Growth & Employment Trends in the Technology & Life Sciences Sector

CBIZ & Mayer Hoffman McCann PC

Description

SECOND EDITION

CBIZ & MAYER HOFFMAN McCANN P.C.

Growth & Employment Trends

in the Technology &

Life Sciences Sector

. Table of Contents

3

|

EXECUTIVE SUMMARY

4

|

PART 1: THE EXPANSION LANDSCAPE

8

|

PART 2: WORKFORCE SNAPSHOT

1 2

|

PART 3: OPPORTUNITIES AHEAD

1 6

|

ABOUT CBIZ & MHM

1 6

|

SURVEY METHODOLOGY

. CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT

.C.

Executive Summary

To grow operations, companies typically need two things, money and people. The challenging piece of the expansion puzzle for companies in the

technology and life sciences sector is not money—companies are not having trouble finding funding sources—rather, it’s recruiting and retaining talent.

CBIZ and Mayer Hoffman McCann P.C. (MHM), along with CBIZ’s retained executive search group, EFL Associates, sought to dive deeper into the

industry’s balance between opportunities and obstacles. We put together our second annual Growth & Employment Trends in Technology & Life

Sciences Sector report to explore these issues in more detail.

Our evaluation included several factors, such as economic conditions, federal policies and broader industry trends as well as the insights those in the industry shared with us. We compiled our findings into this report in order to provide best practices companies can use moving forward. Our analysis revealed similar patterns for 2015 as noted in the previous year. Companies plan to both physically expand and hire, but many noted the economy and finding and retaining the right personnel limits their growth.

The following number among our other key findings: Expansion is a priority. 61% of respondents named growth as the end goal for their company, and 96% say they have plans to physically expand in the next 24 months. Companies are investing in technology to address challenges. 93% of respondents plan to invest in technology in the next 24 months, and 29% see technological advances providing their greatest source of opportunity. A balance is needed between support and scrutiny. 61% say governmental regulations present an impediment to their operations, while 50% of respondents say tax incentives and benefits would have the greatest positive impact on their company. Leadership presents an obstacle to company development. 67% of respondents cite leadership as an obstacle to growth, and 87% say their company’s incomplete leadership succession plan has an impact on their workforce. Healthcare expenses trigger growth limitations.

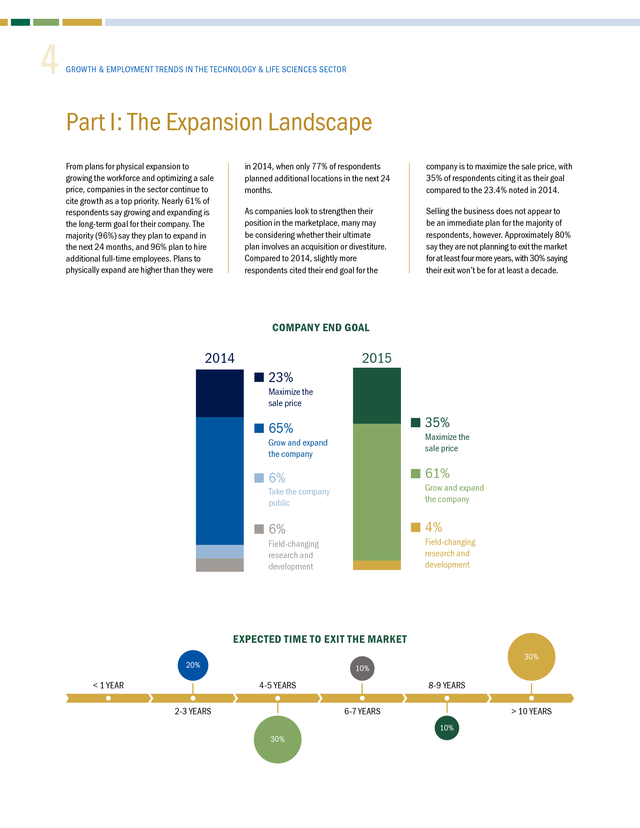

More than 86% of respondents say the cost of employee benefits and healthcare inhibits their growth, while more than 28% say labor costs are affecting their hiring plans. Changes in higher education could make a difference. More than 26% of companies seek a broader talent pool, and 88% say that education courses more aligned with the needs of the industry would address their challenges. 3 . 4 GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR Part I: The Expansion Landscape in 2014, when only 77% of respondents planned additional locations in the next 24 months. company is to maximize the sale price, with 35% of respondents citing it as their goal compared to the 23.4% noted in 2014. As companies look to strengthen their position in the marketplace, many may be considering whether their ultimate plan involves an acquisition or divestiture. Compared to 2014, slightly more respondents cited their end goal for the From plans for physical expansion to growing the workforce and optimizing a sale price, companies in the sector continue to cite growth as a top priority. Nearly 61% of respondents say growing and expanding is the long-term goal for their company. The majority (96%) say they plan to expand in the next 24 months, and 96% plan to hire additional full-time employees. Plans to physically expand are higher than they were Selling the business does not appear to be an immediate plan for the majority of respondents, however.

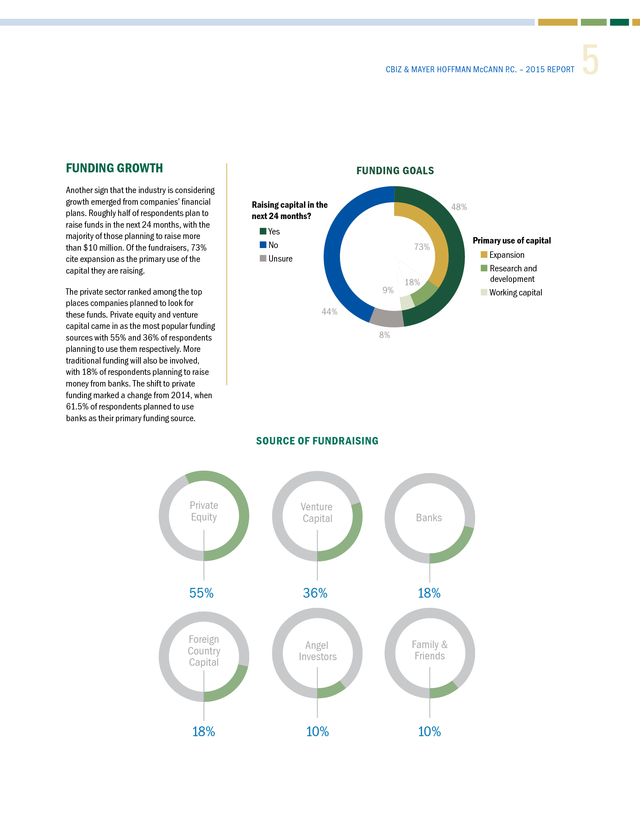

Approximately 80% say they are not planning to exit the market for at least four more years, with 30% saying their exit won’t be for at least a decade. COMPANY END GOAL 2014 2015 23% Maximize the sale price 35% 65% Maximize the sale price Grow and expand the company 6% 61% Take the company public Grow and expand the company 6% 4% Field-changing research and development Field-changing research and development EXPECTED TIME TO EXIT THE MARKET 20% < 1 YEAR 10% 4-5 YEARS 2-3 YEARS 59% 8-9 YEARS 6-7 YEARS > 10 YEARS 10% 30% 30% . CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. FUNDING GROWTH FUNDING GOALS Another sign that the industry is considering growth emerged from companies’ financial plans. Roughly half of respondents plan to raise funds in the next 24 months, with the majority of those planning to raise more than $10 million. Of the fundraisers, 73% cite expansion as the primary use of the capital they are raising. The private sector ranked among the top places companies planned to look for these funds. Private equity and venture capital came in as the most popular funding sources with 55% and 36% of respondents planning to use them respectively.

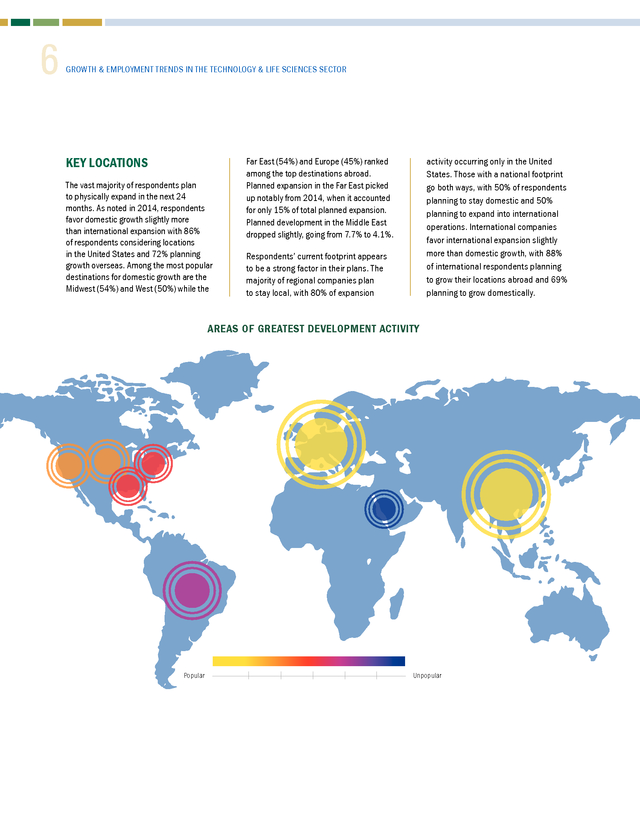

More traditional funding will also be involved, with 18% of respondents planning to raise money from banks. The shift to private funding marked a change from 2014, when 61.5% of respondents planned to use banks as their primary funding source. Raising capital in the next 24 months? 48% â– Yes â– No â– Unsure 73% 9% 18% 44% 8% SOURCE OF FUNDRAISING Private Equity Venture Capital Banks 55% 36% 18% Foreign Country Capital Angel Investors Family & Friends 18% 10% 10% Primary use of capital â– Expansion â– Research and development â– Working capital 5 . GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR KEY LOCATIONS The vast majority of respondents plan to physically expand in the next 24 months. As noted in 2014, respondents favor domestic growth slightly more than international expansion with 86% of respondents considering locations in the United States and 72% planning growth overseas. Among the most popular destinations for domestic growth are the Midwest (54%) and West (50%) while the Far East (54%) and Europe (45%) ranked among the top destinations abroad. Planned expansion in the Far East picked up notably from 2014, when it accounted for only 15% of total planned expansion. Planned development in the Middle East dropped slightly, going from 7.7% to 4.1%. Respondents’ current footprint appears to be a strong factor in their plans. The majority of regional companies plan to stay local, with 80% of expansion activity occurring only in the United States.

Those with a national footprint go both ways, with 50% of respondents planning to stay domestic and 50% planning to expand into international operations. International companies favor international expansion slightly more than domestic growth, with 88% of international respondents planning to grow their locations abroad and 69% planning to grow domestically. AREAS OF GREATEST DEVELOPMENT ACTIVITY —— —— —— —————————————————————————————————————————————————— Unpopular —— Popular —— 6 . CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. ECONOMIC WOES The economy could be one of the major reasons why technology and life sciences companies are not undertaking broader expansion plans. When asked to evaluate the factors affecting company growth, economic conditions came in first with 83% of respondents citing it as having an impact on their company. Governmental regulations also appear to be a factor affecting growth, with 61% naming them as a top concern. Respondents say two governmental regulatory areas in particular present obstacles, the Food and Drug Administration(FDA)’s regulatory pathway and federal guidelines for research and development activities. Access to funding is not a large issue for companies in the sector.

Approximately 61% of respondents say insufficient capital does not affect their growth plans, and half say cash flow limitations are a low concern. Other areas that have a small effect on the sector’s growth include public market pathways and quality control. This represents a change from 2014, where quality control ranked as companies’ top factor affecting expansion. Level of Concern FACTORS AFFECTING COMPANY GROWTH Insufficient capital Access to public markets Quality control â– Major factor Intellectual property concerns Inadequate product demand â– Significant factor Production Governmental inefficiencies regulations â– Factor â– Minor factor Cash flow limitations Economic Cost of conditions research and development â– Not a major factor 7 .

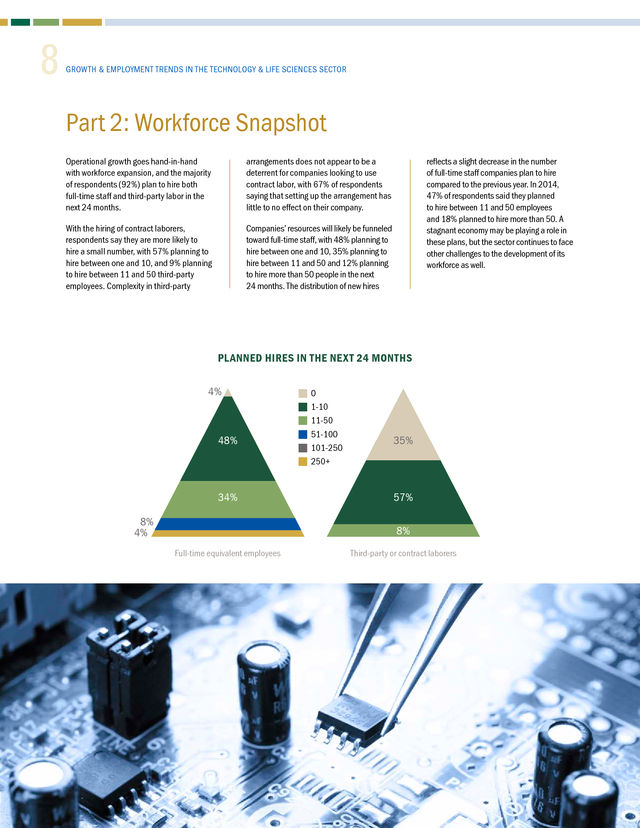

8 GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR Part 2: Workforce Snapshot Operational growth goes hand-in-hand with workforce expansion, and the majority of respondents (92%) plan to hire both full-time staff and third-party labor in the next 24 months. With the hiring of contract laborers, respondents say they are more likely to hire a small number, with 57% planning to hire between one and 10, and 9% planning to hire between 11 and 50 third-party employees. Complexity in third-party reflects a slight decrease in the number of full-time staff companies plan to hire compared to the previous year. In 2014, 47% of respondents said they planned to hire between 11 and 50 employees and 18% planned to hire more than 50. A stagnant economy may be playing a role in these plans, but the sector continues to face other challenges to the development of its workforce as well. arrangements does not appear to be a deterrent for companies looking to use contract labor, with 67% of respondents saying that setting up the arrangement has little to no effect on their company. Companies’ resources will likely be funneled toward full-time staff, with 48% planning to hire between one and 10, 35% planning to hire between 11 and 50 and 12% planning to hire more than 50 people in the next 24 months.

The distribution of new hires PLANNED HIRES IN THE NEXT 24 MONTHS 4% 48% 34% 8% 4% ï® ï® ï® ï® ï® ï® 0 1-10 11-50 51-100 101-250 250+ 35% 57% 8% Full-time equivalent employees Third-party or contract laborers . CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. THE ACA AND THE HIRING PROCESS The Affordable Care Act (ACA) could be playing a role in the hiring process. Of the companies not planning to hire additional staff, almost 29% say it’s because of concern over how the ACA may affect their bottom line. The concern carries over to those companies planning to grow their workforce as well. More than 86% say the cost of employee benefits and healthcare has a major impact on their plans for staffing levels. Of particular concern is the effect consolidation of insurance carriers will have on health insurance premiums, which respondents ranked as their number one ACA issue. Third-party and contract laborers are not subject to the mandate that requires employers to provide their staff with adequate and affordable coverage, but companies do not appear to be favoring the use of third-party over full-time employees.

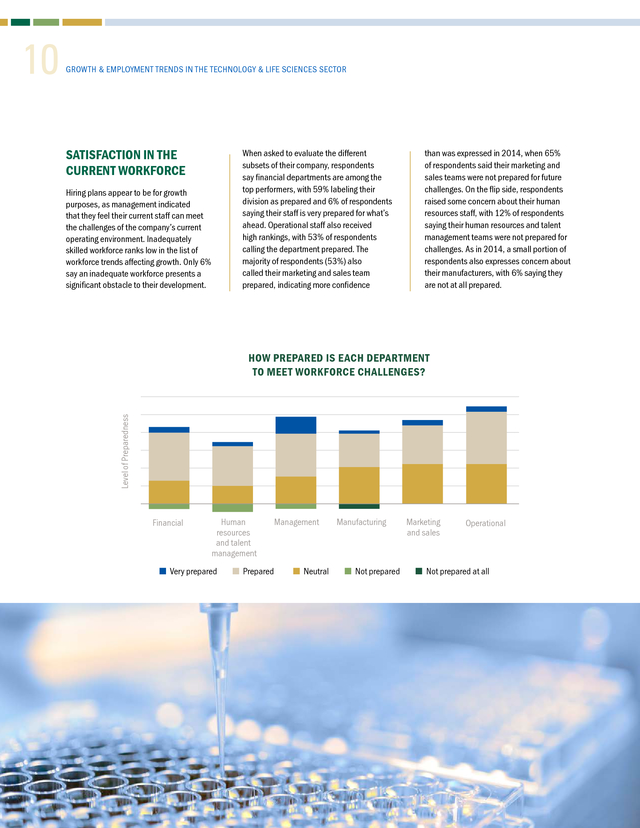

Nearly 35% of companies do not plan to hire additional third-party laborers. Of those that do plan to grow staff, the majority (57%) intend to add between one and 10 contract positions. WHY ARE YOU NOT PLANNING TO HIRE? Affordable Care Act concerns 29% HOW DOES THE COST OF EMPLOYEE BENEFITS AND HEALTHCARE AFFECT YOUR COMPANY? Cost of labor too great 29% 54% 7% 7% 32% â– â– â– â– Significant factor Factor Minor factor Not a major factor of respondents say the cost of employee benefits and healthcare plays a significant factor in their workforce planning. 9 . GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR SATISFACTION IN THE CURRENT WORKFORCE When asked to evaluate the different subsets of their company, respondents say financial departments are among the top performers, with 59% labeling their division as prepared and 6% of respondents saying their staff is very prepared for what’s ahead. Operational staff also received high rankings, with 53% of respondents calling the department prepared. The majority of respondents (53%) also called their marketing and sales team prepared, indicating more confidence Hiring plans appear to be for growth purposes, as management indicated that they feel their current staff can meet the challenges of the company’s current operating environment. Inadequately skilled workforce ranks low in the list of workforce trends affecting growth.

Only 6% say an inadequate workforce presents a significant obstacle to their development. than was expressed in 2014, when 65% of respondents said their marketing and sales teams were not prepared for future challenges. On the flip side, respondents raised some concern about their human resources staff, with 12% of respondents saying their human resources and talent management teams were not prepared for challenges. As in 2014, a small portion of respondents also expresses concern about their manufacturers, with 6% saying they are not at all prepared. HOW PREPARED IS EACH DEPARTMENT TO MEET WORKFORCE CHALLENGES? Level of Preparedness 10 Financial Human resources and talent management â– Very prepared â– Prepared Management â– Neutral Manufacturing â– Not prepared Marketing and sales Operational â– Not prepared at all .

CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. THE RETENTION ISSUE are limited career mobility options for younger staff. With competition in the marketplace, talented young employees may be increasingly deciding whether to take their talents elsewhere. Keeping employees who are well-prepared for the industry is another concern. The workforce trends most impacting companies include employee retention and increased competition for talent, each with more than 86% of respondents saying they have a large effect on their company. Part of the problem may be the limited room for internal growth and development of employees. Nearly three-quarters of respondents say there There may not be an immediate fix to the limited mobility option, either; less than 30% of companies say baby boomers’ exit from the business is creating an issue, which could be indicative that the industry has a younger-than-average workforce.

At the same time, younger employees may have future opportunities in leadership positions. More than 70% of respondents say they do not have a clear successor to run the business. Though the number of companies without an identified successor may be high, naming a successor has not historically been a key concern; in 2014, only 5.9% of companies said that no clear successor to run the business was a top challenge to their organization.

This may shift in the future. Level of Impact IMPACT OF WORKFORCE TRENDS Baby boomers’ exit from the workforce Complexity in third-party and contract labor arrangements ï® Major factor Compliance with federal regulations Cost of employee benefits and healthcare ï® Significant factor Employee retention ï® Factor Increased competition for talent ï® Minor factor Limited career mobility options for younger employees No clear successor to run the business ï® Not a major factor Security of employee personally identifiable information 11 . 12 GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR Part 3: Opportunities Ahead To combat the challenges with recruitment and retention, companies plan to make investments in their current strategies. Forty percent of respondents say they plan to invest in better employee retention strategies, and more than 46% say they are going to improve compensation and benefits. Companies appear to be looking at other avenues for advancement as well. Technology and training and professional development ranked as the top choices for workplace investments. Emphasis on training and development decreased slightly in 2015; 67% of respondents planned for professional development programs in 2015 compared to 88% in 2014. Nevertheless, the emphasis on what can be done to improve their operating strategies indicates that respondents plan to look at internal adjustments rather than external ones to address their top workforce challenges. TOP INVESTMENTS IN THE NEXT 24 MONTHS Employee retention strategies Compensation and benefits 46.7% Technology 93.3% 40% Recruitment Training and professional development 66.7% 53.3% .

CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. FEDERAL CHANGES COULD MAKE A DIFFERENCE Federal developments may also signal relief for some of the sector’s key obstacles. More than 66% of respondents say the cost of experimentation limits their growth abilities. The recently enacted Protecting Americans from Tax Hikes (PATH) Act may be just what many in the industry wanted. Among its other provisions, the PATH Act makes a federal tax credit for research and development permanent.

Previously the federal tax credit had been allowed to expire only to receive a retroactive renewal. This made planning very difficult for many in the industry. Small businesses in particular may benefit from the PATH Act’s modifications.

The revised credit allows those with less than $50 million in gross receipts claim the credit against their alternative minimum tax (AMT) liability or against the employer’s Federal Insurance Contributions Act (FICA) liability. Respondents ranked higher education courses that are more aligned with skills demanded in the industry as having the second biggest impact on their company. The training of new employees might help address the competition and retention challenges many in the sector face. of respondents say the cost of R&D limits their growth abilities. 13 . 14 GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR WHICH WOULD BEST ADDRESS YOUR CHALLENGES? 6.7% Offering contract laborers more competitive compensation 6.7% Creating more flexible work arrangements 26.7% Broader talent pool WISH LIST FOR CHANGES At the top of the wish list for improvements companies would like to see for their workforce challenges are infrastructure improvements, broadening the talent pool and offering more competitive compensation. The focus on compensation, however, is not as strong as it noted in 2014, when 94% of respondents said that modifying compensation and benefits would address challenges in their workforce. In 2015, almost 27% of respondents point to competitive compensation practices as the solution, and less than 7% say flexible work arrangements might make a difference. More than 26% of companies are looking for a broader talent pool in their applicants. While many companies are evaluating how to improve their employee training, companies are also hoping to see changes in the education realm. Respondents ranked higher and continuing education courses that are more aligned with the skills demanded in the industry as the item that would have the second greatest positive impact on their company.

Other key improvements companies would to see include tax incentives and credits for training programs. Not having a large impact on companies are clarification of crowdfunding regulations and industry deregulation. 26.7% Offering more competitive compensation HOW IMPORTANT WOULD THE FOLLOWING BE FOR YOUR ORGANIZATION'S GROWTH? 33.3% Improving infrastructure Clarification of crowdfunding regulations ï® Very important Higher and continuing education courses that are more aligned with the skills demanded in the industry ï® Moderately important Tax incentives and credits for training programs and research and development activities ï® Slightly important Industry deregulation ï® Not very important . CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. CONCLUSION Growth in the technology and life sciences sector continues to hinge on the ability to find the right people. Companies appear to be moving away from flexible work scheduling and other arrangements to look for internal solutions to their staffing concerns. Many do not appear to view third-party solutions as the answer; companies plan to hire more full-time employees than part-time laborers. To help encourage and reward development of new or improved products and processes, Congress enacted a permanent extension of the federal research and experimentation tax credit in 2015. With the demand that the technology and life sciences companies have for finding the right staffing levels, we may see federal action to encourage education and development for employees in the sector in 2016.

Other trends we expect to see for 2016 include: R&D takes off. 35% of respondents say that innovation in R&D provides them their greatest source of opportunity. With the R&D tax credit made permanent, more companies may be willing to invest more in experimentation efforts. More companies are thinking of the sale.

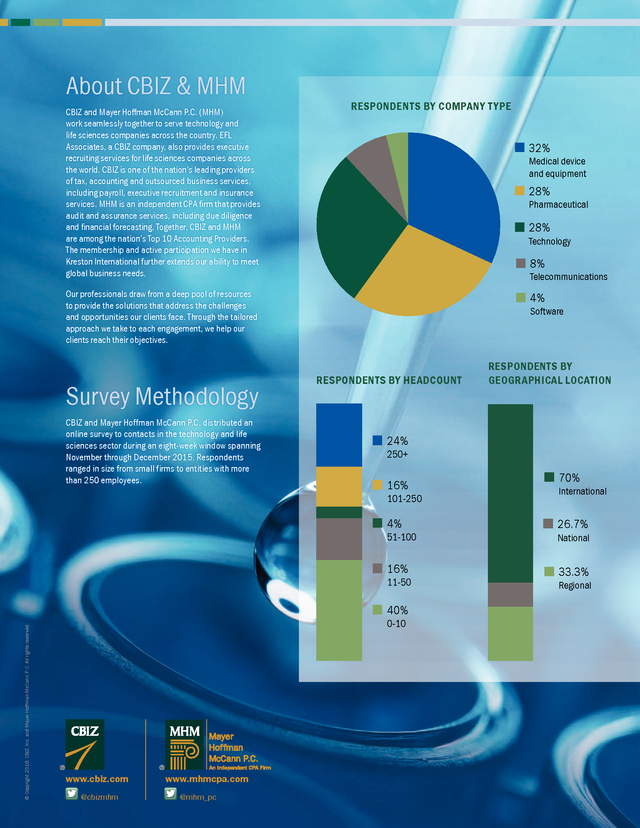

More companies started to consider optimal sale price as their prime goal for the company in 2015, and as expansion continues, we expect to see more merger, acquisition and divestiture activity in the sector. Hiring begins to taper off. Companies do not plan to add as many staff members as in 2014, and the cost of providing employee benefits may keep the numbers of full-time staff members low in the coming months as well. Infrastructure is revamped. Though only 5% of respondents say improving supply chain efficiencies is a priority, both the domestic and the international economy are still struggling. We expect companies to focus more on internal improvements and development to increase profitability. Pipeline programs are revisited. With the majority of companies satisfied with their current workforce and nearly 27% seeking a broader talent pool, we expect to see more the industry pipelines between companies and universities. Retention gets creative. Employee retention continues to be the largest challenge facing the workforce, and to keep the resources they have, more companies will likely look into new strategies for retention and employee satisfaction. 15 . About CBIZ & MHM RESPONDENTS BY COMPANY TYPE CBIZ and Mayer Hoffman McCann P.C. (MHM) work seamlessly together to serve technology and life sciences companies across the country. EFL Associates, a CBIZ company, also provides executive recruiting services for life sciences companies across the world. CBIZ is one of the nation’s leading providers of tax, accounting and outsourced business services, including payroll, executive recruitment and insurance services.

MHM is an independent CPA firm that provides audit and assurance services, including due diligence and financial forecasting. Together, CBIZ and MHM are among the nation’s Top 10 Accounting Providers. The membership and active participation we have in Kreston International further extends our ability to meet global business needs. 32% Medical device and equipment 28% Pharmaceutical 28% Technology 8% Telecommunications Our professionals draw from a deep pool of resources to provide the solutions that address the challenges and opportunities our clients face. Through the tailored approach we take to each engagement, we help our clients reach their objectives. Survey Methodology CBIZ and Mayer Hoffman McCann P.C.

distributed an online survey to contacts in the technology and life sciences sector during an eight-week window spanning November through December 2015. Respondents ranged in size from small firms to entities with more than 250 employees. 4% Software RESPONDENTS BY HEADCOUNT 24% 24% 250+ 16% 4% 16% 16% 101-250 4% 51-100 16% 11-50 © Copyright 2016. CBIZ, Inc.

and Mayer Hoffman McCann P.C. All rights reserved. 40% 40% 0-10 www.cbiz.com @cbizmhm www.mhmcpa.com @mhm_pc RESPONDENTS BY GEOGRAPHICAL LOCATION 70% International 26.7% National 33.3% Regional .

Our evaluation included several factors, such as economic conditions, federal policies and broader industry trends as well as the insights those in the industry shared with us. We compiled our findings into this report in order to provide best practices companies can use moving forward. Our analysis revealed similar patterns for 2015 as noted in the previous year. Companies plan to both physically expand and hire, but many noted the economy and finding and retaining the right personnel limits their growth.

The following number among our other key findings: Expansion is a priority. 61% of respondents named growth as the end goal for their company, and 96% say they have plans to physically expand in the next 24 months. Companies are investing in technology to address challenges. 93% of respondents plan to invest in technology in the next 24 months, and 29% see technological advances providing their greatest source of opportunity. A balance is needed between support and scrutiny. 61% say governmental regulations present an impediment to their operations, while 50% of respondents say tax incentives and benefits would have the greatest positive impact on their company. Leadership presents an obstacle to company development. 67% of respondents cite leadership as an obstacle to growth, and 87% say their company’s incomplete leadership succession plan has an impact on their workforce. Healthcare expenses trigger growth limitations.

More than 86% of respondents say the cost of employee benefits and healthcare inhibits their growth, while more than 28% say labor costs are affecting their hiring plans. Changes in higher education could make a difference. More than 26% of companies seek a broader talent pool, and 88% say that education courses more aligned with the needs of the industry would address their challenges. 3 . 4 GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR Part I: The Expansion Landscape in 2014, when only 77% of respondents planned additional locations in the next 24 months. company is to maximize the sale price, with 35% of respondents citing it as their goal compared to the 23.4% noted in 2014. As companies look to strengthen their position in the marketplace, many may be considering whether their ultimate plan involves an acquisition or divestiture. Compared to 2014, slightly more respondents cited their end goal for the From plans for physical expansion to growing the workforce and optimizing a sale price, companies in the sector continue to cite growth as a top priority. Nearly 61% of respondents say growing and expanding is the long-term goal for their company. The majority (96%) say they plan to expand in the next 24 months, and 96% plan to hire additional full-time employees. Plans to physically expand are higher than they were Selling the business does not appear to be an immediate plan for the majority of respondents, however.

Approximately 80% say they are not planning to exit the market for at least four more years, with 30% saying their exit won’t be for at least a decade. COMPANY END GOAL 2014 2015 23% Maximize the sale price 35% 65% Maximize the sale price Grow and expand the company 6% 61% Take the company public Grow and expand the company 6% 4% Field-changing research and development Field-changing research and development EXPECTED TIME TO EXIT THE MARKET 20% < 1 YEAR 10% 4-5 YEARS 2-3 YEARS 59% 8-9 YEARS 6-7 YEARS > 10 YEARS 10% 30% 30% . CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. FUNDING GROWTH FUNDING GOALS Another sign that the industry is considering growth emerged from companies’ financial plans. Roughly half of respondents plan to raise funds in the next 24 months, with the majority of those planning to raise more than $10 million. Of the fundraisers, 73% cite expansion as the primary use of the capital they are raising. The private sector ranked among the top places companies planned to look for these funds. Private equity and venture capital came in as the most popular funding sources with 55% and 36% of respondents planning to use them respectively.

More traditional funding will also be involved, with 18% of respondents planning to raise money from banks. The shift to private funding marked a change from 2014, when 61.5% of respondents planned to use banks as their primary funding source. Raising capital in the next 24 months? 48% â– Yes â– No â– Unsure 73% 9% 18% 44% 8% SOURCE OF FUNDRAISING Private Equity Venture Capital Banks 55% 36% 18% Foreign Country Capital Angel Investors Family & Friends 18% 10% 10% Primary use of capital â– Expansion â– Research and development â– Working capital 5 . GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR KEY LOCATIONS The vast majority of respondents plan to physically expand in the next 24 months. As noted in 2014, respondents favor domestic growth slightly more than international expansion with 86% of respondents considering locations in the United States and 72% planning growth overseas. Among the most popular destinations for domestic growth are the Midwest (54%) and West (50%) while the Far East (54%) and Europe (45%) ranked among the top destinations abroad. Planned expansion in the Far East picked up notably from 2014, when it accounted for only 15% of total planned expansion. Planned development in the Middle East dropped slightly, going from 7.7% to 4.1%. Respondents’ current footprint appears to be a strong factor in their plans. The majority of regional companies plan to stay local, with 80% of expansion activity occurring only in the United States.

Those with a national footprint go both ways, with 50% of respondents planning to stay domestic and 50% planning to expand into international operations. International companies favor international expansion slightly more than domestic growth, with 88% of international respondents planning to grow their locations abroad and 69% planning to grow domestically. AREAS OF GREATEST DEVELOPMENT ACTIVITY —— —— —— —————————————————————————————————————————————————— Unpopular —— Popular —— 6 . CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. ECONOMIC WOES The economy could be one of the major reasons why technology and life sciences companies are not undertaking broader expansion plans. When asked to evaluate the factors affecting company growth, economic conditions came in first with 83% of respondents citing it as having an impact on their company. Governmental regulations also appear to be a factor affecting growth, with 61% naming them as a top concern. Respondents say two governmental regulatory areas in particular present obstacles, the Food and Drug Administration(FDA)’s regulatory pathway and federal guidelines for research and development activities. Access to funding is not a large issue for companies in the sector.

Approximately 61% of respondents say insufficient capital does not affect their growth plans, and half say cash flow limitations are a low concern. Other areas that have a small effect on the sector’s growth include public market pathways and quality control. This represents a change from 2014, where quality control ranked as companies’ top factor affecting expansion. Level of Concern FACTORS AFFECTING COMPANY GROWTH Insufficient capital Access to public markets Quality control â– Major factor Intellectual property concerns Inadequate product demand â– Significant factor Production Governmental inefficiencies regulations â– Factor â– Minor factor Cash flow limitations Economic Cost of conditions research and development â– Not a major factor 7 .

8 GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR Part 2: Workforce Snapshot Operational growth goes hand-in-hand with workforce expansion, and the majority of respondents (92%) plan to hire both full-time staff and third-party labor in the next 24 months. With the hiring of contract laborers, respondents say they are more likely to hire a small number, with 57% planning to hire between one and 10, and 9% planning to hire between 11 and 50 third-party employees. Complexity in third-party reflects a slight decrease in the number of full-time staff companies plan to hire compared to the previous year. In 2014, 47% of respondents said they planned to hire between 11 and 50 employees and 18% planned to hire more than 50. A stagnant economy may be playing a role in these plans, but the sector continues to face other challenges to the development of its workforce as well. arrangements does not appear to be a deterrent for companies looking to use contract labor, with 67% of respondents saying that setting up the arrangement has little to no effect on their company. Companies’ resources will likely be funneled toward full-time staff, with 48% planning to hire between one and 10, 35% planning to hire between 11 and 50 and 12% planning to hire more than 50 people in the next 24 months.

The distribution of new hires PLANNED HIRES IN THE NEXT 24 MONTHS 4% 48% 34% 8% 4% ï® ï® ï® ï® ï® ï® 0 1-10 11-50 51-100 101-250 250+ 35% 57% 8% Full-time equivalent employees Third-party or contract laborers . CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. THE ACA AND THE HIRING PROCESS The Affordable Care Act (ACA) could be playing a role in the hiring process. Of the companies not planning to hire additional staff, almost 29% say it’s because of concern over how the ACA may affect their bottom line. The concern carries over to those companies planning to grow their workforce as well. More than 86% say the cost of employee benefits and healthcare has a major impact on their plans for staffing levels. Of particular concern is the effect consolidation of insurance carriers will have on health insurance premiums, which respondents ranked as their number one ACA issue. Third-party and contract laborers are not subject to the mandate that requires employers to provide their staff with adequate and affordable coverage, but companies do not appear to be favoring the use of third-party over full-time employees.

Nearly 35% of companies do not plan to hire additional third-party laborers. Of those that do plan to grow staff, the majority (57%) intend to add between one and 10 contract positions. WHY ARE YOU NOT PLANNING TO HIRE? Affordable Care Act concerns 29% HOW DOES THE COST OF EMPLOYEE BENEFITS AND HEALTHCARE AFFECT YOUR COMPANY? Cost of labor too great 29% 54% 7% 7% 32% â– â– â– â– Significant factor Factor Minor factor Not a major factor of respondents say the cost of employee benefits and healthcare plays a significant factor in their workforce planning. 9 . GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR SATISFACTION IN THE CURRENT WORKFORCE When asked to evaluate the different subsets of their company, respondents say financial departments are among the top performers, with 59% labeling their division as prepared and 6% of respondents saying their staff is very prepared for what’s ahead. Operational staff also received high rankings, with 53% of respondents calling the department prepared. The majority of respondents (53%) also called their marketing and sales team prepared, indicating more confidence Hiring plans appear to be for growth purposes, as management indicated that they feel their current staff can meet the challenges of the company’s current operating environment. Inadequately skilled workforce ranks low in the list of workforce trends affecting growth.

Only 6% say an inadequate workforce presents a significant obstacle to their development. than was expressed in 2014, when 65% of respondents said their marketing and sales teams were not prepared for future challenges. On the flip side, respondents raised some concern about their human resources staff, with 12% of respondents saying their human resources and talent management teams were not prepared for challenges. As in 2014, a small portion of respondents also expresses concern about their manufacturers, with 6% saying they are not at all prepared. HOW PREPARED IS EACH DEPARTMENT TO MEET WORKFORCE CHALLENGES? Level of Preparedness 10 Financial Human resources and talent management â– Very prepared â– Prepared Management â– Neutral Manufacturing â– Not prepared Marketing and sales Operational â– Not prepared at all .

CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. THE RETENTION ISSUE are limited career mobility options for younger staff. With competition in the marketplace, talented young employees may be increasingly deciding whether to take their talents elsewhere. Keeping employees who are well-prepared for the industry is another concern. The workforce trends most impacting companies include employee retention and increased competition for talent, each with more than 86% of respondents saying they have a large effect on their company. Part of the problem may be the limited room for internal growth and development of employees. Nearly three-quarters of respondents say there There may not be an immediate fix to the limited mobility option, either; less than 30% of companies say baby boomers’ exit from the business is creating an issue, which could be indicative that the industry has a younger-than-average workforce.

At the same time, younger employees may have future opportunities in leadership positions. More than 70% of respondents say they do not have a clear successor to run the business. Though the number of companies without an identified successor may be high, naming a successor has not historically been a key concern; in 2014, only 5.9% of companies said that no clear successor to run the business was a top challenge to their organization.

This may shift in the future. Level of Impact IMPACT OF WORKFORCE TRENDS Baby boomers’ exit from the workforce Complexity in third-party and contract labor arrangements ï® Major factor Compliance with federal regulations Cost of employee benefits and healthcare ï® Significant factor Employee retention ï® Factor Increased competition for talent ï® Minor factor Limited career mobility options for younger employees No clear successor to run the business ï® Not a major factor Security of employee personally identifiable information 11 . 12 GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR Part 3: Opportunities Ahead To combat the challenges with recruitment and retention, companies plan to make investments in their current strategies. Forty percent of respondents say they plan to invest in better employee retention strategies, and more than 46% say they are going to improve compensation and benefits. Companies appear to be looking at other avenues for advancement as well. Technology and training and professional development ranked as the top choices for workplace investments. Emphasis on training and development decreased slightly in 2015; 67% of respondents planned for professional development programs in 2015 compared to 88% in 2014. Nevertheless, the emphasis on what can be done to improve their operating strategies indicates that respondents plan to look at internal adjustments rather than external ones to address their top workforce challenges. TOP INVESTMENTS IN THE NEXT 24 MONTHS Employee retention strategies Compensation and benefits 46.7% Technology 93.3% 40% Recruitment Training and professional development 66.7% 53.3% .

CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. FEDERAL CHANGES COULD MAKE A DIFFERENCE Federal developments may also signal relief for some of the sector’s key obstacles. More than 66% of respondents say the cost of experimentation limits their growth abilities. The recently enacted Protecting Americans from Tax Hikes (PATH) Act may be just what many in the industry wanted. Among its other provisions, the PATH Act makes a federal tax credit for research and development permanent.

Previously the federal tax credit had been allowed to expire only to receive a retroactive renewal. This made planning very difficult for many in the industry. Small businesses in particular may benefit from the PATH Act’s modifications.

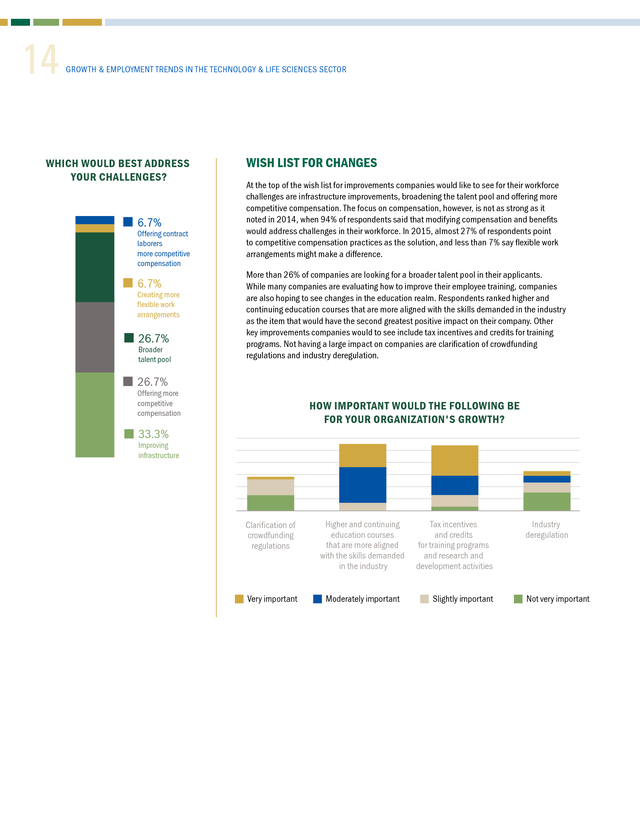

The revised credit allows those with less than $50 million in gross receipts claim the credit against their alternative minimum tax (AMT) liability or against the employer’s Federal Insurance Contributions Act (FICA) liability. Respondents ranked higher education courses that are more aligned with skills demanded in the industry as having the second biggest impact on their company. The training of new employees might help address the competition and retention challenges many in the sector face. of respondents say the cost of R&D limits their growth abilities. 13 . 14 GROWTH & EMPLOYMENT TRENDS IN THE TECHNOLOGY & LIFE SCIENCES SECTOR WHICH WOULD BEST ADDRESS YOUR CHALLENGES? 6.7% Offering contract laborers more competitive compensation 6.7% Creating more flexible work arrangements 26.7% Broader talent pool WISH LIST FOR CHANGES At the top of the wish list for improvements companies would like to see for their workforce challenges are infrastructure improvements, broadening the talent pool and offering more competitive compensation. The focus on compensation, however, is not as strong as it noted in 2014, when 94% of respondents said that modifying compensation and benefits would address challenges in their workforce. In 2015, almost 27% of respondents point to competitive compensation practices as the solution, and less than 7% say flexible work arrangements might make a difference. More than 26% of companies are looking for a broader talent pool in their applicants. While many companies are evaluating how to improve their employee training, companies are also hoping to see changes in the education realm. Respondents ranked higher and continuing education courses that are more aligned with the skills demanded in the industry as the item that would have the second greatest positive impact on their company.

Other key improvements companies would to see include tax incentives and credits for training programs. Not having a large impact on companies are clarification of crowdfunding regulations and industry deregulation. 26.7% Offering more competitive compensation HOW IMPORTANT WOULD THE FOLLOWING BE FOR YOUR ORGANIZATION'S GROWTH? 33.3% Improving infrastructure Clarification of crowdfunding regulations ï® Very important Higher and continuing education courses that are more aligned with the skills demanded in the industry ï® Moderately important Tax incentives and credits for training programs and research and development activities ï® Slightly important Industry deregulation ï® Not very important . CBIZ & MAYER HOFFMAN McCANN P – 2015 REPORT .C. CONCLUSION Growth in the technology and life sciences sector continues to hinge on the ability to find the right people. Companies appear to be moving away from flexible work scheduling and other arrangements to look for internal solutions to their staffing concerns. Many do not appear to view third-party solutions as the answer; companies plan to hire more full-time employees than part-time laborers. To help encourage and reward development of new or improved products and processes, Congress enacted a permanent extension of the federal research and experimentation tax credit in 2015. With the demand that the technology and life sciences companies have for finding the right staffing levels, we may see federal action to encourage education and development for employees in the sector in 2016.

Other trends we expect to see for 2016 include: R&D takes off. 35% of respondents say that innovation in R&D provides them their greatest source of opportunity. With the R&D tax credit made permanent, more companies may be willing to invest more in experimentation efforts. More companies are thinking of the sale.

More companies started to consider optimal sale price as their prime goal for the company in 2015, and as expansion continues, we expect to see more merger, acquisition and divestiture activity in the sector. Hiring begins to taper off. Companies do not plan to add as many staff members as in 2014, and the cost of providing employee benefits may keep the numbers of full-time staff members low in the coming months as well. Infrastructure is revamped. Though only 5% of respondents say improving supply chain efficiencies is a priority, both the domestic and the international economy are still struggling. We expect companies to focus more on internal improvements and development to increase profitability. Pipeline programs are revisited. With the majority of companies satisfied with their current workforce and nearly 27% seeking a broader talent pool, we expect to see more the industry pipelines between companies and universities. Retention gets creative. Employee retention continues to be the largest challenge facing the workforce, and to keep the resources they have, more companies will likely look into new strategies for retention and employee satisfaction. 15 . About CBIZ & MHM RESPONDENTS BY COMPANY TYPE CBIZ and Mayer Hoffman McCann P.C. (MHM) work seamlessly together to serve technology and life sciences companies across the country. EFL Associates, a CBIZ company, also provides executive recruiting services for life sciences companies across the world. CBIZ is one of the nation’s leading providers of tax, accounting and outsourced business services, including payroll, executive recruitment and insurance services.

MHM is an independent CPA firm that provides audit and assurance services, including due diligence and financial forecasting. Together, CBIZ and MHM are among the nation’s Top 10 Accounting Providers. The membership and active participation we have in Kreston International further extends our ability to meet global business needs. 32% Medical device and equipment 28% Pharmaceutical 28% Technology 8% Telecommunications Our professionals draw from a deep pool of resources to provide the solutions that address the challenges and opportunities our clients face. Through the tailored approach we take to each engagement, we help our clients reach their objectives. Survey Methodology CBIZ and Mayer Hoffman McCann P.C.

distributed an online survey to contacts in the technology and life sciences sector during an eight-week window spanning November through December 2015. Respondents ranged in size from small firms to entities with more than 250 employees. 4% Software RESPONDENTS BY HEADCOUNT 24% 24% 250+ 16% 4% 16% 16% 101-250 4% 51-100 16% 11-50 © Copyright 2016. CBIZ, Inc.

and Mayer Hoffman McCann P.C. All rights reserved. 40% 40% 0-10 www.cbiz.com @cbizmhm www.mhmcpa.com @mhm_pc RESPONDENTS BY GEOGRAPHICAL LOCATION 70% International 26.7% National 33.3% Regional .