Description

What You Need to Know –

Changes in Financial Accounting Standards: 2015

. What You Need to Know – Changes in Financial Accounting Standards: 2015

Table of Contents

OVERVIEW ............................................................................................................................................................. 3

ACCOUNTING STANDARDS UPDATES ..................................................................................................................... 3

OPTIONAL PRIVATE COMPANY ACCOUNTING ALTERNATIVES.................................................................................................14

INDUSTRY-SPECIFIC FINAL & PROPOSED ACCOUNTING STANDARDS UPDATES ..........................................................................17

PROPOSED ACCOUNTING STANDARDS UPDATES – EXPOSURE DRAFTS ....................................................................................19

AGENDA ITEMS .................................................................................................................................................... 25

RESEARCH PROJECTS .....................................................................................................................................................27

CONCLUSION .......................................................................................................................................................

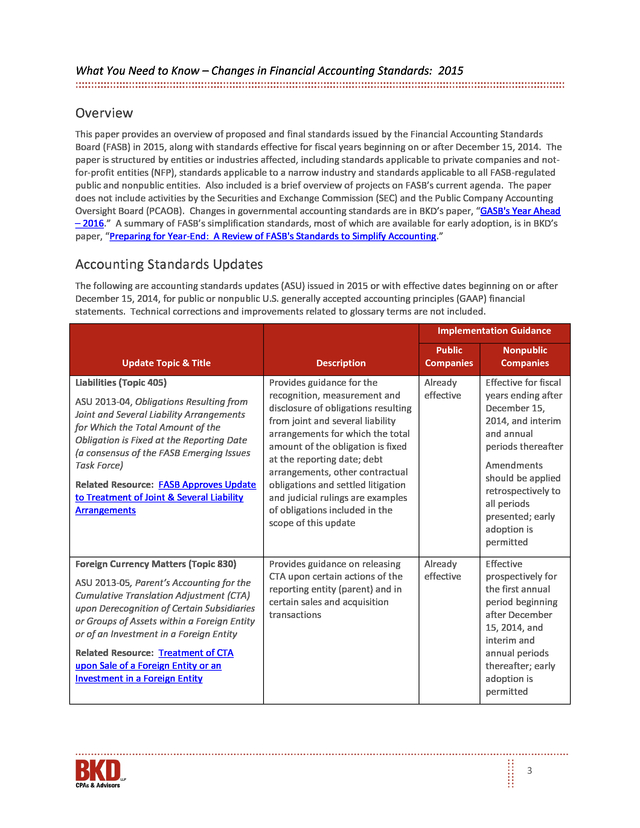

27 CONTRIBUTOR ..................................................................................................................................................... 27 2 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Overview This paper provides an overview of proposed and final standards issued by the Financial Accounting Standards Board (FASB) in 2015, along with standards effective for fiscal years beginning on or after December 15, 2014. The paper is structured by entities or industries affected, including standards applicable to private companies and notfor-profit entities (NFP), standards applicable to a narrow industry and standards applicable to all FASB-regulated public and nonpublic entities. Also included is a brief overview of projects on FASB’s current agenda. The paper does not include activities by the Securities and Exchange Commission (SEC) and the Public Company Accounting Oversight Board (PCAOB).

Changes in governmental accounting standards are in BKD’s paper, “GASB's Year Ahead – 2016.” A summary of FASB’s simplification standards, most of which are available for early adoption, is in BKD’s paper, “Preparing for Year-End: A Review of FASB's Standards to Simplify Accounting.” Accounting Standards Updates The following are accounting standards updates (ASU) issued in 2015 or with effective dates beginning on or after December 15, 2014, for public or nonpublic U.S. generally accepted accounting principles (GAAP) financial statements. Technical corrections and improvements related to glossary terms are not included. Implementation Guidance Update Topic & Title Liabilities (Topic 405) ASU 2013-04, Obligations Resulting from Joint and Several Liability Arrangements for Which the Total Amount of the Obligation is Fixed at the Reporting Date (a consensus of the FASB Emerging Issues Task Force) Related Resource: FASB Approves Update to Treatment of Joint & Several Liability Arrangements Foreign Currency Matters (Topic 830) ASU 2013-05, Parent’s Accounting for the Cumulative Translation Adjustment (CTA) upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity Related Resource: Treatment of CTA upon Sale of a Foreign Entity or an Investment in a Foreign Entity Description Public Companies Provides guidance for the recognition, measurement and disclosure of obligations resulting from joint and several liability arrangements for which the total amount of the obligation is fixed at the reporting date; debt arrangements, other contractual obligations and settled litigation and judicial rulings are examples of obligations included in the scope of this update Already effective Provides guidance on releasing CTA upon certain actions of the reporting entity (parent) and in certain sales and acquisition transactions Already effective Nonpublic Companies Effective for fiscal years ending after December 15, 2014, and interim and annual periods thereafter Amendments should be applied retrospectively to all periods presented; early adoption is permitted Effective prospectively for the first annual period beginning after December 15, 2014, and interim and annual periods thereafter; early adoption is permitted 3 .

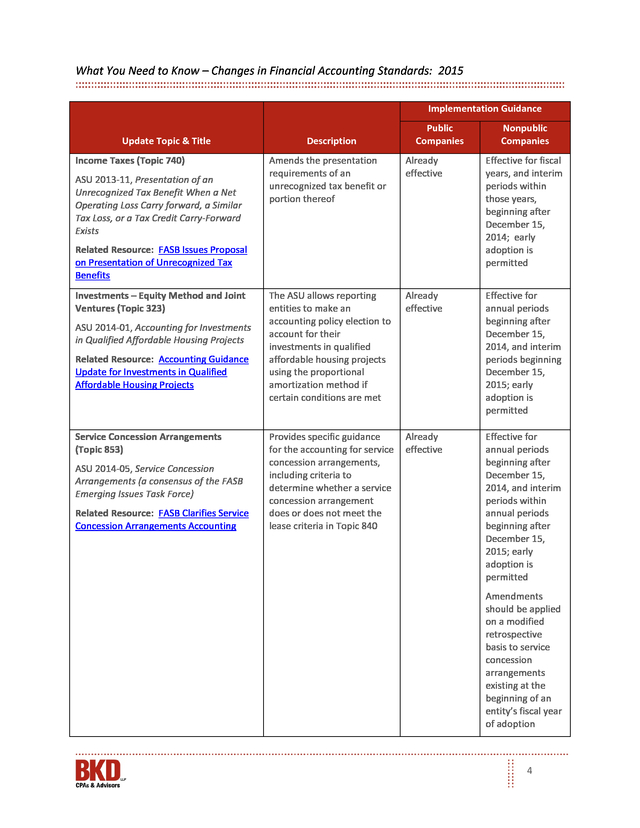

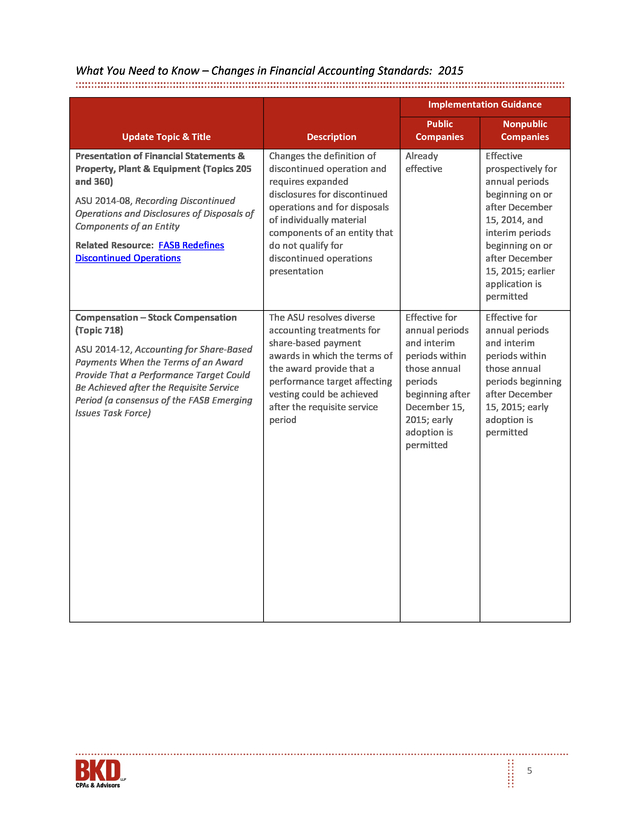

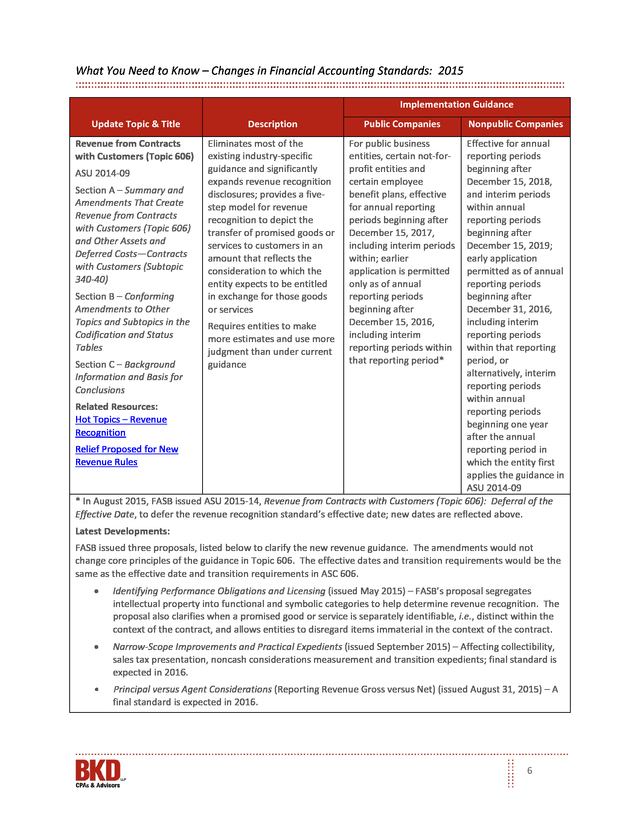

What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Income Taxes (Topic 740) ASU 2013-11, Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carry forward, a Similar Tax Loss, or a Tax Credit Carry-Forward Exists Description Public Companies Amends the presentation requirements of an unrecognized tax benefit or portion thereof Already effective Effective for fiscal years, and interim periods within those years, beginning after December 15, 2014; early adoption is permitted The ASU allows reporting entities to make an accounting policy election to account for their investments in qualified affordable housing projects using the proportional amortization method if certain conditions are met Already effective Effective for annual periods beginning after December 15, 2014, and interim periods beginning December 15, 2015; early adoption is permitted Provides specific guidance for the accounting for service concession arrangements, including criteria to determine whether a service concession arrangement does or does not meet the lease criteria in Topic 840 Already effective Effective for annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015; early adoption is permitted Related Resource: FASB Issues Proposal on Presentation of Unrecognized Tax Benefits Investments – Equity Method and Joint Ventures (Topic 323) ASU 2014-01, Accounting for Investments in Qualified Affordable Housing Projects Related Resource: Accounting Guidance Update for Investments in Qualified Affordable Housing Projects Service Concession Arrangements (Topic 853) ASU 2014-05, Service Concession Arrangements (a consensus of the FASB Emerging Issues Task Force) Related Resource: FASB Clarifies Service Concession Arrangements Accounting Nonpublic Companies Amendments should be applied on a modified retrospective basis to service concession arrangements existing at the beginning of an entity’s fiscal year of adoption 4 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Public Companies Nonpublic Companies Update Topic & Title Description Presentation of Financial Statements & Property, Plant & Equipment (Topics 205 and 360) Changes the definition of discontinued operation and requires expanded disclosures for discontinued operations and for disposals of individually material components of an entity that do not qualify for discontinued operations presentation Already effective Effective prospectively for annual periods beginning on or after December 15, 2014, and interim periods beginning on or after December 15, 2015; earlier application is permitted The ASU resolves diverse accounting treatments for share-based payment awards in which the terms of the award provide that a performance target affecting vesting could be achieved after the requisite service period Effective for annual periods and interim periods within those annual periods beginning after December 15, 2015; early adoption is permitted Effective for annual periods and interim periods within those annual periods beginning after December 15, 2015; early adoption is permitted ASU 2014-08, Recording Discontinued Operations and Disclosures of Disposals of Components of an Entity Related Resource: FASB Redefines Discontinued Operations Compensation – Stock Compensation (Topic 718) ASU 2014-12, Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period (a consensus of the FASB Emerging Issues Task Force) 5 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Description Public Companies Revenue from Contracts with Customers (Topic 606) Eliminates most of the existing industry-specific guidance and significantly expands revenue recognition disclosures; provides a fivestep model for revenue recognition to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services Nonpublic Companies For public business entities, certain not-forprofit entities and certain employee benefit plans, effective for annual reporting periods beginning after December 15, 2017, including interim periods within; earlier application is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period* Effective for annual reporting periods beginning after ASU 2014-09 December 15, 2018, Section A – Summary and and interim periods Amendments That Create within annual Revenue from Contracts reporting periods with Customers (Topic 606) beginning after and Other Assets and December 15, 2019; Deferred Costs—Contracts early application with Customers (Subtopic permitted as of annual 340-40) reporting periods Section B – Conforming beginning after Amendments to Other December 31, 2016, Topics and Subtopics in the including interim Requires entities to make Codification and Status reporting periods more estimates and use more Tables within that reporting judgment than under current period, or Section C – Background guidance alternatively, interim Information and Basis for reporting periods Conclusions within annual Related Resources: reporting periods Hot Topics – Revenue beginning one year Recognition after the annual Relief Proposed for New reporting period in Revenue Rules which the entity first applies the guidance in ASU 2014-09 * In August 2015, FASB issued ASU 2015-14, Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date, to defer the revenue recognition standard’s effective date; new dates are reflected above. Latest Developments: FASB issued three proposals, listed below to clarify the new revenue guidance. The amendments would not change core principles of the guidance in Topic 606. The effective dates and transition requirements would be the same as the effective date and transition requirements in ASC 606. • Identifying Performance Obligations and Licensing (issued May 2015) – FASB’s proposal segregates intellectual property into functional and symbolic categories to help determine revenue recognition. The proposal also clarifies when a promised good or service is separately identifiable, i.e., distinct within the context of the contract, and allows entities to disregard items immaterial in the context of the contract. • Narrow-Scope Improvements and Practical Expedients (issued September 2015) – Affecting collectibility, sales tax presentation, noncash considerations measurement and transition expedients; final standard is expected in 2016. • Principal versus Agent Considerations (Reporting Revenue Gross versus Net) (issued August 31, 2015) – A final standard is expected in 2016. 6 .

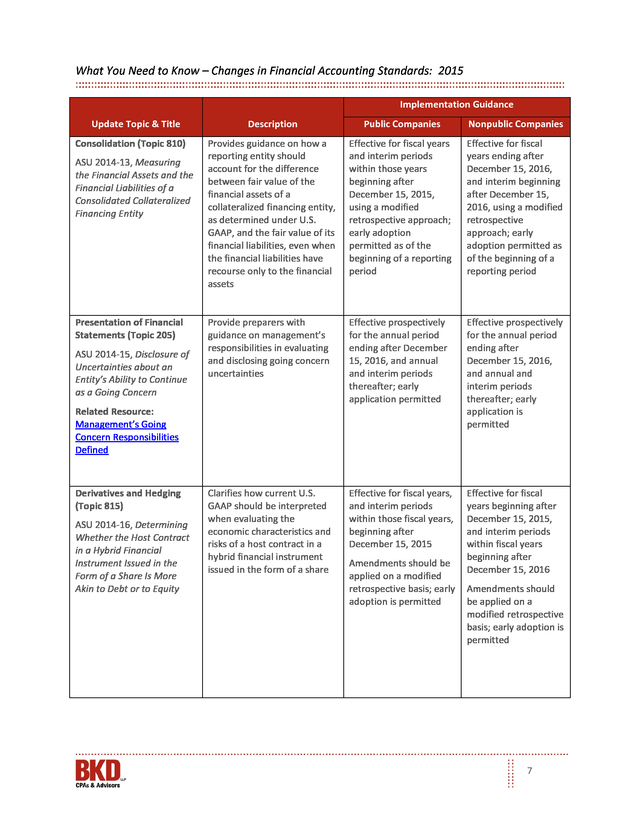

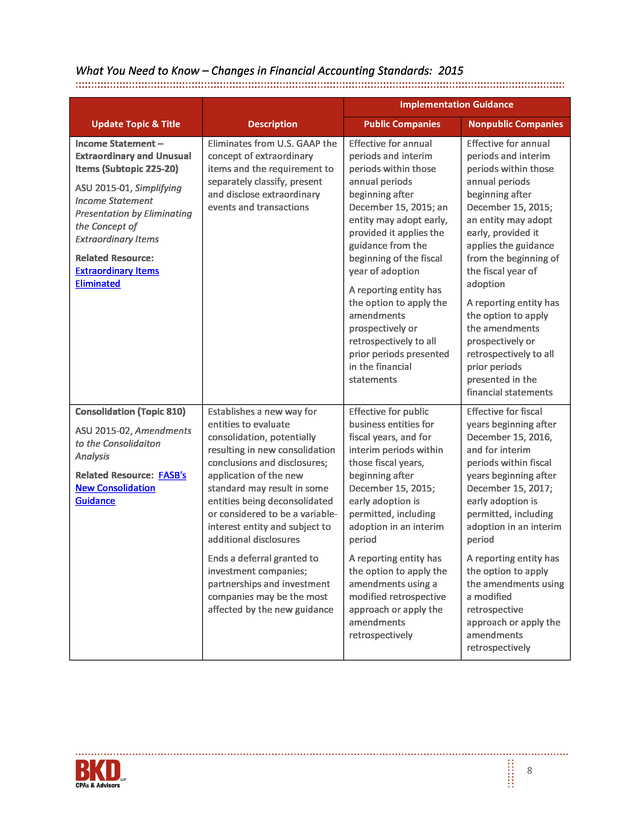

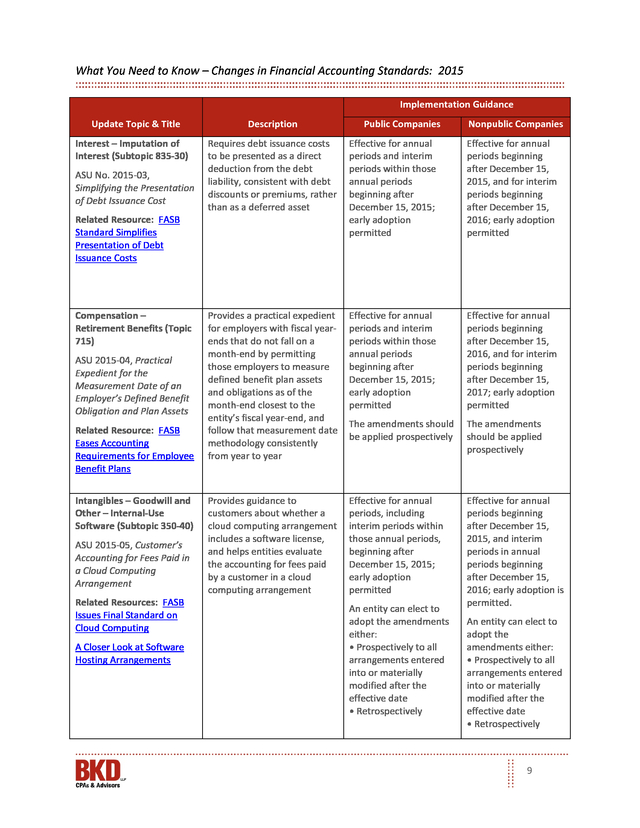

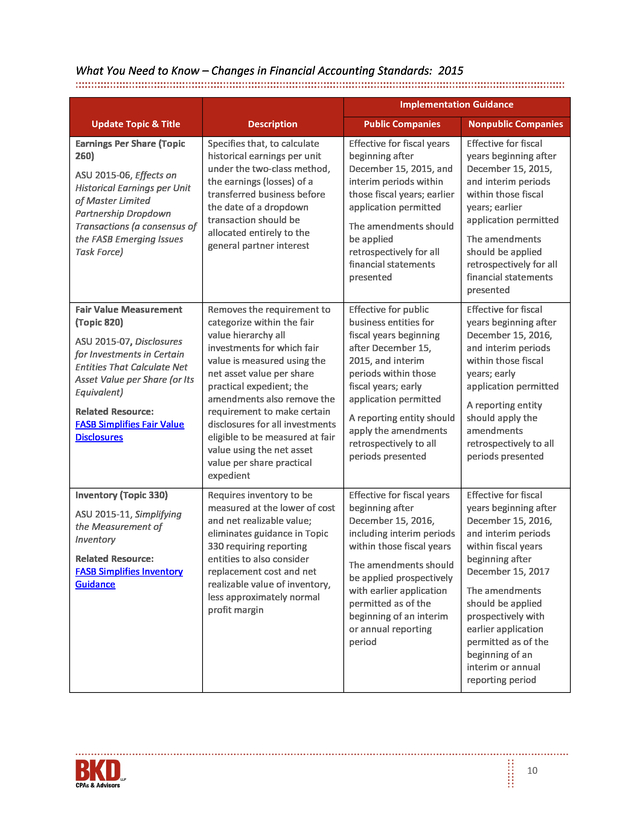

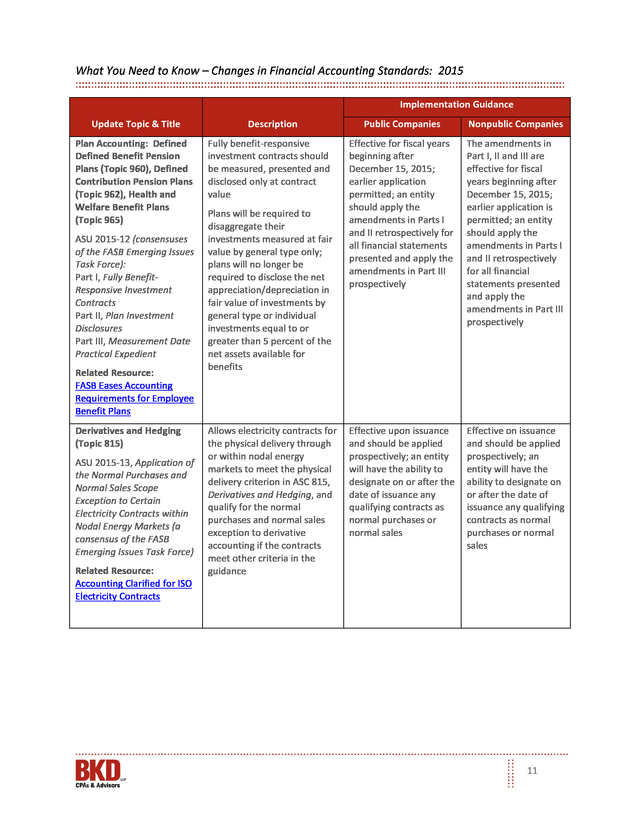

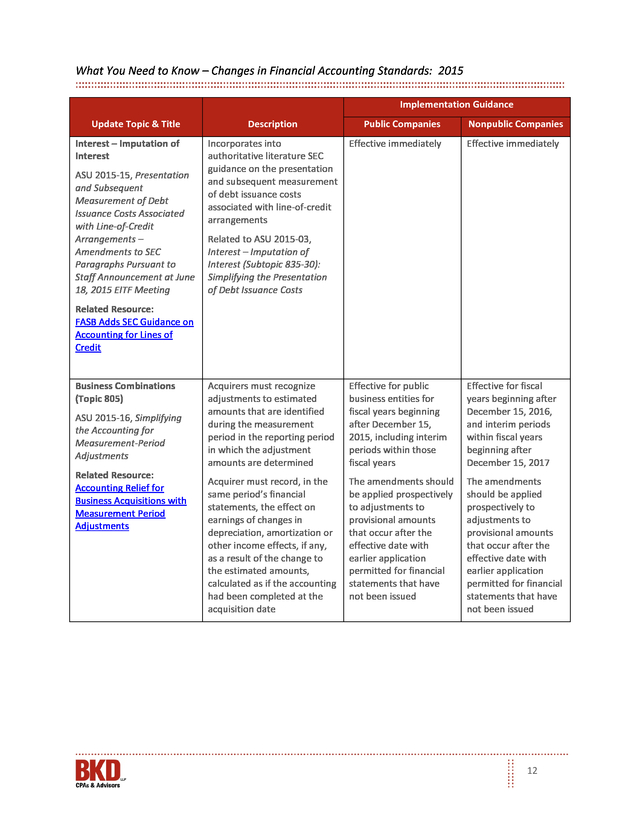

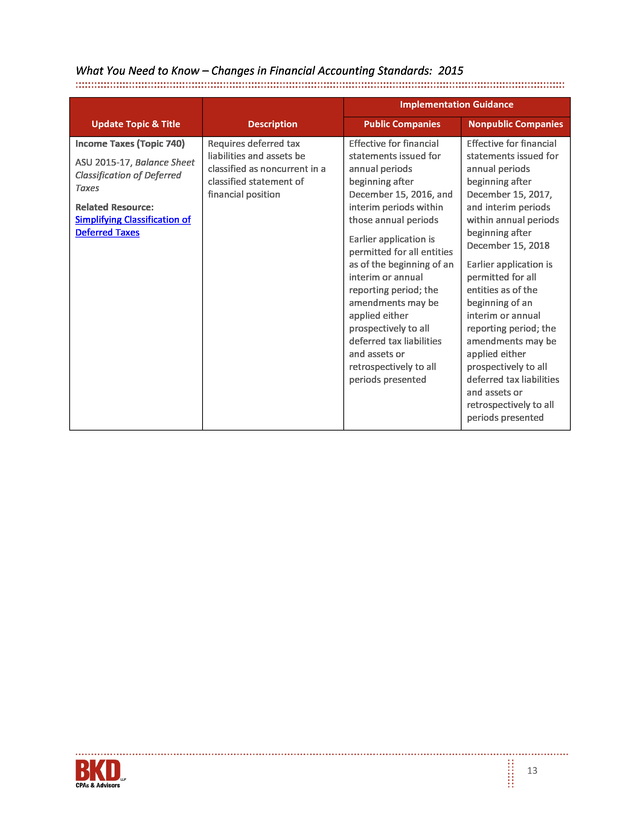

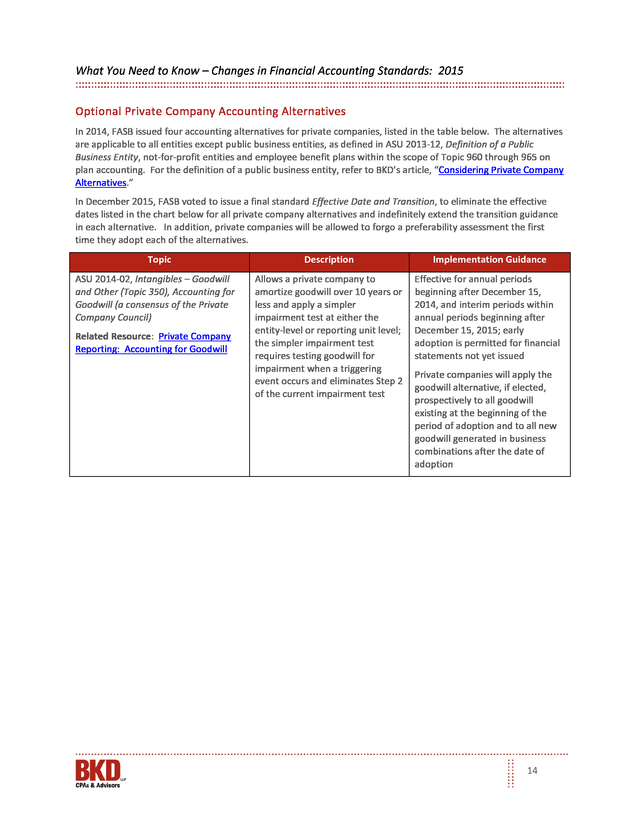

What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Consolidation (Topic 810) ASU 2014-13, Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity Presentation of Financial Statements (Topic 205) ASU 2014-15, Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern Description Public Companies Nonpublic Companies Provides guidance on how a reporting entity should account for the difference between fair value of the financial assets of a collateralized financing entity, as determined under U.S. GAAP, and the fair value of its financial liabilities, even when the financial liabilities have recourse only to the financial assets Effective for fiscal years and interim periods within those years beginning after December 15, 2015, using a modified retrospective approach; early adoption permitted as of the beginning of a reporting period Effective for fiscal years ending after December 15, 2016, and interim beginning after December 15, 2016, using a modified retrospective approach; early adoption permitted as of the beginning of a reporting period Provide preparers with guidance on management’s responsibilities in evaluating and disclosing going concern uncertainties Effective prospectively for the annual period ending after December 15, 2016, and annual and interim periods thereafter; early application permitted Effective prospectively for the annual period ending after December 15, 2016, and annual and interim periods thereafter; early application is permitted Clarifies how current U.S. GAAP should be interpreted when evaluating the economic characteristics and risks of a host contract in a hybrid financial instrument issued in the form of a share Effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015 Effective for fiscal years beginning after December 15, 2015, and interim periods within fiscal years beginning after December 15, 2016 Related Resource: Management’s Going Concern Responsibilities Defined Derivatives and Hedging (Topic 815) ASU 2014-16, Determining Whether the Host Contract in a Hybrid Financial Instrument Issued in the Form of a Share Is More Akin to Debt or to Equity Amendments should be applied on a modified retrospective basis; early adoption is permitted Amendments should be applied on a modified retrospective basis; early adoption is permitted 7 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Description Income Statement – Extraordinary and Unusual Items (Subtopic 225-20) Eliminates from U.S. GAAP the concept of extraordinary items and the requirement to separately classify, present and disclose extraordinary events and transactions ASU 2015-01, Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items Related Resource: Extraordinary Items Eliminated Consolidation (Topic 810) ASU 2015-02, Amendments to the Consolidaiton Analysis Related Resource: FASB's New Consolidation Guidance Public Companies Effective for annual periods and interim periods within those annual periods beginning after December 15, 2015; an entity may adopt early, provided it applies the guidance from the beginning of the fiscal year of adoption A reporting entity has the option to apply the amendments prospectively or retrospectively to all prior periods presented in the financial statements Nonpublic Companies Effective for annual periods and interim periods within those annual periods beginning after December 15, 2015; an entity may adopt early, provided it applies the guidance from the beginning of the fiscal year of adoption A reporting entity has the option to apply the amendments prospectively or retrospectively to all prior periods presented in the financial statements Establishes a new way for entities to evaluate consolidation, potentially resulting in new consolidation conclusions and disclosures; application of the new standard may result in some entities being deconsolidated or considered to be a variableinterest entity and subject to additional disclosures Effective for public business entities for fiscal years, and for interim periods within those fiscal years, beginning after December 15, 2015; early adoption is permitted, including adoption in an interim period Effective for fiscal years beginning after December 15, 2016, and for interim periods within fiscal years beginning after December 15, 2017; early adoption is permitted, including adoption in an interim period Ends a deferral granted to investment companies; partnerships and investment companies may be the most affected by the new guidance A reporting entity has the option to apply the amendments using a modified retrospective approach or apply the amendments retrospectively A reporting entity has the option to apply the amendments using a modified retrospective approach or apply the amendments retrospectively 8 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Interest – Imputation of Interest (Subtopic 835-30) ASU No. 2015-03, Simplifying the Presentation of Debt Issuance Cost Related Resource: FASB Standard Simplifies Presentation of Debt Issuance Costs Compensation – Retirement Benefits (Topic 715) ASU 2015-04, Practical Expedient for the Measurement Date of an Employer’s Defined Benefit Obligation and Plan Assets Related Resource: FASB Eases Accounting Requirements for Employee Benefit Plans Intangibles – Goodwill and Other – Internal-Use Software (Subtopic 350-40) ASU 2015-05, Customer’s Accounting for Fees Paid in a Cloud Computing Arrangement Related Resources: FASB Issues Final Standard on Cloud Computing A Closer Look at Software Hosting Arrangements Description Public Companies Nonpublic Companies Requires debt issuance costs to be presented as a direct deduction from the debt liability, consistent with debt discounts or premiums, rather than as a deferred asset Effective for annual periods and interim periods within those annual periods beginning after December 15, 2015; early adoption permitted Effective for annual periods beginning after December 15, 2015, and for interim periods beginning after December 15, 2016; early adoption permitted Provides a practical expedient for employers with fiscal yearends that do not fall on a month-end by permitting those employers to measure defined benefit plan assets and obligations as of the month-end closest to the entity’s fiscal year-end, and follow that measurement date methodology consistently from year to year Effective for annual periods and interim periods within those annual periods beginning after December 15, 2015; early adoption permitted Effective for annual periods beginning after December 15, 2016, and for interim periods beginning after December 15, 2017; early adoption permitted The amendments should be applied prospectively The amendments should be applied prospectively Provides guidance to customers about whether a cloud computing arrangement includes a software license, and helps entities evaluate the accounting for fees paid by a customer in a cloud computing arrangement Effective for annual periods, including interim periods within those annual periods, beginning after December 15, 2015; early adoption permitted Effective for annual periods beginning after December 15, 2015, and interim periods in annual periods beginning after December 15, 2016; early adoption is permitted. An entity can elect to adopt the amendments either: • Prospectively to all arrangements entered into or materially modified after the effective date • Retrospectively An entity can elect to adopt the amendments either: • Prospectively to all arrangements entered into or materially modified after the effective date • Retrospectively 9 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Earnings Per Share (Topic 260) ASU 2015-06, Effects on Historical Earnings per Unit of Master Limited Partnership Dropdown Transactions (a consensus of the FASB Emerging Issues Task Force) Fair Value Measurement (Topic 820) ASU 2015-07, Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent) Related Resource: FASB Simplifies Fair Value Disclosures Inventory (Topic 330) ASU 2015-11, Simplifying the Measurement of Inventory Related Resource: FASB Simplifies Inventory Guidance Description Public Companies Nonpublic Companies Specifies that, to calculate historical earnings per unit under the two-class method, the earnings (losses) of a transferred business before the date of a dropdown transaction should be allocated entirely to the general partner interest Effective for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years; earlier application permitted Effective for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years; earlier application permitted Removes the requirement to categorize within the fair value hierarchy all investments for which fair value is measured using the net asset value per share practical expedient; the amendments also remove the requirement to make certain disclosures for all investments eligible to be measured at fair value using the net asset value per share practical expedient Effective for public business entities for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years; early application permitted Requires inventory to be measured at the lower of cost and net realizable value; eliminates guidance in Topic 330 requiring reporting entities to also consider replacement cost and net realizable value of inventory, less approximately normal profit margin Effective for fiscal years beginning after December 15, 2016, including interim periods within those fiscal years The amendments should be applied retrospectively for all financial statements presented A reporting entity should apply the amendments retrospectively to all periods presented The amendments should be applied prospectively with earlier application permitted as of the beginning of an interim or annual reporting period The amendments should be applied retrospectively for all financial statements presented Effective for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years; early application permitted A reporting entity should apply the amendments retrospectively to all periods presented Effective for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017 The amendments should be applied prospectively with earlier application permitted as of the beginning of an interim or annual reporting period 10 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Plan Accounting: Defined Defined Benefit Pension Plans (Topic 960), Defined Contribution Pension Plans (Topic 962), Health and Welfare Benefit Plans (Topic 965) ASU 2015-12 (consensuses of the FASB Emerging Issues Task Force): Part I, Fully BenefitResponsive Investment Contracts Part II, Plan Investment Disclosures Part III, Measurement Date Practical Expedient Related Resource: FASB Eases Accounting Requirements for Employee Benefit Plans Derivatives and Hedging (Topic 815) ASU 2015-13, Application of the Normal Purchases and Normal Sales Scope Exception to Certain Electricity Contracts within Nodal Energy Markets (a consensus of the FASB Emerging Issues Task Force) Related Resource: Accounting Clarified for ISO Electricity Contracts Description Fully benefit-responsive investment contracts should be measured, presented and disclosed only at contract value Plans will be required to disaggregate their investments measured at fair value by general type only; plans will no longer be required to disclose the net appreciation/depreciation in fair value of investments by general type or individual investments equal to or greater than 5 percent of the net assets available for benefits Allows electricity contracts for the physical delivery through or within nodal energy markets to meet the physical delivery criterion in ASC 815, Derivatives and Hedging, and qualify for the normal purchases and normal sales exception to derivative accounting if the contracts meet other criteria in the guidance Public Companies Nonpublic Companies Effective for fiscal years beginning after December 15, 2015; earlier application permitted; an entity should apply the amendments in Parts I and II retrospectively for all financial statements presented and apply the amendments in Part III prospectively The amendments in Part I, II and III are effective for fiscal years beginning after December 15, 2015; earlier application is permitted; an entity should apply the amendments in Parts I and II retrospectively for all financial statements presented and apply the amendments in Part III prospectively Effective upon issuance and should be applied prospectively; an entity will have the ability to designate on or after the date of issuance any qualifying contracts as normal purchases or normal sales Effective on issuance and should be applied prospectively; an entity will have the ability to designate on or after the date of issuance any qualifying contracts as normal purchases or normal sales 11 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Interest – Imputation of Interest ASU 2015-15, Presentation and Subsequent Measurement of Debt Issuance Costs Associated with Line-of-Credit Arrangements – Amendments to SEC Paragraphs Pursuant to Staff Announcement at June 18, 2015 EITF Meeting Description Incorporates into authoritative literature SEC guidance on the presentation and subsequent measurement of debt issuance costs associated with line-of-credit arrangements Public Companies Nonpublic Companies Effective immediately Effective immediately Acquirers must recognize adjustments to estimated amounts that are identified during the measurement period in the reporting period in which the adjustment amounts are determined Effective for public business entities for fiscal years beginning after December 15, 2015, including interim periods within those fiscal years Effective for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017 Acquirer must record, in the same period’s financial statements, the effect on earnings of changes in depreciation, amortization or other income effects, if any, as a result of the change to the estimated amounts, calculated as if the accounting had been completed at the acquisition date The amendments should be applied prospectively to adjustments to provisional amounts that occur after the effective date with earlier application permitted for financial statements that have not been issued The amendments should be applied prospectively to adjustments to provisional amounts that occur after the effective date with earlier application permitted for financial statements that have not been issued Related to ASU 2015-03, Interest – Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs Related Resource: FASB Adds SEC Guidance on Accounting for Lines of Credit Business Combinations (Topic 805) ASU 2015-16, Simplifying the Accounting for Measurement-Period Adjustments Related Resource: Accounting Relief for Business Acquisitions with Measurement Period Adjustments 12 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Income Taxes (Topic 740) ASU 2015-17, Balance Sheet Classification of Deferred Taxes Related Resource: Simplifying Classification of Deferred Taxes Description Requires deferred tax liabilities and assets be classified as noncurrent in a classified statement of financial position Public Companies Nonpublic Companies Effective for financial statements issued for annual periods beginning after December 15, 2016, and interim periods within those annual periods Effective for financial statements issued for annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018 Earlier application is permitted for all entities as of the beginning of an interim or annual reporting period; the amendments may be applied either prospectively to all deferred tax liabilities and assets or retrospectively to all periods presented Earlier application is permitted for all entities as of the beginning of an interim or annual reporting period; the amendments may be applied either prospectively to all deferred tax liabilities and assets or retrospectively to all periods presented 13 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Optional Private Company Accounting Alternatives In 2014, FASB issued four accounting alternatives for private companies, listed in the table below. The alternatives are applicable to all entities except public business entities, as defined in ASU 2013-12, Definition of a Public Business Entity, not-for-profit entities and employee benefit plans within the scope of Topic 960 through 965 on plan accounting. For the definition of a public business entity, refer to BKD’s article, “Considering Private Company Alternatives.” In December 2015, FASB voted to issue a final standard Effective Date and Transition, to eliminate the effective dates listed in the chart below for all private company alternatives and indefinitely extend the transition guidance in each alternative. In addition, private companies will be allowed to forgo a preferability assessment the first time they adopt each of the alternatives. Topic ASU 2014-02, Intangibles – Goodwill and Other (Topic 350), Accounting for Goodwill (a consensus of the Private Company Council) Related Resource: Private Company Reporting: Accounting for Goodwill Description Implementation Guidance Allows a private company to amortize goodwill over 10 years or less and apply a simpler impairment test at either the entity-level or reporting unit level; the simpler impairment test requires testing goodwill for impairment when a triggering event occurs and eliminates Step 2 of the current impairment test Effective for annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015; early adoption is permitted for financial statements not yet issued Private companies will apply the goodwill alternative, if elected, prospectively to all goodwill existing at the beginning of the period of adoption and to all new goodwill generated in business combinations after the date of adoption 14 .

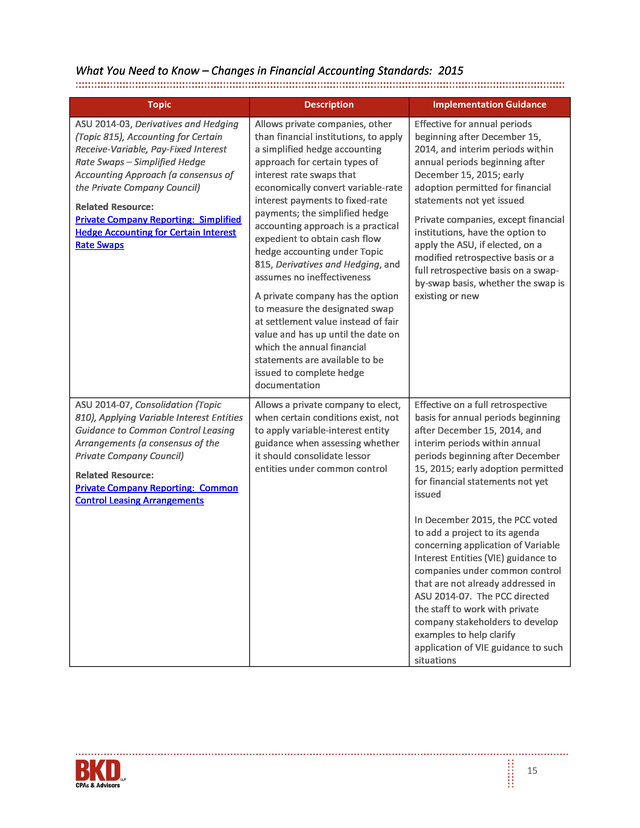

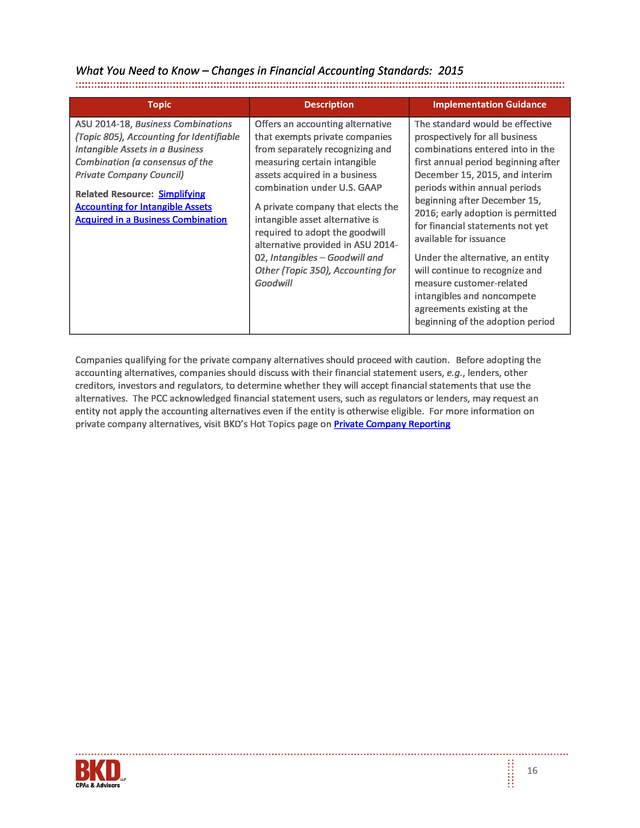

What You Need to Know – Changes in Financial Accounting Standards: 2015 Topic Description ASU 2014-03, Derivatives and Hedging (Topic 815), Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps – Simplified Hedge Accounting Approach (a consensus of the Private Company Council) Allows private companies, other than financial institutions, to apply a simplified hedge accounting approach for certain types of interest rate swaps that economically convert variable-rate interest payments to fixed-rate payments; the simplified hedge accounting approach is a practical expedient to obtain cash flow hedge accounting under Topic 815, Derivatives and Hedging, and assumes no ineffectiveness Related Resource: Private Company Reporting: Simplified Hedge Accounting for Certain Interest Rate Swaps A private company has the option to measure the designated swap at settlement value instead of fair value and has up until the date on which the annual financial statements are available to be issued to complete hedge documentation ASU 2014-07, Consolidation (Topic 810), Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements (a consensus of the Private Company Council) Related Resource: Private Company Reporting: Common Control Leasing Arrangements Allows a private company to elect, when certain conditions exist, not to apply variable-interest entity guidance when assessing whether it should consolidate lessor entities under common control Implementation Guidance Effective for annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015; early adoption permitted for financial statements not yet issued Private companies, except financial institutions, have the option to apply the ASU, if elected, on a modified retrospective basis or a full retrospective basis on a swapby-swap basis, whether the swap is existing or new Effective on a full retrospective basis for annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015; early adoption permitted for financial statements not yet issued In December 2015, the PCC voted to add a project to its agenda concerning application of Variable Interest Entities (VIE) guidance to companies under common control that are not already addressed in ASU 2014-07. The PCC directed the staff to work with private company stakeholders to develop examples to help clarify application of VIE guidance to such situations 15 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Topic ASU 2014-18, Business Combinations (Topic 805), Accounting for Identifiable Intangible Assets in a Business Combination (a consensus of the Private Company Council) Related Resource: Simplifying Accounting for Intangible Assets Acquired in a Business Combination Description Offers an accounting alternative that exempts private companies from separately recognizing and measuring certain intangible assets acquired in a business combination under U.S. GAAP A private company that elects the intangible asset alternative is required to adopt the goodwill alternative provided in ASU 201402, Intangibles – Goodwill and Other (Topic 350), Accounting for Goodwill Implementation Guidance The standard would be effective prospectively for all business combinations entered into in the first annual period beginning after December 15, 2015, and interim periods within annual periods beginning after December 15, 2016; early adoption is permitted for financial statements not yet available for issuance Under the alternative, an entity will continue to recognize and measure customer-related intangibles and noncompete agreements existing at the beginning of the adoption period Companies qualifying for the private company alternatives should proceed with caution. Before adopting the accounting alternatives, companies should discuss with their financial statement users, e.g., lenders, other creditors, investors and regulators, to determine whether they will accept financial statements that use the alternatives. The PCC acknowledged financial statement users, such as regulators or lenders, may request an entity not apply the accounting alternatives even if the entity is otherwise eligible.

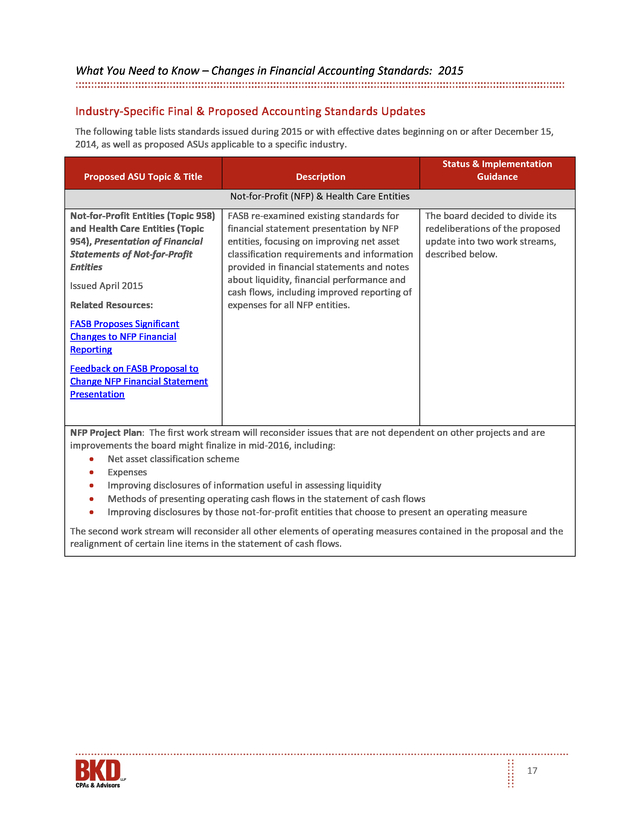

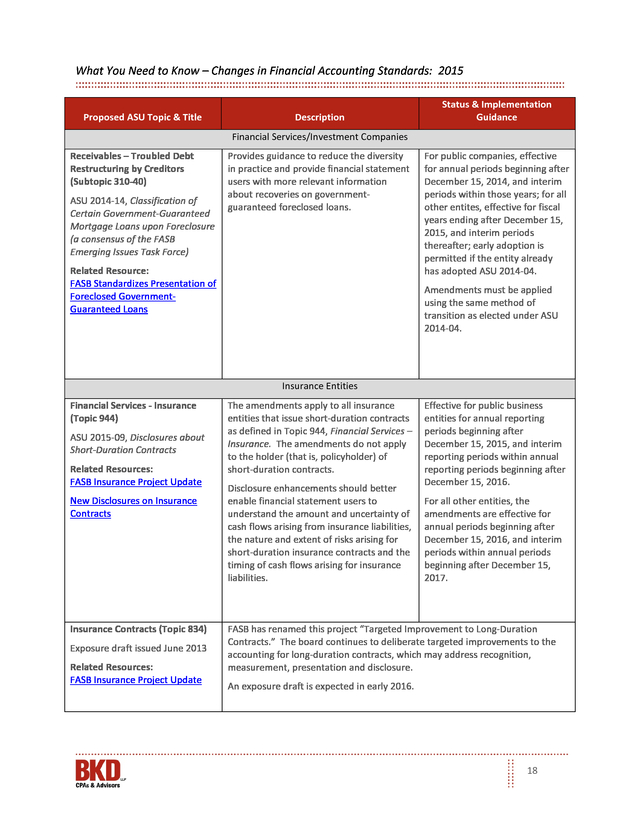

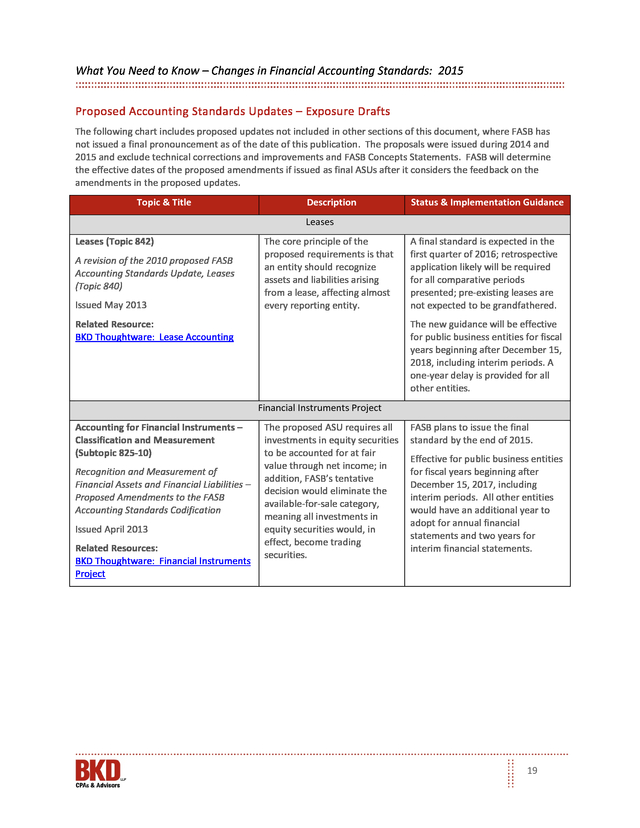

For more information on private company alternatives, visit BKD’s Hot Topics page on Private Company Reporting 16 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Industry-Specific Final & Proposed Accounting Standards Updates The following table lists standards issued during 2015 or with effective dates beginning on or after December 15, 2014, as well as proposed ASUs applicable to a specific industry. Proposed ASU Topic & Title Description Status & Implementation Guidance Not-for-Profit (NFP) & Health Care Entities Not-for-Profit Entities (Topic 958) and Health Care Entities (Topic 954), Presentation of Financial Statements of Not-for-Profit Entities Issued April 2015 Related Resources: FASB re-examined existing standards for financial statement presentation by NFP entities, focusing on improving net asset classification requirements and information provided in financial statements and notes about liquidity, financial performance and cash flows, including improved reporting of expenses for all NFP entities. The board decided to divide its redeliberations of the proposed update into two work streams, described below. FASB Proposes Significant Changes to NFP Financial Reporting Feedback on FASB Proposal to Change NFP Financial Statement Presentation NFP Project Plan: The first work stream will reconsider issues that are not dependent on other projects and are improvements the board might finalize in mid-2016, including: • Net asset classification scheme • Expenses • Improving disclosures of information useful in assessing liquidity • Methods of presenting operating cash flows in the statement of cash flows • Improving disclosures by those not-for-profit entities that choose to present an operating measure The second work stream will reconsider all other elements of operating measures contained in the proposal and the realignment of certain line items in the statement of cash flows. 17 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Proposed ASU Topic & Title Description Status & Implementation Guidance Financial Services/Investment Companies Receivables – Troubled Debt Restructuring by Creditors (Subtopic 310-40) ASU 2014-14, Classification of Certain Government-Guaranteed Mortgage Loans upon Foreclosure (a consensus of the FASB Emerging Issues Task Force) Provides guidance to reduce the diversity in practice and provide financial statement users with more relevant information about recoveries on governmentguaranteed foreclosed loans. Related Resource: FASB Standardizes Presentation of Foreclosed GovernmentGuaranteed Loans For public companies, effective for annual periods beginning after December 15, 2014, and interim periods within those years; for all other entites, effective for fiscal years ending after December 15, 2015, and interim periods thereafter; early adoption is permitted if the entity already has adopted ASU 2014-04. Amendments must be applied using the same method of transition as elected under ASU 2014-04. Insurance Entities Financial Services - Insurance (Topic 944) ASU 2015-09, Disclosures about Short-Duration Contracts Related Resources: FASB Insurance Project Update New Disclosures on Insurance Contracts Insurance Contracts (Topic 834) Exposure draft issued June 2013 Related Resources: FASB Insurance Project Update The amendments apply to all insurance entities that issue short-duration contracts as defined in Topic 944, Financial Services – Insurance. The amendments do not apply to the holder (that is, policyholder) of short-duration contracts. Disclosure enhancements should better enable financial statement users to understand the amount and uncertainty of cash flows arising from insurance liabilities, the nature and extent of risks arising for short-duration insurance contracts and the timing of cash flows arising for insurance liabilities. Effective for public business entities for annual reporting periods beginning after December 15, 2015, and interim reporting periods within annual reporting periods beginning after December 15, 2016. For all other entities, the amendments are effective for annual periods beginning after December 15, 2016, and interim periods within annual periods beginning after December 15, 2017. FASB has renamed this project “Targeted Improvement to Long-Duration Contracts.” The board continues to deliberate targeted improvements to the accounting for long-duration contracts, which may address recognition, measurement, presentation and disclosure. An exposure draft is expected in early 2016. 18 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Proposed Accounting Standards Updates – Exposure Drafts The following chart includes proposed updates not included in other sections of this document, where FASB has not issued a final pronouncement as of the date of this publication. The proposals were issued during 2014 and 2015 and exclude technical corrections and improvements and FASB Concepts Statements. FASB will determine the effective dates of the proposed amendments if issued as final ASUs after it considers the feedback on the amendments in the proposed updates. Topic & Title Description Status & Implementation Guidance Leases Leases (Topic 842) A revision of the 2010 proposed FASB Accounting Standards Update, Leases (Topic 840) Issued May 2013 The core principle of the proposed requirements is that an entity should recognize assets and liabilities arising from a lease, affecting almost every reporting entity. Related Resource: BKD Thoughtware: Lease Accounting A final standard is expected in the first quarter of 2016; retrospective application likely will be required for all comparative periods presented; pre-existing leases are not expected to be grandfathered. The new guidance will be effective for public business entities for fiscal years beginning after December 15, 2018, including interim periods. A one-year delay is provided for all other entities. Financial Instruments Project Accounting for Financial Instruments – Classification and Measurement (Subtopic 825-10) Recognition and Measurement of Financial Assets and Financial Liabilities – Proposed Amendments to the FASB Accounting Standards Codification Issued April 2013 Related Resources: BKD Thoughtware: Financial Instruments Project The proposed ASU requires all investments in equity securities to be accounted for at fair value through net income; in addition, FASB’s tentative decision would eliminate the available-for-sale category, meaning all investments in equity securities would, in effect, become trading securities. FASB plans to issue the final standard by the end of 2015. Effective for public business entities for fiscal years beginning after December 15, 2017, including interim periods.

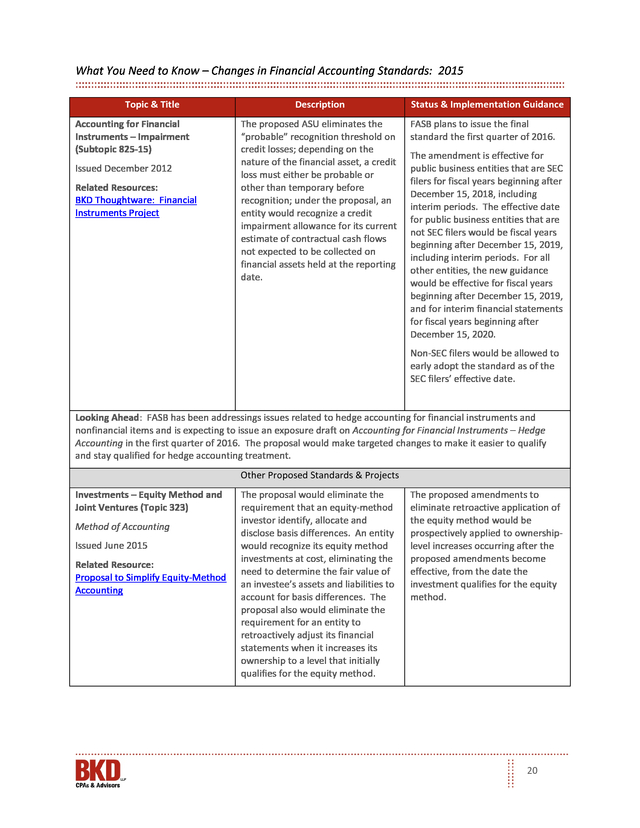

All other entities would have an additional year to adopt for annual financial statements and two years for interim financial statements. 19 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Topic & Title Accounting for Financial Instruments – Impairment (Subtopic 825-15) Issued December 2012 Related Resources: BKD Thoughtware: Financial Instruments Project Description The proposed ASU eliminates the “probable” recognition threshold on credit losses; depending on the nature of the financial asset, a credit loss must either be probable or other than temporary before recognition; under the proposal, an entity would recognize a credit impairment allowance for its current estimate of contractual cash flows not expected to be collected on financial assets held at the reporting date. Status & Implementation Guidance FASB plans to issue the final standard the first quarter of 2016. The amendment is effective for public business entities that are SEC filers for fiscal years beginning after December 15, 2018, including interim periods. The effective date for public business entities that are not SEC filers would be fiscal years beginning after December 15, 2019, including interim periods. For all other entities, the new guidance would be effective for fiscal years beginning after December 15, 2019, and for interim financial statements for fiscal years beginning after December 15, 2020. Non-SEC filers would be allowed to early adopt the standard as of the SEC filers’ effective date. Looking Ahead: FASB has been addressings issues related to hedge accounting for financial instruments and nonfinancial items and is expecting to issue an exposure draft on Accounting for Financial Instruments – Hedge Accounting in the first quarter of 2016. The proposal would make targeted changes to make it easier to qualify and stay qualified for hedge accounting treatment. Other Proposed Standards & Projects Investments – Equity Method and Joint Ventures (Topic 323) Method of Accounting Issued June 2015 Related Resource: Proposal to Simplify Equity-Method Accounting The proposal would eliminate the requirement that an equity-method investor identify, allocate and disclose basis differences.

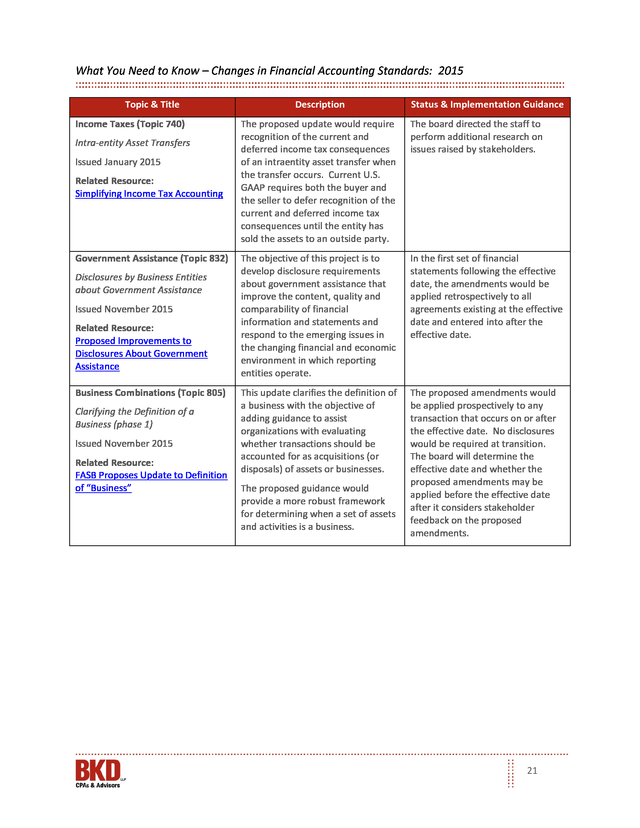

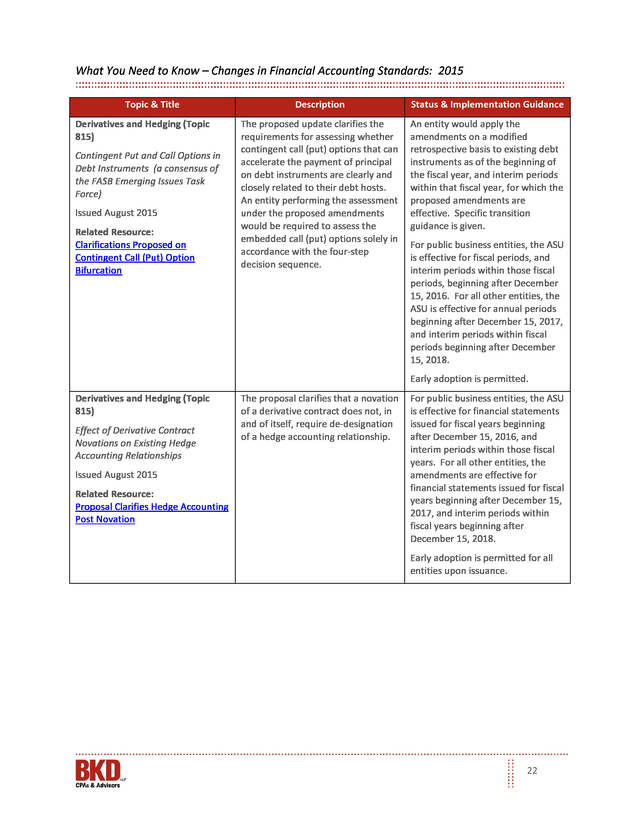

An entity would recognize its equity method investments at cost, eliminating the need to determine the fair value of an investee’s assets and liabilities to account for basis differences. The proposal also would eliminate the requirement for an entity to retroactively adjust its financial statements when it increases its ownership to a level that initially qualifies for the equity method. The proposed amendments to eliminate retroactive application of the equity method would be prospectively applied to ownershiplevel increases occurring after the proposed amendments become effective, from the date the investment qualifies for the equity method. 20 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Topic & Title Income Taxes (Topic 740) Intra-entity Asset Transfers Issued January 2015 Related Resource: Simplifying Income Tax Accounting Government Assistance (Topic 832) Disclosures by Business Entities about Government Assistance Issued November 2015 Related Resource: Proposed Improvements to Disclosures About Government Assistance Business Combinations (Topic 805) Clarifying the Definition of a Business (phase 1) Issued November 2015 Related Resource: FASB Proposes Update to Definition of “Business” Description Status & Implementation Guidance The proposed update would require recognition of the current and deferred income tax consequences of an intraentity asset transfer when the transfer occurs. Current U.S. GAAP requires both the buyer and the seller to defer recognition of the current and deferred income tax consequences until the entity has sold the assets to an outside party. The board directed the staff to perform additional research on issues raised by stakeholders. The objective of this project is to develop disclosure requirements about government assistance that improve the content, quality and comparability of financial information and statements and respond to the emerging issues in the changing financial and economic environment in which reporting entities operate. In the first set of financial statements following the effective date, the amendments would be applied retrospectively to all agreements existing at the effective date and entered into after the effective date. This update clarifies the definition of a business with the objective of adding guidance to assist organizations with evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses. The proposed amendments would be applied prospectively to any transaction that occurs on or after the effective date. No disclosures would be required at transition. The board will determine the effective date and whether the proposed amendments may be applied before the effective date after it considers stakeholder feedback on the proposed amendments. The proposed guidance would provide a more robust framework for determining when a set of assets and activities is a business. 21 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Topic & Title Derivatives and Hedging (Topic 815) Contingent Put and Call Options in Debt Instruments (a consensus of the FASB Emerging Issues Task Force) Issued August 2015 Related Resource: Clarifications Proposed on Contingent Call (Put) Option Bifurcation Description Status & Implementation Guidance The proposed update clarifies the requirements for assessing whether contingent call (put) options that can accelerate the payment of principal on debt instruments are clearly and closely related to their debt hosts. An entity performing the assessment under the proposed amendments would be required to assess the embedded call (put) options solely in accordance with the four-step decision sequence. An entity would apply the amendments on a modified retrospective basis to existing debt instruments as of the beginning of the fiscal year, and interim periods within that fiscal year, for which the proposed amendments are effective. Specific transition guidance is given. For public business entities, the ASU is effective for fiscal periods, and interim periods within those fiscal periods, beginning after December 15, 2016. For all other entities, the ASU is effective for annual periods beginning after December 15, 2017, and interim periods within fiscal periods beginning after December 15, 2018. Early adoption is permitted. Derivatives and Hedging (Topic 815) Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships Issued August 2015 Related Resource: Proposal Clarifies Hedge Accounting Post Novation The proposal clarifies that a novation of a derivative contract does not, in and of itself, require de-designation of a hedge accounting relationship. For public business entities, the ASU is effective for financial statements issued for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years. For all other entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018. Early adoption is permitted for all entities upon issuance. 22 .

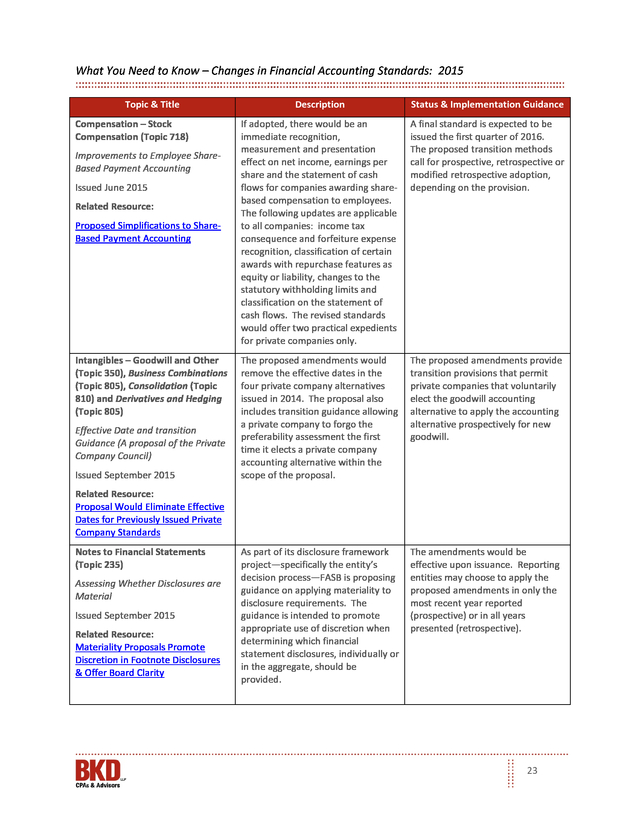

What You Need to Know – Changes in Financial Accounting Standards: 2015 Topic & Title Compensation – Stock Compensation (Topic 718) Improvements to Employee ShareBased Payment Accounting Issued June 2015 Related Resource: Proposed Simplifications to ShareBased Payment Accounting Intangibles – Goodwill and Other (Topic 350), Business Combinations (Topic 805), Consolidation (Topic 810) and Derivatives and Hedging (Topic 805) Effective Date and transition Guidance (A proposal of the Private Company Council) Issued September 2015 Description Status & Implementation Guidance If adopted, there would be an immediate recognition, measurement and presentation effect on net income, earnings per share and the statement of cash flows for companies awarding sharebased compensation to employees. The following updates are applicable to all companies: income tax consequence and forfeiture expense recognition, classification of certain awards with repurchase features as equity or liability, changes to the statutory withholding limits and classification on the statement of cash flows. The revised standards would offer two practical expedients for private companies only. A final standard is expected to be issued the first quarter of 2016. The proposed transition methods call for prospective, retrospective or modified retrospective adoption, depending on the provision. The proposed amendments would remove the effective dates in the four private company alternatives issued in 2014. The proposal also includes transition guidance allowing a private company to forgo the preferability assessment the first time it elects a private company accounting alternative within the scope of the proposal. The proposed amendments provide transition provisions that permit private companies that voluntarily elect the goodwill accounting alternative to apply the accounting alternative prospectively for new goodwill. As part of its disclosure framework project—specifically the entity’s decision process—FASB is proposing guidance on applying materiality to disclosure requirements. The guidance is intended to promote appropriate use of discretion when determining which financial statement disclosures, individually or in the aggregate, should be provided. The amendments would be effective upon issuance.

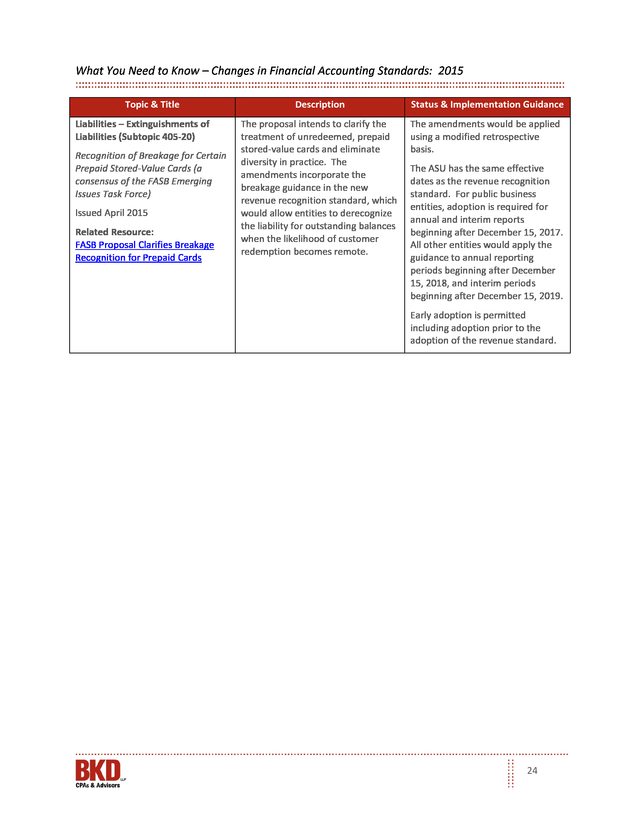

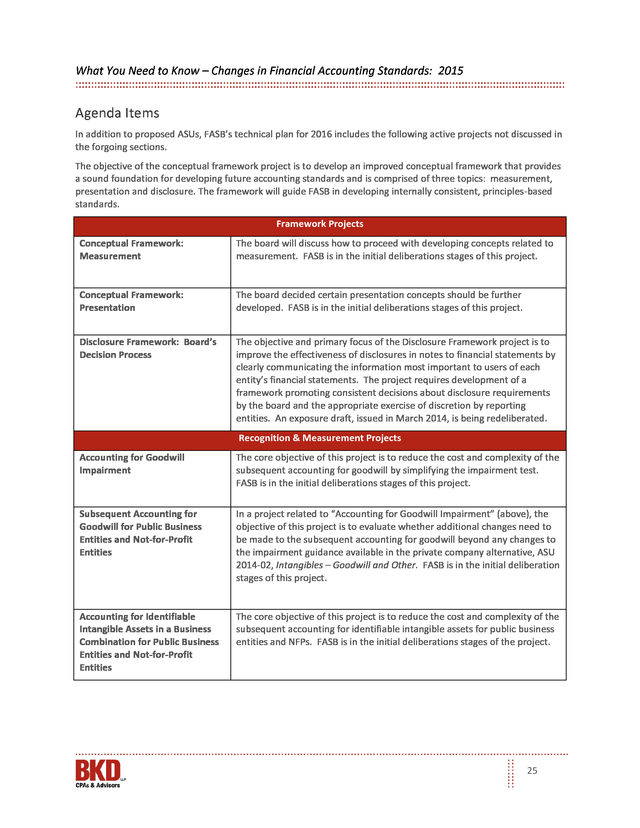

Reporting entities may choose to apply the proposed amendments in only the most recent year reported (prospective) or in all years presented (retrospective). Related Resource: Proposal Would Eliminate Effective Dates for Previously Issued Private Company Standards Notes to Financial Statements (Topic 235) Assessing Whether Disclosures are Material Issued September 2015 Related Resource: Materiality Proposals Promote Discretion in Footnote Disclosures & Offer Board Clarity 23 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Topic & Title Liabilities – Extinguishments of Liabilities (Subtopic 405-20) Recognition of Breakage for Certain Prepaid Stored-Value Cards (a consensus of the FASB Emerging Issues Task Force) Issued April 2015 Related Resource: FASB Proposal Clarifies Breakage Recognition for Prepaid Cards Description Status & Implementation Guidance The proposal intends to clarify the treatment of unredeemed, prepaid stored-value cards and eliminate diversity in practice. The amendments incorporate the breakage guidance in the new revenue recognition standard, which would allow entities to derecognize the liability for outstanding balances when the likelihood of customer redemption becomes remote. The amendments would be applied using a modified retrospective basis. The ASU has the same effective dates as the revenue recognition standard. For public business entities, adoption is required for annual and interim reports beginning after December 15, 2017. All other entities would apply the guidance to annual reporting periods beginning after December 15, 2018, and interim periods beginning after December 15, 2019. Early adoption is permitted including adoption prior to the adoption of the revenue standard. 24 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Agenda Items In addition to proposed ASUs, FASB’s technical plan for 2016 includes the following active projects not discussed in the forgoing sections. The objective of the conceptual framework project is to develop an improved conceptual framework that provides a sound foundation for developing future accounting standards and is comprised of three topics: measurement, presentation and disclosure. The framework will guide FASB in developing internally consistent, principles-based standards. Framework Projects Conceptual Framework: Measurement The board will discuss how to proceed with developing concepts related to measurement. FASB is in the initial deliberations stages of this project. Conceptual Framework: Presentation The board decided certain presentation concepts should be further developed. FASB is in the initial deliberations stages of this project. Disclosure Framework: Board’s Decision Process The objective and primary focus of the Disclosure Framework project is to improve the effectiveness of disclosures in notes to financial statements by clearly communicating the information most important to users of each entity’s financial statements.

The project requires development of a framework promoting consistent decisions about disclosure requirements by the board and the appropriate exercise of discretion by reporting entities. An exposure draft, issued in March 2014, is being redeliberated. Recognition & Measurement Projects Accounting for Goodwill Impairment The core objective of this project is to reduce the cost and complexity of the subsequent accounting for goodwill by simplifying the impairment test. FASB is in the initial deliberations stages of this project. Subsequent Accounting for Goodwill for Public Business Entities and Not-for-Profit Entities In a project related to “Accounting for Goodwill Impairment” (above), the objective of this project is to evaluate whether additional changes need to be made to the subsequent accounting for goodwill beyond any changes to the impairment guidance available in the private company alternative, ASU 2014-02, Intangibles – Goodwill and Other. FASB is in the initial deliberation stages of this project. Accounting for Identifiable Intangible Assets in a Business Combination for Public Business Entities and Not-for-Profit Entities The core objective of this project is to reduce the cost and complexity of the subsequent accounting for identifiable intangible assets for public business entities and NFPs.

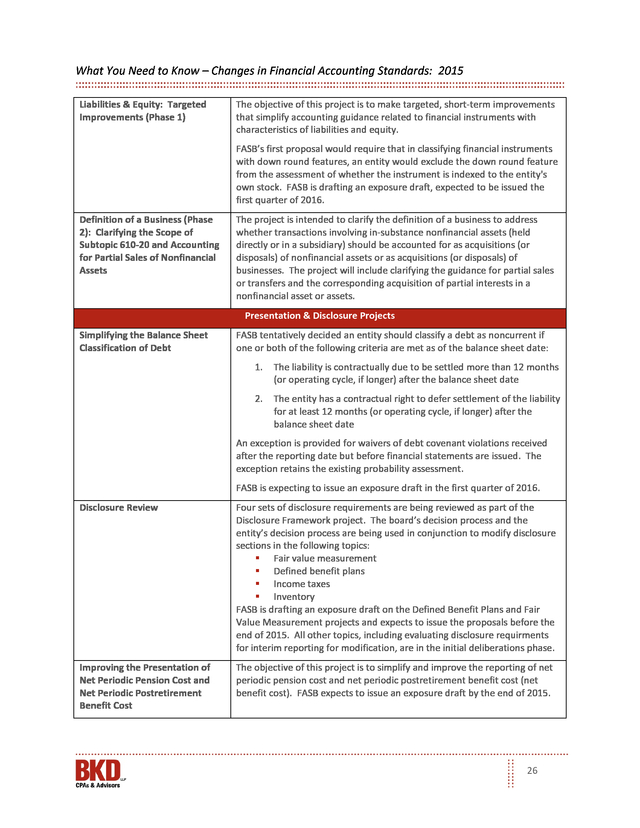

FASB is in the initial deliberations stages of the project. 25 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Liabilities & Equity: Targeted Improvements (Phase 1) The objective of this project is to make targeted, short-term improvements that simplify accounting guidance related to financial instruments with characteristics of liabilities and equity. FASB’s first proposal would require that in classifying financial instruments with down round features, an entity would exclude the down round feature from the assessment of whether the instrument is indexed to the entity's own stock. FASB is drafting an exposure draft, expected to be issued the first quarter of 2016. Definition of a Business (Phase 2): Clarifying the Scope of Subtopic 610-20 and Accounting for Partial Sales of Nonfinancial Assets The project is intended to clarify the definition of a business to address whether transactions involving in-substance nonfinancial assets (held directly or in a subsidiary) should be accounted for as acquisitions (or disposals) of nonfinancial assets or as acquisitions (or disposals) of businesses. The project will include clarifying the guidance for partial sales or transfers and the corresponding acquisition of partial interests in a nonfinancial asset or assets. Presentation & Disclosure Projects Simplifying the Balance Sheet Classification of Debt FASB tentatively decided an entity should classify a debt as noncurrent if one or both of the following criteria are met as of the balance sheet date: 1. The liability is contractually due to be settled more than 12 months (or operating cycle, if longer) after the balance sheet date 2. The entity has a contractual right to defer settlement of the liability for at least 12 months (or operating cycle, if longer) after the balance sheet date An exception is provided for waivers of debt covenant violations received after the reporting date but before financial statements are issued. The exception retains the existing probability assessment. FASB is expecting to issue an exposure draft in the first quarter of 2016. Disclosure Review Four sets of disclosure requirements are being reviewed as part of the Disclosure Framework project.

The board’s decision process and the entity’s decision process are being used in conjunction to modify disclosure sections in the following topics:  Fair value measurement  Defined benefit plans  Income taxes  Inventory FASB is drafting an exposure draft on the Defined Benefit Plans and Fair Value Measurement projects and expects to issue the proposals before the end of 2015. All other topics, including evaluating disclosure requirments for interim reporting for modification, are in the initial deliberations phase. Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost The objective of this project is to simplify and improve the reporting of net periodic pension cost and net periodic postretirement benefit cost (net benefit cost). FASB expects to issue an exposure draft by the end of 2015. 26 .

What You Need to Know – Changes in Financial Accounting Standards: 2015 Statement of Cash Flows: Classification of Certain Cash Receipts and Cash Payments (EITF 15-F) The objective of this project is to reduce diversity in practice, clarify existing principles and provide additional guidance on what an entity should consider in determining classification of certain cash flows. As part of the project, the staff will research potential additional disclosures that could result in increased relevance for users. FASB is in the initial deliberation phase of this project. Improving the Equity Method of Accounting FASB is in the initial deliberation stage of this project. Accounting for Interest Income Associated with the purchase of Callable Debt Securities FASB tentatively decided to amortize all premiums to the first call date and all discounts to the maturity date. An exposure draft is expected in early 2016. Research Projects In addition to the topics above, FASB has the following research projects on its agenda:  Accounting for Convertible Financial Instruments  Accounting for Financial Instruments: Interest Rate Risk Disclosures  Accounting for Income Taxes: Presentation of Tax Expense/Benefit  Applying Variable Interest Entity Guidance to Non-Leasing Arrangements under Common Control (PCC Research Agenda)  Financial Performance Reporting (formerly Financial Statement Presentation)  Improving Classification Guidance in the Statement of Cash Flows  Nonemployee Share-Based Payment Accounting Improvements  Partnership Accounting (PCC Research Agenda) Conclusion FASB addressed many topics in 2015. Companies are encouraged to plan for the numerous effects on company operations, compliance and financial systems and results that could be caused by upcoming GAAP changes.

If you have any questions or would like more information, contact your BKD advisor. Contributor Connie Spinelli Director 303.861.4545 cspinelli@bkd.com 27 .

27 CONTRIBUTOR ..................................................................................................................................................... 27 2 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Overview This paper provides an overview of proposed and final standards issued by the Financial Accounting Standards Board (FASB) in 2015, along with standards effective for fiscal years beginning on or after December 15, 2014. The paper is structured by entities or industries affected, including standards applicable to private companies and notfor-profit entities (NFP), standards applicable to a narrow industry and standards applicable to all FASB-regulated public and nonpublic entities. Also included is a brief overview of projects on FASB’s current agenda. The paper does not include activities by the Securities and Exchange Commission (SEC) and the Public Company Accounting Oversight Board (PCAOB).

Changes in governmental accounting standards are in BKD’s paper, “GASB's Year Ahead – 2016.” A summary of FASB’s simplification standards, most of which are available for early adoption, is in BKD’s paper, “Preparing for Year-End: A Review of FASB's Standards to Simplify Accounting.” Accounting Standards Updates The following are accounting standards updates (ASU) issued in 2015 or with effective dates beginning on or after December 15, 2014, for public or nonpublic U.S. generally accepted accounting principles (GAAP) financial statements. Technical corrections and improvements related to glossary terms are not included. Implementation Guidance Update Topic & Title Liabilities (Topic 405) ASU 2013-04, Obligations Resulting from Joint and Several Liability Arrangements for Which the Total Amount of the Obligation is Fixed at the Reporting Date (a consensus of the FASB Emerging Issues Task Force) Related Resource: FASB Approves Update to Treatment of Joint & Several Liability Arrangements Foreign Currency Matters (Topic 830) ASU 2013-05, Parent’s Accounting for the Cumulative Translation Adjustment (CTA) upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity Related Resource: Treatment of CTA upon Sale of a Foreign Entity or an Investment in a Foreign Entity Description Public Companies Provides guidance for the recognition, measurement and disclosure of obligations resulting from joint and several liability arrangements for which the total amount of the obligation is fixed at the reporting date; debt arrangements, other contractual obligations and settled litigation and judicial rulings are examples of obligations included in the scope of this update Already effective Provides guidance on releasing CTA upon certain actions of the reporting entity (parent) and in certain sales and acquisition transactions Already effective Nonpublic Companies Effective for fiscal years ending after December 15, 2014, and interim and annual periods thereafter Amendments should be applied retrospectively to all periods presented; early adoption is permitted Effective prospectively for the first annual period beginning after December 15, 2014, and interim and annual periods thereafter; early adoption is permitted 3 .

What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Income Taxes (Topic 740) ASU 2013-11, Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carry forward, a Similar Tax Loss, or a Tax Credit Carry-Forward Exists Description Public Companies Amends the presentation requirements of an unrecognized tax benefit or portion thereof Already effective Effective for fiscal years, and interim periods within those years, beginning after December 15, 2014; early adoption is permitted The ASU allows reporting entities to make an accounting policy election to account for their investments in qualified affordable housing projects using the proportional amortization method if certain conditions are met Already effective Effective for annual periods beginning after December 15, 2014, and interim periods beginning December 15, 2015; early adoption is permitted Provides specific guidance for the accounting for service concession arrangements, including criteria to determine whether a service concession arrangement does or does not meet the lease criteria in Topic 840 Already effective Effective for annual periods beginning after December 15, 2014, and interim periods within annual periods beginning after December 15, 2015; early adoption is permitted Related Resource: FASB Issues Proposal on Presentation of Unrecognized Tax Benefits Investments – Equity Method and Joint Ventures (Topic 323) ASU 2014-01, Accounting for Investments in Qualified Affordable Housing Projects Related Resource: Accounting Guidance Update for Investments in Qualified Affordable Housing Projects Service Concession Arrangements (Topic 853) ASU 2014-05, Service Concession Arrangements (a consensus of the FASB Emerging Issues Task Force) Related Resource: FASB Clarifies Service Concession Arrangements Accounting Nonpublic Companies Amendments should be applied on a modified retrospective basis to service concession arrangements existing at the beginning of an entity’s fiscal year of adoption 4 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Public Companies Nonpublic Companies Update Topic & Title Description Presentation of Financial Statements & Property, Plant & Equipment (Topics 205 and 360) Changes the definition of discontinued operation and requires expanded disclosures for discontinued operations and for disposals of individually material components of an entity that do not qualify for discontinued operations presentation Already effective Effective prospectively for annual periods beginning on or after December 15, 2014, and interim periods beginning on or after December 15, 2015; earlier application is permitted The ASU resolves diverse accounting treatments for share-based payment awards in which the terms of the award provide that a performance target affecting vesting could be achieved after the requisite service period Effective for annual periods and interim periods within those annual periods beginning after December 15, 2015; early adoption is permitted Effective for annual periods and interim periods within those annual periods beginning after December 15, 2015; early adoption is permitted ASU 2014-08, Recording Discontinued Operations and Disclosures of Disposals of Components of an Entity Related Resource: FASB Redefines Discontinued Operations Compensation – Stock Compensation (Topic 718) ASU 2014-12, Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period (a consensus of the FASB Emerging Issues Task Force) 5 . What You Need to Know – Changes in Financial Accounting Standards: 2015 Implementation Guidance Update Topic & Title Description Public Companies Revenue from Contracts with Customers (Topic 606) Eliminates most of the existing industry-specific guidance and significantly expands revenue recognition disclosures; provides a fivestep model for revenue recognition to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services Nonpublic Companies For public business entities, certain not-forprofit entities and certain employee benefit plans, effective for annual reporting periods beginning after December 15, 2017, including interim periods within; earlier application is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period* Effective for annual reporting periods beginning after ASU 2014-09 December 15, 2018, Section A – Summary and and interim periods Amendments That Create within annual Revenue from Contracts reporting periods with Customers (Topic 606) beginning after and Other Assets and December 15, 2019; Deferred Costs—Contracts early application with Customers (Subtopic permitted as of annual 340-40) reporting periods Section B – Conforming beginning after Amendments to Other December 31, 2016, Topics and Subtopics in the including interim Requires entities to make Codification and Status reporting periods more estimates and use more Tables within that reporting judgment than under current period, or Section C – Background guidance alternatively, interim Information and Basis for reporting periods Conclusions within annual Related Resources: reporting periods Hot Topics – Revenue beginning one year Recognition after the annual Relief Proposed for New reporting period in Revenue Rules which the entity first applies the guidance in ASU 2014-09 * In August 2015, FASB issued ASU 2015-14, Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date, to defer the revenue recognition standard’s effective date; new dates are reflected above. Latest Developments: FASB issued three proposals, listed below to clarify the new revenue guidance. The amendments would not change core principles of the guidance in Topic 606. The effective dates and transition requirements would be the same as the effective date and transition requirements in ASC 606. • Identifying Performance Obligations and Licensing (issued May 2015) – FASB’s proposal segregates intellectual property into functional and symbolic categories to help determine revenue recognition. The proposal also clarifies when a promised good or service is separately identifiable, i.e., distinct within the context of the contract, and allows entities to disregard items immaterial in the context of the contract. • Narrow-Scope Improvements and Practical Expedients (issued September 2015) – Affecting collectibility, sales tax presentation, noncash considerations measurement and transition expedients; final standard is expected in 2016. • Principal versus Agent Considerations (Reporting Revenue Gross versus Net) (issued August 31, 2015) – A final standard is expected in 2016. 6 .