (west to east) 11 . 12 Energy companies continue to reduce assets and debt in order to reshape portfolios and to safeguard ratings and profitability. Institutional Clients Group one global card platform in over 40 countries with over 50,000 cardholders. Over 10,000 man days have been saved by implementing this platform. Moreover, they have been able to determine the suppliers global spend to renegotiate prices, leverage process benefits and economies of scale. 3. Leveraging Bank Connectivity and Digitalization Bank integration needs are evolving quickly as treasurers are looking to do more with less and adapt global market standards and bank agnostic solutions which provide more flexibility.

More specifically, they are looking to optimize investments already made in technology and software solutions. With banking and treasury technology solutions advancing daily, treasurers are selecting platforms that are truly global in nature and can deliver a consistent, standardized and automated experience across all geographies and superior reconciliation capabilities. Two such examples include: 1) Alliance Lite2 service which SWIFT has developed.

This facilitates connectivity and integration with multiple banks through a single connection, and; 2) The emergence of a global market standard for formats such as ISO 20022 XML which provides richer information for streamlining reconciliations and facilitating straight-through processing between banks. Where treasury resources are at premium, mobile technology including tablets and smart phones are on the rise and are now being increasingly used to access banking services on the go. For instance, mobile users with Citi have approved US$800 billion worth of transactions since 2011. Streamlining bank analytics is another widely used tool in this environment to automate and simplify reporting with the view of moving towards a real-time balance sheet. Global solutions that simplify and accelerate bank integration are helping energy companies significantly reduce the costs, time and technology resources required to implement bank connectivity.

Indeed, projects that typically took 12 to 18 months to implement now often take two to three months. Some of these important advances around implementation tools designed to accelerate and streamline implementation include Citi’s ERP Integrator, which physically extracts files and has a hard code that helps standardize and reduce the need for writing codes to effect the integration. At an industry level, the Financial Services Network has been launched by SAP to enable integration between a SAP system and banks. More recently, SWIFT’s MyStandards is a service which has been designed and developed with the guidance and insight from Citi and other firms. It provides an artificial test environment through the Readiness Portal to validate test files and messages online and receive instant feedback.

All these solutions mitigate the need for complex technical projects and accelerate project completion time compared to traditional integration projects and helps standards adoption and end-to-end digitalization. 4. Improving Working Capital With the price of oil plummeting, working capital has naturally reduced too. Nonetheless, improving working capital efficiency remains extremely important to provide cash flows. Renegotiating input costs with suppliers has been a key strategy for energy companies.

At the same time, they are looking to help strategic suppliers weather the storm through supplier financing programs managed by banks. Citi has developed tailored global supplier finance programs to support oil companies and oil trading companies. One variation is Dynamic Discounting whereby buyers can use their own balance sheet or excess cash to generate additional purchasing discount and yield; whilst supporting sellers to reduce working capital and get paid earlier.

Another technique that is quickly being adopted by oil companies to reduce bank costs is the deployment of global umbrella credit facilities and pricing for guarantee facilities. Aside from lowering the cost of guarantees, these facilities help to improve liquidity and manage counterparty risk. Another key focus has been monetizing receivables to increase liquidity. 5.

Mitigating Risk and Alternative Financing Energy companies continue to reduce assets and debt in order to reshape portfolios and to safeguard ratings and profitability. Banks are helping post-merger and acquisition . Lower for Longer: How Companies Are Adapting and Embedding Resilience | Building a Resilient Treasury for 2016 integration by using Agency and Trust services. They are also providing important alternative debt financing structures, such as reservebased lending and commodity trade finance. An example of the latter is the $8.32 billion prepayment financing for Glencore and Vitol’s long-term crude oil purchases from one of Russia’s top crude oil producers. This was a landmark transaction for the energy sector and, since then, smaller financing structures are actively being pursued by some refiners. Off-balance sheet trade finance structures are also gaining interest. For example, Vivo Energy, a JV with Shell in Uganda with over 100 service stations, has greatly improved their cash flow and working capital. They have achieved this by securing early payments at no extra cost to Vivo through a structured bills discounting program.

As a result, the company can now potentially increase sales. Export Credit Agency (ECA) financing is a valuable way of diversifying funding sources and preserving bank lines and traditional debt capital markets. Typically, the agency may guarantee between 50% to 100% of the total financing and such facilities may not count against bank lines. In addition, governments, like Japan and China, have relied on ECAs to secure the supply of commodities, such as oil, through pre-export financing structures (relying on guarantees and co-lending from such agencies as Japan Bank for International Cooperation (JBIC) and Development Bank of Japan).

These programs are expected to expand in the future. As the emerging market economies are slowing, with some going into recession, the International Finance Corporation (IFC), a member of the World Bank Group, and Citi recently announced the signing of a $1.2 billion risk-sharing facility to help stimulate the growth of trade in these markets and to support economic development. IFC and Citi will use the funding to expand the availability of trade credit for companies, thereby supporting additional trade flows of more than $6 billion through 2019. 13 Leveraging Citi’s Globally Powered Network In summary, it is difficult to predict when and where the next regulatory and market challenges will occur. However, continuing to have a disciplined market-oriented approach and a global banking partner that can deliver seamless and flexible solutions, locally, regionally and globally, is critical. This helps avoid treasury strategies from becoming fragmented and sub-optimal, as the Balkanization of financial and banking regulations continues. Citi’s presence in over 100 countries, coupled with our local industry expertise, can help treasurers build a resilient treasury for the future. By partnering with global banks with strong local capabilities, treasurers can increase their resilience and leverage them as their ‘eyes and ears’ on the ground. .

. . IMPORTANT DISCLOSURES Citigroup Global Markets Inc. (“Citi”) is a registered broker-dealer in the United States. It is a member of Citigroup Inc. and is affiliated with Citibank, N.A.

and its subsidiaries and branches worldwide (collectively “Citibank”). Despite those affiliations, securities recommended, offered, sold by, or held at, Citi: (i) are not insured by the Federal Deposit Insurance Corporation; (ii) are not deposits or other obligations of any insured depository institution (including Citibank); and (iii) are subject to investment risks, including the possible loss of the principal amount invested. This material has been prepared by members of Citi’s Investment Banking Department and may include excerpts of other materials which have been previously been made available to other third parties. Although this publication may make reference to research reports that have been prepared and distributed by Citi and/or its affiliates, this publication has not been prepared by research personnel and the information provided herein is not intended to constitute “research” as that term is defined by applicable regulatory authorities.

The information contained in this publication is based on generally available information and, although obtained from sources believed to be reliable, its accuracy and completeness is not guaranteed. This material has been provided for informational purposes only, without regard to any particular user’s investment objectives, financial situation, or means. It does not constitute advice on investments or an offer or solicitation to purchase or sell any financial instruments.

Certain transactions and trading strategies, including those involving futures, options, and high-yield securities, give rise to substantial risk and are not suitable for all investors. No liability whatsoever is accepted for any loss (whether direct, indirect or consequential) that may arise from any use of the information contained in or derived from this publication. Past performance is not an indication of future returns. This publication is proprietary to Citi and any copying or distribution to a third party without the prior written consent of Citi and without the inclusion of the appropriate disclaimers as approved by Citi’s internal legal counsel is strictly prohibited. Citi does not provide tax or legal advice.

Any discussion of tax matters in this publication (i) is not intended to be used, and cannot be used or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the “promotion or marketing” of the matters discussed herein. Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor. Citi may have a role in connection with some of the transactions mentioned in this report. Institutional Clients Group icg.citi.com © 2016 Citigroup Global Markets Inc.

All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world. 1383308 GTS26553 01/16 .