Description

CBIZ HEALTH REFORM MATRIX

A TOOL FOR UNDERSTANDING THE IMPACT OF HEALTH CARE REFORM

Patient Protection and Affordable Care Act (Public Law 111-148, enacted March 23, 2010) and the

Health Care and Education Reconciliation Act (Public Law 111-152, enacted March 30, 2010)

. The following matrix is divided into six categories:

EMPLOYER/PLAN SPONSOR ISSUES ....................................................................................................................... 2

REPORTING AND DISCLOSURE ISSUES ................................................................................................................... 18

TAXES AND FEES ................................................................................................................................................ 27

INSURANCE ISSUES.............................................................................................................................................

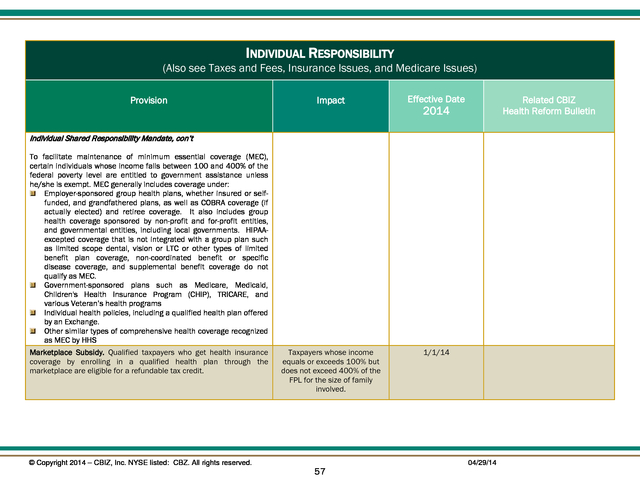

38 INDIVIDUAL RESPONSIBILITY ................................................................................................................................ 53 MEDICARE ISSUES .............................................................................................................................................. 58 © Copyright 2014 – CBIZ, Inc.

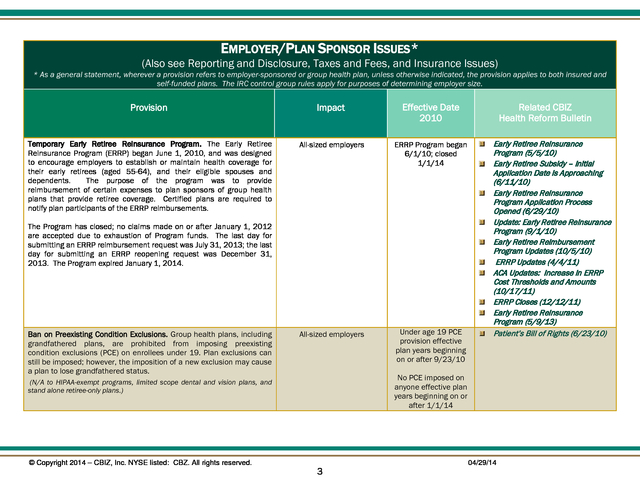

NYSE listed: CBZ. All rights reserved. 1 04/29/14 . EMPLOYER/PLAN SPONSOR ISSUES ALSO SEE REPORTING AND DISCLOSURE ISSUES, TAXES AND FEES, AND INSURANCE ISSUES © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 2 04/29/14 . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date 2010 Temporary Early Retiree Reinsurance Program. The Early Retiree Reinsurance Program (ERRP) began June 1, 2010, and was designed to encourage employers to establish or maintain health coverage for their early retirees (aged 55-64), and their eligible spouses and dependents. The purpose of the program was to provide reimbursement of certain expenses to plan sponsors of group health plans that provide retiree coverage. Certified plans are required to notify plan participants of the ERRP reimbursements. All-sized employers ERRP Program began 6/1/10; closed 1/1/14 All-sized employers Under age 19 PCE provision effective plan years beginning on or after 9/23/10 The Program has closed; no claims made on or after January 1, 2012 are accepted due to exhaustion of Program funds.

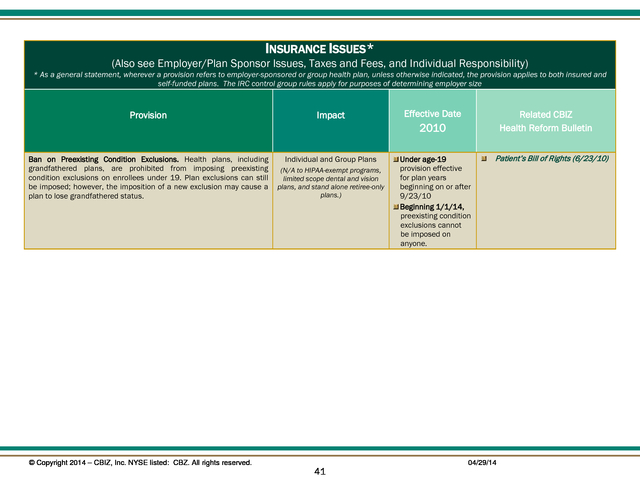

The last day for submitting an ERRP reimbursement request was July 31, 2013; the last day for submitting an ERRP reopening request was December 31, 2013. The Program expired January 1, 2014. Ban on Preexisting Condition Exclusions. Group health plans, including grandfathered plans, are prohibited from imposing preexisting condition exclusions (PCE) on enrollees under 19.

Plan exclusions can still be imposed; however, the imposition of a new exclusion may cause a plan to lose grandfathered status. Early Retiree Reinsurance Program (5/5/10) Early Retiree Subsidy – Initial Application Date is Approaching (6/11/10) Early Retiree Reinsurance Program Application Process Opened (6/29/10) Update: Early Retiree Reinsurance Program (9/1/10) Early Retiree Reimbursement Program Updates (10/5/10) ERRP Updates (4/4/11) ACA Updates: Increase in ERRP Cost Thresholds and Amounts (10/17/11) ERRP Closes (12/12/11) Early Retiree Reinsurance Program (5/9/13) Patient’s Bill of Rights (6/23/10) No PCE imposed on anyone effective plan years beginning on or after 1/1/14 (N/A to HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. Related CBIZ Health Reform Bulletin 3 04/29/14 .

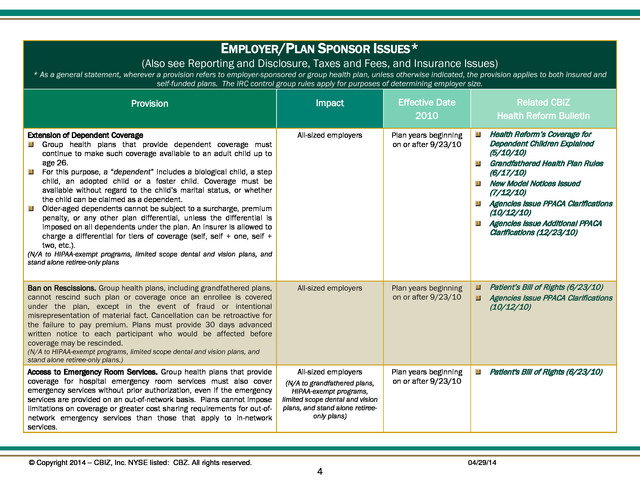

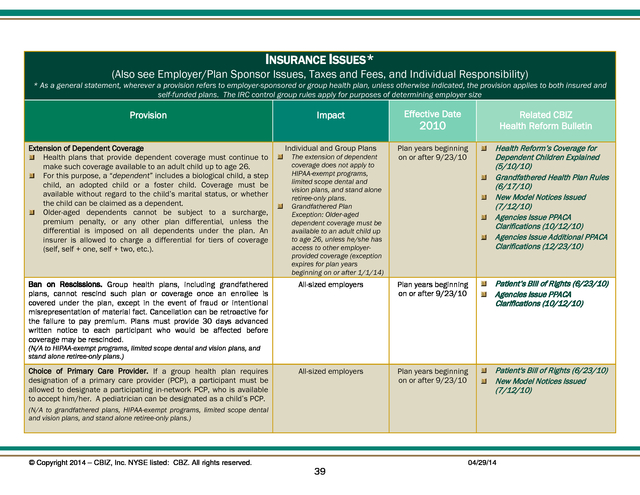

EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date 2010 Related CBIZ Health Reform Bulletin Extension of Dependent Coverage Group health plans that provide dependent coverage must continue to make such coverage available to an adult child up to age 26. For this purpose, a “dependent” includes a biological child, a step child, an adopted child or a foster child. Coverage must be available without regard to the child’s marital status, or whether the child can be claimed as a dependent. Older-aged dependents cannot be subject to a surcharge, premium penalty, or any other plan differential, unless the differential is imposed on all dependents under the plan. An insurer is allowed to charge a differential for tiers of coverage (self, self + one, self + two, etc.). All-sized employers Plan years beginning on or after 9/23/10 Health Reform’s Coverage for Dependent Children Explained (5/10/10) Grandfathered Health Plan Rules (6/17/10) New Model Notices Issued (7/12/10) Agencies Issue PPACA Clarifications (10/12/10) Agencies Issue Additional PPACA Clarifications (12/23/10) Ban on Rescissions.

Group health plans, including grandfathered plans, cannot rescind such plan or coverage once an enrollee is covered under the plan, except in the event of fraud or intentional misrepresentation of material fact. Cancellation can be retroactive for the failure to pay premium. Plans must provide 30 days advanced written notice to each participant who would be affected before coverage may be rescinded. All-sized employers Plan years beginning on or after 9/23/10 Patient’s Bill of Rights (6/23/10) Agencies Issue PPACA Clarifications (10/12/10) Access to Emergency Room Services.

Group health plans that provide coverage for hospital emergency room services must also cover emergency services without prior authorization, even if the emergency services are provided on an out-of-network basis. Plans cannot impose limitations on coverage or greater cost sharing requirements for out-ofnetwork emergency services than those that apply to in-network services. All-sized employers Plan years beginning on or after 9/23/10 Patient's Bill of Rights (6/23/10) (N/A to HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans (N/A to HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

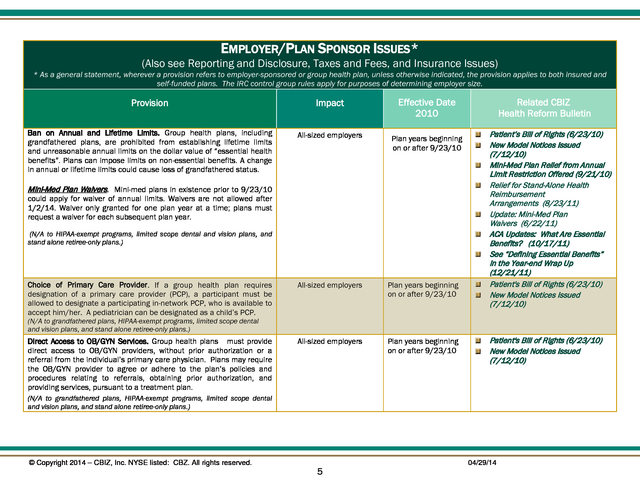

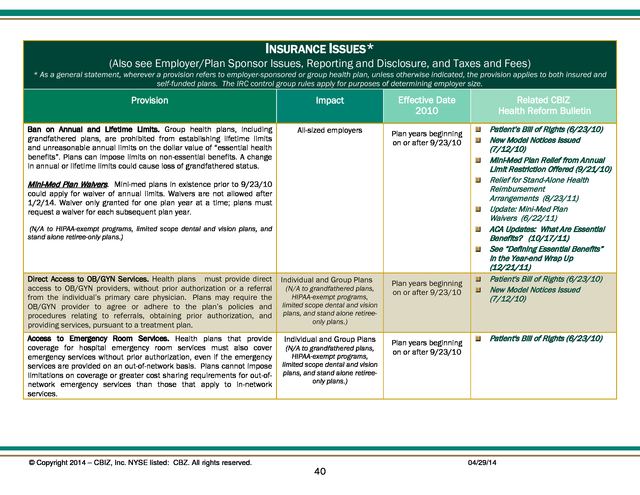

All rights reserved. (N/A to grandfathered plans, HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retireeonly plans) 4 04/29/14 . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date 2010 Ban on Annual and Lifetime Limits. Group health plans, including grandfathered plans, are prohibited from establishing lifetime limits and unreasonable annual limits on the dollar value of “essential health benefits”. Plans can impose limits on non-essential benefits.

A change in annual or lifetime limits could cause loss of grandfathered status. All-sized employers Plan years beginning on or after 9/23/10 Mini-Med Plan Waivers. Mini-med plans in existence prior to 9/23/10 could apply for waiver of annual limits. Waivers are not allowed after 1/2/14.

Waiver only granted for one plan year at a time; plans must request a waiver for each subsequent plan year. (N/A to HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) Choice of Primary Care Provider. If a group health plan requires designation of a primary care provider (PCP), a participant must be allowed to designate a participating in-network PCP, who is available to accept him/her. A pediatrician can be designated as a child’s PCP. All-sized employers Plan years beginning on or after 9/23/10 Direct Access to OB/GYN Services.

Group health plans must provide direct access to OB/GYN providers, without prior authorization or a referral from the individual’s primary care physician. Plans may require the OB/GYN provider to agree or adhere to the plan’s policies and procedures relating to referrals, obtaining prior authorization, and providing services, pursuant to a treatment plan. All-sized employers Plan years beginning on or after 9/23/10 Related CBIZ Health Reform Bulletin Patient’s Bill of Rights (6/23/10) New Model Notices Issued (7/12/10) Mini-Med Plan Relief from Annual Limit Restriction Offered (9/21/10) Relief for Stand-Alone Health Reimbursement Arrangements (8/23/11) Update: Mini-Med Plan Waivers (6/22/11) ACA Updates: What Are Essential Benefits? (10/17/11) See “Defining Essential Benefits” in the Year-end Wrap Up (12/21/11) Patient's Bill of Rights (6/23/10) New Model Notices Issued (7/12/10) (N/A to grandfathered plans, HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) Patient's Bill of Rights (6/23/10) New Model Notices Issued (7/12/10) (N/A to grandfathered plans, HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

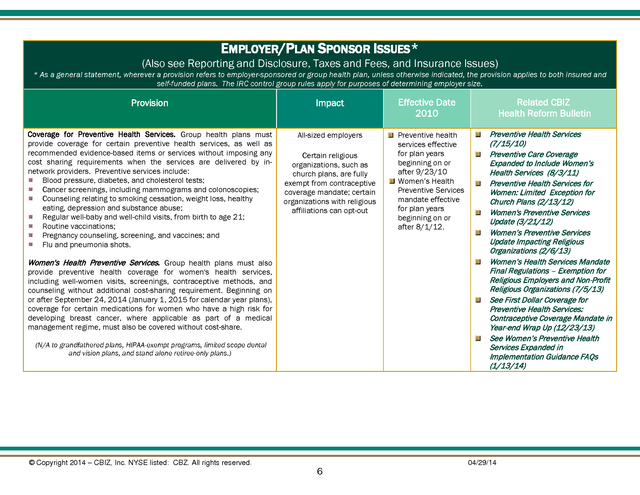

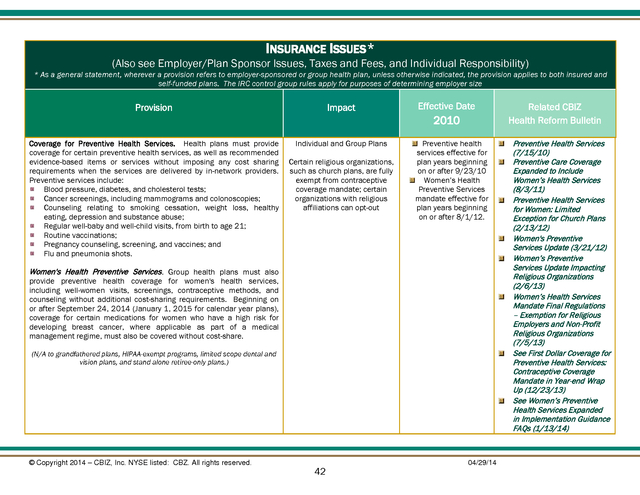

All rights reserved. 5 04/29/14 . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Coverage for Preventive Health Services. Group health plans must provide coverage for certain preventive health services, as well as recommended evidence-based items or services without imposing any cost sharing requirements when the services are delivered by innetwork providers. Preventive services include: Blood pressure, diabetes, and cholesterol tests; Cancer screenings, including mammograms and colonoscopies; Counseling relating to smoking cessation, weight loss, healthy eating, depression and substance abuse; Regular well-baby and well-child visits, from birth to age 21; Routine vaccinations; Pregnancy counseling, screening, and vaccines; and Flu and pneumonia shots. All-sized employers Certain religious organizations, such as church plans, are fully exempt from contraceptive coverage mandate; certain organizations with religious affiliations can opt-out Women's Health Preventive Services.

Group health plans must also provide preventive health coverage for women's health services, including well-women visits, screenings, contraceptive methods, and counseling without additional cost-sharing requirement. Beginning on or after September 24, 2014 (January 1, 2015 for calendar year plans), coverage for certain medications for women who have a high risk for developing breast cancer, where applicable as part of a medical management regime, must also be covered without cost-share. (N/A to grandfathered plans, HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

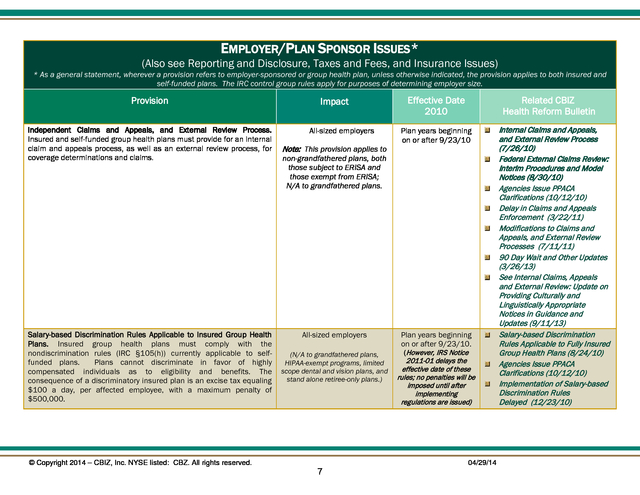

All rights reserved. 6 Effective Date 2010 Preventive health services effective for plan years beginning on or after 9/23/10 Women’s Health Preventive Services mandate effective for plan years beginning on or after 8/1/12. Related CBIZ Health Reform Bulletin Preventive Health Services (7/15/10) Preventive Care Coverage Expanded to Include Women’s Health Services (8/3/11) Preventive Health Services for Women: Limited Exception for Church Plans (2/13/12) Women's Preventive Services Update (3/21/12) Women’s Preventive Services Update Impacting Religious Organizations (2/6/13) Women’s Health Services Mandate Final Regulations – Exemption for Religious Employers and Non-Profit Religious Organizations (7/5/13) See First Dollar Coverage for Preventive Health Services: Contraceptive Coverage Mandate in Year-end Wrap Up (12/23/13) See Women’s Preventive Health Services Expanded in Implementation Guidance FAQs (1/13/14) 04/29/14 . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Independent Claims and Appeals, and External Review Process. Insured and self-funded group health plans must provide for an internal claim and appeals process, as well as an external review process, for coverage determinations and claims. Salary-based Discrimination Rules Applicable to Insured Group Health Plans. Insured group health plans must comply with the nondiscrimination rules (IRC §105(h)) currently applicable to selffunded plans. Plans cannot discriminate in favor of highly compensated individuals as to eligibility and benefits. The consequence of a discriminatory insured plan is an excise tax equaling $100 a day, per affected employee, with a maximum penalty of $500,000. © Copyright 2014 – CBIZ, Inc.

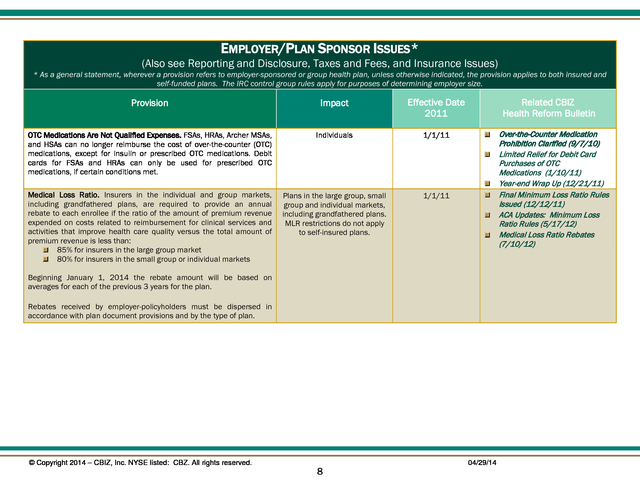

NYSE listed: CBZ. All rights reserved. Impact All-sized employers Note: This provision applies to Effective Date 2010 Related CBIZ Health Reform Bulletin Plan years beginning on or after 9/23/10 non-grandfathered plans, both those subject to ERISA and those exempt from ERISA; N/A to grandfathered plans. All-sized employers (N/A to grandfathered plans, HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) 7 Plan years beginning on or after 9/23/10. (However, IRS Notice 2011-01 delays the effective date of these rules; no penalties will be imposed until after implementing regulations are issued) 04/29/14 Internal Claims and Appeals, and External Review Process (7/26/10) Federal External Claims Review: Interim Procedures and Model Notices (8/30/10) Agencies Issue PPACA Clarifications (10/12/10) Delay in Claims and Appeals Enforcement (3/22/11) Modifications to Claims and Appeals, and External Review Processes (7/11/11) 90 Day Wait and Other Updates (3/26/13) See Internal Claims, Appeals and External Review: Update on Providing Culturally and Linguistically Appropriate Notices in Guidance and Updates (9/11/13) Salary-based Discrimination Rules Applicable to Fully Insured Group Health Plans (8/24/10) Agencies Issue PPACA Clarifications (10/12/10) Implementation of Salary-based Discrimination Rules Delayed (12/23/10) . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date 2011 OTC Medications Are Not Qualified Expenses. FSAs, HRAs, Archer MSAs, and HSAs can no longer reimburse the cost of over-the-counter (OTC) medications, except for insulin or prescribed OTC medications. Debit cards for FSAs and HRAs can only be used for prescribed OTC medications, if certain conditions met. Individuals 1/1/11 Medical Loss Ratio.

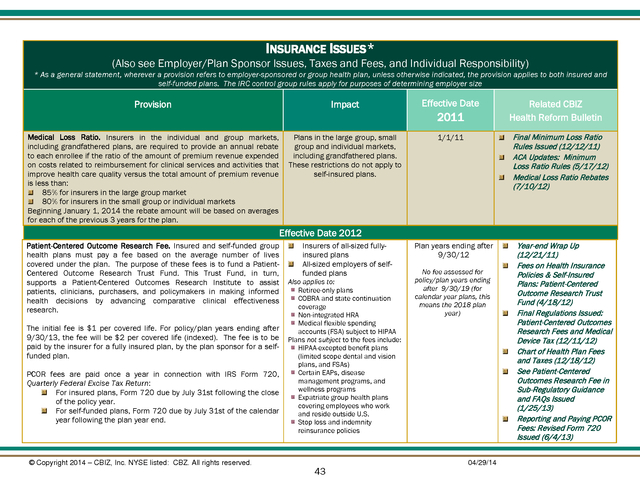

Insurers in the individual and group markets, including grandfathered plans, are required to provide an annual rebate to each enrollee if the ratio of the amount of premium revenue expended on costs related to reimbursement for clinical services and activities that improve health care quality versus the total amount of premium revenue is less than: 85% for insurers in the large group market 80% for insurers in the small group or individual markets Plans in the large group, small group and individual markets, including grandfathered plans. MLR restrictions do not apply to self-insured plans. Related CBIZ Health Reform Bulletin 1/1/11 Over-the-Counter Medication Prohibition Clarified (9/7/10) Limited Relief for Debit Card Purchases of OTC Medications (1/10/11) Year-end Wrap Up (12/21/11) Final Minimum Loss Ratio Rules Issued (12/12/11) ACA Updates: Minimum Loss Ratio Rules (5/17/12) Medical Loss Ratio Rebates (7/10/12) Beginning January 1, 2014 the rebate amount will be based on averages for each of the previous 3 years for the plan. Rebates received by employer-policyholders must be dispersed in accordance with plan document provisions and by the type of plan. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 8 04/29/14 .

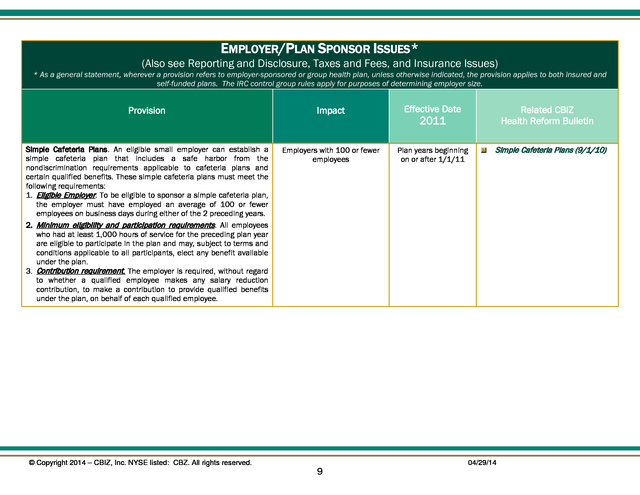

EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Simple Cafeteria Plans. An eligible small employer can establish a simple cafeteria plan that includes a safe harbor from the nondiscrimination requirements applicable to cafeteria plans and certain qualified benefits. These simple cafeteria plans must meet the following requirements: 1.

Eligible Employer. To be eligible to sponsor a simple cafeteria plan, the employer must have employed an average of 100 or fewer employees on business days during either of the 2 preceding years. 2. Minimum eligibility and participation requirements.

All employees who had at least 1,000 hours of service for the preceding plan year are eligible to participate in the plan and may, subject to terms and conditions applicable to all participants, elect any benefit available under the plan. 3. Contribution requirement. The employer is required, without regard to whether a qualified employee makes any salary reduction contribution, to make a contribution to provide qualified benefits under the plan, on behalf of each qualified employee. Employers with 100 or fewer employees Plan years beginning on or after 1/1/11 © Copyright 2014 – CBIZ, Inc.

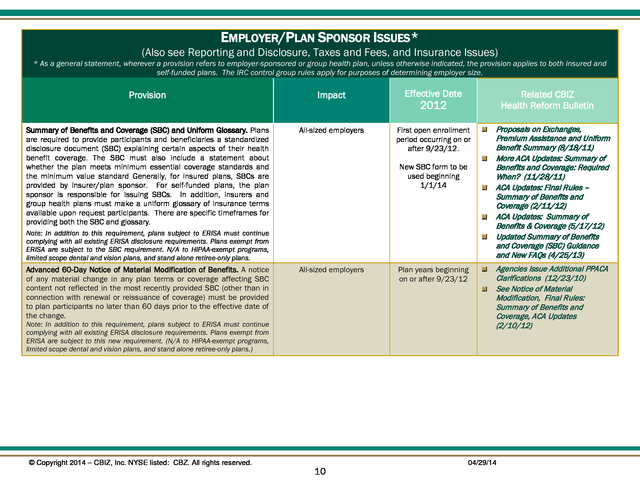

NYSE listed: CBZ. All rights reserved. 9 Related CBIZ Health Reform Bulletin 2011 Simple Cafeteria Plans (9/1/10) 04/29/14 . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Summary of Benefits and Coverage (SBC) and Uniform Glossary. Plans are required to provide participants and beneficiaries a standardized disclosure document (SBC) explaining certain aspects of their health benefit coverage. The SBC must also include a statement about whether the plan meets minimum essential coverage standards and the minimum value standard Generally, for insured plans, SBCs are provided by insurer/plan sponsor.

For self-funded plans, the plan sponsor is responsible for issuing SBCs. In addition, insurers and group health plans must make a uniform glossary of insurance terms available upon request participants. There are specific timeframes for providing both the SBC and glossary. All-sized employers First open enrollment period occurring on or after 9/23/12. Related CBIZ Health Reform Bulletin 2012 New SBC form to be used beginning 1/1/14 Note: In addition to this requirement, plans subject to ERISA must continue complying with all existing ERISA disclosure requirements.

Plans exempt from ERISA are subject to the SBC requirement. N/A to HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans. Advanced 60-Day Notice of Material Modification of Benefits. A notice of any material change in any plan terms or coverage affecting SBC content not reflected in the most recently provided SBC (other than in connection with renewal or reissuance of coverage) must be provided to plan participants no later than 60 days prior to the effective date of the change. All-sized employers Note: In addition to this requirement, plans subject to ERISA must continue complying with all existing ERISA disclosure requirements.

Plans exempt from ERISA are subject to this new requirement. (N/A to HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

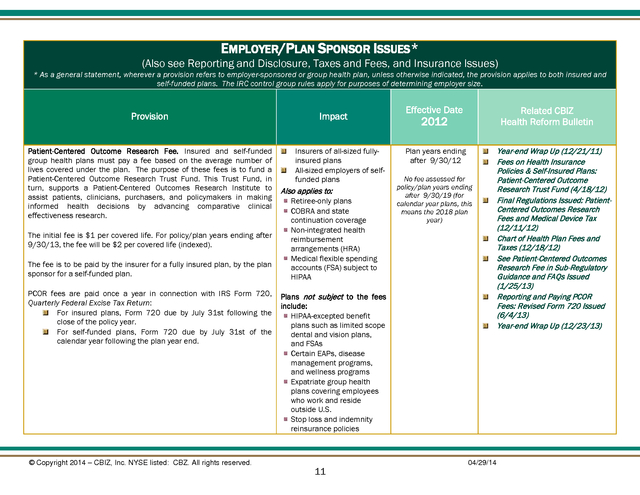

All rights reserved. 10 Plan years beginning on or after 9/23/12 Proposals on Exchanges, Premium Assistance and Uniform Benefit Summary (8/18/11) More ACA Updates: Summary of Benefits and Coverage: Required When? (11/28/11) ACA Updates: Final Rules – Summary of Benefits and Coverage (2/11/12) ACA Updates: Summary of Benefits & Coverage (5/17/12) Updated Summary of Benefits and Coverage (SBC) Guidance and New FAQs (4/25/13) Agencies Issue Additional PPACA Clarifications (12/23/10) See Notice of Material Modification, Final Rules: Summary of Benefits and Coverage, ACA Updates (2/10/12) 04/29/14 . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Patient-Centered Outcome Research Fee. Insured and self-funded group health plans must pay a fee based on the average number of lives covered under the plan. The purpose of these fees is to fund a Patient-Centered Outcome Research Trust Fund.

This Trust Fund, in turn, supports a Patient-Centered Outcomes Research Institute to assist patients, clinicians, purchasers, and policymakers in making informed health decisions by advancing comparative clinical effectiveness research. The initial fee is $1 per covered life. For policy/plan years ending after 9/30/13, the fee will be $2 per covered life (indexed). The fee is to be paid by the insurer for a fully insured plan, by the plan sponsor for a self-funded plan. PCOR fees are paid once a year in connection with IRS Form 720, Quarterly Federal Excise Tax Return: For insured plans, Form 720 due by July 31st following the close of the policy year. For self-funded plans, Form 720 due by July 31st of the calendar year following the plan year end. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

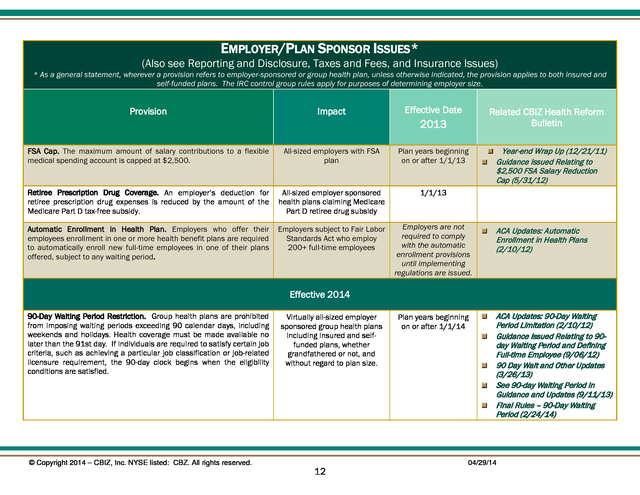

All rights reserved. Impact Insurers of all-sized fullyinsured plans All-sized employers of selffunded plans Also applies to: Retiree-only plans COBRA and state continuation coverage Non-integrated health reimbursement arrangements (HRA) Medical flexible spending accounts (FSA) subject to HIPAA Effective Date Related CBIZ Health Reform Bulletin 2012 Plan years ending after 9/30/12 No fee assessed for policy/plan years ending after 9/30/19 (for calendar year plans, this means the 2018 plan year) Plans not subject to the fees include: HIPAA-excepted benefit plans such as limited scope dental and vision plans, and FSAs Certain EAPs, disease management programs, and wellness programs Expatriate group health plans covering employees who work and reside outside U.S. Stop loss and indemnity reinsurance policies 11 04/29/14 Year-end Wrap Up (12/21/11) Fees on Health Insurance Policies & Self-Insured Plans: Patient-Centered Outcome Research Trust Fund (4/18/12) Final Regulations Issued: PatientCentered Outcomes Research Fees and Medical Device Tax (12/11/12) Chart of Health Plan Fees and Taxes (12/18/12) See Patient-Centered Outcomes Research Fee in Sub-Regulatory Guidance and FAQs Issued (1/25/13) Reporting and Paying PCOR Fees: Revised Form 720 Issued (6/4/13) Year-end Wrap Up (12/23/13) . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date FSA Cap. The maximum amount of salary contributions to a flexible medical spending account is capped at $2,500. All-sized employers with FSA plan Plan years beginning on or after 1/1/13 Retiree Prescription Drug Coverage. An employer’s deduction for retiree prescription drug expenses is reduced by the amount of the Medicare Part D tax-free subsidy. All-sized employer sponsored health plans claiming Medicare Part D retiree drug subsidy 1/1/13 Automatic Enrollment in Health Plan.

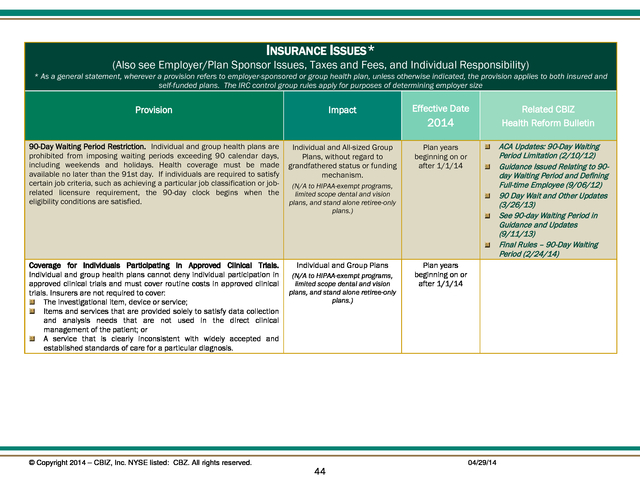

Employers who offer their employees enrollment in one or more health benefit plans are required to automatically enroll new full-time employees in one of their plans offered, subject to any waiting period. Employers subject to Fair Labor Standards Act who employ 200+ full-time employees Employers are not required to comply with the automatic enrollment provisions until implementing regulations are issued. Related CBIZ Health Reform Bulletin 2013 Year-end Wrap Up (12/21/11) Guidance Issued Relating to $2,500 FSA Salary Reduction Cap (5/31/12) ACA Updates: Automatic Enrollment in Health Plans (2/10/12) Effective 2014 90-Day Waiting Period Restriction. Group health plans are prohibited from imposing waiting periods exceeding 90 calendar days, including weekends and holidays. Health coverage must be made available no later than the 91st day.

If individuals are required to satisfy certain job criteria, such as achieving a particular job classification or job-related licensure requirement, the 90-day clock begins when the eligibility conditions are satisfied. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. Virtually all-sized employer sponsored group health plans including insured and selffunded plans, whether grandfathered or not, and without regard to plan size. 12 Plan years beginning on or after 1/1/14 ACA Updates: 90-Day Waiting Period Limitation (2/10/12) Guidance Issued Relating to 90day Waiting Period and Defining Full-time Employee (9/06/12) 90 Day Wait and Other Updates (3/26/13) See 90-day Waiting Period in Guidance and Updates (9/11/13) Final Rules – 90-Day Waiting Period (2/24/14) 04/29/14 .

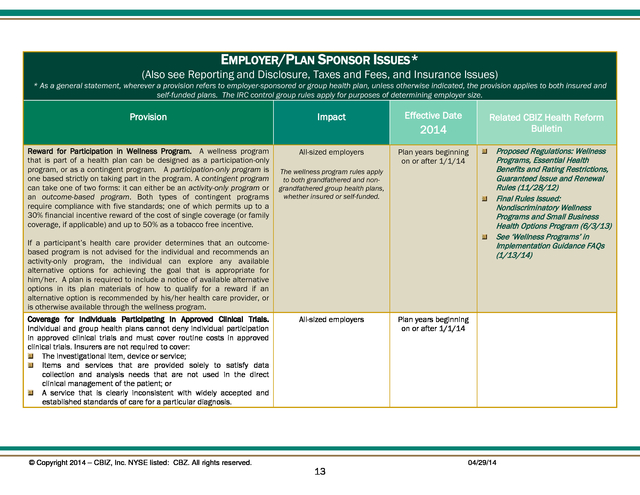

EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Reward for Participation in Wellness Program. A wellness program that is part of a health plan can be designed as a participation-only program, or as a contingent program. A participation-only program is one based strictly on taking part in the program.

A contingent program can take one of two forms: it can either be an activity-only program or an outcome-based program. Both types of contingent programs require compliance with five standards; one of which permits up to a 30% financial incentive reward of the cost of single coverage (or family coverage, if applicable) and up to 50% as a tobacco free incentive. All-sized employers Plan years beginning on or after 1/1/14 Related CBIZ Health Reform Bulletin 2014 The wellness program rules apply to both grandfathered and nongrandfathered group health plans, whether insured or self-funded. If a participant’s health care provider determines that an outcomebased program is not advised for the individual and recommends an activity-only program, the individual can explore any available alternative options for achieving the goal that is appropriate for him/her. A plan is required to include a notice of available alternative options in its plan materials of how to qualify for a reward if an alternative option is recommended by his/her health care provider, or is otherwise available through the wellness program. Coverage for Individuals Participating in Approved Clinical Trials. Individual and group health plans cannot deny individual participation in approved clinical trials and must cover routine costs in approved clinical trials.

Insurers are not required to cover: The investigational item, device or service; Items and services that are provided solely to satisfy data collection and analysis needs that are not used in the direct clinical management of the patient; or A service that is clearly inconsistent with widely accepted and established standards of care for a particular diagnosis. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. All-sized employers 13 Proposed Regulations: Wellness Programs, Essential Health Benefits and Rating Restrictions, Guaranteed Issue and Renewal Rules (11/28/12) Final Rules Issued: Nondiscriminatory Wellness Programs and Small Business Health Options Program (6/3/13) See ‘Wellness Programs’ in Implementation Guidance FAQs (1/13/14) Plan years beginning on or after 1/1/14 04/29/14 .

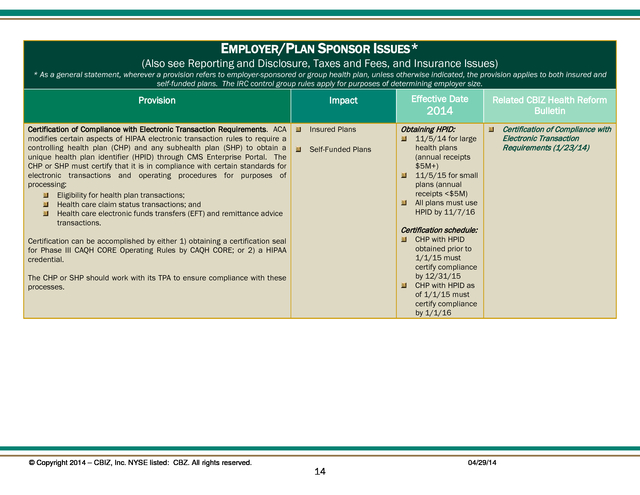

EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Certification of Compliance with Electronic Transaction Requirements. ACA modifies certain aspects of HIPAA electronic transaction rules to require a controlling health plan (CHP) and any subhealth plan (SHP) to obtain a unique health plan identifier (HPID) through CMS Enterprise Portal. The CHP or SHP must certify that it is in compliance with certain standards for electronic transactions and operating procedures for purposes of processing: Eligibility for health plan transactions; Health care claim status transactions; and Health care electronic funds transfers (EFT) and remittance advice transactions. Impact Insured Plans Self-Funded Plans 2014 Related CBIZ Health Reform Bulletin Obtaining HPID: 11/5/14 for large health plans (annual receipts $5M+) 11/5/15 for small plans (annual receipts <$5M) All plans must use HPID by 11/7/16 Certification schedule: CHP with HPID obtained prior to 1/1/15 must certify compliance by 12/31/15 CHP with HPID as of 1/1/15 must certify compliance by 1/1/16 Certification can be accomplished by either 1) obtaining a certification seal for Phase III CAQH CORE Operating Rules by CAQH CORE; or 2) a HIPAA credential. The CHP or SHP should work with its TPA to ensure compliance with these processes. © Copyright 2014 – CBIZ, Inc.

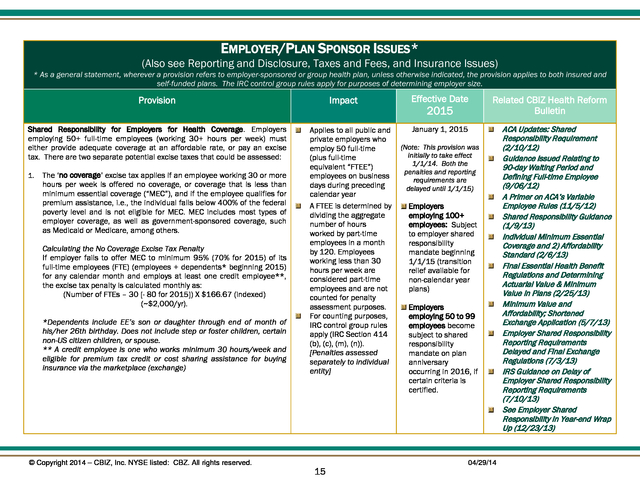

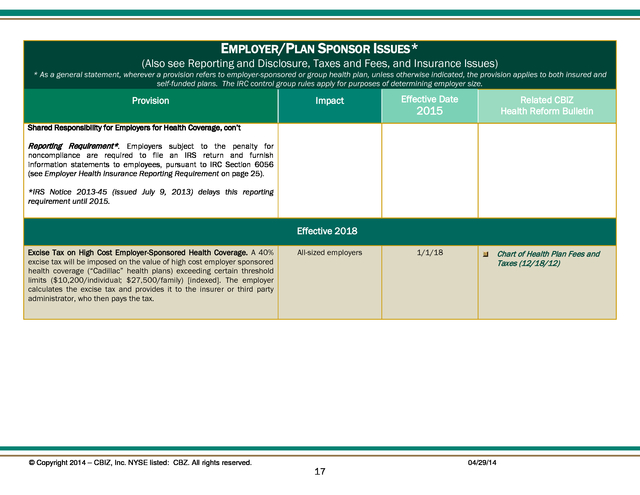

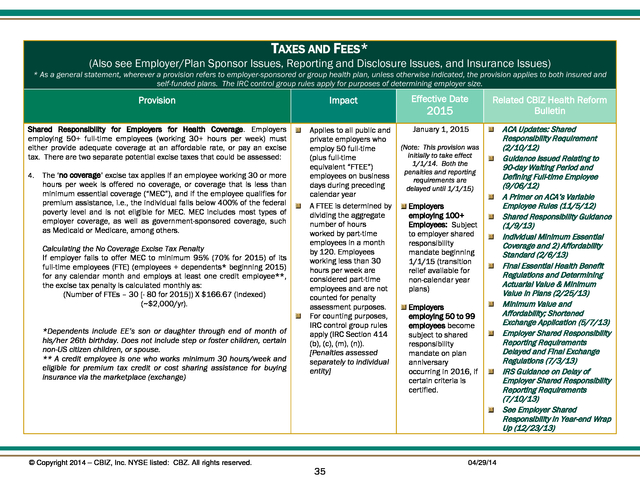

NYSE listed: CBZ. All rights reserved. Effective Date 14 04/29/14 Certification of Compliance with Electronic Transaction Requirements (1/23/14) . EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Shared Responsibility for Employers for Health Coverage. Employers employing 50+ full-time employees (working 30+ hours per week) must either provide adequate coverage at an affordable rate, or pay an excise tax. There are two separate potential excise taxes that could be assessed: 1. The ‘no coverage’ excise tax applies if an employee working 30 or more hours per week is offered no coverage, or coverage that is less than minimum essential coverage (“MEC”), and if the employee qualifies for premium assistance, i.e., the individual falls below 400% of the federal poverty level and is not eligible for MEC.

MEC includes most types of employer coverage, as well as government-sponsored coverage, such as Medicaid or Medicare, among others. Calculating the No Coverage Excise Tax Penalty If employer fails to offer MEC to minimum 95% (70% for 2015) of its full-time employees (FTE) (employees + dependents* beginning 2015) for any calendar month and employs at least one credit employee**, the excise tax penalty is calculated monthly as: (Number of FTEs – 30 [- 80 for 2015]) X $166.67 (indexed) (~$2,000/yr). *Dependents include EE’s son or daughter through end of month of his/her 26th birthday. Does not include step or foster children, certain non-US citizen children, or spouse. ** A credit employee is one who works minimum 30 hours/week and eligible for premium tax credit or cost sharing assistance for buying insurance via the marketplace (exchange) © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

All rights reserved. Impact Applies to all public and private employers who employ 50 full-time (plus full-time equivalent “FTEE”) employees on business days during preceding calendar year A FTEE is determined by dividing the aggregate number of hours worked by part-time employees in a month by 120. Employees working less than 30 hours per week are considered part-time employees and are not counted for penalty assessment purposes. For counting purposes, IRC control group rules apply (IRC Section 414 (b), (c), (m), (n)). [Penalties assessed separately to individual entity] 15 Effective Date 2015 Related CBIZ Health Reform Bulletin January 1, 2015 (Note: This provision was initially to take effect 1/1/14. Both the penalties and reporting requirements are delayed until 1/1/15) Employers employing 100+ employees: Subject to employer shared responsibility mandate beginning 1/1/15 (transition relief available for non-calendar year plans) Employers employing 50 to 99 employees become subject to shared responsibility mandate on plan anniversary occurring in 2016, if certain criteria is certified. 04/29/14 ACA Updates: Shared Responsibility Requirement (2/10/12) Guidance Issued Relating to 90-day Waiting Period and Defining Full-time Employee (9/06/12) A Primer on ACA’s Variable Employee Rules (11/5/12) Shared Responsibility Guidance (1/9/13) Individual Minimum Essential Coverage and 2) Affordability Standard (2/6/13) Final Essential Health Benefit Regulations and Determining Actuarial Value & Minimum Value in Plans (2/25/13) Minimum Value and Affordability; Shortened Exchange Application (5/7/13) Employer Shared Responsibility Reporting Requirements Delayed and Final Exchange Regulations (7/3/13) IRS Guidance on Delay of Employer Shared Responsibility Reporting Requirements (7/10/13) See Employer Shared Responsibility in Year-end Wrap Up (12/23/13) .

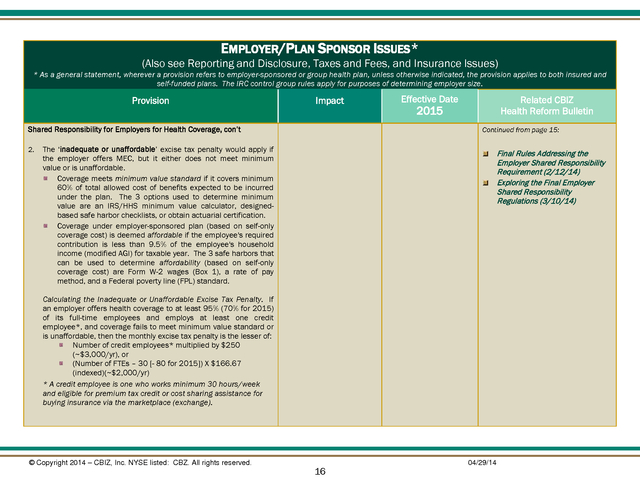

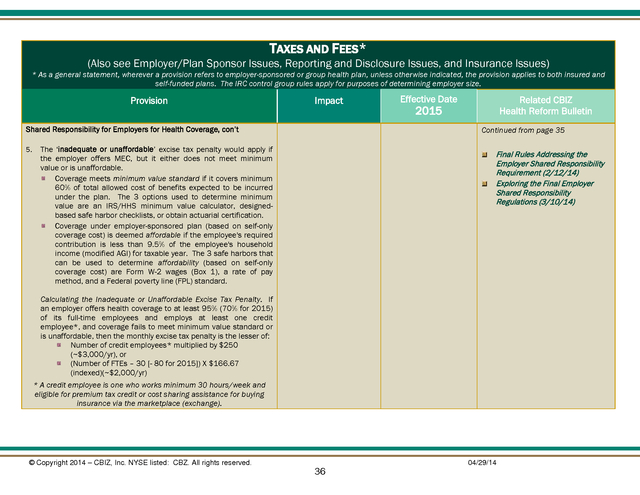

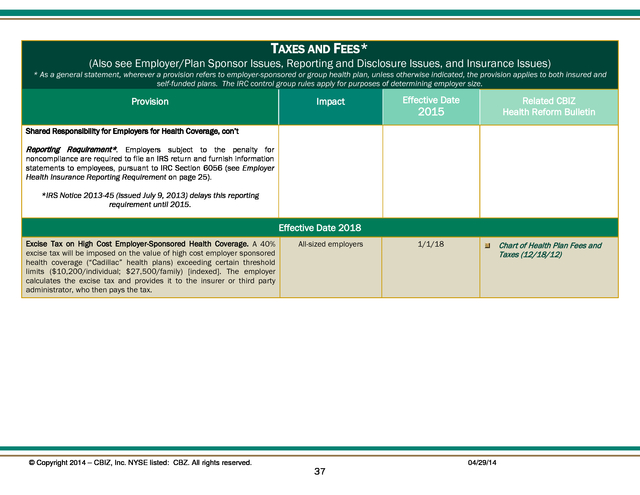

EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Shared Responsibility for Employers for Health Coverage, con’t 2. Effective Date Related CBIZ Health Reform Bulletin 2015 Continued from page 15: The ‘inadequate or unaffordable’ excise tax penalty would apply if the employer offers MEC, but it either does not meet minimum value or is unaffordable. Coverage meets minimum value standard if it covers minimum 60% of total allowed cost of benefits expected to be incurred under the plan. The 3 options used to determine minimum value are an IRS/HHS minimum value calculator, designedbased safe harbor checklists, or obtain actuarial certification. Coverage under employer-sponsored plan (based on self-only coverage cost) is deemed affordable if the employee's required contribution is less than 9.5% of the employee's household income (modified AGI) for taxable year. The 3 safe harbors that can be used to determine affordability (based on self-only coverage cost) are Form W-2 wages (Box 1), a rate of pay method, and a Federal poverty line (FPL) standard. Final Rules Addressing the Employer Shared Responsibility Requirement (2/12/14) Exploring the Final Employer Shared Responsibility Regulations (3/10/14) Calculating the Inadequate or Unaffordable Excise Tax Penalty.

If an employer offers health coverage to at least 95% (70% for 2015) of its full-time employees and employs at least one credit employee*, and coverage fails to meet minimum value standard or is unaffordable, then the monthly excise tax penalty is the lesser of: Number of credit employees* multiplied by $250 (~$3,000/yr), or (Number of FTEs – 30 [- 80 for 2015]) X $166.67 (indexed)(~$2,000/yr) * A credit employee is one who works minimum 30 hours/week and eligible for premium tax credit or cost sharing assistance for buying insurance via the marketplace (exchange). © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 16 04/29/14 .

EMPLOYER/PLAN SPONSOR ISSUES* (Also see Reporting and Disclosure, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Related CBIZ Health Reform Bulletin 1/1/18 Chart of Health Plan Fees and Taxes (12/18/12) 2015 Shared Responsibility for Employers for Health Coverage, con’t Reporting Requirement*. Employers subject to the penalty for noncompliance are required to file an IRS return and furnish information statements to employees, pursuant to IRC Section 6056 (see Employer Health Insurance Reporting Requirement on page 25). *IRS Notice 2013-45 (issued July 9, 2013) delays this reporting requirement until 2015. Effective 2018 Excise Tax on High Cost Employer-Sponsored Health Coverage. A 40% excise tax will be imposed on the value of high cost employer sponsored health coverage (“Cadillac” health plans) exceeding certain threshold limits ($10,200/individual; $27,500/family) [indexed].

The employer calculates the excise tax and provides it to the insurer or third party administrator, who then pays the tax. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. All-sized employers 17 04/29/14 .

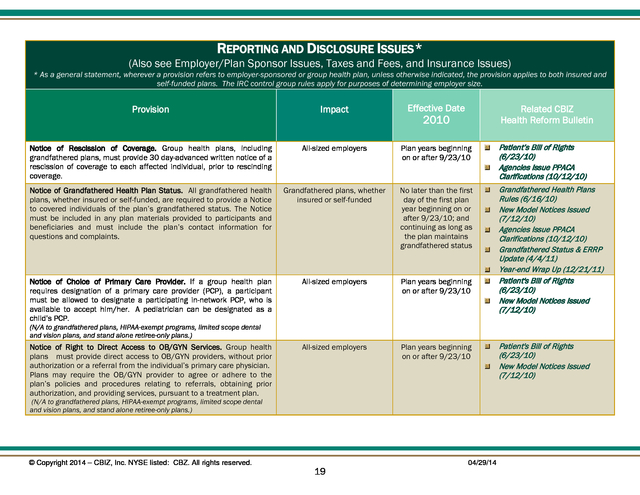

REPORTING AND DISCLOSURE ISSUES ALSO SEE EMPLOYER/PLAN SPONSOR ISSUES, TAXES AND FEES, AND INSURANCE ISSUES © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 18 04/29/14 . REPORTING AND DISCLOSURE ISSUES* (Also see Employer/Plan Sponsor Issues, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Notice of Rescission of Coverage. Group health plans, including grandfathered plans, must provide 30 day-advanced written notice of a rescission of coverage to each affected individual, prior to rescinding coverage. All-sized employers Plan years beginning on or after 9/23/10 Patient’s Bill of Rights (6/23/10) Agencies Issue PPACA Clarifications (10/12/10) Notice of Grandfathered Health Plan Status. All grandfathered health plans, whether insured or self-funded, are required to provide a Notice to covered individuals of the plan’s grandfathered status.

The Notice must be included in any plan materials provided to participants and beneficiaries and must include the plan’s contact information for questions and complaints. Grandfathered plans, whether insured or self-funded No later than the first day of the first plan year beginning on or after 9/23/10; and continuing as long as the plan maintains grandfathered status Notice of Choice of Primary Care Provider. If a group health plan requires designation of a primary care provider (PCP), a participant must be allowed to designate a participating in-network PCP, who is available to accept him/her. A pediatrician can be designated as a child’s PCP. All-sized employers Plan years beginning on or after 9/23/10 Grandfathered Health Plans Rules (6/16/10) New Model Notices Issued (7/12/10) Agencies Issue PPACA Clarifications (10/12/10) Grandfathered Status & ERRP Update (4/4/11) Year-end Wrap Up (12/21/11) Patient's Bill of Rights (6/23/10) New Model Notices Issued (7/12/10) Notice of Right to Direct Access to OB/GYN Services.

Group health plans must provide direct access to OB/GYN providers, without prior authorization or a referral from the individual’s primary care physician. Plans may require the OB/GYN provider to agree or adhere to the plan’s policies and procedures relating to referrals, obtaining prior authorization, and providing services, pursuant to a treatment plan. All-sized employers Plan years beginning on or after 9/23/10 Related CBIZ Health Reform Bulletin 2010 (N/A to grandfathered plans, HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) (N/A to grandfathered plans, HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 19 04/29/14 Patient's Bill of Rights (6/23/10) New Model Notices Issued (7/12/10) .

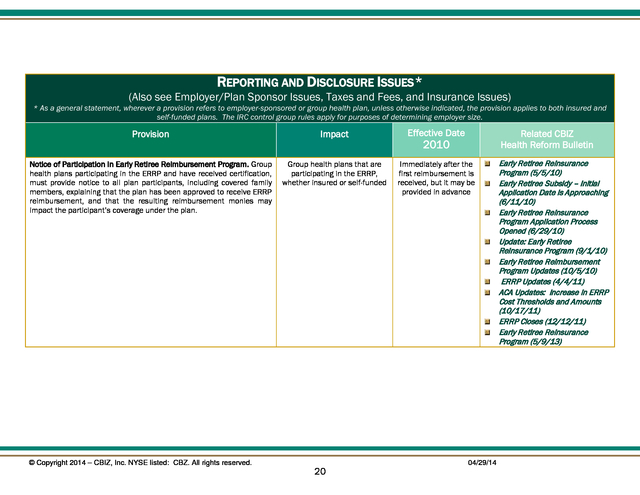

REPORTING AND DISCLOSURE ISSUES* (Also see Employer/Plan Sponsor Issues, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Notice of Participation in Early Retiree Reimbursement Program. Group health plans participating in the ERRP and have received certification, must provide notice to all plan participants, including covered family members, explaining that the plan has been approved to receive ERRP reimbursement, and that the resulting reimbursement monies may impact the participant’s coverage under the plan. Group health plans that are participating in the ERRP, whether insured or self-funded Immediately after the first reimbursement is received, but it may be provided in advance © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

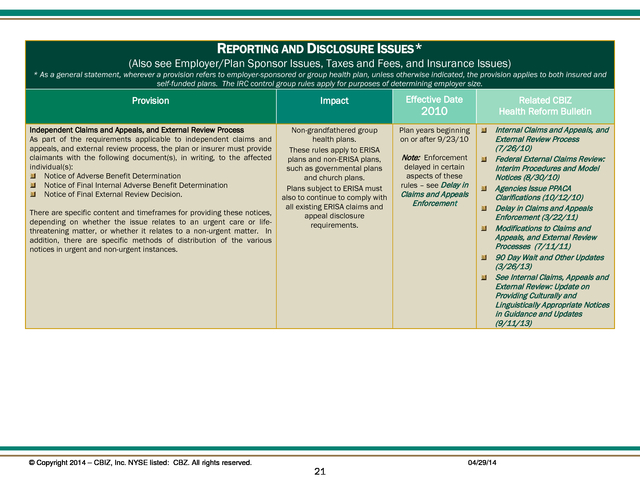

All rights reserved. 20 Related CBIZ Health Reform Bulletin 2010 04/29/14 Early Retiree Reinsurance Program (5/5/10) Early Retiree Subsidy – Initial Application Date is Approaching (6/11/10) Early Retiree Reinsurance Program Application Process Opened (6/29/10) Update: Early Retiree Reinsurance Program (9/1/10) Early Retiree Reimbursement Program Updates (10/5/10) ERRP Updates (4/4/11) ACA Updates: Increase in ERRP Cost Thresholds and Amounts (10/17/11) ERRP Closes (12/12/11) Early Retiree Reinsurance Program (5/9/13) . REPORTING AND DISCLOSURE ISSUES* (Also see Employer/Plan Sponsor Issues, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Independent Claims and Appeals, and External Review Process As part of the requirements applicable to independent claims and appeals, and external review process, the plan or insurer must provide claimants with the following document(s), in writing, to the affected individual(s): Notice of Adverse Benefit Determination Notice of Final Internal Adverse Benefit Determination Notice of Final External Review Decision. Non-grandfathered group health plans. These rules apply to ERISA plans and non-ERISA plans, such as governmental plans and church plans. Plans subject to ERISA must also to continue to comply with all existing ERISA claims and appeal disclosure requirements. Plan years beginning on or after 9/23/10 There are specific content and timeframes for providing these notices, depending on whether the issue relates to an urgent care or lifethreatening matter, or whether it relates to a non-urgent matter. In addition, there are specific methods of distribution of the various notices in urgent and non-urgent instances. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

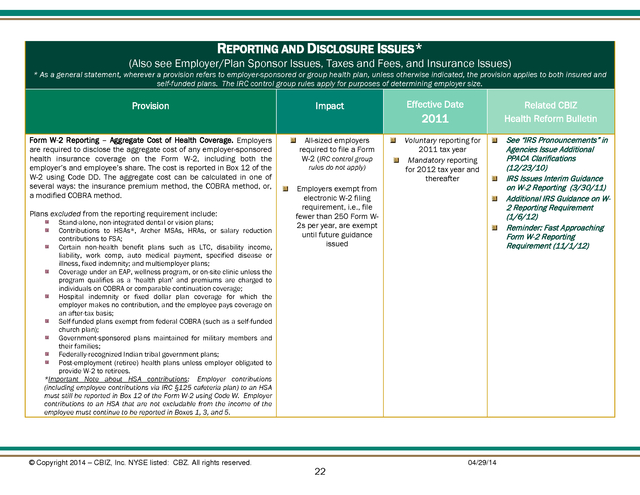

All rights reserved. 21 Related CBIZ Health Reform Bulletin 2010 Note: Enforcement delayed in certain aspects of these rules – see Delay in Claims and Appeals Enforcement Internal Claims and Appeals, and External Review Process (7/26/10) Federal External Claims Review: Interim Procedures and Model Notices (8/30/10) Agencies Issue PPACA Clarifications (10/12/10) Delay in Claims and Appeals Enforcement (3/22/11) Modifications to Claims and Appeals, and External Review Processes (7/11/11) 90 Day Wait and Other Updates (3/26/13) See Internal Claims, Appeals and External Review: Update on Providing Culturally and Linguistically Appropriate Notices in Guidance and Updates (9/11/13) 04/29/14 . REPORTING AND DISCLOSURE ISSUES* (Also see Employer/Plan Sponsor Issues, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Form W-2 Reporting – Aggregate Cost of Health Coverage. Employers are required to disclose the aggregate cost of any employer-sponsored health insurance coverage on the Form W-2, including both the employer’s and employee’s share. The cost is reported in Box 12 of the W-2 using Code DD.

The aggregate cost can be calculated in one of several ways: the insurance premium method, the COBRA method, or, a modified COBRA method. Plans excluded from the reporting requirement include: Stand-alone, non-integrated dental or vision plans; Contributions to HSAs*, Archer MSAs, HRAs, or salary reduction contributions to FSA; Certain non-health benefit plans such as LTC, disability income, liability, work comp, auto medical payment, specified disease or illness, fixed indemnity; and multiemployer plans; Coverage under an EAP, wellness program, or on-site clinic unless the program qualifies as a ‘health plan’ and premiums are charged to individuals on COBRA or comparable continuation coverage; Hospital indemnity or fixed dollar plan coverage for which the employer makes no contribution, and the employee pays coverage on an after-tax basis; Self-funded plans exempt from federal COBRA (such as a self-funded church plan); Government-sponsored plans maintained for military members and their families; Federally-recognized Indian tribal government plans; Post-employment (retiree) health plans unless employer obligated to provide W-2 to retirees. *Important Note about HSA contributions: Employer contributions (including employee contributions via IRC §125 cafeteria plan) to an HSA must still be reported in Box 12 of the Form W-2 using Code W. Employer contributions to an HSA that are not excludable from the income of the employee must continue to be reported in Boxes 1, 3, and 5. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

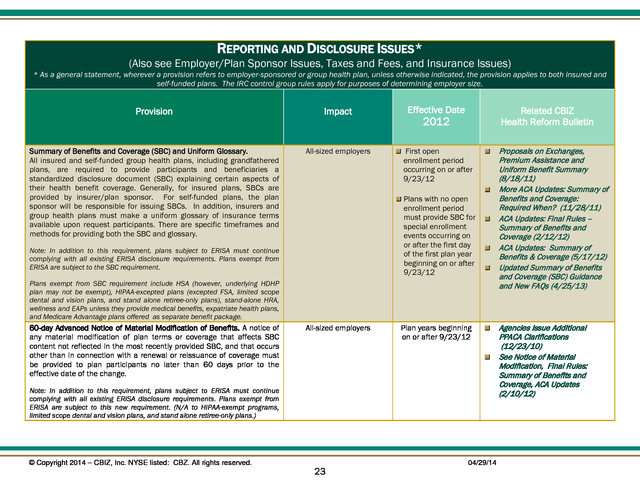

All rights reserved. Impact All-sized employers required to file a Form W-2 (IRC control group rules do not apply) Employers exempt from electronic W-2 filing requirement, i.e., file fewer than 250 Form W2s per year, are exempt until future guidance issued 22 Effective Date Related CBIZ Health Reform Bulletin 2011 Voluntary reporting for 2011 tax year Mandatory reporting for 2012 tax year and thereafter 04/29/14 See “IRS Pronouncements” in Agencies Issue Additional PPACA Clarifications (12/23/10) IRS Issues Interim Guidance on W-2 Reporting (3/30/11) Additional IRS Guidance on W2 Reporting Requirement (1/6/12) Reminder: Fast Approaching Form W-2 Reporting Requirement (11/1/12) . REPORTING AND DISCLOSURE ISSUES* (Also see Employer/Plan Sponsor Issues, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Summary of Benefits and Coverage (SBC) and Uniform Glossary. All insured and self-funded group health plans, including grandfathered plans, are required to provide participants and beneficiaries a standardized disclosure document (SBC) explaining certain aspects of their health benefit coverage. Generally, for insured plans, SBCs are provided by insurer/plan sponsor. For self-funded plans, the plan sponsor will be responsible for issuing SBCs.

In addition, insurers and group health plans must make a uniform glossary of insurance terms available upon request participants. There are specific timeframes and methods for providing both the SBC and glossary. All-sized employers First open enrollment period occurring on or after 9/23/12 Related CBIZ Health Reform Bulletin 2012 Plans with no open enrollment period must provide SBC for special enrollment events occurring on or after the first day of the first plan year beginning on or after 9/23/12 Note: In addition to this requirement, plans subject to ERISA must continue complying with all existing ERISA disclosure requirements. Plans exempt from ERISA are subject to the SBC requirement. Plans exempt from SBC requirement include HSA (however, underlying HDHP plan may not be exempt), HIPAA-excepted plans (excepted FSA, limited scope dental and vision plans, and stand alone retiree-only plans), stand-alone HRA, wellness and EAPs unless they provide medical benefits, expatriate health plans, and Medicare Advantage plans offered as separate benefit package. 60-day Advanced Notice of Material Modification of Benefits.

A notice of any material modification of plan terms or coverage that affects SBC content not reflected in the most recently provided SBC, and that occurs other than in connection with a renewal or reissuance of coverage must be provided to plan participants no later than 60 days prior to the effective date of the change. All-sized employers Plan years beginning on or after 9/23/12 Note: In addition to this requirement, plans subject to ERISA must continue complying with all existing ERISA disclosure requirements. Plans exempt from ERISA are subject to this new requirement. (N/A to HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) © Copyright 2014 – CBIZ, Inc.

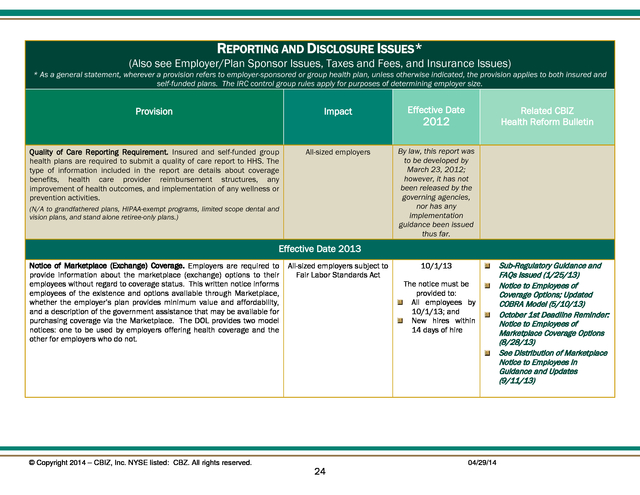

NYSE listed: CBZ. All rights reserved. 23 04/29/14 Proposals on Exchanges, Premium Assistance and Uniform Benefit Summary (8/18/11) More ACA Updates: Summary of Benefits and Coverage: Required When? (11/28/11) ACA Updates: Final Rules – Summary of Benefits and Coverage (2/12/12) ACA Updates: Summary of Benefits & Coverage (5/17/12) Updated Summary of Benefits and Coverage (SBC) Guidance and New FAQs (4/25/13) Agencies Issue Additional PPACA Clarifications (12/23/10) See Notice of Material Modification, Final Rules: Summary of Benefits and Coverage, ACA Updates (2/10/12) . REPORTING AND DISCLOSURE ISSUES* (Also see Employer/Plan Sponsor Issues, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Quality of Care Reporting Requirement. Insured and self-funded group health plans are required to submit a quality of care report to HHS. The type of information included in the report are details about coverage benefits, health care provider reimbursement structures, any improvement of health outcomes, and implementation of any wellness or prevention activities. All-sized employers By law, this report was to be developed by March 23, 2012; however, it has not been released by the governing agencies, nor has any implementation guidance been issued thus far. (N/A to grandfathered plans, HIPAA-exempt programs, limited scope dental and vision plans, and stand alone retiree-only plans.) Related CBIZ Health Reform Bulletin 2012 Effective Date 2013 Notice of Marketplace (Exchange) Coverage.

Employers are required to provide information about the marketplace (exchange) options to their employees without regard to coverage status. This written notice informs employees of the existence and options available through Marketplace, whether the employer’s plan provides minimum value and affordability, and a description of the government assistance that may be available for purchasing coverage via the Marketplace. The DOL provides two model notices: one to be used by employers offering health coverage and the other for employers who do not. © Copyright 2014 – CBIZ, Inc.

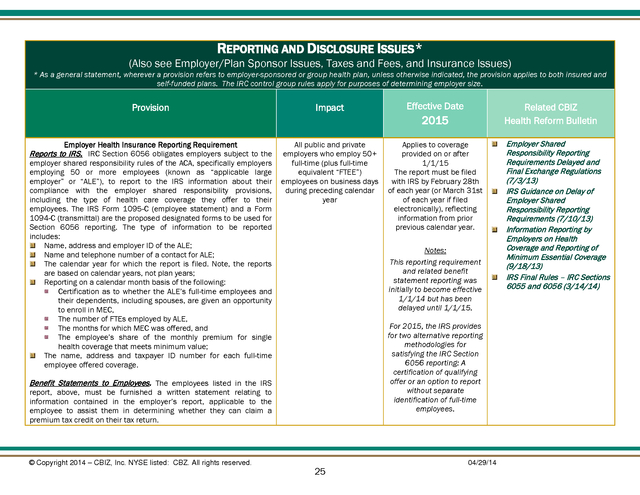

NYSE listed: CBZ. All rights reserved. All-sized employers subject to Fair Labor Standards Act 24 10/1/13 The notice must be provided to: All employees by 10/1/13; and New hires within 14 days of hire 04/29/14 Sub-Regulatory Guidance and FAQs Issued (1/25/13) Notice to Employees of Coverage Options; Updated COBRA Model (5/10/13) October 1st Deadline Reminder: Notice to Employees of Marketplace Coverage Options (8/28/13) See Distribution of Marketplace Notice to Employees in Guidance and Updates (9/11/13) . REPORTING AND DISCLOSURE ISSUES* (Also see Employer/Plan Sponsor Issues, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Employer Health Insurance Reporting Requirement All public and private employers who employ 50+ full-time (plus full-time equivalent “FTEE”) employees on business days during preceding calendar year Applies to coverage provided on or after 1/1/15 The report must be filed with IRS by February 28th of each year (or March 31st of each year if filed electronically), reflecting information from prior previous calendar year. Reports to IRS. IRC Section 6056 obligates employers subject to the employer shared responsibility rules of the ACA, specifically employers employing 50 or more employees (known as “applicable large employer” or “ALE”), to report to the IRS information about their compliance with the employer shared responsibility provisions, including the type of health care coverage they offer to their employees. The IRS Form 1095-C (employee statement) and a Form 1094-C (transmittal) are the proposed designated forms to be used for Section 6056 reporting.

The type of information to be reported includes: Name, address and employer ID of the ALE; Name and telephone number of a contact for ALE; The calendar year for which the report is filed. Note, the reports are based on calendar years, not plan years; Reporting on a calendar month basis of the following: Certification as to whether the ALE’s full-time employees and their dependents, including spouses, are given an opportunity to enroll in MEC, The number of FTEs employed by ALE, The months for which MEC was offered, and The employee’s share of the monthly premium for single health coverage that meets minimum value; The name, address and taxpayer ID number for each full-time employee offered coverage. 2015 Notes: This reporting requirement and related benefit statement reporting was initially to become effective 1/1/14 but has been delayed until 1/1/15. For 2015, the IRS provides for two alternative reporting methodologies for satisfying the IRC Section 6056 reporting: A certification of qualifying offer or an option to report without separate identification of full-time employees. Benefit Statements to Employees. The employees listed in the IRS report, above, must be furnished a written statement relating to information contained in the employer’s report, applicable to the employee to assist them in determining whether they can claim a premium tax credit on their tax return. © Copyright 2014 – CBIZ, Inc.

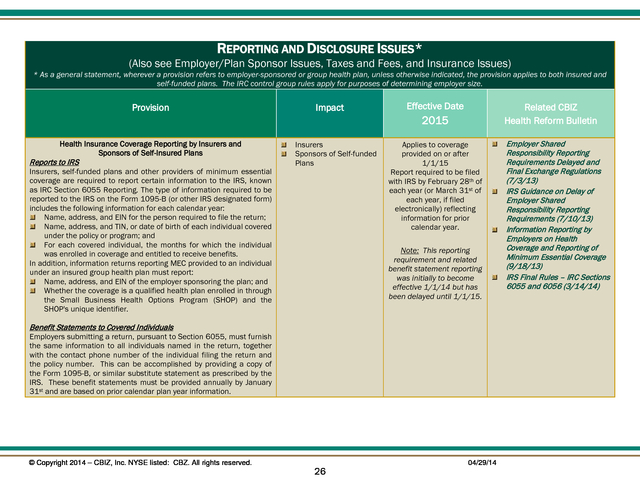

NYSE listed: CBZ. All rights reserved. Related CBIZ Health Reform Bulletin 25 04/29/14 Employer Shared Responsibility Reporting Requirements Delayed and Final Exchange Regulations (7/3/13) IRS Guidance on Delay of Employer Shared Responsibility Reporting Requirements (7/10/13) Information Reporting by Employers on Health Coverage and Reporting of Minimum Essential Coverage (9/18/13) IRS Final Rules – IRC Sections 6055 and 6056 (3/14/14) . REPORTING AND DISCLOSURE ISSUES* (Also see Employer/Plan Sponsor Issues, Taxes and Fees, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Health Insurance Coverage Reporting by Insurers and Sponsors of Self-Insured Plans Reports to IRS Insurers, self-funded plans and other providers of minimum essential coverage are required to report certain information to the IRS, known as IRC Section 6055 Reporting. The type of information required to be reported to the IRS on the Form 1095-B (or other IRS designated form) includes the following information for each calendar year: Name, address, and EIN for the person required to file the return; Name, address, and TIN, or date of birth of each individual covered under the policy or program; and For each covered individual, the months for which the individual was enrolled in coverage and entitled to receive benefits. In addition, information returns reporting MEC provided to an individual under an insured group health plan must report: Name, address, and EIN of the employer sponsoring the plan; and Whether the coverage is a qualified health plan enrolled in through the Small Business Health Options Program (SHOP) and the SHOP's unique identifier. Impact Insurers Sponsors of Self-funded Plans Effective Date Related CBIZ Health Reform Bulletin 2015 Applies to coverage provided on or after 1/1/15 Report required to be filed with IRS by February 28th of each year (or March 31st of each year, if filed electronically) reflecting information for prior calendar year. Note: This reporting requirement and related benefit statement reporting was initially to become effective 1/1/14 but has been delayed until 1/1/15. Benefit Statements to Covered Individuals Employers submitting a return, pursuant to Section 6055, must furnish the same information to all individuals named in the return, together with the contact phone number of the individual filing the return and the policy number. This can be accomplished by providing a copy of the Form 1095-B, or similar substitute statement as prescribed by the IRS.

These benefit statements must be provided annually by January 31st and are based on prior calendar plan year information. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 26 04/29/14 Employer Shared Responsibility Reporting Requirements Delayed and Final Exchange Regulations (7/3/13) IRS Guidance on Delay of Employer Shared Responsibility Reporting Requirements (7/10/13) Information Reporting by Employers on Health Coverage and Reporting of Minimum Essential Coverage (9/18/13) IRS Final Rules – IRC Sections 6055 and 6056 (3/14/14) .

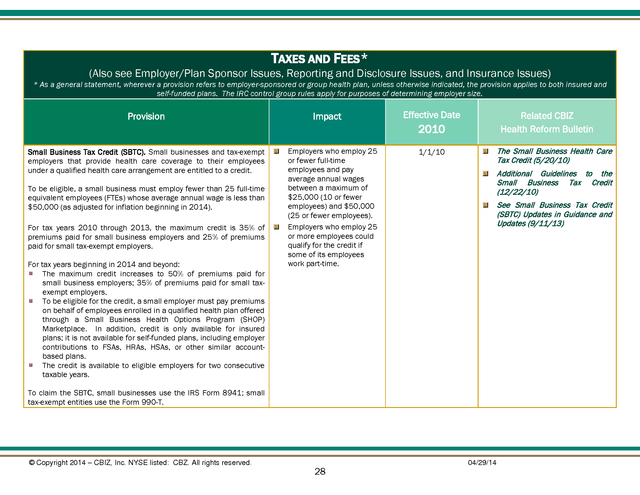

TAXES AND FEES ALSO SEE EMPLOYER/PLAN SPONSOR ISSUES, REPORTING AND DISCLOSURE ISSUES & INSURANCE ISSUES © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 27 04/29/14 . TAXES AND FEES* (Also see Employer/Plan Sponsor Issues, Reporting and Disclosure Issues, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Small Business Tax Credit (SBTC). Small businesses and tax-exempt employers that provide health care coverage to their employees under a qualified health care arrangement are entitled to a credit. To be eligible, a small business must employ fewer than 25 full-time equivalent employees (FTEs) whose average annual wage is less than $50,000 (as adjusted for inflation beginning in 2014). For tax years 2010 through 2013, the maximum credit is 35% of premiums paid for small business employers and 25% of premiums paid for small tax-exempt employers. For tax years beginning in 2014 and beyond: The maximum credit increases to 50% of premiums paid for small business employers; 35% of premiums paid for small taxexempt employers. To be eligible for the credit, a small employer must pay premiums on behalf of employees enrolled in a qualified health plan offered through a Small Business Health Options Program (SHOP) Marketplace. In addition, credit is only available for insured plans; it is not available for self-funded plans, including employer contributions to FSAs, HRAs, HSAs, or other similar accountbased plans. The credit is available to eligible employers for two consecutive taxable years. Impact Employers who employ 25 or fewer full-time employees and pay average annual wages between a maximum of $25,000 (10 or fewer employees) and $50,000 (25 or fewer employees). Employers who employ 25 or more employees could qualify for the credit if some of its employees work part-time. Effective Date Related CBIZ Health Reform Bulletin 2010 The Small Business Health Care Tax Credit (5/20/10) 1/1/10 Additional Guidelines to the Small Business Tax Credit (12/22/10) See Small Business Tax Credit (SBTC) Updates in Guidance and Updates (9/11/13) To claim the SBTC, small businesses use the IRS Form 8941; small tax-exempt entities use the Form 990-T. © Copyright 2014 – CBIZ, Inc.

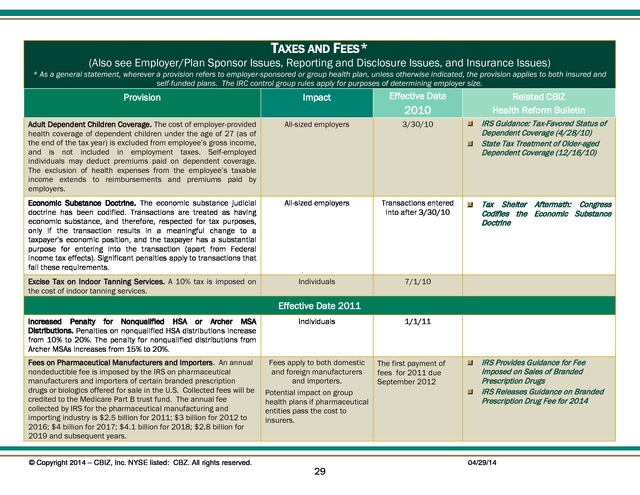

NYSE listed: CBZ. All rights reserved. 28 04/29/14 . TAXES AND FEES* (Also see Employer/Plan Sponsor Issues, Reporting and Disclosure Issues, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date Adult Dependent Children Coverage. The cost of employer-provided health coverage of dependent children under the age of 27 (as of the end of the tax year) is excluded from employee’s gross income, and is not included in employment taxes. Self-employed individuals may deduct premiums paid on dependent coverage. The exclusion of health expenses from the employee’s taxable income extends to reimbursements and premiums paid by employers. All-sized employers 3/30/10 Economic Substance Doctrine.

The economic substance judicial doctrine has been codified. Transactions are treated as having economic substance, and therefore, respected for tax purposes, only if the transaction results in a meaningful change to a taxpayer’s economic position, and the taxpayer has a substantial purpose for entering into the transaction (apart from Federal income tax effects). Significant penalties apply to transactions that fail these requirements. All-sized employers Transactions entered into after 3/30/10 Excise Tax on Indoor Tanning Services.

A 10% tax is imposed on the cost of indoor tanning services. Individuals 7/1/10 2010 Related CBIZ Health Reform Bulletin IRS Guidance: Tax-Favored Status of Dependent Coverage (4/28/10) State Tax Treatment of Older-aged Dependent Coverage (12/16/10) Tax Shelter Aftermath: Congress Codifies the Economic Substance Doctrine Effective Date 2011 Increased Penalty for Nonqualified HSA or Archer MSA Distributions. Penalties on nonqualified HSA distributions increase from 10% to 20%. The penalty for nonqualified distributions from Archer MSAs increases from 15% to 20%. Individuals Fees on Pharmaceutical Manufacturers and Importers.

An annual nondeductible fee is imposed by the IRS on pharmaceutical manufacturers and importers of certain branded prescription drugs or biologics offered for sale in the U.S. Collected fees will be credited to the Medicare Part B trust fund. The annual fee collected by IRS for the pharmaceutical manufacturing and importing industry is $2.5 billion for 2011; $3 billion for 2012 to 2016; $4 billion for 2017; $4.1 billion for 2018; $2.8 billion for 2019 and subsequent years. Fees apply to both domestic and foreign manufacturers and importers. Potential impact on group health plans if pharmaceutical entities pass the cost to insurers. © Copyright 2014 – CBIZ, Inc.

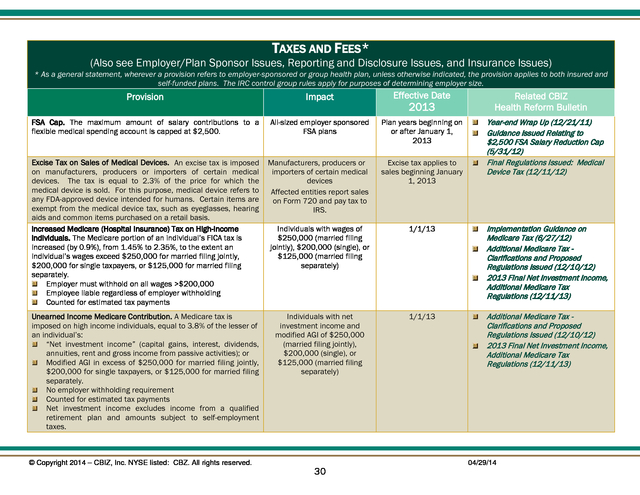

NYSE listed: CBZ. All rights reserved. 29 1/1/11 The first payment of fees for 2011 due September 2012 IRS Provides Guidance for Fee Imposed on Sales of Branded Prescription Drugs IRS Releases Guidance on Branded Prescription Drug Fee for 2014 04/29/14 . TAXES AND FEES* (Also see Employer/Plan Sponsor Issues, Reporting and Disclosure Issues, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size. Provision Impact Effective Date FSA Cap. The maximum amount of salary contributions to a flexible medical spending account is capped at $2,500. All-sized employer sponsored FSA plans Plan years beginning on or after January 1, 2013 Excise Tax on Sales of Medical Devices. An excise tax is imposed on manufacturers, producers or importers of certain medical devices.

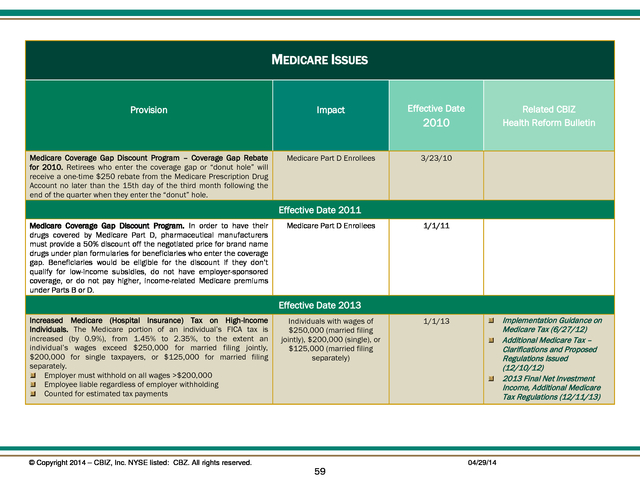

The tax is equal to 2.3% of the price for which the medical device is sold. For this purpose, medical device refers to any FDA-approved device intended for humans. Certain items are exempt from the medical device tax, such as eyeglasses, hearing aids and common items purchased on a retail basis. Increased Medicare (Hospital Insurance) Tax on High-Income Individuals.

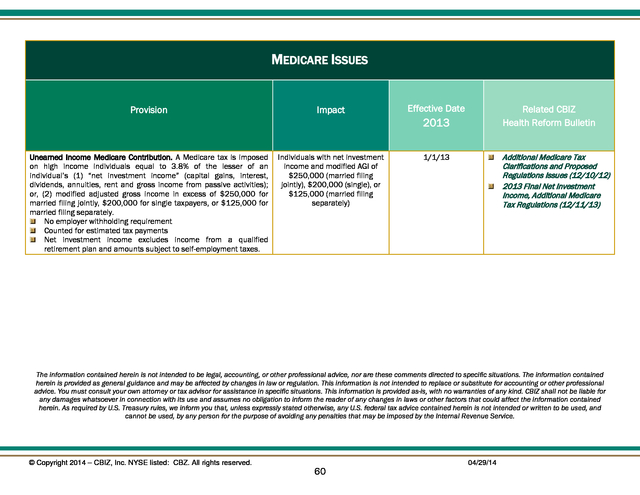

The Medicare portion of an individual’s FICA tax is increased (by 0.9%), from 1.45% to 2.35%, to the extent an individual’s wages exceed $250,000 for married filing jointly, $200,000 for single taxpayers, or $125,000 for married filing separately. Employer must withhold on all wages >$200,000 Employee liable regardless of employer withholding Counted for estimated tax payments Manufacturers, producers or importers of certain medical devices Affected entities report sales on Form 720 and pay tax to IRS. Excise tax applies to sales beginning January 1, 2013 Individuals with wages of $250,000 (married filing jointly), $200,000 (single), or $125,000 (married filing separately) 1/1/13 Implementation Guidance on Medicare Tax (6/27/12) Additional Medicare Tax Clarifications and Proposed Regulations Issued (12/10/12) 2013 Final Net Investment Income, Additional Medicare Tax Regulations (12/11/13) Unearned Income Medicare Contribution. A Medicare tax is imposed on high income individuals, equal to 3.8% of the lesser of an individual’s: “Net investment income” (capital gains, interest, dividends, annuities, rent and gross income from passive activities); or Modified AGI in excess of $250,000 for married filing jointly, $200,000 for single taxpayers, or $125,000 for married filing separately. No employer withholding requirement Counted for estimated tax payments Net investment income excludes income from a qualified retirement plan and amounts subject to self-employment taxes. Individuals with net investment income and modified AGI of $250,000 (married filing jointly), $200,000 (single), or $125,000 (married filing separately) 1/1/13 Additional Medicare Tax Clarifications and Proposed Regulations Issued (12/10/12) 2013 Final Net Investment Income, Additional Medicare Tax Regulations (12/11/13) © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.

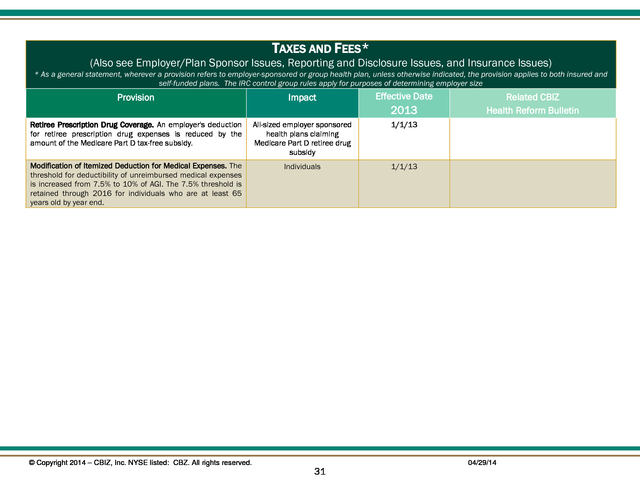

All rights reserved. 30 2013 Related CBIZ Health Reform Bulletin Year-end Wrap Up (12/21/11) Guidance Issued Relating to $2,500 FSA Salary Reduction Cap (5/31/12) Final Regulations Issued: Medical Device Tax (12/11/12) 04/29/14 . TAXES AND FEES* (Also see Employer/Plan Sponsor Issues, Reporting and Disclosure Issues, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size Provision Impact Effective Date Retiree Prescription Drug Coverage. An employer's deduction for retiree prescription drug expenses is reduced by the amount of the Medicare Part D tax-free subsidy. All-sized employer sponsored health plans claiming Medicare Part D retiree drug subsidy 1/1/13 Modification of Itemized Deduction for Medical Expenses. The threshold for deductibility of unreimbursed medical expenses is increased from 7.5% to 10% of AGI.

The 7.5% threshold is retained through 2016 for individuals who are at least 65 years old by year end. Individuals 1/1/13 2013 Related CBIZ Health Reform Bulletin Effective Date 2011 © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 31 04/29/14 .

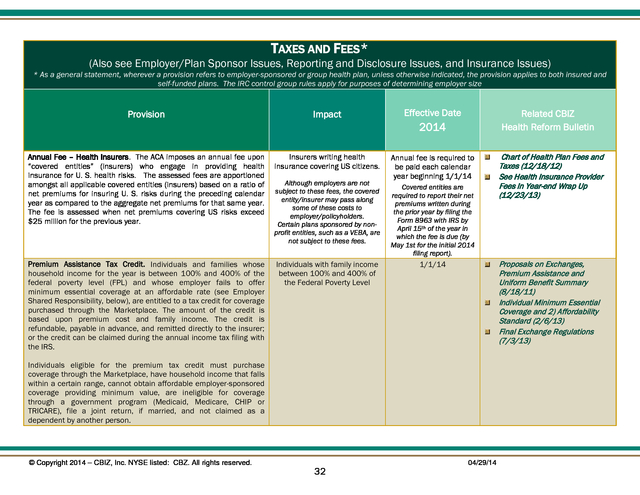

TAXES AND FEES* (Also see Employer/Plan Sponsor Issues, Reporting and Disclosure Issues, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size Provision Impact Effective Date Annual Fee – Health Insurers. The ACA imposes an annual fee upon “covered entities” (insurers) who engage in providing health insurance for U. S.

health risks. The assessed fees are apportioned amongst all applicable covered entities (insurers) based on a ratio of net premiums for insuring U. S.

risks during the preceding calendar year as compared to the aggregate net premiums for that same year. The fee is assessed when net premiums covering US risks exceed $25 million for the previous year. Insurers writing health insurance covering US citizens. Annual fee is required to be paid each calendar year beginning 1/1/14 Premium Assistance Tax Credit. Individuals and families whose household income for the year is between 100% and 400% of the federal poverty level (FPL) and whose employer fails to offer minimum essential coverage at an affordable rate (see Employer Shared Responsibility, below), are entitled to a tax credit for coverage purchased through the Marketplace. The amount of the credit is based upon premium cost and family income.

The credit is refundable, payable in advance, and remitted directly to the insurer; or the credit can be claimed during the annual income tax filing with the IRS. Although employers are not subject to these fees, the covered entity/insurer may pass along some of these costs to employer/policyholders. Certain plans sponsored by nonprofit entities, such as a VEBA, are not subject to these fees. Individuals with family income between 100% and 400% of the Federal Poverty Level Related CBIZ Health Reform Bulletin 2014 Covered entities are required to report their net premiums written during the prior year by filing the Form 8963 with IRS by April 15th of the year in which the fee is due (by May 1st for the initial 2014 filing report). Proposals on Exchanges, Premium Assistance and Uniform Benefit Summary (8/18/11) Individual Minimum Essential Coverage and 2) Affordability Standard (2/6/13) Final Exchange Regulations (7/3/13) 1/1/14 Individuals eligible for the premium tax credit must purchase coverage through the Marketplace, have household income that falls within a certain range, cannot obtain affordable employer-sponsored coverage providing minimum value, are ineligible for coverage through a government program (Medicaid, Medicare, CHIP or TRICARE), file a joint return, if married, and not claimed as a dependent by another person. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 32 Chart of Health Plan Fees and Taxes (12/18/12) See Health Insurance Provider Fees in Year-end Wrap Up (12/23/13) 04/29/14 .

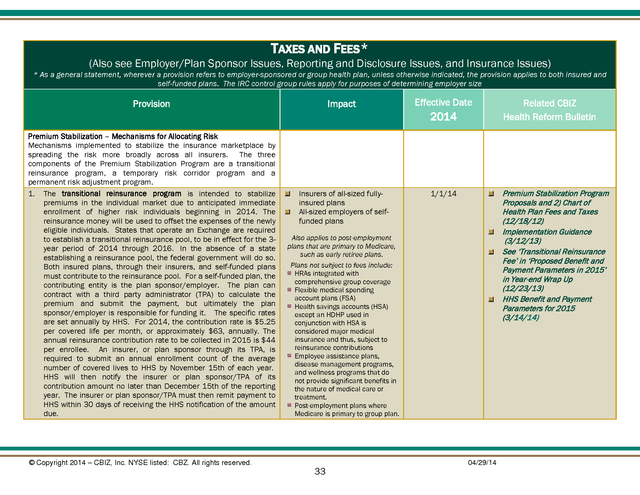

TAXES AND FEES* (Also see Employer/Plan Sponsor Issues, Reporting and Disclosure Issues, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size Impact Effective Date Insurers of all-sized fullyinsured plans All-sized employers of selffunded plans 1/1/14 Provision Premium Stabilization – Mechanisms for Allocating Risk Mechanisms implemented to stabilize the insurance marketplace by spreading the risk more broadly across all insurers. The three components of the Premium Stabilization Program are a transitional reinsurance program, a temporary risk corridor program and a permanent risk adjustment program. 1. The transitional reinsurance program is intended to stabilize premiums in the individual market due to anticipated immediate enrollment of higher risk individuals beginning in 2014.

The reinsurance money will be used to offset the expenses of the newly eligible individuals. States that operate an Exchange are required to establish a transitional reinsurance pool, to be in effect for the 3year period of 2014 through 2016. In the absence of a state establishing a reinsurance pool, the federal government will do so. Both insured plans, through their insurers, and self-funded plans must contribute to the reinsurance pool.

For a self-funded plan, the contributing entity is the plan sponsor/employer. The plan can contract with a third party administrator (TPA) to calculate the premium and submit the payment, but ultimately the plan sponsor/employer is responsible for funding it. The specific rates are set annually by HHS.

For 2014, the contribution rate is $5.25 per covered life per month, or approximately $63, annually. The annual reinsurance contribution rate to be collected in 2015 is $44 per enrollee. An insurer, or plan sponsor through its TPA, is required to submit an annual enrollment count of the average number of covered lives to HHS by November 15th of each year. HHS will then notify the insurer or plan sponsor/TPA of its contribution amount no later than December 15th of the reporting year.

The insurer or plan sponsor/TPA must then remit payment to HHS within 30 days of receiving the HHS notification of the amount due. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ. All rights reserved. 2014 Premium Stabilization Program Proposals and 2) Chart of Health Plan Fees and Taxes (12/18/12) Implementation Guidance (3/12/13) See ‘Transitional Reinsurance Fee’ in ‘Proposed Benefit and Payment Parameters in 2015’ in Year-end Wrap Up (12/23/13) HHS Benefit and Payment Parameters for 2015 (3/14/14) Also applies to post-employment plans that are primary to Medicare, such as early retiree plans. Plans not subject to fees include: HRAs integrated with comprehensive group coverage Flexible medical spending account plans (FSA) Health savings accounts (HSA) except an HDHP used in conjunction with HSA is considered major medical insurance and thus, subject to reinsurance contributions Employee assistance plans, disease management programs, and wellness programs that do not provide significant benefits in the nature of medical care or treatment. Post-employment plans where Medicare is primary to group plan. 33 Related CBIZ Health Reform Bulletin 04/29/14 .

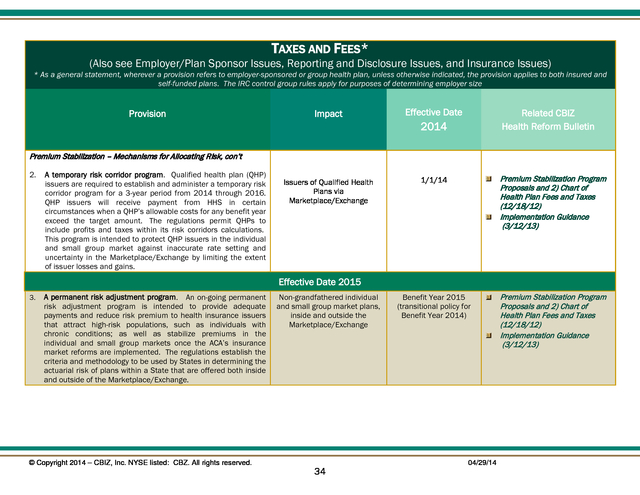

TAXES AND FEES* (Also see Employer/Plan Sponsor Issues, Reporting and Disclosure Issues, and Insurance Issues) * As a general statement, wherever a provision refers to employer-sponsored or group health plan, unless otherwise indicated, the provision applies to both insured and self-funded plans. The IRC control group rules apply for purposes of determining employer size Provision Impact Effective Date Issuers of Qualified Health Plans via Marketplace/Exchange 1/1/14 Premium Stabilization Program Proposals and 2) Chart of Health Plan Fees and Taxes (12/18/12) Implementation Guidance (3/12/13) Benefit Year 2015 (transitional policy for Benefit Year 2014) Premium Stabilization Program Proposals and 2) Chart of Health Plan Fees and Taxes (12/18/12) Implementation Guidance (3/12/13) Related CBIZ Health Reform Bulletin 2014 Premium Stabilization – Mechanisms for Allocating Risk, con’t 2. A temporary risk corridor program. Qualified health plan (QHP) issuers are required to establish and administer a temporary risk corridor program for a 3-year period from 2014 through 2016. QHP issuers will receive payment from HHS in certain circumstances when a QHP’s allowable costs for any benefit year exceed the target amount. The regulations permit QHPs to include profits and taxes within its risk corridors calculations. This program is intended to protect QHP issuers in the individual and small group market against inaccurate rate setting and uncertainty in the Marketplace/Exchange by limiting the extent of issuer losses and gains. Effective Date 2015 3. A permanent risk adjustment program.

An on-going permanent risk adjustment program is intended to provide adequate payments and reduce risk premium to health insurance issuers that attract high-risk populations, such as individuals with chronic conditions; as well as stabilize premiums in the individual and small group markets once the ACA’s insurance market reforms are implemented. The regulations establish the criteria and methodology to be used by States in determining the actuarial risk of plans within a State that are offered both inside and outside of the Marketplace/Exchange. © Copyright 2014 – CBIZ, Inc. NYSE listed: CBZ.