Description

Volume 3 Issue 3

M a g a z ine

COVER TO COME

To the EB-5 Community

by Congressmen Jared

Polis and Mark Amodei

EB5Investors.com

EB-5 Investor Scrutiny

Common Misconceptions and

a Step-by-Step Overview of

the EB-5 Application Process

. Volume 3 - Issue 3

On the cover

This issue focuses on the recent legislative developments leading up

to and following the December 11th extension deadline for the

EB-5 Regional Center Program. Congressman Jared Polis and

Mark Amodei discuss the one-year extension, beginning on page

21. We also invited industry veterans to weigh in on another

important, timely issue: what is the scrutiny process that EB-5

investors go through? Read the break-down of the process

beginning on page 58.

4

Publisher’s Note

6

EB-5 Brazil

by Dennis Rodrigues

10

Avoiding the Inadvertent

Investment Company

by Angelo Paparelli, Mark Katzoff,

Christopher Robertson and Gregory White

14

Page 21

Pre-Immigration Tax Planning

by Jacob Stein

62 Why EB-5 Investors Cannot Simply

Buy a Green Card

COVER STORY

21 To the EB-5 Community

by David Hirson and Winnie Ng

by Congressman Jared Polis and Mark Amodei

26

Understanding Loan Documents

in EB-5 Project Financing

68

by Steve Park

by Abbas Hashmi

35

Upcoming Events

36

Prevailing Against the Notice of

Intent to Terminate

70

by Christian Triantaphyllis

40

74

Amendments and Effective Changes to the 76

EB-5 Regional Center Program Delayed for

Consideration until September 30, 2016

EB5’s Status Quo Extension:

A Regional Center Perspective

86

48

Conference Recap: the 4th Annual

California EB-5 Conference, Los Angeles, 91

August 2015

54

Conference Recap: the 2015 Shenzhen

Private Delegation, Shenzhen, China,

October 2015

58

EB-5 Investor Scrutiny

58 Let’s Get the Truth Straight: Correcting

Common Misconceptions about EB-5

by Reid Thomas and Kaitlin Halloran

Investor Profile: David Brown

Migration Agent Interviews

Larry Wang: Well Trend CEO

Thomas Kut: Immigration Consultant

by EB5 Investors Magazine Staff

by Angel Brunner

FEATURE ARTICLE

“You’re Chasing Rainbows in Vietnam”

The Stunning Growth of EB-5 in Vietnam

by Brandon Meyer

by Enrique Gonzalez

44

Basic Do’s and Dont’s for Marketing to

Middle Eastern & South Asian EB-5

Investors

Opinion: A Secondary Liquidity Market

Could Benefit EB-5

by Jon Baker

Opinion: An Open Letter to USCIS From

A Practicing EB-5 Economist On USCIS

Guidance to Economic Inputs for Job

Creation Studies

by Scott Barnhart

96

Misappropriations Fraud Detection

& Deterrence

by Robert Kraft

98

Why the Definition of “Capital” For the

Purposes of the EB-5 Program Should

Be Broad

by Dillon Colucci

WWW.EB5INVESTORS.COM

3

. Understanding

Loan Documents in

EB-5 Project Financing

by Steve Park

Background

Emphasizing the compliance requirements under the EB-5

program and applicable securities laws, EB-5 project teams

frequently defer negotiating definitive financing documents

to a later date. In certain cases, EB-5 project teams may not

want to finalize definitive loan documents when the terms

and timing of senior financing (either debt or equity) are

uncertain or will depend on the amount and timing of the

actual EB-5 funding. However, well-planned financing documents are critical in protecting investors’ interests and should

not be treated as an after-thought or perfunctory post-offering

26

step to put the EB-5 funds into the job creating enterprise

(“JCE”) borrower.

EB-5 project financing can take the form of equity or debt

or any combination of the two. Each form brings its own

unique benefits as well as structural challenges to consider

for all parties involved.

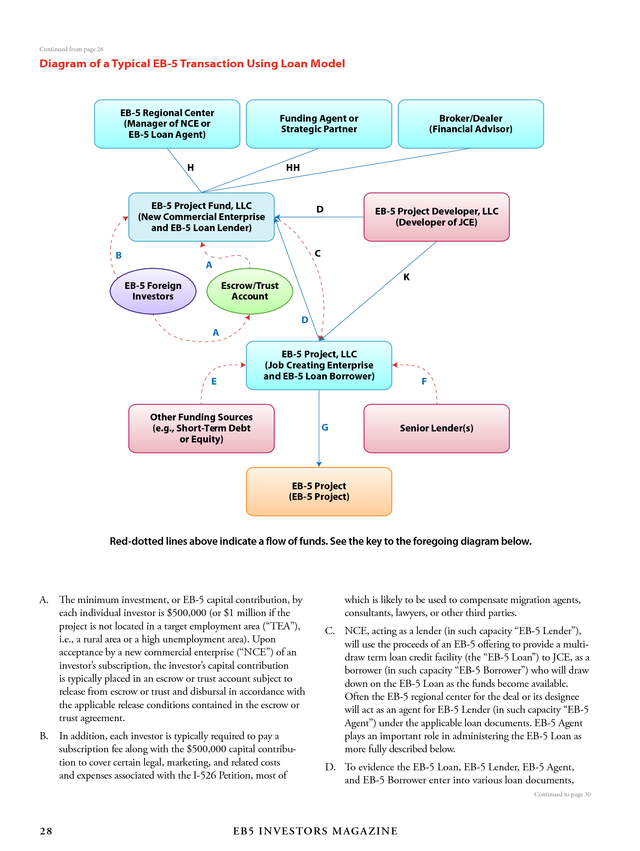

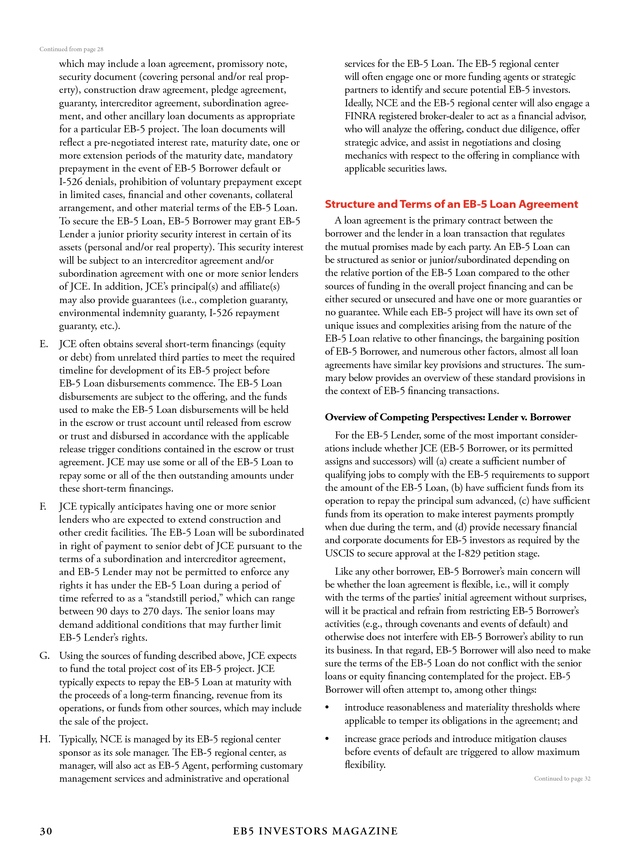

This article explains the typical loan arrangement used in EB-5 transactions, focusing on the overall structure to identify various parties and ancillary loan documents involved and their respective roles in EB-5 transactions. EB5 INVESTORS MAGAZINE Continued to page 28 . Continued from page 26 Diagram of a Typical EB-5 Transaction Using Loan Model EB-5 Regional Center (Manager of NCE or EB-5 Loan Agent) Funding Agent or Strategic Partner H HH EB-5 Project Fund, LLC (New Commercial Enterprise and EB-5 Loan Lender) B Broker/Dealer (Financial Advisor) D EB-5 Project Developer, LLC (Developer of JCE) C A EB-5 Foreign Investors K Escrow/Trust Account D A EB-5 Project, LLC (Job Creating Enterprise and EB-5 Loan Borrower) E Other Funding Sources (e.g., Short-Term Debt or Equity) G F Senior Lender(s) EB-5 Project (EB-5 Project) Red-dotted lines above indicate a flow of funds. See the key to the foregoing diagram below. A. The minimum investment, or EB-5 capital contribution, by each individual investor is $500,000 (or $1 million if the project is not located in a target employment area (“TEA”), i.e., a rural area or a high unemployment area). Upon acceptance by a new commercial enterprise (“NCE”) of an investor’s subscription, the investor’s capital contribution is typically placed in an escrow or trust account subject to release from escrow or trust and disbursal in accordance with the applicable release conditions contained in the escrow or trust agreement. B. In addition, each investor is typically required to pay a subscription fee along with the $500,000 capital contribution to cover certain legal, marketing, and related costs and expenses associated with the I-526 Petition, most of which is likely to be used to compensate migration agents, consultants, lawyers, or other third parties. C. NCE, acting as a lender (in such capacity “EB-5 Lender”), will use the proceeds of an EB-5 offering to provide a multidraw term loan credit facility (the “EB-5 Loan”) to JCE, as a borrower (in such capacity “EB-5 Borrower”) who will draw down on the EB-5 Loan as the funds become available. Often the EB-5 regional center for the deal or its designee will act as an agent for EB-5 Lender (in such capacity “EB-5 Agent”) under the applicable loan documents. EB-5 Agent plays an important role in administering the EB-5 Loan as more fully described below. D. To evidence the EB-5 Loan, EB-5 Lender, EB-5 Agent, and EB-5 Borrower enter into various loan documents, Continued to page 30 28 EB5 INVESTORS MAGAZINE .

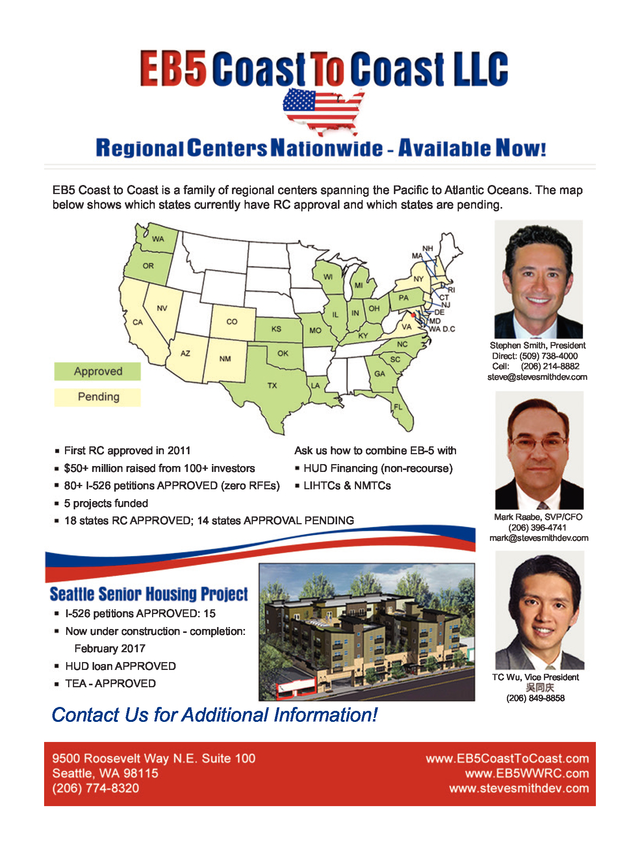

EB5 Coast to Coast is a family of regional centers spanning the Pacific to Atlantic Oceans. The map below shows which states currently have RC approval and which states are pending. Stephen Smith, President Direct: (509) 738-4000 Cell: (206) 214-8882 steve@stevesmithdev.com First RC approved in 2011 Ask us how to combine EB-5 with $50+ million raised from 100+ investors HUD Financing (non-recourse) 80+ I-526 petitions APPROVED (zero RFEs) LIHTCs & NMTCs 5 projects funded 18 states RC APPROVED; 14 states APPROVAL PENDING Mark Raabe, SVP/CFO (206) 396-4741 mark@stevesmithdev.com I-526 petitions APPROVED: 15 Now under construction - completion: February 2017 HUD loan APPROVED TEA - APPROVED Contact Us for Additional Information! TC Wu, Vice President (206) 849-8858 . Continued from page 28 which may include a loan agreement, promissory note, security document (covering personal and/or real property), construction draw agreement, pledge agreement, guaranty, intercreditor agreement, subordination agreement, and other ancillary loan documents as appropriate for a particular EB-5 project. The loan documents will reflect a pre-negotiated interest rate, maturity date, one or more extension periods of the maturity date, mandatory prepayment in the event of EB-5 Borrower default or I-526 denials, prohibition of voluntary prepayment except in limited cases, financial and other covenants, collateral arrangement, and other material terms of the EB-5 Loan. To secure the EB-5 Loan, EB-5 Borrower may grant EB-5 Lender a junior priority security interest in certain of its assets (personal and/or real property). This security interest will be subject to an intercreditor agreement and/or subordination agreement with one or more senior lenders of JCE. In addition, JCE’s principal(s) and affiliate(s) may also provide guarantees (i.e., completion guaranty, environmental indemnity guaranty, I-526 repayment guaranty, etc.). E. JCE often obtains several short-term financings (equity or debt) from unrelated third parties to meet the required timeline for development of its EB-5 project before EB-5 Loan disbursements commence.

The EB-5 Loan disbursements are subject to the offering, and the funds used to make the EB-5 Loan disbursements will be held in the escrow or trust account until released from escrow or trust and disbursed in accordance with the applicable release trigger conditions contained in the escrow or trust agreement. JCE may use some or all of the EB-5 Loan to repay some or all of the then outstanding amounts under these short-term financings. F. JCE typically anticipates having one or more senior lenders who are expected to extend construction and other credit facilities. The EB-5 Loan will be subordinated in right of payment to senior debt of JCE pursuant to the terms of a subordination and intercreditor agreement, and EB-5 Lender may not be permitted to enforce any rights it has under the EB-5 Loan during a period of time referred to as a “standstill period,” which can range between 90 days to 270 days.

The senior loans may demand additional conditions that may further limit EB-5 Lender’s rights. G. Using the sources of funding described above, JCE expects to fund the total project cost of its EB-5 project. JCE typically expects to repay the EB-5 Loan at maturity with the proceeds of a long-term financing, revenue from its operations, or funds from other sources, which may include the sale of the project. H. Typically, NCE is managed by its EB-5 regional center sponsor as its sole manager. The EB-5 regional center, as manager, will also act as EB-5 Agent, performing customary management services and administrative and operational 30 services for the EB-5 Loan.

The EB-5 regional center will often engage one or more funding agents or strategic partners to identify and secure potential EB-5 investors. Ideally, NCE and the EB-5 regional center will also engage a FINRA registered broker-dealer to act as a financial advisor, who will analyze the offering, conduct due diligence, offer strategic advice, and assist in negotiations and closing mechanics with respect to the offering in compliance with applicable securities laws. Structure and Terms of an EB-5 Loan Agreement A loan agreement is the primary contract between the borrower and the lender in a loan transaction that regulates the mutual promises made by each party. An EB-5 Loan can be structured as senior or junior/subordinated depending on the relative portion of the EB-5 Loan compared to the other sources of funding in the overall project financing and can be either secured or unsecured and have one or more guaranties or no guarantee. While each EB-5 project will have its own set of unique issues and complexities arising from the nature of the EB-5 Loan relative to other financings, the bargaining position of EB-5 Borrower, and numerous other factors, almost all loan agreements have similar key provisions and structures.

The summary below provides an overview of these standard provisions in the context of EB-5 financing transactions. Overview of Competing Perspectives: Lender v. Borrower For the EB-5 Lender, some of the most important considerations include whether JCE (EB-5 Borrower, or its permitted assigns and successors) will (a) create a sufficient number of qualifying jobs to comply with the EB-5 requirements to support the amount of the EB-5 Loan, (b) have sufficient funds from its operation to repay the principal sum advanced, (c) have sufficient funds from its operation to make interest payments promptly when due during the term, and (d) provide necessary financial and corporate documents for EB-5 investors as required by the USCIS to secure approval at the I-829 petition stage. Like any other borrower, EB-5 Borrower’s main concern will be whether the loan agreement is flexible, i.e., will it comply with the terms of the parties’ initial agreement without surprises, will it be practical and refrain from restricting EB-5 Borrower’s activities (e.g., through covenants and events of default) and otherwise does not interfere with EB-5 Borrower’s ability to run its business. In that regard, EB-5 Borrower will also need to make sure the terms of the EB-5 Loan do not conflict with the senior loans or equity financing contemplated for the project.

EB-5 Borrower will often attempt to, among other things: • introduce reasonableness and materiality thresholds where applicable to temper its obligations in the agreement; and • increase grace periods and introduce mitigation clauses before events of default are triggered to allow maximum flexibility. EB5 INVESTORS MAGAZINE Continued to page 32 . Continued from page 30 Definitions Capitalized defined terms are crucial in loan agreements because they are repeated throughout the loan agreement as well as other related ancillary loan documents. The first section of the loan agreement will typically define these capitalized terms used in the loan agreement. Borrowing Terms and Procedures The second section of the loan agreement will typically provide detailed procedures for borrowing, including the following: • the amount of the loan; • the time period for borrowing and procedure for loan advances (e.g., a multi-draw with a fixed availability period or based on construction draws); • the repayment of principal and accrued and unpaid interest at final maturity; • the availability of extension periods exercisable by EB-5 Borrower for an increased interest rate and/or an extension fee; and • computation of interest rate and other fees (e.g., origination fee). Conditions Precedent for Closing and/or Funding This section specifies the conditions that EB-5 Borrower must meet before EB-5 Lender will lend money under the loan agreement and is often divided into two categories: initial conditions to be satisfied before the first loan advance and conditions that apply to all advances (the first and any subsequent advances). Examples of conditions precedent relevant to the EB-5 Loan transactions include the following: • production of various documents such as corporate authorization related documents (e.g., secretarial certificates, authorizing resolutions, good standing certificates, etc.) and other ancillary loan documents, including guaranties, pledge agreements, and intercreditor agreements, as applicable; • proof of EB-5 Borrower’s receipt of other funds in the project’s capital stack before the EB-5 Loan is funded (e.g., proof of equity, tax credits, senior loan, etc.); • receipt and satisfactory review of customary due diligence documents including an appraisal, title and survey reports, lien searches and environmental reports with respect to the project; and • to the extent the EB-5 Loan is secured, evidence that the security interest in all collateral is properly perfected (e.g., through filing of applicable UCC financing statements for certain personal property and recording of mortgage, deed to secure debt, or deed of trust for certain real property). the payments of interest and principal (e.g., monthly, quarterly, or annually; interest only for certain period; or interest and principal installments); • for each EB-5 Loan advance under the loan agreement and (b) the date that is a few business days after the Form I-829 Petitions of all EB-5 investors are either (i) adjudicated by the USCIS or (ii) voluntarily or involuntarily abandoned or withdrawn. To structure the funding or borrowing mechanics for the EB-5 Loan transactions properly, the parties must understand precisely how and when EB-5 funds will be released from the escrow or trust account and time the EB-5 Loan disbursements under the loan agreement accordingly. In most cases, EB-5 Lender will not have the funds to disburse the entire amount of the EB-5 Loan committed under the loan agreement at the initial closing. As EB-5 Lender raises funds from EB-5 investors over time, EB-5 Lender and EB-5 Borrower will need to maintain close communication and schedule the EB-5 Loan disbursements based on the EB-5 investments then held in the escrow or trust account and applicable release triggers. For an EB-5 Lender, it will be important to negotiate a binding commitment from EB-5 Borrower to draw down on the EB-5 Loan so long as EB-5 Lender raises certain minimum amount within a reasonable time negotiated between the parties (e.g., 50 percent of the EB-5 Loan commitment within 12 to 24 months of the loan agreement date).

This is unique to EB-5 loan transactions in that EB-5 Lender has legitimate reasons to worry about EB-5 Borrower refusing to draw down on the EB-5 Loan after EB-5 Lender has incurred substantial costs in raising EB-5 funds from foreign investors and the investors have relied on EB-5 Borrower’s commitment to utilizing the full principal amount by filing their I-526 Petition with the U.S. Citizenship and Immigration Services (the “USCIS”) in advance of the full drawdown. Typically, the maturity date for the EB-5 Loan is scheduled to be the later of (a) the fifth anniversary date of the funding date It is crucial for EB-5 Lender to have a designated team or personnel to administer the EB-5 Loan and properly verify conditions precedent before funding each disbursement under the loan agreement. Representations and Warranties One of the many ways EB-5 Lenders can minimize their risks is through representations and warranties from EB-5 Borrowers. The representations and warranties section of the loan agreement allows EB-5 Lenders to: (a) gather material information about EB-5 Borrower and its operation and assets; (b) to garner the rights to monitor the business of EB-5 Borrower on an ongoing basis properly; and (c) allocate risks to hold EB-5 Borrower liable if any representation or warranty is untrue (whether or not EB-5 Borrower is at fault). While representations and warranties are fairly standard, it is important for EB-5 Borrowers to review them carefully to ensure that each provision contains suitable carve-outs and materiality thresholds wherever appropriate. Covenants Covenants are particularly relevant and important for long-term credit arrangements such as an EB-5 Loan, which will typically have a term longer than five years based on the Continued to page 34 32 EB5 INVESTORS MAGAZINE .

Continued from page 32 EB-5 program requirements. Covenants are designed to protect EB-5 Lenders’ investment during the life of the EB-5 Loan by monitoring EB-5 Borrower’s operation, restricting certain actions EB-5 Borrower can take, and requiring certain other actions to be taken. A loan covenant requires the borrower to fulfill certain conditions or forbids the borrower from undertaking certain actions. The covenants section of the loan agreement is often the most heavily negotiated between EB-5 Borrower and EB-5 Lender because EB-5 Borrower naturally wants to run its business without any interference from EB-5 Lender while EB-5 Lender has a legitimate right (and duty to protect EB-5 investors) to impose an appropriate level of constraints on EB-5 Borrower to protect its loan investment.

There are four categories of covenants commonly found in the loan agreement: • Information covenants: unaudited quarterly financial statements, audited annual financial statements, compliance certificates, notice upon occurrence of a material adverse change in EB-5 Borrower’s business • Affirmative covenants: paying taxes, maintaining insurance, permitting EB-5 Lender to inspect books and records as well as the project, making minimum capital expenditure or hiring certain number of direct full-time employees to comply with EB-5 job creation analysis • • severability, governing law, jurisdiction, waiver of jury trial, US Patriot Act and other similar regulatory requirements. Other Ancillary EB-5 Loan Documents and Important Considerations Other ancillary EB-5 Loan documents may include a promissory note, security document (covering personal and/or real property), construction draw agreement, pledge agreement, guaranty, subordination agreement and intercreditor agreement, as required by particular circumstances of an EB-5 project. However, one of the most common and critical issues relate to the perfection of securities interests in collateral, especially when dealing with EB-5 transactions secured by real property with multiple lenders and funding during construction. Rules governing security interests are very complex, and EB-5 Lenders must rely on experienced commercial finance attorneys to perfect their security interests properly under applicable law (e.g., personal property under Article 9 of the Uniform Commercial Code and real property under the real property law of applicable jurisdiction). In such instances, additional items to consider include: • Third party construction draw management • General contractor and subcontractor consents and waivers Negative covenants: requiring written consent of EB-5 Lender to incur additional debt, sell certain assets, pay dividends, pledge additional collateral, make material changes to the business plan or project, hire executive level persons, enter into material agreements, etc. • Phase I environmental report • Appraisal report • ALTA survey • Title search and lender’s policy of title insurance Financial covenants: net worth, leverage ratio, coverage ratio, minimum EBITDA • Mortgage recording tax A breach of covenant will be an event of default and trigger various remedies that EB-5 Lender may pursue (e.g., accelerating the loan or foreclosing on collateral) subject to the rights of senior lender if EB-5 Lender agreed to subordinate.

Accordingly, EB-5 Borrowers must review the covenants carefully to ensure that each provision contains suitable carve-outs or grace periods and materiality thresholds wherever appropriate to accommodate their project. Events of Defaults All loan agreements contain a section that details certain events of defaults (such as non-payment of interest or principal on the EB-5 Loan, a breach of covenant, or insolvency of EB-5 Borrower), which will allow EB-5 Lender to exercise its remedies, including acceleration of the repayment of outstanding debt, pursuing guarantors, if any, and/or enforcing its security interests, if any. However, more often than not, these remedies are subject to the rights of senior lender if EB-5 Lender agreed to subordinate, as discussed herein. Conclusion By now, almost everyone in the EB-5 industry has developed an appreciation for, or at the very least, an acceptance of, the need for well-planned securities offering materials and EB-5 compliant business plan and economic impact analysis. EB-5 project teams should give equal consideration to carefully evaluating the EB-5 financing structures and negotiating appropriate loan documents with EB-5 Borrowers.

Before finalizing the loan terms, it is also very important to discuss the proposed loan structure with target funding agents to understand whether it would be acceptable to their EB-5 investors and what additional terms or conditions, if any, may be required to be marketable. ★ Miscellaneous Provisions The last section of all loan agreements will include certain boilerplate provisions to cover notices, integration, counterpart, 34 Steve Park EB5 INVESTORS MAGAZINE Steve Park is a securities attorney and a partner at Ballard Spahr LLP, in Atlanta, Ga. Park is fluent in Korean, and focuses his practice on corporate, securities and finance law. His emphasis is on corporate governance, corporate finance, compliance with SEC regulations, private and public securities offerings and the requirements of reporting.

Park regularly works on commercial lending transactions with lenders and borrowers involved in EB-5 financing matters. .

This article explains the typical loan arrangement used in EB-5 transactions, focusing on the overall structure to identify various parties and ancillary loan documents involved and their respective roles in EB-5 transactions. EB5 INVESTORS MAGAZINE Continued to page 28 . Continued from page 26 Diagram of a Typical EB-5 Transaction Using Loan Model EB-5 Regional Center (Manager of NCE or EB-5 Loan Agent) Funding Agent or Strategic Partner H HH EB-5 Project Fund, LLC (New Commercial Enterprise and EB-5 Loan Lender) B Broker/Dealer (Financial Advisor) D EB-5 Project Developer, LLC (Developer of JCE) C A EB-5 Foreign Investors K Escrow/Trust Account D A EB-5 Project, LLC (Job Creating Enterprise and EB-5 Loan Borrower) E Other Funding Sources (e.g., Short-Term Debt or Equity) G F Senior Lender(s) EB-5 Project (EB-5 Project) Red-dotted lines above indicate a flow of funds. See the key to the foregoing diagram below. A. The minimum investment, or EB-5 capital contribution, by each individual investor is $500,000 (or $1 million if the project is not located in a target employment area (“TEA”), i.e., a rural area or a high unemployment area). Upon acceptance by a new commercial enterprise (“NCE”) of an investor’s subscription, the investor’s capital contribution is typically placed in an escrow or trust account subject to release from escrow or trust and disbursal in accordance with the applicable release conditions contained in the escrow or trust agreement. B. In addition, each investor is typically required to pay a subscription fee along with the $500,000 capital contribution to cover certain legal, marketing, and related costs and expenses associated with the I-526 Petition, most of which is likely to be used to compensate migration agents, consultants, lawyers, or other third parties. C. NCE, acting as a lender (in such capacity “EB-5 Lender”), will use the proceeds of an EB-5 offering to provide a multidraw term loan credit facility (the “EB-5 Loan”) to JCE, as a borrower (in such capacity “EB-5 Borrower”) who will draw down on the EB-5 Loan as the funds become available. Often the EB-5 regional center for the deal or its designee will act as an agent for EB-5 Lender (in such capacity “EB-5 Agent”) under the applicable loan documents. EB-5 Agent plays an important role in administering the EB-5 Loan as more fully described below. D. To evidence the EB-5 Loan, EB-5 Lender, EB-5 Agent, and EB-5 Borrower enter into various loan documents, Continued to page 30 28 EB5 INVESTORS MAGAZINE .

EB5 Coast to Coast is a family of regional centers spanning the Pacific to Atlantic Oceans. The map below shows which states currently have RC approval and which states are pending. Stephen Smith, President Direct: (509) 738-4000 Cell: (206) 214-8882 steve@stevesmithdev.com First RC approved in 2011 Ask us how to combine EB-5 with $50+ million raised from 100+ investors HUD Financing (non-recourse) 80+ I-526 petitions APPROVED (zero RFEs) LIHTCs & NMTCs 5 projects funded 18 states RC APPROVED; 14 states APPROVAL PENDING Mark Raabe, SVP/CFO (206) 396-4741 mark@stevesmithdev.com I-526 petitions APPROVED: 15 Now under construction - completion: February 2017 HUD loan APPROVED TEA - APPROVED Contact Us for Additional Information! TC Wu, Vice President (206) 849-8858 . Continued from page 28 which may include a loan agreement, promissory note, security document (covering personal and/or real property), construction draw agreement, pledge agreement, guaranty, intercreditor agreement, subordination agreement, and other ancillary loan documents as appropriate for a particular EB-5 project. The loan documents will reflect a pre-negotiated interest rate, maturity date, one or more extension periods of the maturity date, mandatory prepayment in the event of EB-5 Borrower default or I-526 denials, prohibition of voluntary prepayment except in limited cases, financial and other covenants, collateral arrangement, and other material terms of the EB-5 Loan. To secure the EB-5 Loan, EB-5 Borrower may grant EB-5 Lender a junior priority security interest in certain of its assets (personal and/or real property). This security interest will be subject to an intercreditor agreement and/or subordination agreement with one or more senior lenders of JCE. In addition, JCE’s principal(s) and affiliate(s) may also provide guarantees (i.e., completion guaranty, environmental indemnity guaranty, I-526 repayment guaranty, etc.). E. JCE often obtains several short-term financings (equity or debt) from unrelated third parties to meet the required timeline for development of its EB-5 project before EB-5 Loan disbursements commence.

The EB-5 Loan disbursements are subject to the offering, and the funds used to make the EB-5 Loan disbursements will be held in the escrow or trust account until released from escrow or trust and disbursed in accordance with the applicable release trigger conditions contained in the escrow or trust agreement. JCE may use some or all of the EB-5 Loan to repay some or all of the then outstanding amounts under these short-term financings. F. JCE typically anticipates having one or more senior lenders who are expected to extend construction and other credit facilities. The EB-5 Loan will be subordinated in right of payment to senior debt of JCE pursuant to the terms of a subordination and intercreditor agreement, and EB-5 Lender may not be permitted to enforce any rights it has under the EB-5 Loan during a period of time referred to as a “standstill period,” which can range between 90 days to 270 days.

The senior loans may demand additional conditions that may further limit EB-5 Lender’s rights. G. Using the sources of funding described above, JCE expects to fund the total project cost of its EB-5 project. JCE typically expects to repay the EB-5 Loan at maturity with the proceeds of a long-term financing, revenue from its operations, or funds from other sources, which may include the sale of the project. H. Typically, NCE is managed by its EB-5 regional center sponsor as its sole manager. The EB-5 regional center, as manager, will also act as EB-5 Agent, performing customary management services and administrative and operational 30 services for the EB-5 Loan.

The EB-5 regional center will often engage one or more funding agents or strategic partners to identify and secure potential EB-5 investors. Ideally, NCE and the EB-5 regional center will also engage a FINRA registered broker-dealer to act as a financial advisor, who will analyze the offering, conduct due diligence, offer strategic advice, and assist in negotiations and closing mechanics with respect to the offering in compliance with applicable securities laws. Structure and Terms of an EB-5 Loan Agreement A loan agreement is the primary contract between the borrower and the lender in a loan transaction that regulates the mutual promises made by each party. An EB-5 Loan can be structured as senior or junior/subordinated depending on the relative portion of the EB-5 Loan compared to the other sources of funding in the overall project financing and can be either secured or unsecured and have one or more guaranties or no guarantee. While each EB-5 project will have its own set of unique issues and complexities arising from the nature of the EB-5 Loan relative to other financings, the bargaining position of EB-5 Borrower, and numerous other factors, almost all loan agreements have similar key provisions and structures.

The summary below provides an overview of these standard provisions in the context of EB-5 financing transactions. Overview of Competing Perspectives: Lender v. Borrower For the EB-5 Lender, some of the most important considerations include whether JCE (EB-5 Borrower, or its permitted assigns and successors) will (a) create a sufficient number of qualifying jobs to comply with the EB-5 requirements to support the amount of the EB-5 Loan, (b) have sufficient funds from its operation to repay the principal sum advanced, (c) have sufficient funds from its operation to make interest payments promptly when due during the term, and (d) provide necessary financial and corporate documents for EB-5 investors as required by the USCIS to secure approval at the I-829 petition stage. Like any other borrower, EB-5 Borrower’s main concern will be whether the loan agreement is flexible, i.e., will it comply with the terms of the parties’ initial agreement without surprises, will it be practical and refrain from restricting EB-5 Borrower’s activities (e.g., through covenants and events of default) and otherwise does not interfere with EB-5 Borrower’s ability to run its business. In that regard, EB-5 Borrower will also need to make sure the terms of the EB-5 Loan do not conflict with the senior loans or equity financing contemplated for the project.

EB-5 Borrower will often attempt to, among other things: • introduce reasonableness and materiality thresholds where applicable to temper its obligations in the agreement; and • increase grace periods and introduce mitigation clauses before events of default are triggered to allow maximum flexibility. EB5 INVESTORS MAGAZINE Continued to page 32 . Continued from page 30 Definitions Capitalized defined terms are crucial in loan agreements because they are repeated throughout the loan agreement as well as other related ancillary loan documents. The first section of the loan agreement will typically define these capitalized terms used in the loan agreement. Borrowing Terms and Procedures The second section of the loan agreement will typically provide detailed procedures for borrowing, including the following: • the amount of the loan; • the time period for borrowing and procedure for loan advances (e.g., a multi-draw with a fixed availability period or based on construction draws); • the repayment of principal and accrued and unpaid interest at final maturity; • the availability of extension periods exercisable by EB-5 Borrower for an increased interest rate and/or an extension fee; and • computation of interest rate and other fees (e.g., origination fee). Conditions Precedent for Closing and/or Funding This section specifies the conditions that EB-5 Borrower must meet before EB-5 Lender will lend money under the loan agreement and is often divided into two categories: initial conditions to be satisfied before the first loan advance and conditions that apply to all advances (the first and any subsequent advances). Examples of conditions precedent relevant to the EB-5 Loan transactions include the following: • production of various documents such as corporate authorization related documents (e.g., secretarial certificates, authorizing resolutions, good standing certificates, etc.) and other ancillary loan documents, including guaranties, pledge agreements, and intercreditor agreements, as applicable; • proof of EB-5 Borrower’s receipt of other funds in the project’s capital stack before the EB-5 Loan is funded (e.g., proof of equity, tax credits, senior loan, etc.); • receipt and satisfactory review of customary due diligence documents including an appraisal, title and survey reports, lien searches and environmental reports with respect to the project; and • to the extent the EB-5 Loan is secured, evidence that the security interest in all collateral is properly perfected (e.g., through filing of applicable UCC financing statements for certain personal property and recording of mortgage, deed to secure debt, or deed of trust for certain real property). the payments of interest and principal (e.g., monthly, quarterly, or annually; interest only for certain period; or interest and principal installments); • for each EB-5 Loan advance under the loan agreement and (b) the date that is a few business days after the Form I-829 Petitions of all EB-5 investors are either (i) adjudicated by the USCIS or (ii) voluntarily or involuntarily abandoned or withdrawn. To structure the funding or borrowing mechanics for the EB-5 Loan transactions properly, the parties must understand precisely how and when EB-5 funds will be released from the escrow or trust account and time the EB-5 Loan disbursements under the loan agreement accordingly. In most cases, EB-5 Lender will not have the funds to disburse the entire amount of the EB-5 Loan committed under the loan agreement at the initial closing. As EB-5 Lender raises funds from EB-5 investors over time, EB-5 Lender and EB-5 Borrower will need to maintain close communication and schedule the EB-5 Loan disbursements based on the EB-5 investments then held in the escrow or trust account and applicable release triggers. For an EB-5 Lender, it will be important to negotiate a binding commitment from EB-5 Borrower to draw down on the EB-5 Loan so long as EB-5 Lender raises certain minimum amount within a reasonable time negotiated between the parties (e.g., 50 percent of the EB-5 Loan commitment within 12 to 24 months of the loan agreement date).

This is unique to EB-5 loan transactions in that EB-5 Lender has legitimate reasons to worry about EB-5 Borrower refusing to draw down on the EB-5 Loan after EB-5 Lender has incurred substantial costs in raising EB-5 funds from foreign investors and the investors have relied on EB-5 Borrower’s commitment to utilizing the full principal amount by filing their I-526 Petition with the U.S. Citizenship and Immigration Services (the “USCIS”) in advance of the full drawdown. Typically, the maturity date for the EB-5 Loan is scheduled to be the later of (a) the fifth anniversary date of the funding date It is crucial for EB-5 Lender to have a designated team or personnel to administer the EB-5 Loan and properly verify conditions precedent before funding each disbursement under the loan agreement. Representations and Warranties One of the many ways EB-5 Lenders can minimize their risks is through representations and warranties from EB-5 Borrowers. The representations and warranties section of the loan agreement allows EB-5 Lenders to: (a) gather material information about EB-5 Borrower and its operation and assets; (b) to garner the rights to monitor the business of EB-5 Borrower on an ongoing basis properly; and (c) allocate risks to hold EB-5 Borrower liable if any representation or warranty is untrue (whether or not EB-5 Borrower is at fault). While representations and warranties are fairly standard, it is important for EB-5 Borrowers to review them carefully to ensure that each provision contains suitable carve-outs and materiality thresholds wherever appropriate. Covenants Covenants are particularly relevant and important for long-term credit arrangements such as an EB-5 Loan, which will typically have a term longer than five years based on the Continued to page 34 32 EB5 INVESTORS MAGAZINE .

Continued from page 32 EB-5 program requirements. Covenants are designed to protect EB-5 Lenders’ investment during the life of the EB-5 Loan by monitoring EB-5 Borrower’s operation, restricting certain actions EB-5 Borrower can take, and requiring certain other actions to be taken. A loan covenant requires the borrower to fulfill certain conditions or forbids the borrower from undertaking certain actions. The covenants section of the loan agreement is often the most heavily negotiated between EB-5 Borrower and EB-5 Lender because EB-5 Borrower naturally wants to run its business without any interference from EB-5 Lender while EB-5 Lender has a legitimate right (and duty to protect EB-5 investors) to impose an appropriate level of constraints on EB-5 Borrower to protect its loan investment.

There are four categories of covenants commonly found in the loan agreement: • Information covenants: unaudited quarterly financial statements, audited annual financial statements, compliance certificates, notice upon occurrence of a material adverse change in EB-5 Borrower’s business • Affirmative covenants: paying taxes, maintaining insurance, permitting EB-5 Lender to inspect books and records as well as the project, making minimum capital expenditure or hiring certain number of direct full-time employees to comply with EB-5 job creation analysis • • severability, governing law, jurisdiction, waiver of jury trial, US Patriot Act and other similar regulatory requirements. Other Ancillary EB-5 Loan Documents and Important Considerations Other ancillary EB-5 Loan documents may include a promissory note, security document (covering personal and/or real property), construction draw agreement, pledge agreement, guaranty, subordination agreement and intercreditor agreement, as required by particular circumstances of an EB-5 project. However, one of the most common and critical issues relate to the perfection of securities interests in collateral, especially when dealing with EB-5 transactions secured by real property with multiple lenders and funding during construction. Rules governing security interests are very complex, and EB-5 Lenders must rely on experienced commercial finance attorneys to perfect their security interests properly under applicable law (e.g., personal property under Article 9 of the Uniform Commercial Code and real property under the real property law of applicable jurisdiction). In such instances, additional items to consider include: • Third party construction draw management • General contractor and subcontractor consents and waivers Negative covenants: requiring written consent of EB-5 Lender to incur additional debt, sell certain assets, pay dividends, pledge additional collateral, make material changes to the business plan or project, hire executive level persons, enter into material agreements, etc. • Phase I environmental report • Appraisal report • ALTA survey • Title search and lender’s policy of title insurance Financial covenants: net worth, leverage ratio, coverage ratio, minimum EBITDA • Mortgage recording tax A breach of covenant will be an event of default and trigger various remedies that EB-5 Lender may pursue (e.g., accelerating the loan or foreclosing on collateral) subject to the rights of senior lender if EB-5 Lender agreed to subordinate.

Accordingly, EB-5 Borrowers must review the covenants carefully to ensure that each provision contains suitable carve-outs or grace periods and materiality thresholds wherever appropriate to accommodate their project. Events of Defaults All loan agreements contain a section that details certain events of defaults (such as non-payment of interest or principal on the EB-5 Loan, a breach of covenant, or insolvency of EB-5 Borrower), which will allow EB-5 Lender to exercise its remedies, including acceleration of the repayment of outstanding debt, pursuing guarantors, if any, and/or enforcing its security interests, if any. However, more often than not, these remedies are subject to the rights of senior lender if EB-5 Lender agreed to subordinate, as discussed herein. Conclusion By now, almost everyone in the EB-5 industry has developed an appreciation for, or at the very least, an acceptance of, the need for well-planned securities offering materials and EB-5 compliant business plan and economic impact analysis. EB-5 project teams should give equal consideration to carefully evaluating the EB-5 financing structures and negotiating appropriate loan documents with EB-5 Borrowers.

Before finalizing the loan terms, it is also very important to discuss the proposed loan structure with target funding agents to understand whether it would be acceptable to their EB-5 investors and what additional terms or conditions, if any, may be required to be marketable. ★ Miscellaneous Provisions The last section of all loan agreements will include certain boilerplate provisions to cover notices, integration, counterpart, 34 Steve Park EB5 INVESTORS MAGAZINE Steve Park is a securities attorney and a partner at Ballard Spahr LLP, in Atlanta, Ga. Park is fluent in Korean, and focuses his practice on corporate, securities and finance law. His emphasis is on corporate governance, corporate finance, compliance with SEC regulations, private and public securities offerings and the requirements of reporting.

Park regularly works on commercial lending transactions with lenders and borrowers involved in EB-5 financing matters. .