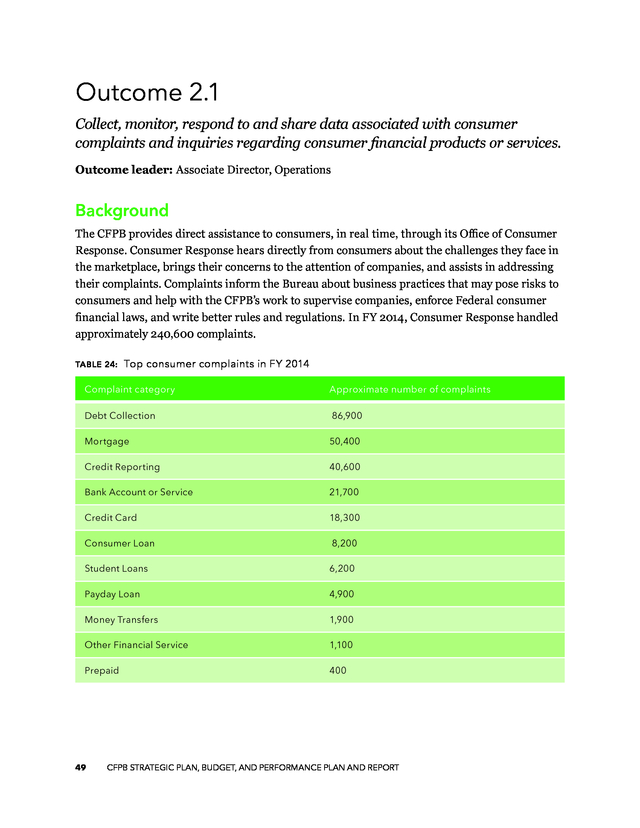

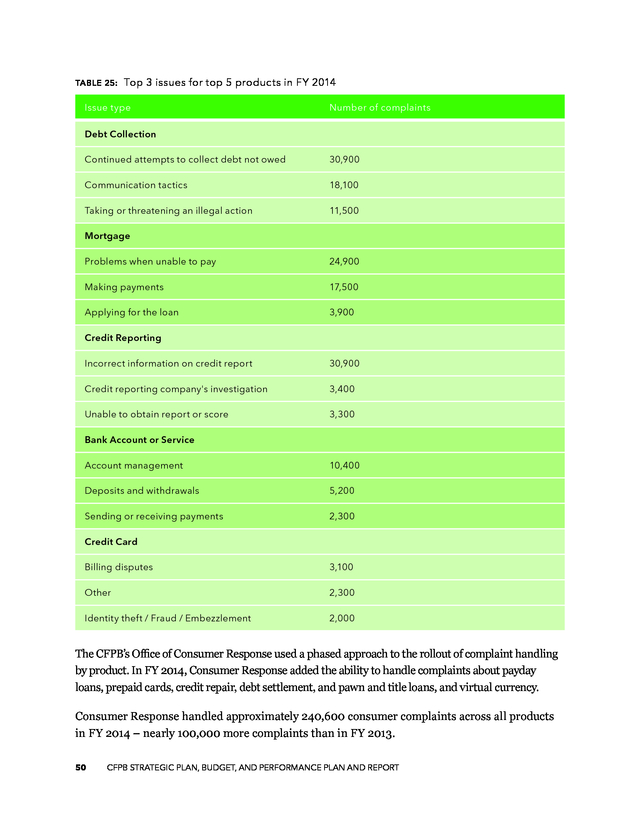

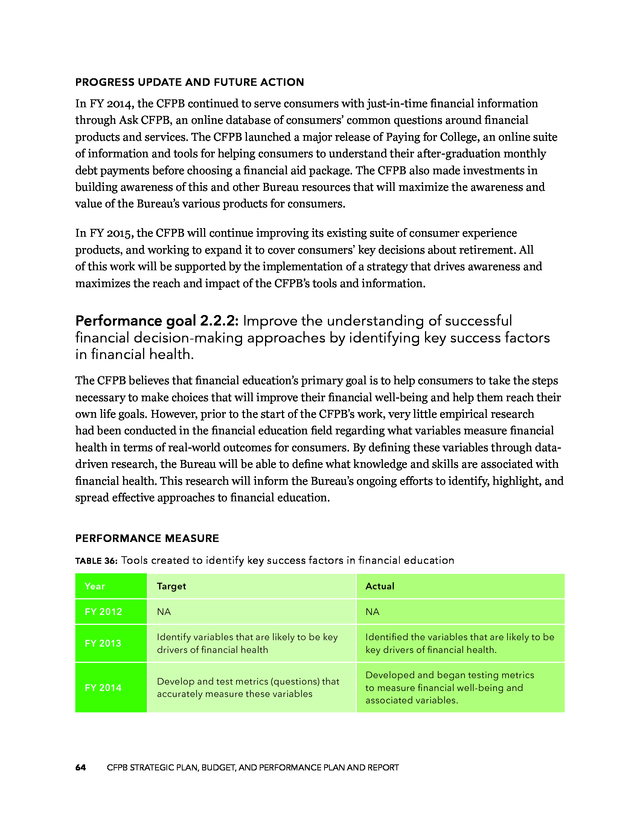

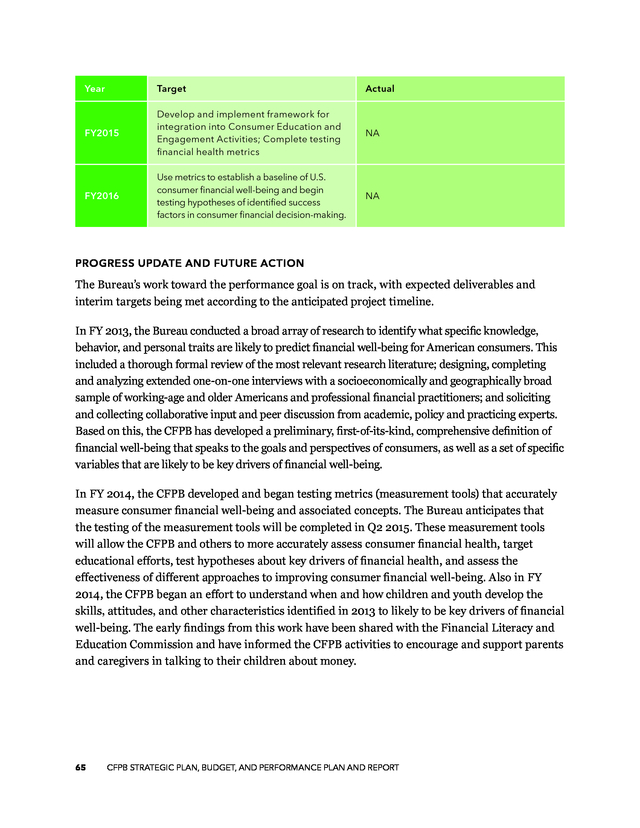

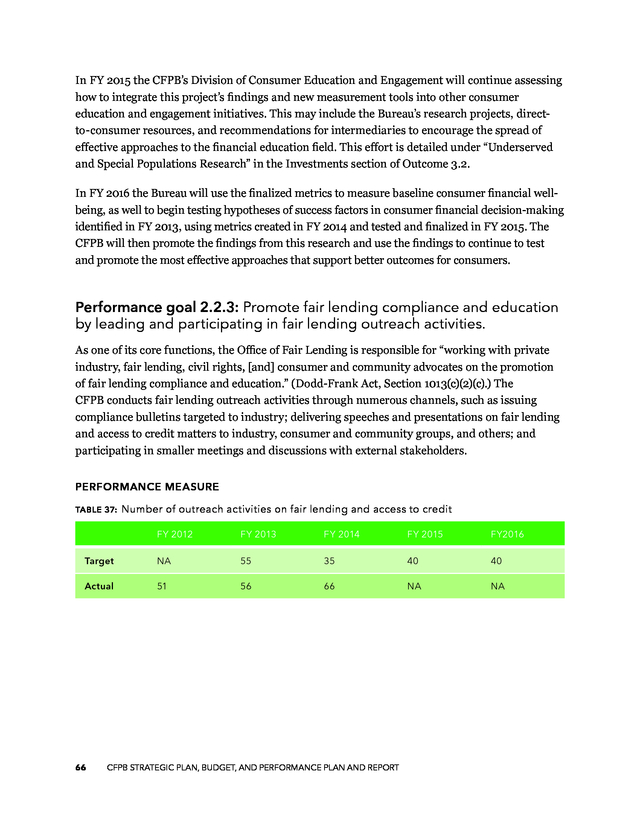

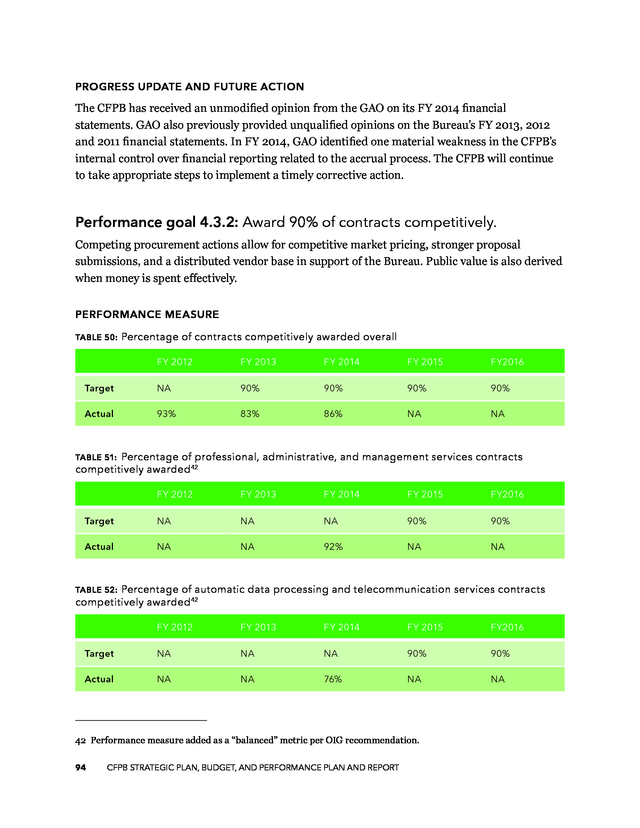

Description

February 2015

The CFPB strategic plan,

budget, and performance

plan and report

Consumer Financial

Protection Bureau

. Table of Contents

Letter from the Director.........................................................................................................4

Overview of the CFPB............................................................................................................6

Plan Overview........................................................................................................................10

Budget Overview..................................................................................................................11

Bureau Fund...................................................................................................... 11

Budget by strategic goal..................................................................................... 12

Budget by program............................................................................................ 13

FTE by program................................................................................................

15 Budget by object class........................................................................................16 Summary of key investments............................................................................ 17 Budget authority................................................................................................21 Civil Penalty Fund budget authority.................................................................22 Goal 1......................................................................................................................................23 Introduction...................................................................................................... 24 Outcome 1.1.......................................................................................................

26 Outcome 1.2.......................................................................................................33 Outcome 1.3.......................................................................................................33 Goal 2......................................................................................................................................46 Introduction.......................................................................................................47 Outcome 2.1.......................................................................................................49 Outcome 2.2.......................................................................................................56 2 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Goal 3......................................................................................................................................68 Introduction...................................................................................................... 69 Outcome 3.1.......................................................................................................70 Outcome 3.2.......................................................................................................73 Goal 4......................................................................................................................................78 Introduction.......................................................................................................79 Outcome 4.1...................................................................................................... 80 Outcome 4.2...................................................................................................... 86 Outcome 4.3......................................................................................................

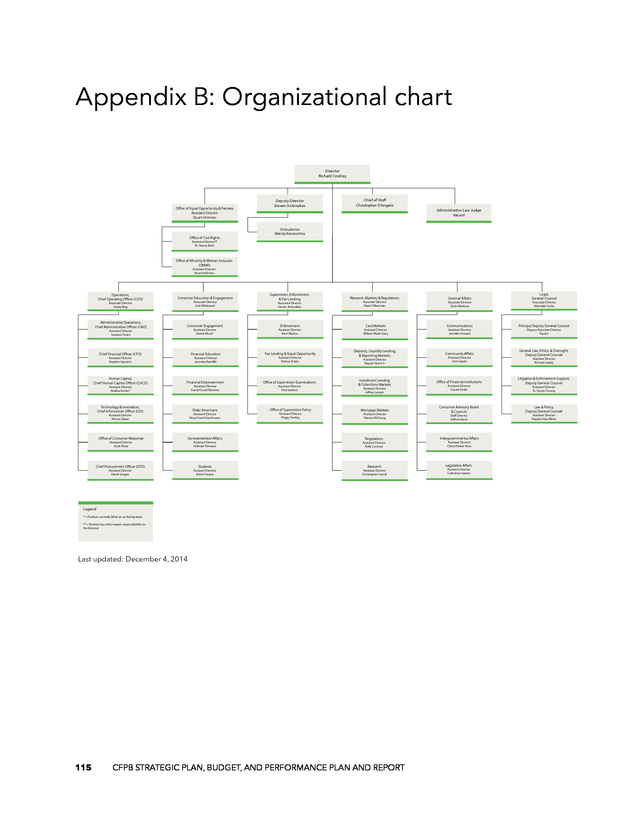

92 Outcome 4.4......................................................................................................97 Appendix A: Program evaluation, data validation, and management challenges........................................................................................... 100 Appendix B: Organizational chart....................................................................................115 3 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Message from Richard Cordray Director of the CFPB Continuing the Consumer Financial Protection Bureau’s (CFPB’s or Bureau’s) established practice, I am pleased to share an integrated view of planning and performance updates that address requirements set forth in the Government Performance and Results Act (GPRA) of 1993, as amended in the GPRA Modernization Act (GPRAMA) of 2010. This document presents the CFPB’s goals, investment choices, and accomplishments holistically. Presenting the Bureau’s long-term focus areas, resource allocations, and progress achieved to date in a unified document aims to provide a balanced and transparent status update on the CFPB’s work to American consumers, Congress, and other key stakeholders. I am proud to share the CFPB’s Strategic Plan for fiscal years 2013-2017, which guides our longrange work, as well as a comprehensive review of progress that the CFPB achieved in fiscal year (FY) 2014 across its four Strategic Goals. In addition, this document contains the Bureau’s most current view of budget projections for FY 2015-2016, and corresponding measures across its performance goals. The CFPB continues to strengthen its performance planning and reporting capabilities. This year’s report reflects the Bureau’s continued emphasis on balanced performance planning, accurate data for measuring performance, and evaluating programs with a view toward increasing effectiveness. To share a few highlights, in FY 2014, the CFPB: §§ Provided digital content, materials, and decision tools to over 5.6 million consumers – nearly triple the number of consumers reached in the previous year; §§ Handled over 240,000 consumer complaints across a broad range of financial products and issue types; 4 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . §§ Shared investigative information with more than 50 different government agencies in 280 matters; §§ Published 9 notable reports about specific consumer financial products, markets, or regulations, including the CARD Act Report, a report on Arbitration Study Preliminary Results, and others; and §§ Hosted 13 public events on key issues affecting consumer financial markets such as credit cards, mortgages, auto finance, and payday lending. Results achieved in the course of fiscal year 2014 suggest that the Bureau continues to mature across its areas of focus in supervision, enforcement, research, and outreach to American consumers. While the CFPB’s resource base is not expected to experience substantial increases in FY2015-16, the Bureau’s work to date indicates that consumers of financial services face challenges across product areas, highlighting the need for the Bureau to maintain a sharp focus on leveraging available resources carefully. The CFPB will ensure effectiveness of its actions based on careful planning, data-driven choices, deployment of innovative operational and technological solutions, and engaging of its mission-focused workforce across the nation. Congress created the CFPB as an independent Bureau within the Federal Reserve System as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, in direct response to a severe financial crisis. While the immediate effects of the turmoil have receded over the last several years, structural issues that the CFPB has identified through its work clearly signal that the Bureau’s mission of protecting American consumers remains as critical as ever.

The Bureau will continue to work closely with Congress, businesses, consumer advocates, and Federal, state, and local partners to increase continuously its effectiveness and the robustness of its consumer protection efforts. Sincerely, Richard Cordray, Director February 2015 5 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Overview of the CFPB The Bureau of Consumer Financial Protection, known as the Consumer Financial Protection Bureau (CFPB), was established on July 21, 2010 under Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act Public Law No. 111-203 (Dodd-Frank Act). The CFPB was established as an independent bureau within the Federal Reserve System. The Bureau is an Executive agency as defined in Section 105 of Title 5, United States Code. The Dodd-Frank Act authorizes the CFPB to exercise its authorities to ensure that, with respect to consumer financial products and services: 1. Consumers are provided with timely and understandable information to make responsible decisions about financial transactions; 2. Consumers are protected from unfair, deceptive, or abusive acts and practices and from discrimination; 3. Outdated, unnecessary, or unduly burdensome regulations are regularly identified and addressed in order to reduce unwarranted regulatory burdens; 4. Federal consumer financial law is enforced consistently in order to promote fair competition; and 5. Markets for consumer financial products and services operate transparently and efficiently to facilitate access and innovation. Under the Dodd-Frank Act, on the designated transfer date, July 21, 2011, certain authorities and functions of several agencies relating to Federal consumer financial law transferred to the CFPB in order to accomplish the above objectives.

These authorities were transferred from the Board of Governors of the Federal Reserve System (Board of Governors), Office of the Comptroller of the Currency (OCC), Office of Thrift Supervision (OTS), Federal Deposit Insurance Corporation (FDIC), National Credit Union Administration (NCUA), and the Department of Housing and Urban Development (HUD). In addition, Congress vested the Bureau with authority to enforce in certain circumstances the Federal Trade Commission’s (FTC) Telemarketing Sales Rule and its rules under the FTC Act, although the FTC retains full authority over these rules. The Dodd-Frank Act also provided the CFPB with certain other Federal consumer financial regulatory authorities. 6 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT .

Our organization Under the Dodd-Frank Act, the Secretary of the Treasury was responsible for establishing the CFPB and performing certain functions of the Bureau until a Director of the CFPB was in place. The Bureau’s day-to-day operations were managed by the Special Advisor to the Secretary of the Treasury for the Consumer Financial Protection Bureau until January 4, 2012, when President Obama recess appointed Richard Cordray as the first Director of the CFPB. Subsequently, the U.S. Senate confirmed the appointment of Richard Cordray on July 16, 2013, and Director Cordray was sworn in as the first Senate confirmed Director of the CFPB on July 17, 2013. To accomplish its mission, the CFPB is organized into six primary divisions: 1. Consumer Education and Engagement: works to empower consumers with the knowledge, tools, and capabilities they need in order to make better-informed financial decisions by engaging them in the right moments of their financial lives, while addressing the unique financial challenges faced by four specific populations. 2. Supervision, Enforcement and Fair Lending: ensures compliance with Federal consumer financial laws by supervising market participants and bringing enforcement actions when appropriate. 3. Research, Markets and Regulations: conducts research to understand consumer financial markets and consumer behavior, evaluates whether there is a need for regulation, and determines the costs and benefits of potential or existing regulations. 4. Legal Division: ensures the Bureau’s compliance with all applicable laws and provides advice to the Director and the Bureau’s divisions. 5. External Affairs: manages the Bureau’s relationships with external stakeholders and ensures that the Bureau maintains robust dialogue with interested stakeholders to promote understanding, transparency, and accountability. 6. Operations: builds and sustains the CFPB’s operational infrastructure to support the entire organization and hears directly from consumers about challenges they face in the marketplaces through their complaints, questions, and feedback. 7 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Our mission The CFPB is a 21st century agency that helps consumer finance markets work by making rules more effective, by consistently and fairly enforcing those rules, and by empowering consumers to take more control over their economic lives. Our vision If we achieve our mission, then we will have encouraged the development of a consumer finance marketplace §§ where customers can see prices and risks up front and where they can easily make product comparisons; §§ in which no one can build a business model around unfair, deceptive, or abusive practices; §§ that works for American consumers, responsible providers, and the economy as a whole. We will achieve our mission and vision through: Data-driven analysis The CFPB is a data-driven agency. We take in data, manage it, store it, share it appropriately, and protect it from unauthorized access. Our aim is to use data purposefully, to analyze and distill data to enable informed decision-making in all internal and external functions. Innovative use of technology Technology is core to the CFPB accomplishing its mission. This means developing and leveraging technology to enhance the CFPB’s reach, impact, and effectiveness.

We strive to be recognized as an innovative, 21st century agency whose approach to technology serves as a model within government. Valuing the best people and great teamwork At the CFPB, we believe our people are our greatest asset. Therefore, we invest in world-class training and support in order to create a diverse and inclusive environment that encourages employees at all levels to tackle complex challenges. We also believe effective teamwork extends outside the walls of the CFPB.

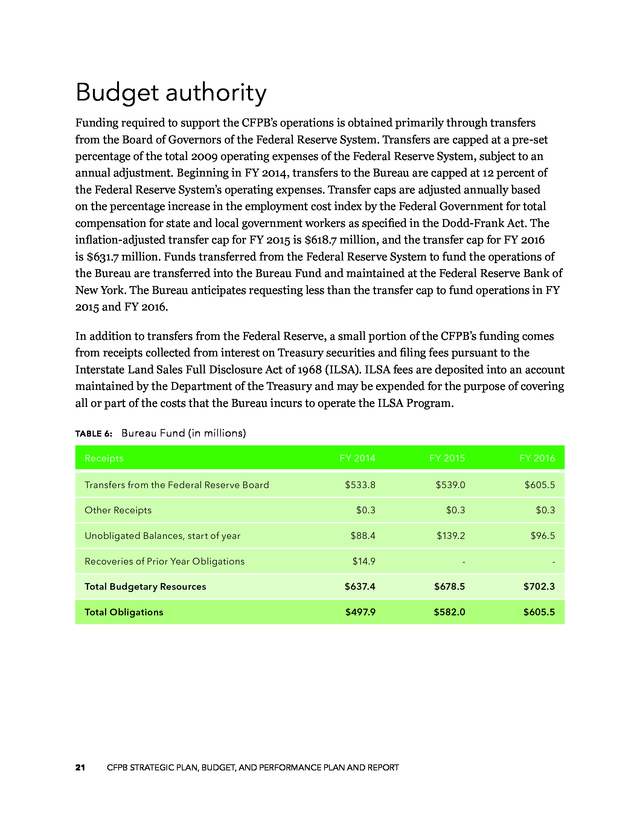

We seek input from and collaborate with consumers, industry, government entities, and other external stakeholders. 8 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . We aim to embody the following values in everything we do: Service Our mission begins with service to the consumer and our country. We serve our colleagues by listening to one another and by sharing our collective knowledge and experience. Leadership Fostering leadership and collaboration at all levels is at the core of our success. We believe in investing in the growth of our colleagues and in creating an organization that is accountable to the American people. Innovation Our organization embraces new ideas and technology. We are focused on continuously improving, learning, and pushing ourselves to be great. 9 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Plan overview Our strategic plan articulates four goals Goal 1 Prevent financial harm to consumers while promoting good practices that benefit them. Goal 2 Empower consumers to live better financial lives. Goal 3 Inform the public, policy makers, and the CFPB’s own policy-making with data-driven analysis of consumer finance markets and consumer behavior. Goal 4 Advance the CFPB’s performance by maximizing resource productivity and enhancing impact. In support of each goal we outline Budget Outcomes Desired outcomes that further define the focus of our work. Strategies & investments Strategies and investments that lay out the actions we will take to accomplish our outcomes. Performance goals 10 Resource allocations we will make in order to achieve our goals. Specific, measurable goals we will use to assess our progress along with associated measures and indicators. CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Budget overview The CFPB’s operations are funded principally by transfers made by the Board of Governors of the Federal Reserve System from the combined earnings of the Federal Reserve System, up to the limits set forth in the Dodd-Frank Act. The Director of the CFPB requests transfers from the Federal Reserve System in amounts that he has determined are reasonably necessary to carry out the Bureau’s mission without exceeding the limits in the Dodd-Frank Act. Transfers through FY 2013 were capped at pre-set percentages of the total 2009 operating expenses of the Federal Reserve System. In fiscal years 2014, 2015, and beyond, the cap is adjusted annually based on the percentage increase in the employment cost index published by the Federal Government for the total compensation for State and local government workers.

Transfers from the Federal Reserve System are capped at $618.7 million for FY 2015. For FY 2016, the transfer cap is estimated to be $631.7 million. Funds transferred from the Federal Reserve System are transferred into the Bureau of Consumer Financial Protection Fund (Bureau Fund), which is maintained at the Federal Reserve Bank of New York. Pursuant to the Dodd-Frank Act, the CFPB is also authorized to collect and retain for specified purposes civil penalties obtained from any person for violations of Federal consumer financial laws.

The CFPB is authorized to use these funds for payments to the victims of activities for which civil penalties have been imposed, and may also use the funds for consumer education and financial literacy programs under certain circumstances. Funds collected by the CFPB under this authority are deposited into the Consumer Financial Civil Penalty Fund (Civil Penalty Fund) maintained at the Federal Reserve Bank of New York. Bureau Fund The CFPB FY 2015 and FY 2016 budget estimates included in this Report will support the operations of the Bureau and its continued growth and maturity as a Federal agency. These resources will enable the Bureau to continue to fulfill its statutory obligations, and its mission to make rules more effective, by consistently and fairly enforcing those rules, and by empowering consumers to take more control over their financial lives. 11 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT .

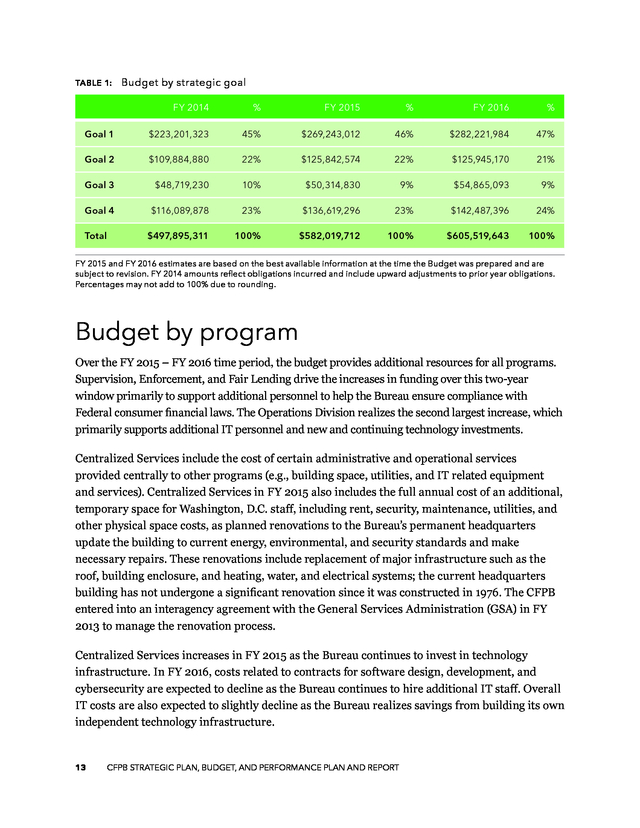

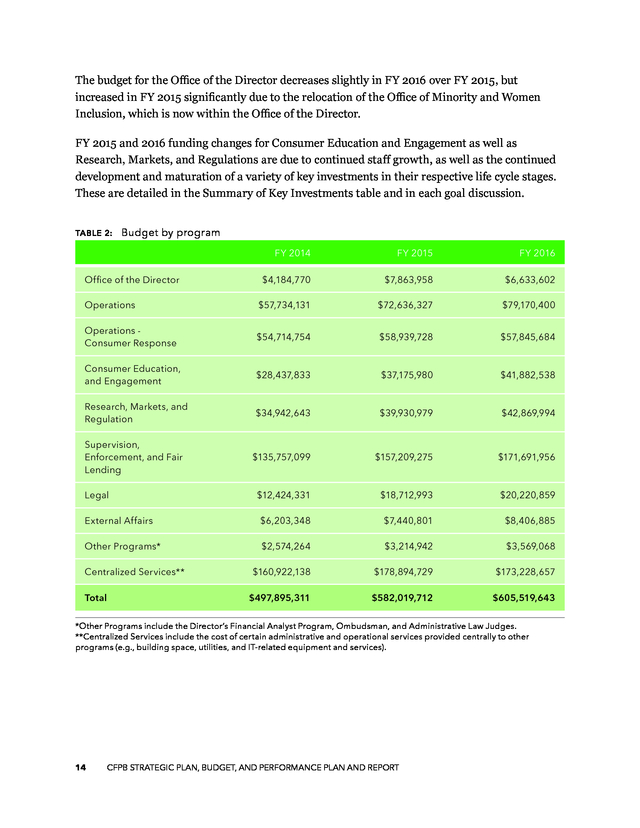

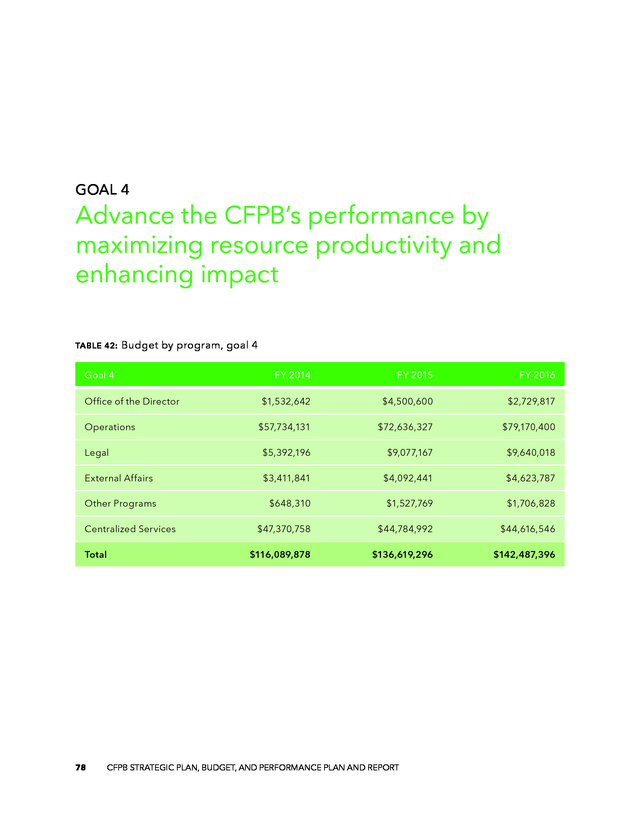

The FY 2016 budget estimate of $605.5 million is 4.0% percent above the FY 2015 budget estimate of $582.0 million. The FY 2015 budget estimate is 16.9% higher than total FY 2014 actuals. To achieve the four strategic goals outlined in this plan, the FY 2015 and 2016 budget estimates support additional staff, especially for supervision and examination activities, ongoing operations, and key investments, with a focus on developing IT infrastructure, cybersecurity, and data management projects. Budget by strategic goal Goal 1 Prevent financial harm to consumers while promoting good practices that benefit them. Goal 2 Empower consumers to live better financial lives. Goal 3 Inform the public, policy makers, and the CFPB’s own policy-making with data-driven analysis of consumer finance markets and consumer behavior. Goal 4 Advance the CFPB’s performance by maximizing resource productivity and enhancing impact. The data below provide a view of our budgetary resources by strategic goal. As shown below, the proportion of funding across all goals is expected to remain relatively constant through FY 2016. Activities related to regulation, supervision, and enforcement activities -- which are included in Goal 1 -- represent the largest portion of the FY 2016 budget at 47% and primarily support the continued growth of the regional supervision and examination workforce as the CFPB moves towards steady-state operation.

Other key investments in FY 2015 and FY 2016 are devoted to activities under Goal 2, which include expanding capacity and systems to improve the handling, processing, and analysis of consumer complaints as well as helping consumers understand the costs, risks, and tradeoffs of financial decisions through financial education outreach. The proportion of funding for Goal 3 and 4 remains stable in FY 2015 and FY 2016, as the Bureau approaches steady state in its research and market monitoring functions and develops an independent in-house technology infrastructure. 12 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . TABLE 1: Budget by strategic goal FY 2014 % FY 2015 % FY 2016 % Goal 1 $223,201,323 45% $269,243,012 46% $282,221,984 47% Goal 2 $109,884,880 22% $125,842,574 22% $125,945,170 21% Goal 3 $48,719,230 10% $50,314,830 9% $54,865,093 9% Goal 4 $116,089,878 23% $136,619,296 23% $142,487,396 24% $497,895,311 100% $582,019,712 100% $605,519,643 100% Total FY 2015 and FY 2016 estimates are based on the best available information at the time the Budget was prepared and are subject to revision. FY 2014 amounts reflect obligations incurred and include upward adjustments to prior year obligations. Percentages may not add to 100% due to rounding. Budget by program Over the FY 2015 – FY 2016 time period, the budget provides additional resources for all programs. Supervision, Enforcement, and Fair Lending drive the increases in funding over this two-year window primarily to support additional personnel to help the Bureau ensure compliance with Federal consumer financial laws. The Operations Division realizes the second largest increase, which primarily supports additional IT personnel and new and continuing technology investments. Centralized Services include the cost of certain administrative and operational services provided centrally to other programs (e.g., building space, utilities, and IT related equipment and services). Centralized Services in FY 2015 also includes the full annual cost of an additional, temporary space for Washington, D.C.

staff, including rent, security, maintenance, utilities, and other physical space costs, as planned renovations to the Bureau’s permanent headquarters update the building to current energy, environmental, and security standards and make necessary repairs. These renovations include replacement of major infrastructure such as the roof, building enclosure, and heating, water, and electrical systems; the current headquarters building has not undergone a significant renovation since it was constructed in 1976. The CFPB entered into an interagency agreement with the General Services Administration (GSA) in FY 2013 to manage the renovation process. Centralized Services increases in FY 2015 as the Bureau continues to invest in technology infrastructure.

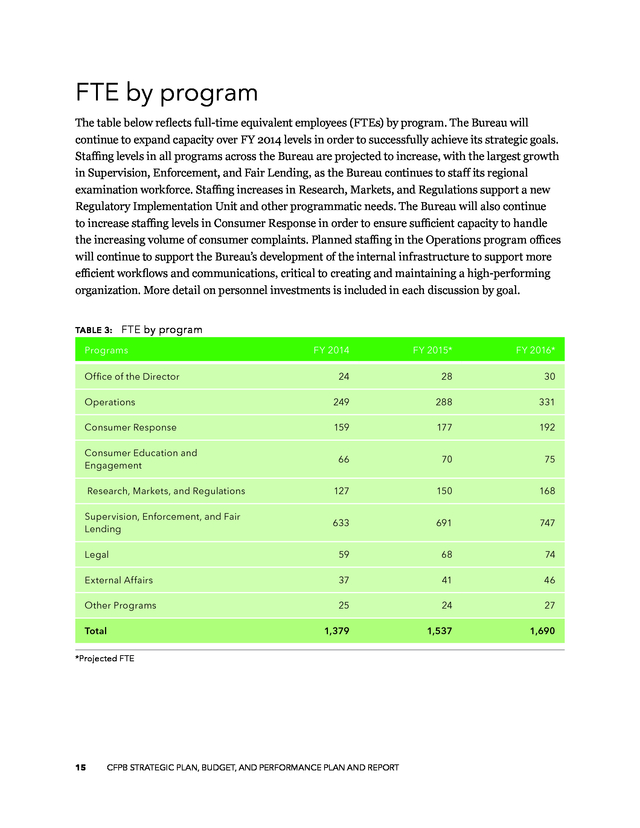

In FY 2016, costs related to contracts for software design, development, and cybersecurity are expected to decline as the Bureau continues to hire additional IT staff. Overall IT costs are also expected to slightly decline as the Bureau realizes savings from building its own independent technology infrastructure. 13 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . The budget for the Office of the Director decreases slightly in FY 2016 over FY 2015, but increased in FY 2015 significantly due to the relocation of the Office of Minority and Women Inclusion, which is now within the Office of the Director. FY 2015 and 2016 funding changes for Consumer Education and Engagement as well as Research, Markets, and Regulations are due to continued staff growth, as well as the continued development and maturation of a variety of key investments in their respective life cycle stages. These are detailed in the Summary of Key Investments table and in each goal discussion. TABLE 2: Budget by program FY 2014 FY 2015 FY 2016 $4,184,770 $7,863,958 $6,633,602 Operations $57,734,131 $72,636,327 $79,170,400 Operations Consumer Response $54,714,754 $58,939,728 $57,845,684 Consumer Education, and Engagement $28,437,833 $37,175,980 $41,882,538 Research, Markets, and Regulation $34,942,643 $39,930,979 $42,869,994 Supervision, Enforcement, and Fair Lending $135,757,099 $157,209,275 $171,691,956 $12,424,331 $18,712,993 $20,220,859 External Affairs $6,203,348 $7,440,801 $8,406,885 Other Programs* $2,574,264 $3,214,942 $3,569,068 $160,922,138 $178,894,729 $173,228,657 $497,895,311 $582,019,712 $605,519,643 Office of the Director Legal Centralized Services** Total *Other Programs include the Director’s Financial Analyst Program, Ombudsman, and Administrative Law Judges. **Centralized Services include the cost of certain administrative and operational services provided centrally to other programs (e.g., building space, utilities, and IT-related equipment and services). 14 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . FTE by program The table below reflects full-time equivalent employees (FTEs) by program. The Bureau will continue to expand capacity over FY 2014 levels in order to successfully achieve its strategic goals. Staffing levels in all programs across the Bureau are projected to increase, with the largest growth in Supervision, Enforcement, and Fair Lending, as the Bureau continues to staff its regional examination workforce. Staffing increases in Research, Markets, and Regulations support a new Regulatory Implementation Unit and other programmatic needs. The Bureau will also continue to increase staffing levels in Consumer Response in order to ensure sufficient capacity to handle the increasing volume of consumer complaints.

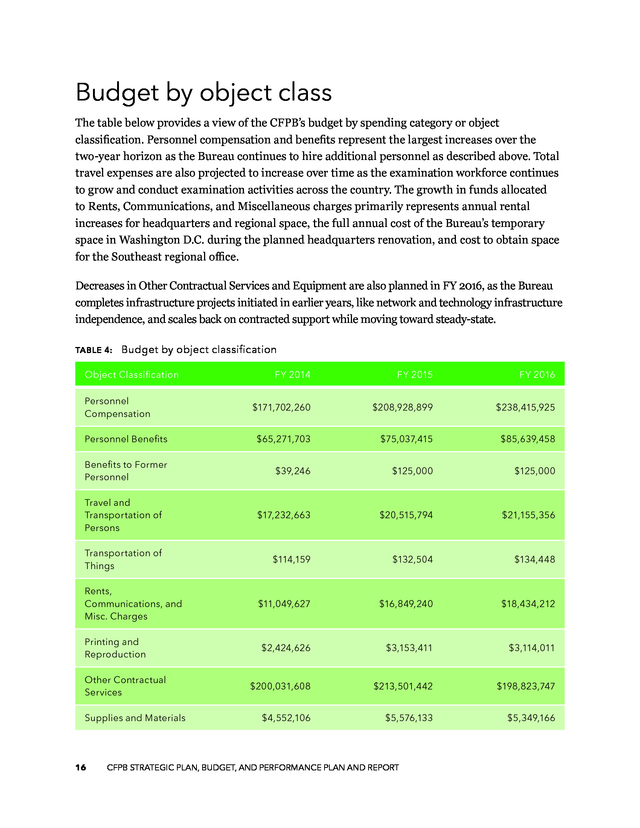

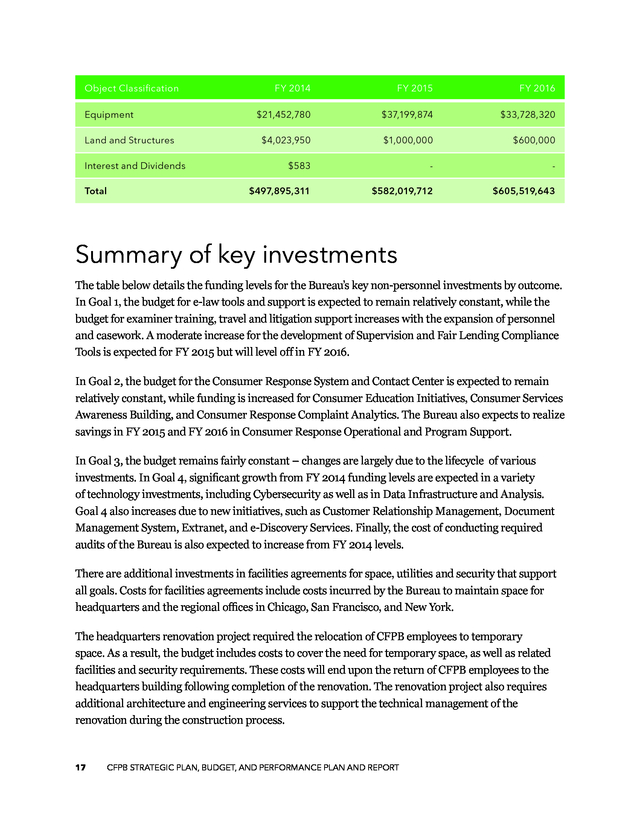

Planned staffing in the Operations program offices will continue to support the Bureau’s development of the internal infrastructure to support more efficient workflows and communications, critical to creating and maintaining a high-performing organization. More detail on personnel investments is included in each discussion by goal. TABLE 3: FTE by program Programs FY 2014 FY 2015* FY 2016* 24 28 30 Operations 249 288 331 Consumer Response 159 177 192 66 70 75 Research, Markets, and Regulations 127 150 168 Supervision, Enforcement, and Fair Lending 633 691 747 Legal 59 68 74 External Affairs 37 41 46 Other Programs 25 24 27 1,379 1,537 1,690 Office of the Director Consumer Education and Engagement Total *Projected FTE 15 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Budget by object class The table below provides a view of the CFPB’s budget by spending category or object classification. Personnel compensation and benefits represent the largest increases over the two-year horizon as the Bureau continues to hire additional personnel as described above. Total travel expenses are also projected to increase over time as the examination workforce continues to grow and conduct examination activities across the country. The growth in funds allocated to Rents, Communications, and Miscellaneous charges primarily represents annual rental increases for headquarters and regional space, the full annual cost of the Bureau’s temporary space in Washington D.C.

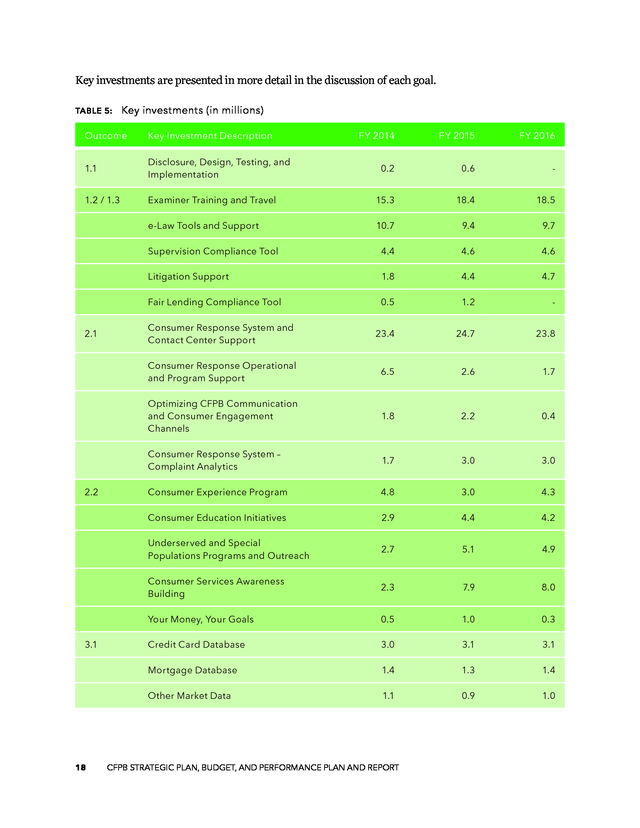

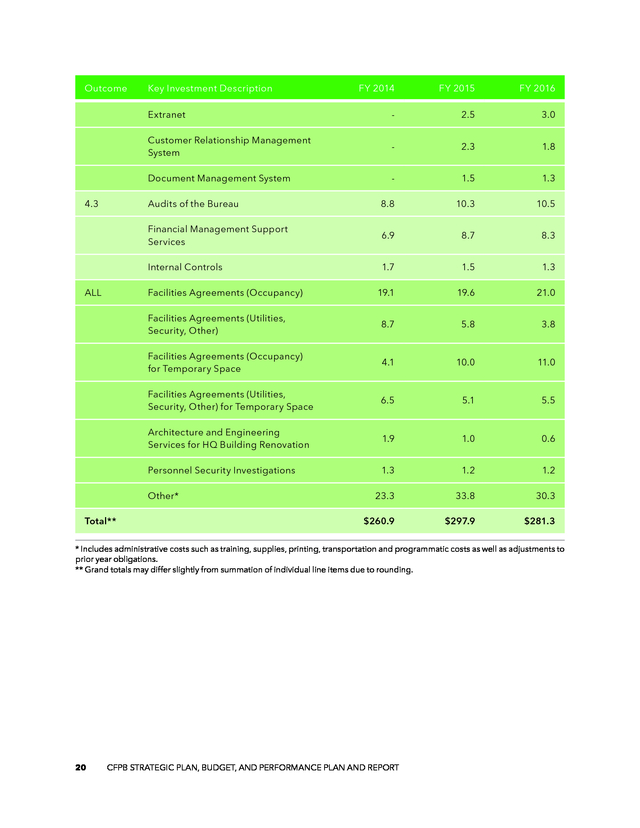

during the planned headquarters renovation, and cost to obtain space for the Southeast regional office. Decreases in Other Contractual Services and Equipment are also planned in FY 2016, as the Bureau completes infrastructure projects initiated in earlier years, like network and technology infrastructure independence, and scales back on contracted support while moving toward steady-state. TABLE 4: Budget by object classification Object Classification FY 2014 FY 2015 FY 2016 $171,702,260 $208,928,899 $238,415,925 Personnel Benefits $65,271,703 $75,037,415 $85,639,458 Benefits to Former Personnel $39,246 $125,000 $125,000 Travel and Transportation of Persons $17,232,663 $20,515,794 $21,155,356 Transportation of Things $114,159 $132,504 $134,448 $11,049,627 $16,849,240 $18,434,212 $2,424,626 $3,153,411 $3,114,011 $200,031,608 $213,501,442 $198,823,747 $4,552,106 $5,576,133 $5,349,166 Personnel Compensation Rents, Communications, and Misc. Charges Printing and Reproduction Other Contractual Services Supplies and Materials 16 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Object Classification Equipment Land and Structures Interest and Dividends Total FY 2014 FY 2015 FY 2016 $21,452,780 $37,199,874 $33,728,320 $4,023,950 $1,000,000 $600,000 $583 - - $497,895,311 $582,019,712 $605,519,643 Summary of key investments The table below details the funding levels for the Bureau’s key non-personnel investments by outcome. In Goal 1, the budget for e-law tools and support is expected to remain relatively constant, while the budget for examiner training, travel and litigation support increases with the expansion of personnel and casework. A moderate increase for the development of Supervision and Fair Lending Compliance Tools is expected for FY 2015 but will level off in FY 2016. In Goal 2, the budget for the Consumer Response System and Contact Center is expected to remain relatively constant, while funding is increased for Consumer Education Initiatives, Consumer Services Awareness Building, and Consumer Response Complaint Analytics. The Bureau also expects to realize savings in FY 2015 and FY 2016 in Consumer Response Operational and Program Support. In Goal 3, the budget remains fairly constant – changes are largely due to the lifecycle of various investments. In Goal 4, significant growth from FY 2014 funding levels are expected in a variety of technology investments, including Cybersecurity as well as in Data Infrastructure and Analysis. Goal 4 also increases due to new initiatives, such as Customer Relationship Management, Document Management System, Extranet, and e-Discovery Services.

Finally, the cost of conducting required audits of the Bureau is also expected to increase from FY 2014 levels. There are additional investments in facilities agreements for space, utilities and security that support all goals. Costs for facilities agreements include costs incurred by the Bureau to maintain space for headquarters and the regional offices in Chicago, San Francisco, and New York. The headquarters renovation project required the relocation of CFPB employees to temporary space. As a result, the budget includes costs to cover the need for temporary space, as well as related facilities and security requirements.

These costs will end upon the return of CFPB employees to the headquarters building following completion of the renovation. The renovation project also requires additional architecture and engineering services to support the technical management of the renovation during the construction process. 17 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Key investments are presented in more detail in the discussion of each goal. TABLE 5: Key investments (in millions) Outcome Key Investment Description 1.1 Disclosure, Design, Testing, and Implementation 1.2 / 1.3 0.6 - Examiner Training and Travel 15.3 18.4 18.5 10.7 9.4 9.7 4.4 4.6 4.6 1.8 4.4 4.7 Fair Lending Compliance Tool 0.5 1.2 - Consumer Response System and Contact Center Support 23.4 24.7 23.8 Consumer Response Operational and Program Support 6.5 2.6 1.7 Optimizing CFPB Communication and Consumer Engagement Channels 1.8 2.2 0.4 Consumer Response System – Complaint Analytics 1.7 3.0 3.0 Consumer Experience Program 4.8 3.0 4.3 Consumer Education Initiatives 2.9 4.4 4.2 Underserved and Special Populations Programs and Outreach 2.7 5.1 4.9 Consumer Services Awareness Building 2.3 7.9 8.0 Your Money, Your Goals 0.5 1.0 0.3 Credit Card Database 3.0 3.1 3.1 Mortgage Database 1.4 1.3 1.4 Other Market Data 18 0.2 Litigation Support 3.1 FY 2016 Supervision Compliance Tool 2.2 FY 2015 e-Law Tools and Support 2.1 FY 2014 1.1 0.9 1.0 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Outcome 1.3 1.3 0.7 0.6 0.6 0.6 Know Before You Owe: Mortgage e-Closing 2.2 - - 2.1 0.7 - Underserved and Special Populations Research 1.7 0.6 1.4 Primary Data Collection 1.2 2.3 2.0 Financial Education Research 1.1 0.4 1.2 Financial Education Metrics 0.8 0.1 1.4 Financial Education Innovations 0.4 0.5 0.5 Human Capital Shared Services, Infrastructure, and Operations 8.3 9.6 10.0 Outreach, Candidate Recruiting, and Candidate Selection Support 2.8 2.7 2.5 Learning, Leadership, and Organization Development Facilitation and Design 2.3 3.7 3.8 Diversity and Inclusion Initiatives 0.5 1.7 - Technology Infrastructure 33.1 22.9 22.6 Technology Infrastructure - Shared Services 12.4 11.2 3.4 IT Portfolio Management 10.9 13.2 12.2 Design and Software Development Support 6.3 6.4 4.8 Cybersecurity 3.4 7.1 6.9 Data Infrastructure and Analysis 2.0 6.6 8.5 e-Discovery Services Implementation 19 FY 2016 Evidence-Based Consumer Research 4.2 FY 2015 HMDA Data Processing 4.1 FY 2014 HMDA Development and Implementation 3.2 Key Investment Description 0.3 5.4 5.8 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Outcome FY 2015 FY 2016 - 2.5 3.0 Customer Relationship Management System - 2.3 1.8 Document Management System - 1.5 1.3 Audits of the Bureau 8.8 10.3 10.5 Financial Management Support Services 6.9 8.7 8.3 Internal Controls 1.7 1.5 1.3 19.1 19.6 21.0 Facilities Agreements (Utilities, Security, Other) 8.7 5.8 3.8 Facilities Agreements (Occupancy) for Temporary Space 4.1 10.0 11.0 Facilities Agreements (Utilities, Security, Other) for Temporary Space 6.5 5.1 5.5 Architecture and Engineering Services for HQ Building Renovation 1.9 1.0 0.6 Personnel Security Investigations ALL FY 2014 Extranet 4.3 Key Investment Description 1.3 1.2 1.2 23.3 33.8 30.3 $260.9 $297.9 $281.3 Facilities Agreements (Occupancy) Other* Total** * Includes administrative costs such as training, supplies, printing, transportation and programmatic costs as well as adjustments to prior year obligations. ** Grand totals may differ slightly from summation of individual line items due to rounding. 20 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Budget authority Funding required to support the CFPB’s operations is obtained primarily through transfers from the Board of Governors of the Federal Reserve System. Transfers are capped at a pre-set percentage of the total 2009 operating expenses of the Federal Reserve System, subject to an annual adjustment. Beginning in FY 2014, transfers to the Bureau are capped at 12 percent of the Federal Reserve System’s operating expenses. Transfer caps are adjusted annually based on the percentage increase in the employment cost index by the Federal Government for total compensation for state and local government workers as specified in the Dodd-Frank Act.

The inflation-adjusted transfer cap for FY 2015 is $618.7 million, and the transfer cap for FY 2016 is $631.7 million. Funds transferred from the Federal Reserve System to fund the operations of the Bureau are transferred into the Bureau Fund and maintained at the Federal Reserve Bank of New York. The Bureau anticipates requesting less than the transfer cap to fund operations in FY 2015 and FY 2016. In addition to transfers from the Federal Reserve, a small portion of the CFPB’s funding comes from receipts collected from interest on Treasury securities and filing fees pursuant to the Interstate Land Sales Full Disclosure Act of 1968 (ILSA).

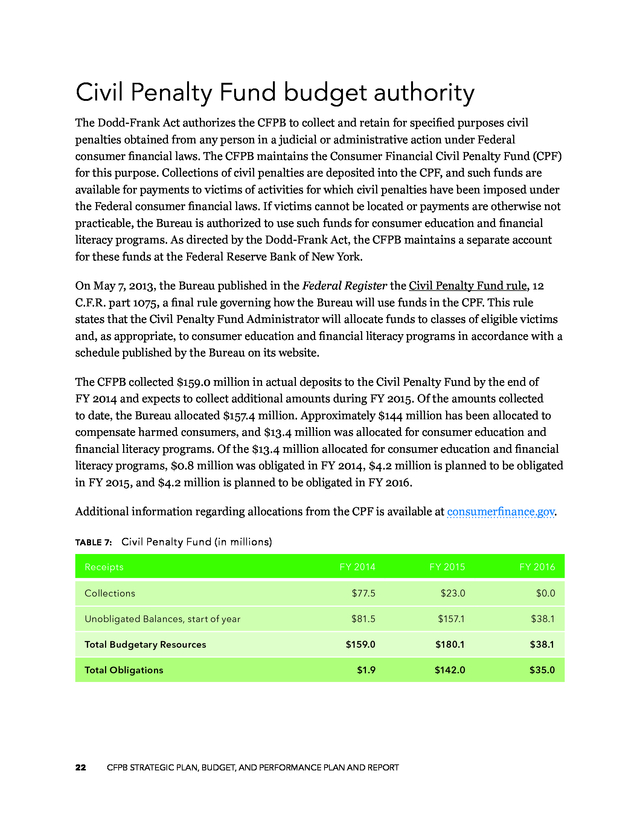

ILSA fees are deposited into an account maintained by the Department of the Treasury and may be expended for the purpose of covering all or part of the costs that the Bureau incurs to operate the ILSA Program. TABLE 6: Bureau Fund (in millions) Receipts FY 2014 FY 2015 FY 2016 $533.8 $539.0 $605.5 $0.3 $0.3 $0.3 Unobligated Balances, start of year $88.4 $139.2 $96.5 Recoveries of Prior Year Obligations $14.9 - - Total Budgetary Resources $637.4 $678.5 $702.3 Total Obligations $497.9 $582.0 $605.5 Transfers from the Federal Reserve Board Other Receipts 21 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Civil Penalty Fund budget authority The Dodd-Frank Act authorizes the CFPB to collect and retain for specified purposes civil penalties obtained from any person in a judicial or administrative action under Federal consumer financial laws. The CFPB maintains the Consumer Financial Civil Penalty Fund (CPF) for this purpose. Collections of civil penalties are deposited into the CPF, and such funds are available for payments to victims of activities for which civil penalties have been imposed under the Federal consumer financial laws. If victims cannot be located or payments are otherwise not practicable, the Bureau is authorized to use such funds for consumer education and financial literacy programs.

As directed by the Dodd-Frank Act, the CFPB maintains a separate account for these funds at the Federal Reserve Bank of New York. On May 7, 2013, the Bureau published in the Federal Register the Civil Penalty Fund rule, 12 C.F.R. part 1075, a final rule governing how the Bureau will use funds in the CPF. This rule states that the Civil Penalty Fund Administrator will allocate funds to classes of eligible victims and, as appropriate, to consumer education and financial literacy programs in accordance with a schedule published by the Bureau on its website. The CFPB collected $159.0 million in actual deposits to the Civil Penalty Fund by the end of FY 2014 and expects to collect additional amounts during FY 2015.

Of the amounts collected to date, the Bureau allocated $157.4 million. Approximately $144 million has been allocated to compensate harmed consumers, and $13.4 million was allocated for consumer education and financial literacy programs. Of the $13.4 million allocated for consumer education and financial literacy programs, $0.8 million was obligated in FY 2014, $4.2 million is planned to be obligated in FY 2015, and $4.2 million is planned to be obligated in FY 2016. Additional information regarding allocations from the CPF is available at consumerfinance.gov. TABLE 7: Civil Penalty Fund (in millions) Receipts FY 2014 FY 2015 FY 2016 Collections $77.5 $23.0 $0.0 Unobligated Balances, start of year $81.5 $157.1 $38.1 $159.0 $180.1 $38.1 $1.9 $142.0 $35.0 Total Budgetary Resources Total Obligations 22 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT .

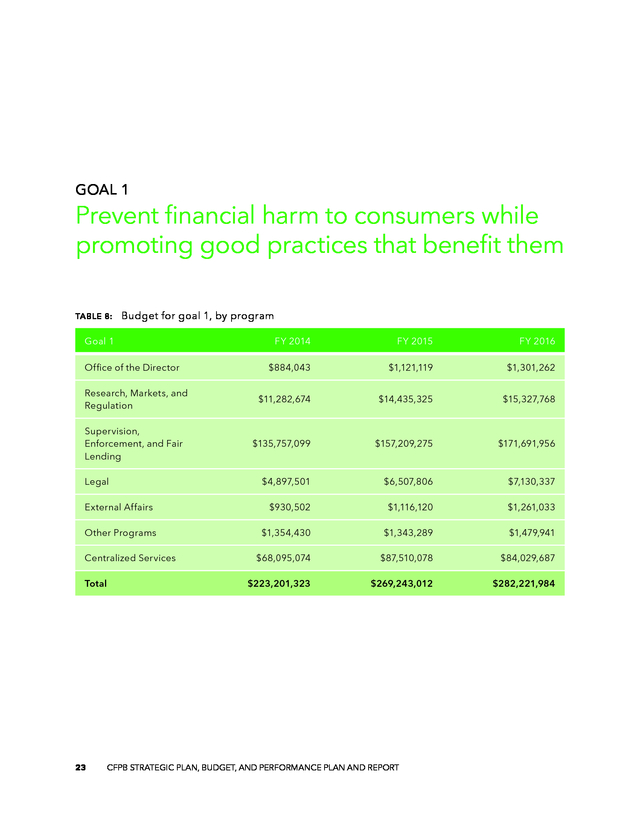

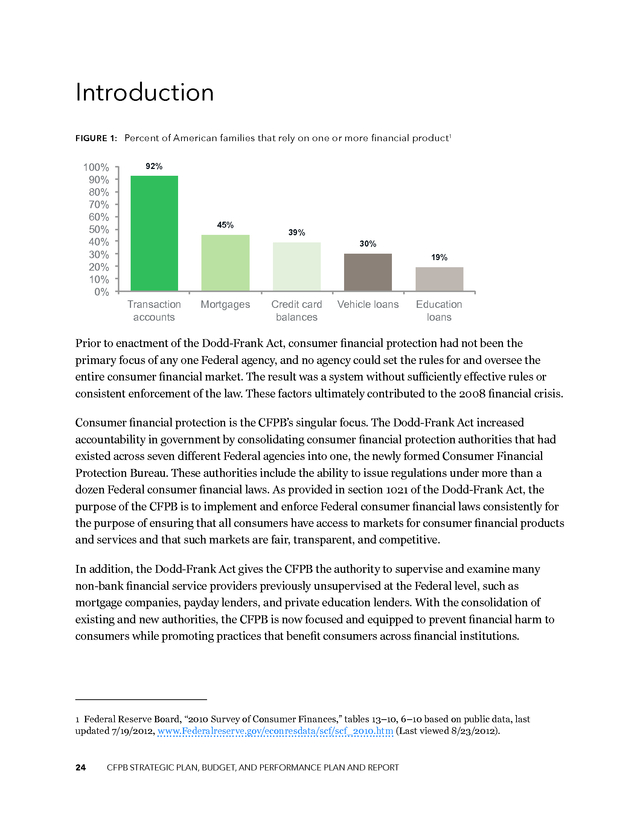

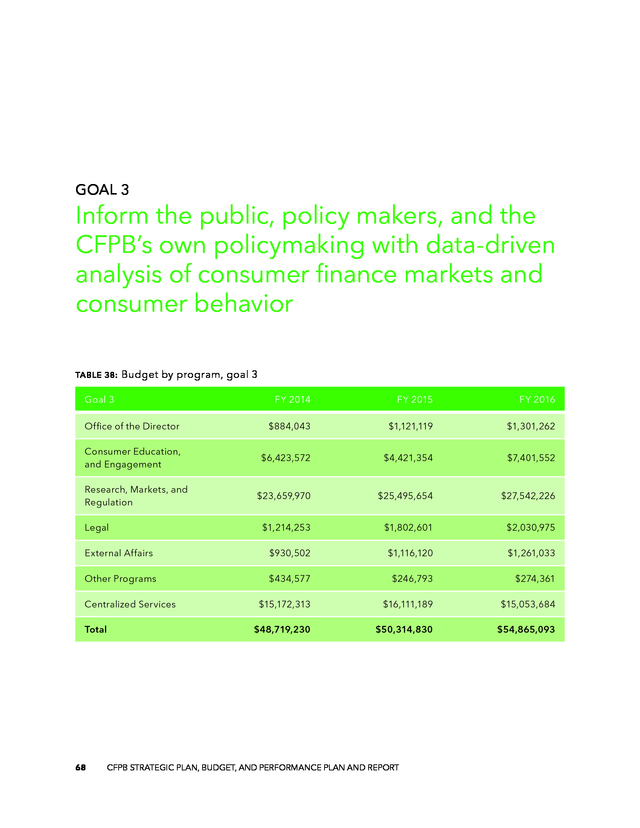

GOAL 1 Prevent financial harm to consumers while promoting good practices that benefit them TABLE 8: Budget for goal 1, by program Goal 1 Office of the Director Research, Markets, and Regulation Supervision, Enforcement, and Fair Lending Legal External Affairs Other Programs Centralized Services Total 23 FY 2014 FY 2015 FY 2016 $884,043 $1,121,119 $1,301,262 $11,282,674 $14,435,325 $15,327,768 $135,757,099 $157,209,275 $171,691,956 $4,897,501 $6,507,806 $7,130,337 $930,502 $1,116,120 $1,261,033 $1,354,430 $1,343,289 $1,479,941 $68,095,074 $87,510,078 $84,029,687 $223,201,323 $269,243,012 $282,221,984 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Introduction FIGURE 1: Percent of American families that rely on one or more financial product1 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% 92% 45% 39% 30% 19% Transaction accounts Mortgages Credit card balances Vehicle loans Education loans Prior to enactment of the Dodd-Frank Act, consumer financial protection had not been the primary focus of any one Federal agency, and no agency could set the rules for and oversee the entire consumer financial market. The result was a system without sufficiently effective rules or consistent enforcement of the law. These factors ultimately contributed to the 2008 financial crisis. Consumer financial protection is the CFPB’s singular focus. The Dodd-Frank Act increased accountability in government by consolidating consumer financial protection authorities that had existed across seven different Federal agencies into one, the newly formed Consumer Financial Protection Bureau.

These authorities include the ability to issue regulations under more than a dozen Federal consumer financial laws. As provided in section 1021 of the Dodd-Frank Act, the purpose of the CFPB is to implement and enforce Federal consumer financial laws consistently for the purpose of ensuring that all consumers have access to markets for consumer financial products and services and that such markets are fair, transparent, and competitive. In addition, the Dodd-Frank Act gives the CFPB the authority to supervise and examine many non-bank financial service providers previously unsupervised at the Federal level, such as mortgage companies, payday lenders, and private education lenders. With the consolidation of existing and new authorities, the CFPB is now focused and equipped to prevent financial harm to consumers while promoting practices that benefit consumers across financial institutions. 1 Federal Reserve Board, “2010 Survey of Consumer Finances,” tables 13–10, 6–10 based on public data, last updated 7/19/2012, www.Federalreserve.gov/econresdata/scf/scf_2010.htm (Last viewed 8/23/2012). 24 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT .

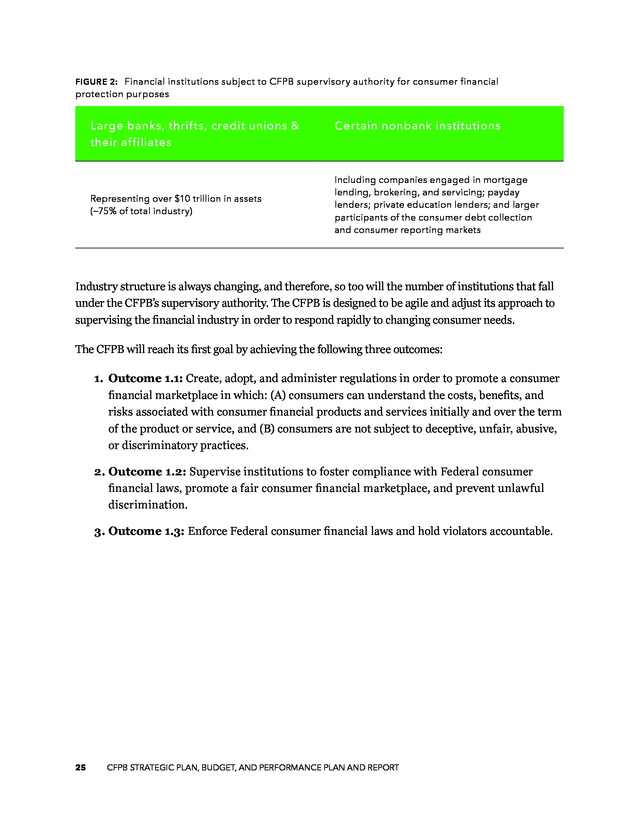

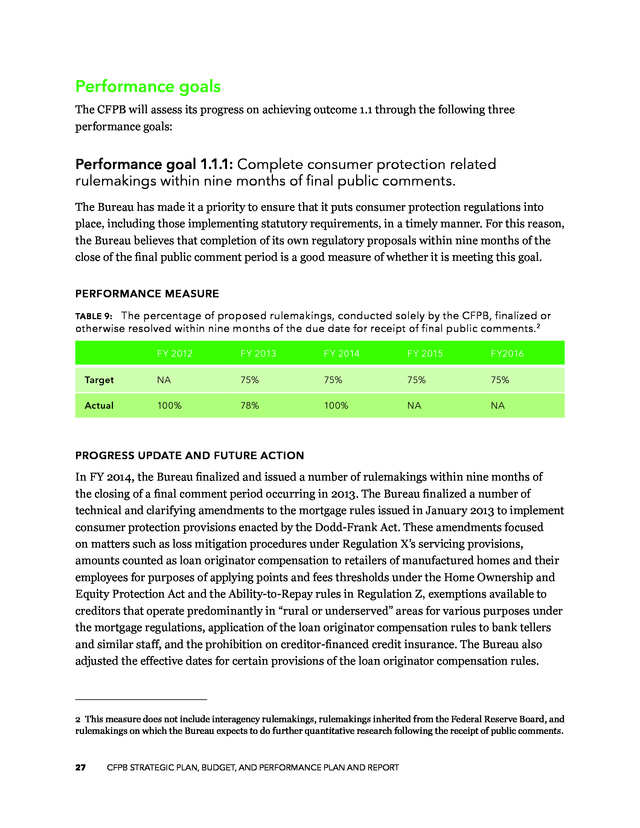

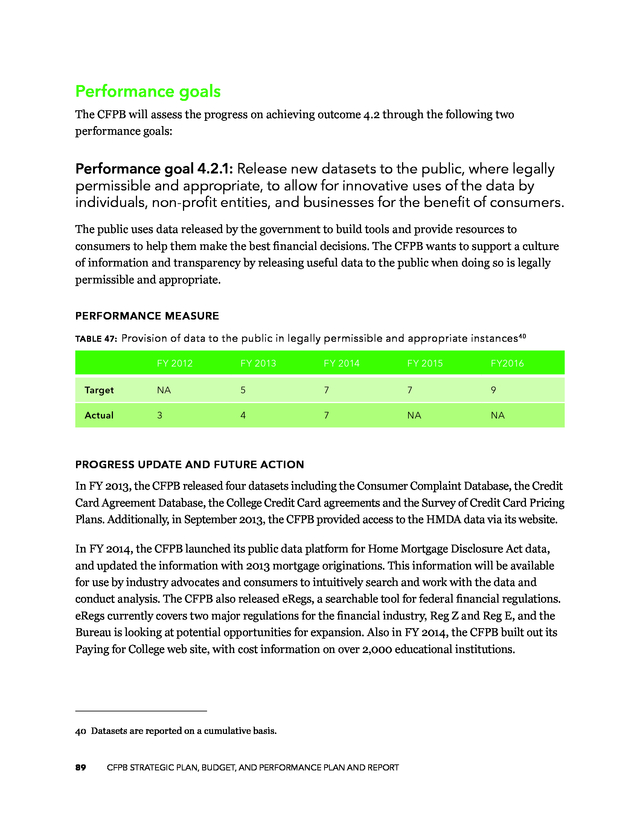

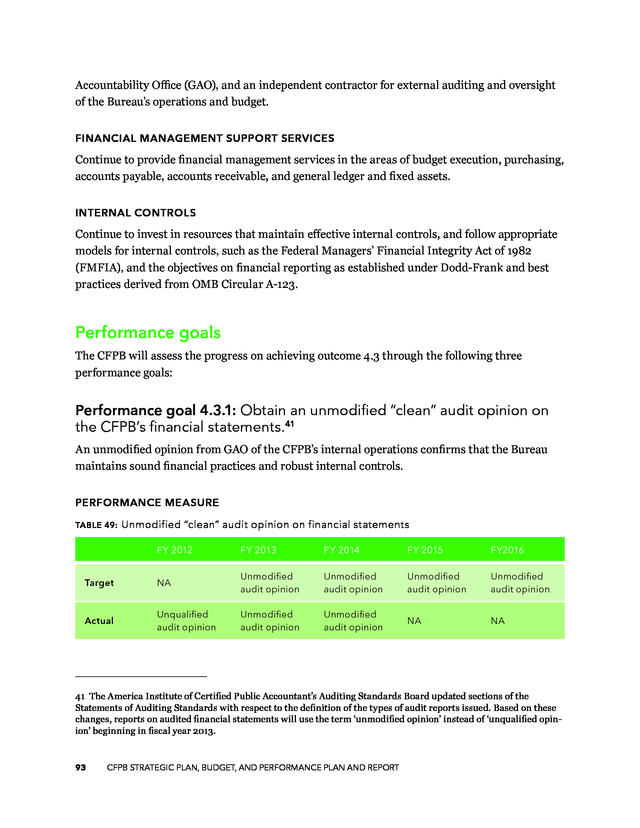

FIGURE 2: Financial institutions subject to CFPB supervisory authority for consumer financial protection purposes Large banks, thrifts, credit unions & their affiliates Representing over $10 trillion in assets (~75% of total industry) Certain nonbank institutions Including companies engaged in mortgage lending, brokering, and servicing; payday lenders; private education lenders; and larger participants of the consumer debt collection and consumer reporting markets Industry structure is always changing, and therefore, so too will the number of institutions that fall under the CFPB’s supervisory authority. The CFPB is designed to be agile and adjust its approach to supervising the financial industry in order to respond rapidly to changing consumer needs. The CFPB will reach its first goal by achieving the following three outcomes: 1. Outcome 1.1: Create, adopt, and administer regulations in order to promote a consumer financial marketplace in which: (A) consumers can understand the costs, benefits, and risks associated with consumer financial products and services initially and over the term of the product or service, and (B) consumers are not subject to deceptive, unfair, abusive, or discriminatory practices. 2. Outcome 1.2: Supervise institutions to foster compliance with Federal consumer financial laws, promote a fair consumer financial marketplace, and prevent unlawful discrimination. 3. Outcome 1.3: Enforce Federal consumer financial laws and hold violators accountable. 25 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Outcome 1.1 Create, adopt, and administer regulations in order to promote a consumer financial marketplace in which: (A) consumers can understand the costs, benefits, and risks associated with consumer financial products and services initially and over the term of the product or service, and (B) consumers are not subject to deceptive, unfair, abusive, or discriminatory practices. Outcome leader: Associate Director of Research, Markets, and Regulations Strategies and investments The following strategies and investments have been put in place to help the CFPB achieve outcome 1.1. Strategies §§ Develop and maintain an efficient fact-based approach to developing, evaluating, revising, and finalizing regulations. §§ Develop a rule-writing team with highly advanced skills in relevant and specialized legal, business, and economic areas. §§ Work with consumers and industry stakeholders on developing regulations to implement existing Federal consumer financial laws effectively. §§ Leverage technology to continuously improve the efficiency and effectiveness of the Federal rulemaking processes and procedures. Investments PERSONNEL Continue to expand capacity to conduct rulemaking activities, provide interpretive guidance, develop small business compliance guides and provide other implementation support, and evaluate benefits and costs of potential rules. DISCLOSURE DESIGN, TESTING, AND IMPLEMENTATION Continue to conduct and gain expertise in disclosure design and disclosure usability testing. Qualitative research, such as one-on-one interviews, enables the Bureau to put forward proposed forms which consumers are more likely to be able to navigate and comprehend. These investments also contribute to evidence-based market research. 26 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Performance goals The CFPB will assess its progress on achieving outcome 1.1 through the following three performance goals: Performance goal 1.1.1: Complete consumer protection related rulemakings within nine months of final public comments. The Bureau has made it a priority to ensure that it puts consumer protection regulations into place, including those implementing statutory requirements, in a timely manner. For this reason, the Bureau believes that completion of its own regulatory proposals within nine months of the close of the final public comment period is a good measure of whether it is meeting this goal. PERFORMANCE MEASURE The percentage of proposed rulemakings, conducted solely by the CFPB, finalized or otherwise resolved within nine months of the due date for receipt of final public comments. 2 TABLE 9: FY 2012 FY 2013 FY 2014 FY 2015 FY2016 Target NA 75% 75% 75% 75% Actual 100% 78% 100% NA NA PROGRESS UPDATE AND FUTURE ACTION In FY 2014, the Bureau finalized and issued a number of rulemakings within nine months of the closing of a final comment period occurring in 2013. The Bureau finalized a number of technical and clarifying amendments to the mortgage rules issued in January 2013 to implement consumer protection provisions enacted by the Dodd-Frank Act.

These amendments focused on matters such as loss mitigation procedures under Regulation X’s servicing provisions, amounts counted as loan originator compensation to retailers of manufactured homes and their employees for purposes of applying points and fees thresholds under the Home Ownership and Equity Protection Act and the Ability-to-Repay rules in Regulation Z, exemptions available to creditors that operate predominantly in “rural or underserved” areas for various purposes under the mortgage regulations, application of the loan originator compensation rules to bank tellers and similar staff, and the prohibition on creditor-financed credit insurance. The Bureau also adjusted the effective dates for certain provisions of the loan originator compensation rules. 2 This measure does not include interagency rulemakings, rulemakings inherited from the Federal Reserve Board, and rulemakings on which the Bureau expects to do further quantitative research following the receipt of public comments. 27 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . In October 2013, the Bureau made additional updates to its title XIV mortgage origination and servicing rules issued in January 2013. Among other things, these rules required that consumers receive counseling before obtaining high-cost mortgages and that servicers provide periodic account statements and rate adjustment notices to mortgage borrowers, and engage in early intervention for delinquent borrowers. Regarding servicing, on October 13, 2013, the Bureau issued an interim final rule suspending periodic statements and certain loss mitigation notices for consumers in bankruptcy, so the Bureau could consider how its servicing rules interact with other laws which may prohibit contacts with consumers such as the Bankruptcy Code and the Fair Debt Collections Practices Act. Based on the comments and further analysis, the Bureau issued a proposal to provide clearer guidance to servicers for consumers in bankruptcy in November 2014.

Also in October 2013, the Bureau clarified the specific disclosures that must be provided before counseling for high-cost mortgages can occur. In November, 2013, the Bureau issued a final rule under Sections 1098 and 1100A of the DoddFrank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) along with forms that combined certain disclosures that consumers receive in connection with applying for and closing on a mortgage loan under the Truth in Lending Act (Regulation Z) and the Real Estate Settlement Procedures Act (Regulation X). The final rule was issued a little over a year after the initial proposal, during which time the Bureau put several prototype forms through rigorous qualitative and quantitative consumer testing to ensure that the disclosures would inform consumers about the costs, benefits and risks of loan offers. The Bureau also periodically sought input from the general public between testing rounds, posting the prototype forms on its “Know Before you Owe” webpage—that webpage received over 150,000 visits and generated over 27,000 public comments.

The Bureau considered these comments, as well as 2,800 letters submitted in response to the rules proposed to implement the forms. The Bureau’s final rule issued in November 2013 established new disclosure requirements and forms in Regulation Z for most closed-end consumer credit transactions secured by real property. Also in November 2013, the Bureau issued a final interpretive rule3 describing data instructions for lenders to use in complying with the requirement under the High-Cost Mortgage and Homeownership Counseling Amendments to the Truth in Lending Act (Regulation Z) and Homeownership Counseling Amendments to the Real Estate Settlement Procedures Act (RESPA Homeownership Counseling Amendments). These rules require creditors to provide applicants with a list of homeownership counselors using data made available by the Bureau or Department of Housing and Urban Development (HUD). 3 The Bureau issued this rule without first issuing a proposal, because it provides technical instructions for which notice and comment is not required under the Administrative Procedures Act. 28 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT .

In 2013, the Bureau amended its 2012 final rule governing remittances under the Electronic Fund Transfer Act (EFTA). The 2012 final rule provided new protections for consumers transferring money to other consumers or businesses abroad, including disclosures, and error resolution and cancellation rights. In late 2012 the Bureau proposed to amend and clarify the rules and to extend the compliance deadline, with comments on both due on January 15 and 30th, 2013. The Bureau finalized both proposals on May 22, 2013.

This final rule made optional the disclosure of foreign taxes and certain foreign fees and adjusted providers’ liability in certain circumstances where a consumer made a mistake. Following on the May 2013 final rule, the Bureau made additional clarifying amendments and a technical correction to the remittances rule on August 14, 2013. The remittance transfer rule, including all of the 2013 amendments, took effect on October 28, 2013. During FY 2014, the Bureau also issued proposed and final rules modifying earlier mortgage ability-to-repay and mortgage servicing rules it had issued in 2013.

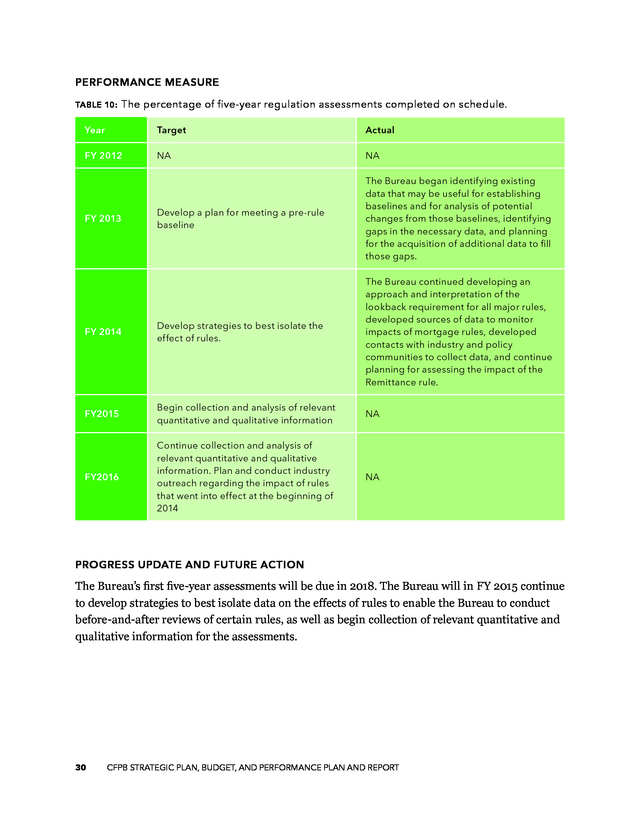

These rules provide mortgage lenders with an ability to cure mortgages that exceed the points and fees cap for “qualified mortgages.” They also clarify how the mortgage and servicing rules apply to certain nonprofits who lend primarily to low- and moderate-income consumers. In addition, the Bureau issued proposed and final rules simplifying existing rules governing annual privacy notices under the Gramm-Leach-Bilely Act. Finally, the Bureau proposed and finalized narrow changes to the rules for its TILA-RESPA combined forms to ensure that consumers who lock interest rates after application receive timely disclosures and to clarify disclosure requirements for construction loans. Performance goal 1.1.2: Complete all five-year regulation assessments on schedule. Section 1022(d) of the Dodd-Frank Act requires the CFPB to assess each significant rule the Bureau adopts under Federal consumer financial law and publish a report of the assessment within five years of the effective date of such rule.

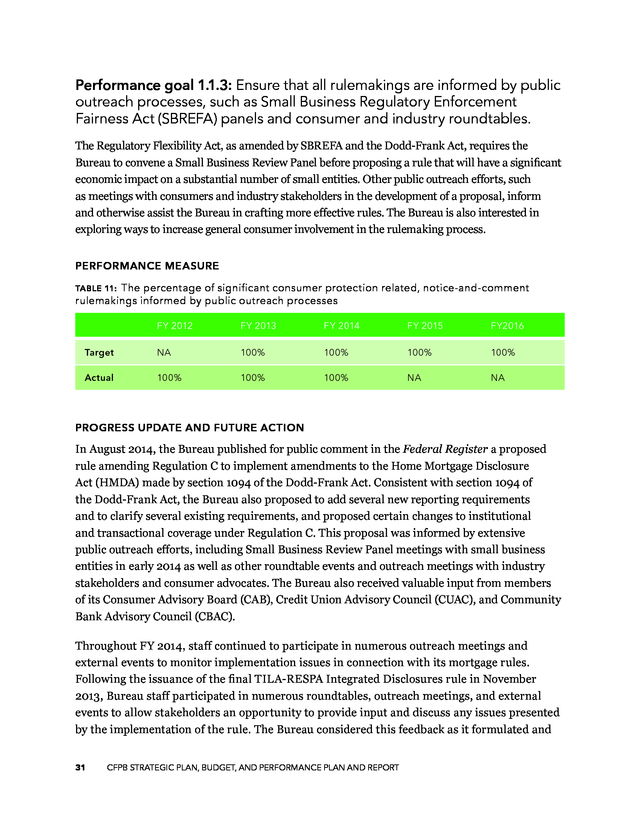

The assessment addresses, among other factors, the rule’s effectiveness in meeting the purposes and objectives of Title X of the DoddFrank Act, and the specific goals the Bureau states for the rule. 29 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . PERFORMANCE MEASURE TABLE 10: The percentage of five-year regulation assessments completed on schedule. Year Target Actual FY 2012 NA NA Develop a plan for meeting a pre-rule baseline The Bureau began identifying existing data that may be useful for establishing baselines and for analysis of potential changes from those baselines, identifying gaps in the necessary data, and planning for the acquisition of additional data to fill those gaps. FY 2014 Develop strategies to best isolate the effect of rules. The Bureau continued developing an approach and interpretation of the lookback requirement for all major rules, developed sources of data to monitor impacts of mortgage rules, developed contacts with industry and policy communities to collect data, and continue planning for assessing the impact of the Remittance rule. FY2015 Begin collection and analysis of relevant quantitative and qualitative information NA FY2016 Continue collection and analysis of relevant quantitative and qualitative information. Plan and conduct industry outreach regarding the impact of rules that went into effect at the beginning of 2014 NA FY 2013 PROGRESS UPDATE AND FUTURE ACTION The Bureau’s first five-year assessments will be due in 2018. The Bureau will in FY 2015 continue to develop strategies to best isolate data on the effects of rules to enable the Bureau to conduct before-and-after reviews of certain rules, as well as begin collection of relevant quantitative and qualitative information for the assessments. 30 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Performance goal 1.1.3: Ensure that all rulemakings are informed by public outreach processes, such as Small Business Regulatory Enforcement Fairness Act (SBREFA) panels and consumer and industry roundtables. The Regulatory Flexibility Act, as amended by SBREFA and the Dodd-Frank Act, requires the Bureau to convene a Small Business Review Panel before proposing a rule that will have a significant economic impact on a substantial number of small entities. Other public outreach efforts, such as meetings with consumers and industry stakeholders in the development of a proposal, inform and otherwise assist the Bureau in crafting more effective rules. The Bureau is also interested in exploring ways to increase general consumer involvement in the rulemaking process. PERFORMANCE MEASURE The percentage of significant consumer protection related, notice-and-comment rulemakings informed by public outreach processes TABLE 11: FY 2012 FY 2013 FY 2014 FY 2015 FY2016 Target NA 100% 100% 100% 100% Actual 100% 100% 100% NA NA PROGRESS UPDATE AND FUTURE ACTION In August 2014, the Bureau published for public comment in the Federal Register a proposed rule amending Regulation C to implement amendments to the Home Mortgage Disclosure Act (HMDA) made by section 1094 of the Dodd-Frank Act. Consistent with section 1094 of the Dodd-Frank Act, the Bureau also proposed to add several new reporting requirements and to clarify several existing requirements, and proposed certain changes to institutional and transactional coverage under Regulation C.

This proposal was informed by extensive public outreach efforts, including Small Business Review Panel meetings with small business entities in early 2014 as well as other roundtable events and outreach meetings with industry stakeholders and consumer advocates. The Bureau also received valuable input from members of its Consumer Advisory Board (CAB), Credit Union Advisory Council (CUAC), and Community Bank Advisory Council (CBAC). Throughout FY 2014, staff continued to participate in numerous outreach meetings and external events to monitor implementation issues in connection with its mortgage rules. Following the issuance of the final TILA-RESPA Integrated Disclosures rule in November 2013, Bureau staff participated in numerous roundtables, outreach meetings, and external events to allow stakeholders an opportunity to provide input and discuss any issues presented by the implementation of the rule. The Bureau considered this feedback as it formulated and 31 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT .

issued additional proposals to clarify or address some of the matters and issues raised in connection with these rules. The CFPB also encouraged all stakeholders to submit formal written comments on these proposals. The Bureau also conducted numerous other public outreach efforts in FY 2014 to inform and assist the Bureau in developing non-mortgage rules. For example, following the Bureau’s release of an advance notice of proposed rulemaking (ANPR) related to debt collection practices in November 2013, Bureau staff continued to participate in outreach events and meetings that included both consumers and industry participants to obtain information and feedback on communications issues, data integrity and information flows, and other topics listed in the ANPR. Furthermore, the Bureau in FY 2014 continued to conduct outreach in connection with its remittances rule, including conducting interviews with regulated entities, which informed revisions to its regulations implementing provisions of the Dodd-Frank Act that established a new system of federal protections for remittance transfers sent by consumers in the United States to individuals and businesses in foreign countries.

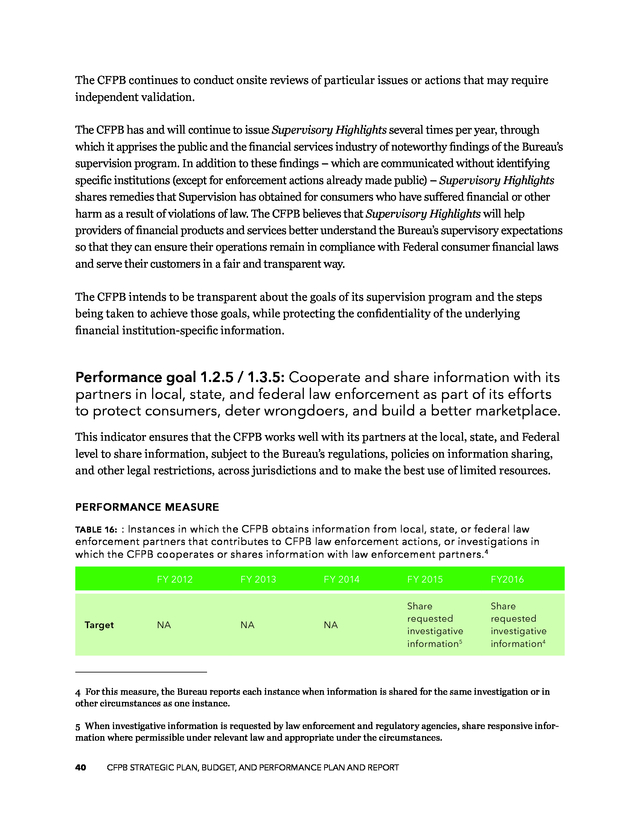

Finally, in connection with prepaid cards, the Bureau conducted outreach as well as interview testing with consumers around the country to help the Bureau develop and design a model disclosure, and posted the model disclosures on its website for public consideration and feedback. In FY 2015, the CFPB intends to continue to undertake its public outreach efforts to consumers and industry stakeholders as it considers topics for other possible future consumer protection related rules. 32 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Outcome 1.2 Supervise institutions to foster compliance with Federal consumer financial laws, promote a fair consumer financial marketplace, and prevent unlawful discrimination. Outcome 1.3 Enforce Federal consumer financial laws and hold violators accountable. Outcome leader: Associate Director of Supervision, Enforcement, and Fair Lending Background The Bureau’s Division of Supervision, Enforcement, and Fair Lending is responsible for supervising for compliance with and enforcing consumer financial protection law, including fair lending laws. The Division closely coordinates its use of both the supervision and enforcement tools, which work in tandem toward the common goal of preventing financial harm to consumers while promoting good practices that benefit them. For example, information received through enforcement may inform supervision priorities; a particular matter may arise through supervision and ultimately be resolved through enforcement; or compliance with enforcement actions may be monitored through supervision. The Associate Director for SEFL is accountable for both outcomes 1.2 and 1.3.

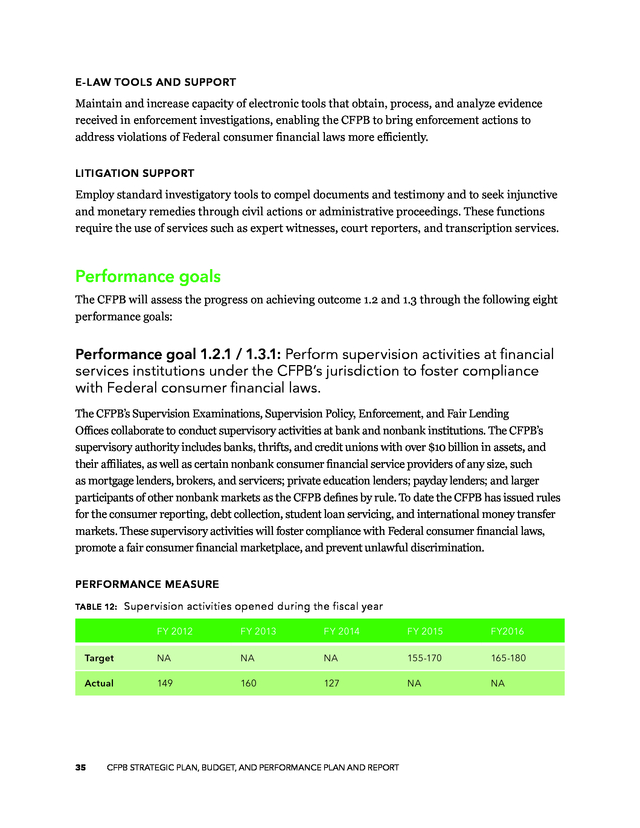

Thus, these outcomes are closely linked and for the purposes of performance reporting, are combined with respect to their constituent performance goals. Strategies and investments The following strategies and investments have been put in place to help the CFPB achieve outcome 1.2 and outcome 1.3. Strategies §§ Acquire and analyze qualitative and quantitative information and data pertaining to consumer financial product and service markets and companies. §§ Focus resources on institutions and their product lines that pose the greatest risk to consumers, based on their size, nature of the product, and field and market intelligence. 33 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . §§ Implement a framework for sharing information, coordinating activity, and promoting best practices with fellow financial institution supervisory and law enforcement agencies to ensure the most effective use of regulatory resources. §§ Implement internal policies that facilitate the integration of the CFPB’s supervision, enforcement, and fair lending functions. §§ Continue to develop a technology solution for coordinating supervisory information, capable of recording, storing, tracking, and reporting information on the CFPB’s supervisory process. §§ Continue implementing a tool capable of reviewing loan and deposit portfolios for compliance with Federal consumer financial laws. Investments PERSONNEL Hire additional staff to expand the CFPB’s capacity to focus on risks to consumers in the policies and practices of consumer financial providers; analyze available data on the activities of providers, on the markets in which they operate, and on the risks to consumers; implement and enforce Federal consumer financial laws consistently for both bank and nonbank consumer financial companies; and investigate and take actions to address potential violations of Federal consumer financial laws. EX AMINER TRAINING AND TRAVEL Continue supporting the development and delivery of training courses essential to examiner commissioning and to maintaining a highly effective workforce. Also support the travel requirements of the CFPB’s distributed workforce in order to effectively carry out its supervision program. SUPERVISION COMPLIANCE TOOL Automate data analysis in order to review loan files more thoroughly, use supervision resources more efficiently, and streamline the on-site portion of the exam. This tool will improve the CFPB’s ability to assess compliance with Federal consumer financial laws, and assess and detect risks to consumers. FAIR LENDING COMPLIANCE TOOL Modules for analysts and examiners to visualize public data sets to identify and investigate potential fair lending matters are being built to share research insights, utilize analytical resources more efficiently, and provide robust analysis on a wider range of examinations. Additional modules currently being developed will streamline examination processes and procedures, increasing process transparency and resource allocation. 34 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . E-L AW TOOLS AND SUPPORT Maintain and increase capacity of electronic tools that obtain, process, and analyze evidence received in enforcement investigations, enabling the CFPB to bring enforcement actions to address violations of Federal consumer financial laws more efficiently. LITIGATION SUPPORT Employ standard investigatory tools to compel documents and testimony and to seek injunctive and monetary remedies through civil actions or administrative proceedings. These functions require the use of services such as expert witnesses, court reporters, and transcription services. Performance goals The CFPB will assess the progress on achieving outcome 1.2 and 1.3 through the following eight performance goals: Performance goal 1.2.1 / 1.3.1: Perform supervision activities at financial services institutions under the CFPB’s jurisdiction to foster compliance with Federal consumer financial laws. The CFPB’s Supervision Examinations, Supervision Policy, Enforcement, and Fair Lending Offices collaborate to conduct supervisory activities at bank and nonbank institutions. The CFPB’s supervisory authority includes banks, thrifts, and credit unions with over $10 billion in assets, and their affiliates, as well as certain nonbank consumer financial service providers of any size, such as mortgage lenders, brokers, and servicers; private education lenders; payday lenders; and larger participants of other nonbank markets as the CFPB defines by rule. To date the CFPB has issued rules for the consumer reporting, debt collection, student loan servicing, and international money transfer markets.

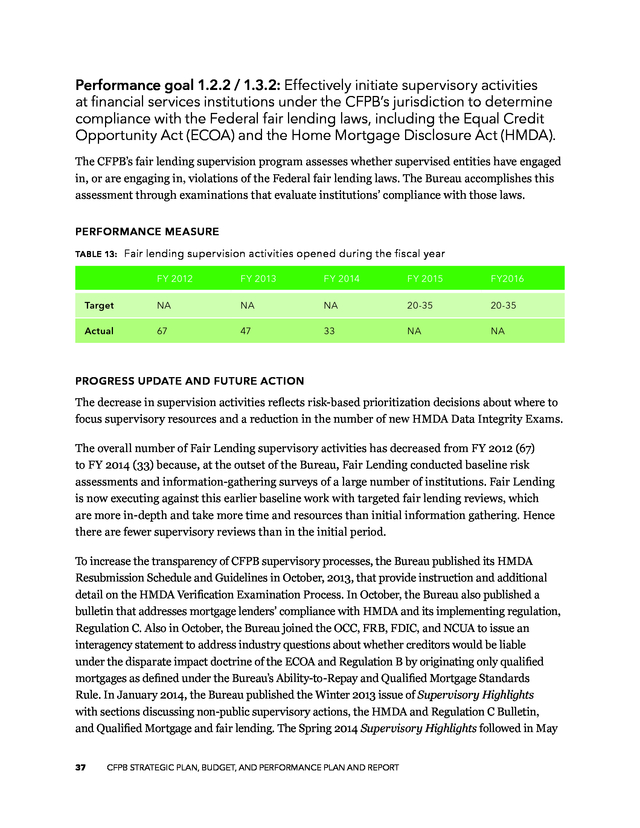

These supervisory activities will foster compliance with Federal consumer financial laws, promote a fair consumer financial marketplace, and prevent unlawful discrimination. PERFORMANCE MEASURE TABLE 12: Supervision activities opened during the fiscal year FY 2012 FY 2013 FY 2014 FY 2015 FY2016 Target NA NA NA 155-170 165-180 Actual 149 160 127 NA NA 35 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . PROGRESS UPDATE AND FUTURE ACTION In FY 2014, the CFPB continued to implement its supervision program, opening 127 supervisory activities at large banks and nonbank financial institutions. These activities included continuing existing supervision program product areas including mortgage origination, mortgage servicing, credit cards, deposits, student lending, short-term, small dollar loans, consumer reporting agencies and nonbank debt collectors. They also included the first ever review of nonbank student loan servicers. The CFPB expanded its Supervision and Examination Manual by adding or revising chapters on: §§ HMDA resubmission schedule and guidelines (October 2013) §§ Remittance transfer examination procedures (October 2013) §§ Updated Regulation E examination procedures, including remittance transfers (October 2013) §§ TILA procedures – Higher-Priced Mortgage Loan Appraisals, Loan Originator Compensation , Ability-to-Repay/Qualified Mortgages, High-Cost Mortgages, and Mortgage Servicing Requirements (November 2013) §§ RESPA procedures – home ownership and equity protection, mortgage servicing requirements (November 2013) §§ Education loan examination procedures (December 2013) §§ Mortgage Servicing examination procedures (January 2014) §§ Mortgage Origination examination procedures (January 2014) §§ Examination report and supervisory letter templates and cover letters (May 2014) The CFPB has also continued to coordinate with applicable Federal and state regulators on supervisory activities to minimize regulatory burden, leverage resources, and decrease the risk of conflicting supervisory directives. To facilitate this coordination, the Bureau has entered into memoranda of understanding with, among others, the Federal prudential regulators, the Federal Trade Commission, and over sixty state bank and nonbank supervisory agencies.

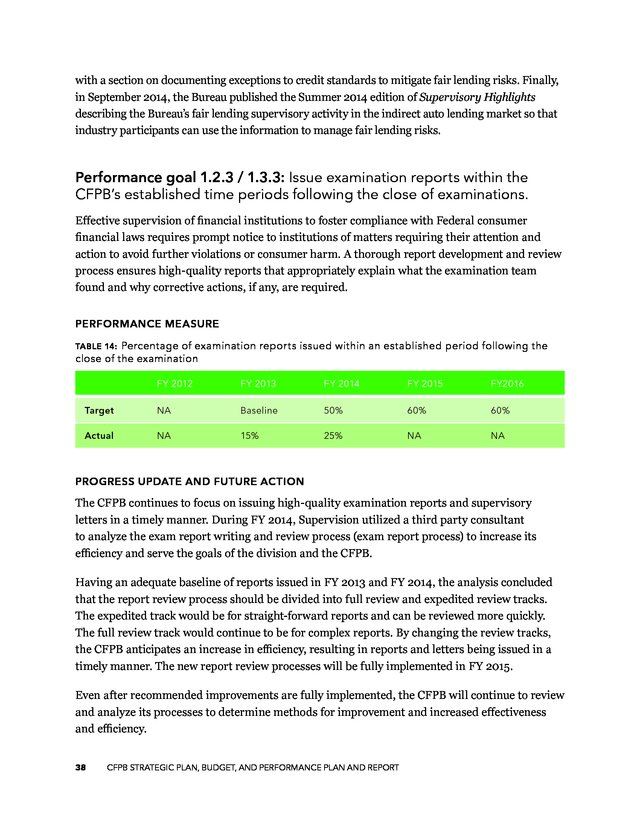

In addition, the CFPB has entered into a framework with state financial agencies that establishes a dynamic and flexible process for coordination on supervision and enforcement matters. The CFPB is also determining a development plan for a replacement system to the Supervision and Examination System, its system of record for supervision work. The Bureau continues to develop and implement a replacement system that will organize entities by institution product line, capture relationships between entities, schedule examinations, support supervisory workflows, and document the supervision process. 36 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Performance goal 1.2.2 / 1.3.2: Effectively initiate supervisory activities at financial services institutions under the CFPB’s jurisdiction to determine compliance with the Federal fair lending laws, including the Equal Credit Opportunity Act (ECOA) and the Home Mortgage Disclosure Act (HMDA). The CFPB’s fair lending supervision program assesses whether supervised entities have engaged in, or are engaging in, violations of the Federal fair lending laws. The Bureau accomplishes this assessment through examinations that evaluate institutions’ compliance with those laws. PERFORMANCE MEASURE TABLE 13: Fair lending supervision activities opened during the fiscal year FY 2012 FY 2013 FY 2014 FY 2015 FY2016 Target NA NA NA 20-35 20-35 Actual 67 47 33 NA NA PROGRESS UPDATE AND FUTURE ACTION The decrease in supervision activities reflects risk-based prioritization decisions about where to focus supervisory resources and a reduction in the number of new HMDA Data Integrity Exams. The overall number of Fair Lending supervisory activities has decreased from FY 2012 (67) to FY 2014 (33) because, at the outset of the Bureau, Fair Lending conducted baseline risk assessments and information-gathering surveys of a large number of institutions. Fair Lending is now executing against this earlier baseline work with targeted fair lending reviews, which are more in-depth and take more time and resources than initial information gathering. Hence there are fewer supervisory reviews than in the initial period. To increase the transparency of CFPB supervisory processes, the Bureau published its HMDA Resubmission Schedule and Guidelines in October, 2013, that provide instruction and additional detail on the HMDA Verification Examination Process.

In October, the Bureau also published a bulletin that addresses mortgage lenders’ compliance with HMDA and its implementing regulation, Regulation C. Also in October, the Bureau joined the OCC, FRB, FDIC, and NCUA to issue an interagency statement to address industry questions about whether creditors would be liable under the disparate impact doctrine of the ECOA and Regulation B by originating only qualified mortgages as defined under the Bureau’s Ability-to-Repay and Qualified Mortgage Standards Rule. In January 2014, the Bureau published the Winter 2013 issue of Supervisory Highlights with sections discussing non-public supervisory actions, the HMDA and Regulation C Bulletin, and Qualified Mortgage and fair lending.

The Spring 2014 Supervisory Highlights followed in May 37 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . with a section on documenting exceptions to credit standards to mitigate fair lending risks. Finally, in September 2014, the Bureau published the Summer 2014 edition of Supervisory Highlights describing the Bureau’s fair lending supervisory activity in the indirect auto lending market so that industry participants can use the information to manage fair lending risks. Performance goal 1.2.3 / 1.3.3: Issue examination reports within the CFPB’s established time periods following the close of examinations. Effective supervision of financial institutions to foster compliance with Federal consumer financial laws requires prompt notice to institutions of matters requiring their attention and action to avoid further violations or consumer harm. A thorough report development and review process ensures high-quality reports that appropriately explain what the examination team found and why corrective actions, if any, are required. PERFORMANCE MEASURE Percentage of examination reports issued within an established period following the close of the examination TABLE 14: FY 2012 FY 2013 FY 2014 FY 2015 FY2016 Target NA Baseline 50% 60% 60% Actual NA 15% 25% NA NA PROGRESS UPDATE AND FUTURE ACTION The CFPB continues to focus on issuing high-quality examination reports and supervisory letters in a timely manner. During FY 2014, Supervision utilized a third party consultant to analyze the exam report writing and review process (exam report process) to increase its efficiency and serve the goals of the division and the CFPB. Having an adequate baseline of reports issued in FY 2013 and FY 2014, the analysis concluded that the report review process should be divided into full review and expedited review tracks. The expedited track would be for straight-forward reports and can be reviewed more quickly. The full review track would continue to be for complex reports.

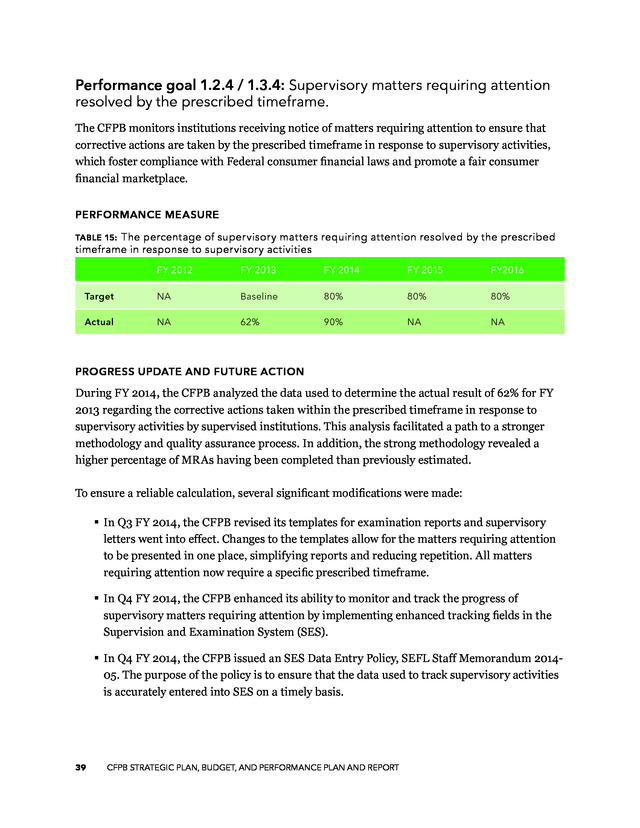

By changing the review tracks, the CFPB anticipates an increase in efficiency, resulting in reports and letters being issued in a timely manner. The new report review processes will be fully implemented in FY 2015. Even after recommended improvements are fully implemented, the CFPB will continue to review and analyze its processes to determine methods for improvement and increased effectiveness and efficiency. 38 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . Performance goal 1.2.4 / 1.3.4: Supervisory matters requiring attention resolved by the prescribed timeframe. The CFPB monitors institutions receiving notice of matters requiring attention to ensure that corrective actions are taken by the prescribed timeframe in response to supervisory activities, which foster compliance with Federal consumer financial laws and promote a fair consumer financial marketplace. PERFORMANCE MEASURE The percentage of supervisory matters requiring attention resolved by the prescribed timeframe in response to supervisory activities TABLE 15: FY 2012 FY 2013 FY 2014 FY 2015 FY2016 Target NA Baseline 80% 80% 80% Actual NA 62% 90% NA NA PROGRESS UPDATE AND FUTURE ACTION During FY 2014, the CFPB analyzed the data used to determine the actual result of 62% for FY 2013 regarding the corrective actions taken within the prescribed timeframe in response to supervisory activities by supervised institutions. This analysis facilitated a path to a stronger methodology and quality assurance process. In addition, the strong methodology revealed a higher percentage of MRAs having been completed than previously estimated. To ensure a reliable calculation, several significant modifications were made: §§ In Q3 FY 2014, the CFPB revised its templates for examination reports and supervisory letters went into effect. Changes to the templates allow for the matters requiring attention to be presented in one place, simplifying reports and reducing repetition.

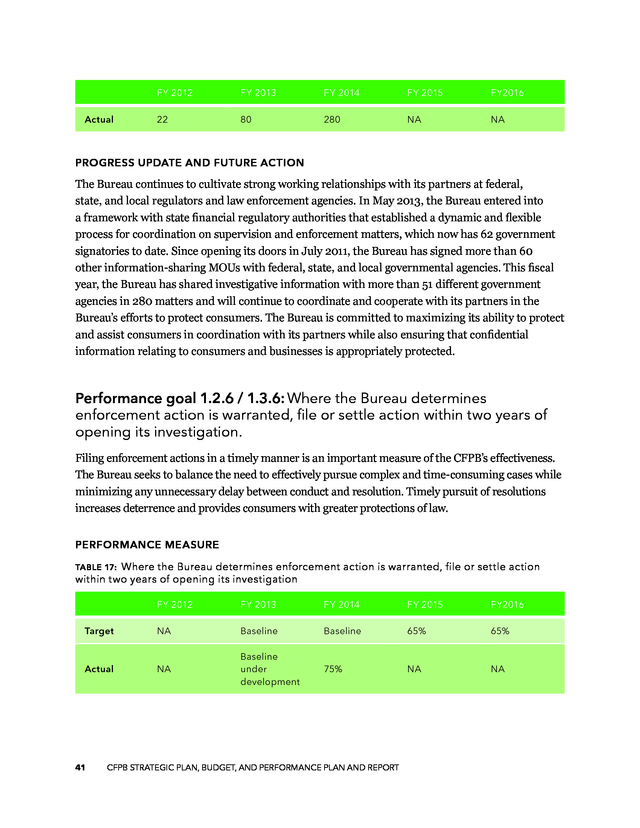

All matters requiring attention now require a specific prescribed timeframe. §§ In Q4 FY 2014, the CFPB enhanced its ability to monitor and track the progress of supervisory matters requiring attention by implementing enhanced tracking fields in the Supervision and Examination System (SES). §§ In Q4 FY 2014, the CFPB issued an SES Data Entry Policy, SEFL Staff Memorandum 201405. The purpose of the policy is to ensure that the data used to track supervisory activities is accurately entered into SES on a timely basis. 39 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . The CFPB continues to conduct onsite reviews of particular issues or actions that may require independent validation. The CFPB has and will continue to issue Supervisory Highlights several times per year, through which it apprises the public and the financial services industry of noteworthy findings of the Bureau’s supervision program. In addition to these findings – which are communicated without identifying specific institutions (except for enforcement actions already made public) – Supervisory Highlights shares remedies that Supervision has obtained for consumers who have suffered financial or other harm as a result of violations of law. The CFPB believes that Supervisory Highlights will help providers of financial products and services better understand the Bureau’s supervisory expectations so that they can ensure their operations remain in compliance with Federal consumer financial laws and serve their customers in a fair and transparent way. The CFPB intends to be transparent about the goals of its supervision program and the steps being taken to achieve those goals, while protecting the confidentiality of the underlying financial institution-specific information. Performance goal 1.2.5 / 1.3.5: Cooperate and share information with its partners in local, state, and federal law enforcement as part of its efforts to protect consumers, deter wrongdoers, and build a better marketplace. This indicator ensures that the CFPB works well with its partners at the local, state, and Federal level to share information, subject to the Bureau’s regulations, policies on information sharing, and other legal restrictions, across jurisdictions and to make the best use of limited resources. PERFORMANCE MEASURE : Instances in which the CFPB obtains information from local, state, or federal law enforcement partners that contributes to CFPB law enforcement actions, or investigations in which the CFPB cooperates or shares information with law enforcement partners.4 5 TABLE 16: FY 2012 Target NA FY 2013 NA FY 2014 FY 2015 FY2016 NA Share requested investigative information5 Share requested investigative information4 4 For this measure, the Bureau reports each instance when information is shared for the same investigation or in other circumstances as one instance. 5 When investigative information is requested by law enforcement and regulatory agencies, share responsive information where permissible under relevant law and appropriate under the circumstances. 40 CFPB STRATEGIC PLAN, BUDGET, AND PERFORMANCE PLAN AND REPORT . FY 2012 Actual FY 2013 FY 2014 FY 2015 FY2016 22 80 280 NA NA PROGRESS UPDATE AND FUTURE ACTION The Bureau continues to cultivate strong working relationships with its partners at federal, state, and local regulators and law enforcement agencies. In May 2013, the Bureau entered into a framework with state financial regulatory authorities that established a dynamic and flexible process for coordination on supervision and enforcement matters, which now has 62 government signatories to date. Since opening its doors in July 2011, the Bureau has signed more than 60 other information-sharing MOUs with federal, state, and local governmental agencies. This fiscal year, the Bureau has shared investigative information with more than 51 different government agencies in 280 matters and will continue to coordinate and cooperate with its partners in the Bureau’s efforts to protect consumers.