Description

21 DECEMBER 2015

BLU PUTNAM, CHIEF ECONOMIST, CME GROUP

DAN BRUSSTAR, SENIOR DIRECTOR, ENERGY RESEARCH, CME GROUP

21 DECEMBER 2015

U.S. Crude oil export ban lifted

All examples in this report are hypothetical interpretations of situations and are used for explanation

purposes only. The views in this report reflect solely those of the authors and not necessarily those

of CME Group or its affiliated institutions. This report and the information herein should not be

considered investment advice or the results of actual market experience.

The U.S.

crude oil export ban was lifted in December 2015 as part of the legislation to fund the Government through September 2016. The export ban was imposed back in 1975 under the administration of President Gerald Ford, in the midst of public anxiety over the rising power of OPEC, reduced US influence over global economic conditions, and fears of slow growth and high inflation – then known as stagflation. In fact, through Presidential actions over the years and other rule changes, the ban was quite leaky, so to speak.

As a result, the short-term impact on oil prices of lifting the export ban is likely to be relatively small in terms of prices and not an important driver for production. Nevertheless, anytime frictions and barriers to free trade are removed the market price discovery process is made more robust and capital allocation more efficient. Hence, the lifting of the export ban is a positive factor for the role of U.S. oil (West Texas Intermediate, aka WTI) as a global benchmark.

Here we provide our perspective on some of the key questions being asked. Question #1: What has really changed? Under the old law, refined product was allowed for export. Crude oil exports required licenses. Effectively, crude oil could be exported to Canada and Mexico by permits, which were virtually automatically granted, as were re-exports of foreign-sourced oil, and some crude oil exports from California and Alaska. Moreover, the definition of refined product had been weakened in the last several years to include some lightly altered crude products (i.e., lighter condensate products).

With the lifting of the crude oil ban, U.S. producers now can export freely; however, do not expect much of a rise in exports of crude oil any time soon. Indeed, the sum of crude oil plus refined product exports is likely to remain more or less on its current trend for 2016-2017. Question #2: Will lifting the crude oil export ban result in greater U.S.

production? No. The low price environment for crude oil globally that commenced in Q4/2014 is still with us, and the longer-term expectation for price is the key driver of future production. China is still decelerating. Growth in emerging markets is slow.

Europe may grow 1% to 2% in real GDP terms, the U.S. a little better, and Japan a little less. No major demand surges here.

And, oil is largely a transportation fuel. Transportation is becoming steadily more energy efficient. In short, the demand situation does not support a return to a higher price environment. On the supply side, we do anticipate less US oil production in 2016, given the lack of investment in the sector in 2015 and the consensus view that the low oil price environment will extend for many years to come. Any drop in U.S.

and Canadian production in 2016, however, would be offset by increased production in the Middle East, including the arrival on world markets of more Iranian oil. Nevertheless, there will be some small benefits to U.S. producers based on the tighter Bakken-WTI spreads, because Bakken and other domestic sweet crudes will now have new export markets that will bring higher revenue overall. Question #3: What is the likely impact on Brent-WTI and other crude oil price spreads? As noted earlier, any policy change that removes market frictions and makes the connection among different sources of oil around the world more efficient will assist the robustness of the global oil price discovery process. Thus, the lifting of the US crude oil export ban could make an incremental difference in narrowing the spread between North Sea Brent and U.S.

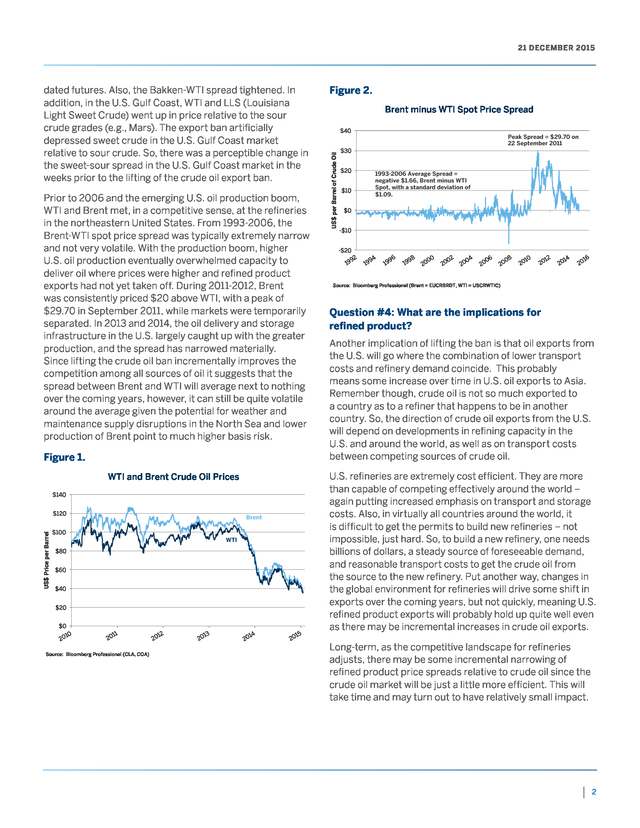

West Texas Intermediate (WTI). Indeed, in early December, amid news of the possibility that the crude oil export ban might be lifted, there were some price actions between different grades of crude. The WTI-Brent spread narrowed slightly in both spot and longer- 1 . 21 DECEMBER 2015 Prior to 2006 and the emerging U.S. oil production boom, WTI and Brent met, in a competitive sense, at the refineries in the northeastern United States. From 1993-2006, the Brent-WTI spot price spread was typically extremely narrow and not very volatile. With the production boom, higher U.S.

oil production eventually overwhelmed capacity to deliver oil where prices were higher and refined product exports had not yet taken off. During 2011-2012, Brent was consistently priced $20 above WTI, with a peak of $29.70 in September 2011, while markets were temporarily separated. In 2013 and 2014, the oil delivery and storage infrastructure in the U.S.

largely caught up with the greater production, and the spread has narrowed materially. Since lifting the crude oil ban incrementally improves the competition among all sources of oil it suggests that the spread between Brent and WTI will average next to nothing over the coming years, however, it can still be quite volatile around the average given the potential for weather and maintenance supply disruptions in the North Sea and lower production of Brent point to much higher basis risk. Figure 1. WTI and Brent Crude Oil Prices $140 US$ Price per Barrel $120 Brent $100 WTI $80 $60 $40 $20 $0 10 20 1 1 20 Source: Bloomberg Professional (CLA, COA) 2 1 20 3 1 20 14 20 5 1 20 Figure 2. Brent minus WTI Spot Price Spread $40 US$ per Barrel of Crude Oil dated futures. Also, the Bakken-WTI spread tightened. In addition, in the U.S.

Gulf Coast, WTI and LLS (Louisiana Light Sweet Crude) went up in price relative to the sour crude grades (e.g., Mars). The export ban artificially depressed sweet crude in the U.S. Gulf Coast market relative to sour crude.

So, there was a perceptible change in the sweet-sour spread in the U.S. Gulf Coast market in the weeks prior to the lifting of the crude oil export ban. Peak Spread = $29.70 on 22 September 2011 $30 $20 1993-2006 Average Spread = negative $1.66, Brent minus WTI Spot, with a standard deviation of $1.09. $10 $0 -$10 -$20 92 19 4 9 19 6 9 19 8 9 19 0 0 20 02 20 4 0 20 6 0 20 8 0 20 10 20 2 1 20 14 20 16 20 Source: Bloomberg Professional (Brent = EUCRBRDT, WTI = USCRWTIC) Question #4: What are the implications for refined product? Another implication of lifting the ban is that oil exports from the U.S. will go where the combination of lower transport costs and refinery demand coincide.

This probably means some increase over time in U.S. oil exports to Asia. Remember though, crude oil is not so much exported to a country as to a refiner that happens to be in another country. So, the direction of crude oil exports from the U.S. will depend on developments in refining capacity in the U.S.

and around the world, as well as on transport costs between competing sources of crude oil. U.S. refineries are extremely cost efficient. They are more than capable of competing effectively around the world – again putting increased emphasis on transport and storage costs.

Also, in virtually all countries around the world, it is difficult to get the permits to build new refineries – not impossible, just hard. So, to build a new refinery, one needs billions of dollars, a steady source of foreseeable demand, and reasonable transport costs to get the crude oil from the source to the new refinery. Put another way, changes in the global environment for refineries will drive some shift in exports over the coming years, but not quickly, meaning U.S. refined product exports will probably hold up quite well even as there may be incremental increases in crude oil exports. Long-term, as the competitive landscape for refineries adjusts, there may be some incremental narrowing of refined product price spreads relative to crude oil since the crude oil market will be just a little more efficient.

This will take time and may turn out to have relatively small impact. 2 . 21 DECEMBER 2015 Question #5: What is the state of the U.S. infrastructure for exporting crude oil? The lifting of the export ban will have the biggest impact in the U.S. Gulf Coast, and to a lesser extent on the West Coast/Alaska. The infrastructure for WTI exports in the U.S. Gulf Coast is already completed, and the U.S. is actively exporting some crude oil and lighter condensate products, not to mention all the NGLs such as propane (which use the same export terminals).

At this time, there is adequate capacity to handle any increases in export flow. 3 . .

crude oil export ban was lifted in December 2015 as part of the legislation to fund the Government through September 2016. The export ban was imposed back in 1975 under the administration of President Gerald Ford, in the midst of public anxiety over the rising power of OPEC, reduced US influence over global economic conditions, and fears of slow growth and high inflation – then known as stagflation. In fact, through Presidential actions over the years and other rule changes, the ban was quite leaky, so to speak.

As a result, the short-term impact on oil prices of lifting the export ban is likely to be relatively small in terms of prices and not an important driver for production. Nevertheless, anytime frictions and barriers to free trade are removed the market price discovery process is made more robust and capital allocation more efficient. Hence, the lifting of the export ban is a positive factor for the role of U.S. oil (West Texas Intermediate, aka WTI) as a global benchmark.

Here we provide our perspective on some of the key questions being asked. Question #1: What has really changed? Under the old law, refined product was allowed for export. Crude oil exports required licenses. Effectively, crude oil could be exported to Canada and Mexico by permits, which were virtually automatically granted, as were re-exports of foreign-sourced oil, and some crude oil exports from California and Alaska. Moreover, the definition of refined product had been weakened in the last several years to include some lightly altered crude products (i.e., lighter condensate products).

With the lifting of the crude oil ban, U.S. producers now can export freely; however, do not expect much of a rise in exports of crude oil any time soon. Indeed, the sum of crude oil plus refined product exports is likely to remain more or less on its current trend for 2016-2017. Question #2: Will lifting the crude oil export ban result in greater U.S.

production? No. The low price environment for crude oil globally that commenced in Q4/2014 is still with us, and the longer-term expectation for price is the key driver of future production. China is still decelerating. Growth in emerging markets is slow.

Europe may grow 1% to 2% in real GDP terms, the U.S. a little better, and Japan a little less. No major demand surges here.

And, oil is largely a transportation fuel. Transportation is becoming steadily more energy efficient. In short, the demand situation does not support a return to a higher price environment. On the supply side, we do anticipate less US oil production in 2016, given the lack of investment in the sector in 2015 and the consensus view that the low oil price environment will extend for many years to come. Any drop in U.S.

and Canadian production in 2016, however, would be offset by increased production in the Middle East, including the arrival on world markets of more Iranian oil. Nevertheless, there will be some small benefits to U.S. producers based on the tighter Bakken-WTI spreads, because Bakken and other domestic sweet crudes will now have new export markets that will bring higher revenue overall. Question #3: What is the likely impact on Brent-WTI and other crude oil price spreads? As noted earlier, any policy change that removes market frictions and makes the connection among different sources of oil around the world more efficient will assist the robustness of the global oil price discovery process. Thus, the lifting of the US crude oil export ban could make an incremental difference in narrowing the spread between North Sea Brent and U.S.

West Texas Intermediate (WTI). Indeed, in early December, amid news of the possibility that the crude oil export ban might be lifted, there were some price actions between different grades of crude. The WTI-Brent spread narrowed slightly in both spot and longer- 1 . 21 DECEMBER 2015 Prior to 2006 and the emerging U.S. oil production boom, WTI and Brent met, in a competitive sense, at the refineries in the northeastern United States. From 1993-2006, the Brent-WTI spot price spread was typically extremely narrow and not very volatile. With the production boom, higher U.S.

oil production eventually overwhelmed capacity to deliver oil where prices were higher and refined product exports had not yet taken off. During 2011-2012, Brent was consistently priced $20 above WTI, with a peak of $29.70 in September 2011, while markets were temporarily separated. In 2013 and 2014, the oil delivery and storage infrastructure in the U.S.

largely caught up with the greater production, and the spread has narrowed materially. Since lifting the crude oil ban incrementally improves the competition among all sources of oil it suggests that the spread between Brent and WTI will average next to nothing over the coming years, however, it can still be quite volatile around the average given the potential for weather and maintenance supply disruptions in the North Sea and lower production of Brent point to much higher basis risk. Figure 1. WTI and Brent Crude Oil Prices $140 US$ Price per Barrel $120 Brent $100 WTI $80 $60 $40 $20 $0 10 20 1 1 20 Source: Bloomberg Professional (CLA, COA) 2 1 20 3 1 20 14 20 5 1 20 Figure 2. Brent minus WTI Spot Price Spread $40 US$ per Barrel of Crude Oil dated futures. Also, the Bakken-WTI spread tightened. In addition, in the U.S.

Gulf Coast, WTI and LLS (Louisiana Light Sweet Crude) went up in price relative to the sour crude grades (e.g., Mars). The export ban artificially depressed sweet crude in the U.S. Gulf Coast market relative to sour crude.

So, there was a perceptible change in the sweet-sour spread in the U.S. Gulf Coast market in the weeks prior to the lifting of the crude oil export ban. Peak Spread = $29.70 on 22 September 2011 $30 $20 1993-2006 Average Spread = negative $1.66, Brent minus WTI Spot, with a standard deviation of $1.09. $10 $0 -$10 -$20 92 19 4 9 19 6 9 19 8 9 19 0 0 20 02 20 4 0 20 6 0 20 8 0 20 10 20 2 1 20 14 20 16 20 Source: Bloomberg Professional (Brent = EUCRBRDT, WTI = USCRWTIC) Question #4: What are the implications for refined product? Another implication of lifting the ban is that oil exports from the U.S. will go where the combination of lower transport costs and refinery demand coincide.

This probably means some increase over time in U.S. oil exports to Asia. Remember though, crude oil is not so much exported to a country as to a refiner that happens to be in another country. So, the direction of crude oil exports from the U.S. will depend on developments in refining capacity in the U.S.

and around the world, as well as on transport costs between competing sources of crude oil. U.S. refineries are extremely cost efficient. They are more than capable of competing effectively around the world – again putting increased emphasis on transport and storage costs.

Also, in virtually all countries around the world, it is difficult to get the permits to build new refineries – not impossible, just hard. So, to build a new refinery, one needs billions of dollars, a steady source of foreseeable demand, and reasonable transport costs to get the crude oil from the source to the new refinery. Put another way, changes in the global environment for refineries will drive some shift in exports over the coming years, but not quickly, meaning U.S. refined product exports will probably hold up quite well even as there may be incremental increases in crude oil exports. Long-term, as the competitive landscape for refineries adjusts, there may be some incremental narrowing of refined product price spreads relative to crude oil since the crude oil market will be just a little more efficient.

This will take time and may turn out to have relatively small impact. 2 . 21 DECEMBER 2015 Question #5: What is the state of the U.S. infrastructure for exporting crude oil? The lifting of the export ban will have the biggest impact in the U.S. Gulf Coast, and to a lesser extent on the West Coast/Alaska. The infrastructure for WTI exports in the U.S. Gulf Coast is already completed, and the U.S. is actively exporting some crude oil and lighter condensate products, not to mention all the NGLs such as propane (which use the same export terminals).

At this time, there is adequate capacity to handle any increases in export flow. 3 . .