Update to Consolidation Guidelines - The new standard for investment companies – April 2015

BKD

Description

Update to Consolidation

Guidelines

. Update to Consolidation Guidelines

Table of Contents

INTRODUCTION ..................................................................................................................................................... 3

PROJECT TIMELINE ................................................................................................................................................. 3

BACKGROUND ....................................................................................................................................................... 4

SCOPE ....................................................................................................................................................................

5 SCOPE EXCEPTIONS.........................................................................................................................................................5 Money Market Funds ............................................................................................................................................5 EVALUATING PARTNERSHIPS & SIMILAR ENTITIES ................................................................................................. 6 VARIABLE INTEREST ENTITY (VIE) MODEL .............................................................................................................. 7 VARIABLE INTEREST ENTITIES ............................................................................................................................................8 EFFECT OF NONCONTROLLING RIGHTS ON PRIMARY BENEFICIARY DETERMINATION ....................................................................8 Substantive Participating Rights ...........................................................................................................................8 Protective Rights ...................................................................................................................................................9 Kick-Out Rights ......................................................................................................................................................9 Redemption Rights ..............................................................................................................................................10 CONSOLIDATION BASED ON VARIABLE INTERESTS ...............................................................................................................10 Fees Paid to Decision Makers..............................................................................................................................11 RELATED PARTIES .........................................................................................................................................................11 Proportional Basis ...............................................................................................................................................12 Related-Party Tie Breaker ...................................................................................................................................12 VOTING INTEREST ENTITY (VOE) MODEL..............................................................................................................

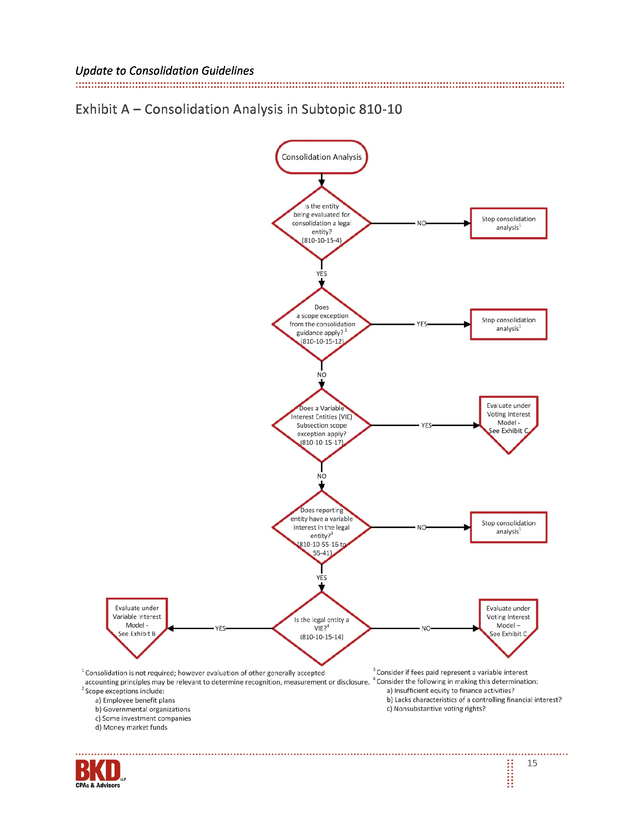

12 EFFECTIVE DATE & TRANSITION ........................................................................................................................... 14 CONTRIBUTOR ..................................................................................................................................................... 14 EXHIBIT A – CONSOLIDATION ANALYSIS IN SUBTOPIC 810-10 ..............................................................................

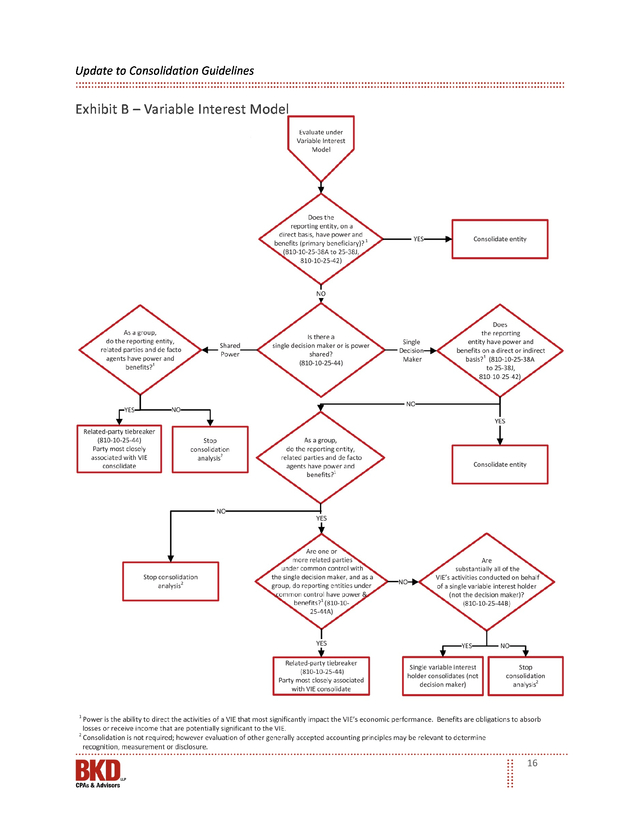

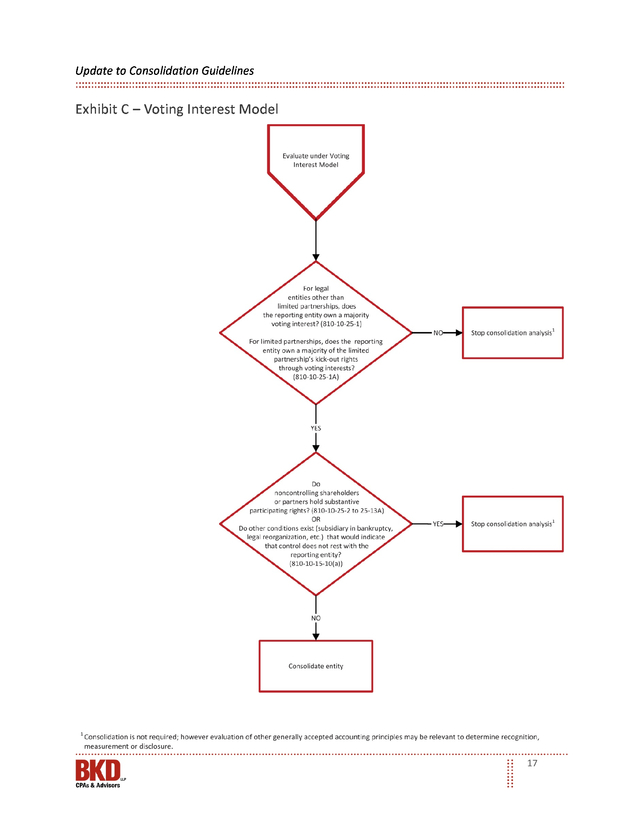

15 EXHIBIT B – VARIABLE INTEREST MODEL ............................................................................................................. 16 EXHIBIT C – VOTING INTEREST MODEL................................................................................................................. 17 EXHIBIT D – VIE DISCLOSURES ..............................................................................................................................

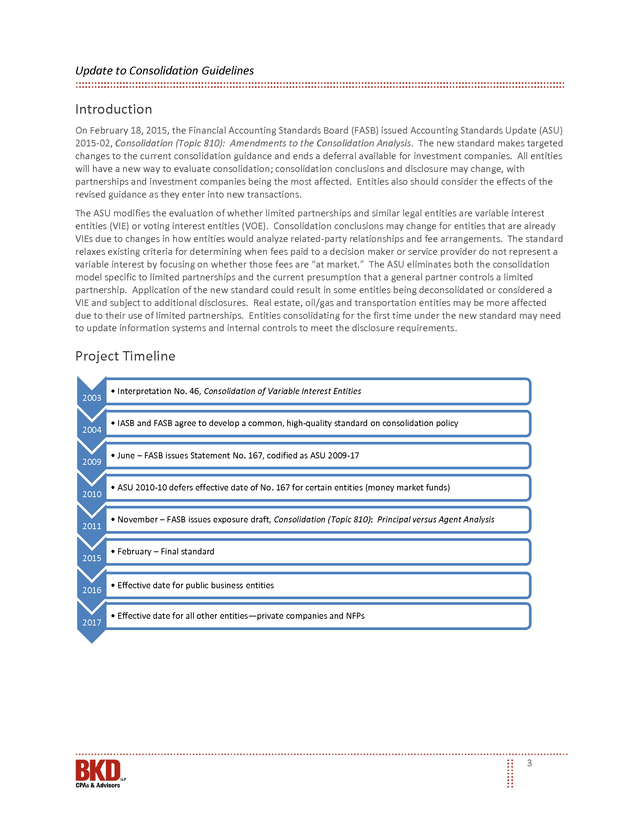

18 PRIMARY BENEFICIARY ..................................................................................................................................................18 HOLDER OF A SIGNIFICANT VARIABLE INTEREST IN A VIE ......................................................................................................18 2 . Update to Consolidation Guidelines Introduction On February 18, 2015, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2015-02, Consolidation (Topic 810): Amendments to the Consolidation Analysis. The new standard makes targeted changes to the current consolidation guidance and ends a deferral available for investment companies. All entities will have a new way to evaluate consolidation; consolidation conclusions and disclosure may change, with partnerships and investment companies being the most affected. Entities also should consider the effects of the revised guidance as they enter into new transactions. The ASU modifies the evaluation of whether limited partnerships and similar legal entities are variable interest entities (VIE) or voting interest entities (VOE).

Consolidation conclusions may change for entities that are already VIEs due to changes in how entities would analyze related-party relationships and fee arrangements. The standard relaxes existing criteria for determining when fees paid to a decision maker or service provider do not represent a variable interest by focusing on whether those fees are “at market.” The ASU eliminates both the consolidation model specific to limited partnerships and the current presumption that a general partner controls a limited partnership. Application of the new standard could result in some entities being deconsolidated or considered a VIE and subject to additional disclosures.

Real estate, oil/gas and transportation entities may be more affected due to their use of limited partnerships. Entities consolidating for the first time under the new standard may need to update information systems and internal controls to meet the disclosure requirements. Project Timeline 2003 2004 2009 2010 2011 2015 2016 2017 • Interpretation No. 46, Consolidation of Variable Interest Entities • IASB and FASB agree to develop a common, high-quality standard on consolidation policy • June – FASB issues Statement No.

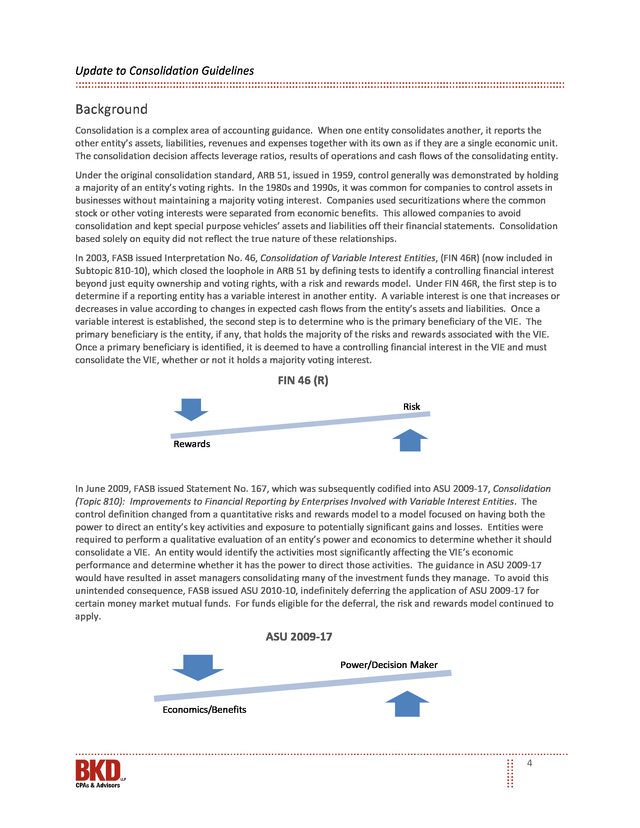

167, codified as ASU 2009-17 • ASU 2010-10 defers effective date of No. 167 for certain entities (money market funds) • November – FASB issues exposure draft, Consolidation (Topic 810): Principal versus Agent Analysis • February – Final standard • Effective date for public business entities • Effective date for all other entities—private companies and NFPs 3 . Update to Consolidation Guidelines Background Consolidation is a complex area of accounting guidance. When one entity consolidates another, it reports the other entity’s assets, liabilities, revenues and expenses together with its own as if they are a single economic unit. The consolidation decision affects leverage ratios, results of operations and cash flows of the consolidating entity. Under the original consolidation standard, ARB 51, issued in 1959, control generally was demonstrated by holding a majority of an entity’s voting rights. In the 1980s and 1990s, it was common for companies to control assets in businesses without maintaining a majority voting interest. Companies used securitizations where the common stock or other voting interests were separated from economic benefits.

This allowed companies to avoid consolidation and kept special purpose vehicles’ assets and liabilities off their financial statements. Consolidation based solely on equity did not reflect the true nature of these relationships. In 2003, FASB issued Interpretation No. 46, Consolidation of Variable Interest Entities, (FIN 46R) (now included in Subtopic 810-10), which closed the loophole in ARB 51 by defining tests to identify a controlling financial interest beyond just equity ownership and voting rights, with a risk and rewards model.

Under FIN 46R, the first step is to determine if a reporting entity has a variable interest in another entity. A variable interest is one that increases or decreases in value according to changes in expected cash flows from the entity’s assets and liabilities. Once a variable interest is established, the second step is to determine who is the primary beneficiary of the VIE.

The primary beneficiary is the entity, if any, that holds the majority of the risks and rewards associated with the VIE. Once a primary beneficiary is identified, it is deemed to have a controlling financial interest in the VIE and must consolidate the VIE, whether or not it holds a majority voting interest. FIN 46 (R) Risk Rewards In June 2009, FASB issued Statement No. 167, which was subsequently codified into ASU 2009-17, Consolidation (Topic 810): Improvements to Financial Reporting by Enterprises Involved with Variable Interest Entities. The control definition changed from a quantitative risks and rewards model to a model focused on having both the power to direct an entity’s key activities and exposure to potentially significant gains and losses.

Entities were required to perform a qualitative evaluation of an entity’s power and economics to determine whether it should consolidate a VIE. An entity would identify the activities most significantly affecting the VIE’s economic performance and determine whether it has the power to direct those activities. The guidance in ASU 2009-17 would have resulted in asset managers consolidating many of the investment funds they manage.

To avoid this unintended consequence, FASB issued ASU 2010-10, indefinitely deferring the application of ASU 2009-17 for certain money market mutual funds. For funds eligible for the deferral, the risk and rewards model continued to apply. ASU 2009-17 Power/Decision Maker Economics/Benefits 4 . Update to Consolidation Guidelines The current VIE model includes two consolidation approaches—one focused on risk and rewards and the other focused on decision-making power and economic exposure. In addition, the original voting interest model continues to apply. This can result in inconsistent consolidation decisions. FASB’s goal in issuing this new standard is to better align its consolidation models to achieve appropriate consolidation outcomes. Scope The standard would affect all entities required to evaluate whether they should consolidate another entity.

The impact will be greatest on entities that have VIEs and limited partnerships that previously were not VIEs. The ASU changes the evaluation of whether an entity is a VIE. Entities that historically were not evaluated under the VIE subsections in Subtopic 810-10 may require evaluation for consolidation under that guidance, while other entities may no longer require evaluation under that guidance.

For example, the ASU replaces guidance for limited partnerships under the voting model (Subtopic 810-20) and introduces a separate analysis in Subtopic 810-10 for evaluating decision-making rights. Today, a limited partnership typically would be a VIE if the general partner has not invested a substantive amount of equity. Under the new guidance, a limited partnership could be a VIE unless substantive kick-out or participating rights can be exercised by a single limited partner or a majority vote of all partners.

The ASU places more emphasis on risk of loss when determining a primary beneficiary; changes to the criteria on evaluating fee arrangements could result in fewer consolidations. Scope Exceptions The ASU carries forward the existing scope exceptions from consolidation under Topic 810-10:  Employee benefit plans covered by Topic 712 or 715  Investment companies covered by Topic 946  Certain governmental organizations As BKD previously reported, construction and extractive industries may continue to apply pro rata consolidation. In addition, entities applying ASU 2014-01, Investments – Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Qualified Affordable Housing Projects, would be exempt from one of the relatedparty tiebreaker requirements, which could result in a limited partner consolidating (see page 12). Research and development arrangements will continue to be evaluated under Subtopic 810-30. Money Market Funds The ASU rescinds the deferral in ASU 2010-10 for certain investment companies. Instead, money market funds registered with the Securities and Exchange Commission (SEC) under Rule 2a-7 of the Investment Company Act of 1940, as well as “similar” unregistered money market funds will be subject to a new scope exception.

To be considered similar, an unregistered money market fund’s structure and targeted outcome must be consistent with that of a registered money market fund. Entities must evaluate the fund’s purpose and design as well as the risks that pass to investees. An unregistered fund’s redemption rights, credit risk exposure, maturity and diversification must be similar to a registered money market fund.

This scope exception includes series mutual funds, as demonstrated by the example provided in the illustrative guidance portion of the standard. Under normal market conditions, a sponsor is able to maintain a stable net asset value (NAV) while still accommodating investor redemption requests. During the financial crisis, several fund sponsors provided financial support to maintain the fund’s $1 NAV, while many more sponsors stood ready to inject financial support if a fund’s NAV dropped below $1 per share. FASB felt this information was critical to financial statement users; the ASU requires increased disclosure for money market fund managers qualifying for the scope exception, as follows:  Information about past financial support provided to the funds for all periods presented; financial support could include capital contributions, standby letters of credit, guarantees of principal and interest, agreements to purchase troubled securities at amortized cost or par and waiver of fees  Explicit commitments to provide financial support in the future 5 .

Update to Consolidation Guidelines Evaluating Partnerships & Similar Entities FASB concluded limited partnerships, due to their unique purpose and design, warranted an assessment separate from corporations. A general partner, through its general partner interest, has the ability to direct activities that significantly impact the economic performance of a limited partnership. This is different from a corporation, where majority shareholders usually direct management who operate the entity. In certain situations, limited partners may have kick-out rights to remove the general partner or participation rights in certain significant business decisions. Current U.S.

GAAP presumes that a general partner in a limited partnership controls (and therefore consolidates) the limited partnership unless substantive kick-out or participating rights exist to overcome that presumption. The ASU eliminates the presumption that a general partner has control; a limited partner would control a limited partnership or similar entity if it could exercise a simple majority of kick-out rights through the partnership interest it holds. Entities that previously applied Subtopic 810-20, Control of Partnerships and Similar Entities, now would apply the limited partnership and similar legal entity guidance within 810-10. FASB eliminated the consolidation model created specifically for limited partnerships contained in Subtopic 810-20.

That model was replaced with an additional requirement for limited partnerships and similar entities to provide partners with either substantive kick-out rights or substantive participating rights over the general partner in order to qualify as VOEs. Limited partnerships that provide limited partners with neither substantive kick-out rights nor substantive participating rights should be evaluated for consolidation as VIEs. A reporting entity that holds a variable interest in a VIE may be required to provide certain disclosures even if it is not the primary beneficiary of the VIE (see Exhibit D). Determining whether substantive kick-out rights exist in a limited partnership would be restricted only to kick-out rights held by limited partners. When determining whether a limited partnership is a VIE, the general partner, entities under common control with the general partner and other parties acting on behalf of the general partner would be excluded from the simple majority or lower threshold of voting interests to exercise kick-out rights.

In addition, participating rights held by the general partner or its related parties are not considered substantive. A general partner able to deconsolidate a business as a result of the new guidance should give careful consideration to goodwill, segment reporting and impairment testing. 6 . Update to Consolidation Guidelines Today, a general partner contributing substantive equity (greater than 1 percent) is grouped with other investors to determine if the equity investors as a group have decision-making power over the most significant activities. As a result, the limited partnership typically is a VOE. The ASU disregards the equity provided by the general partner and focuses instead on the voting rights of the limited partners. Since many limited partners do not hold kick-out or participating rights, more partnerships may be considered VIEs. Case A A limited partnership has three limited partners who have no relationship to the general partners, with each holding an equal amount of the limited partnership’s kick-out rights through voting interests. The partnership agreement requires a simple majority (two of three limited partners) to remove the general partners.

The kickout rights are assumed to be substantive. The partners have the power through voting rights to direct the activities of the partnership that most significantly impact the partnership’s economic performance for a substantive kick-out right. The limited partnership would be considered a VOE. Case B Case B has the same facts as above except that a vote of all three limited partners is required to remove the general partner and the limited partners do not possess substantive participating rights. Because the required vote is greater than a simple majority of the limited partnership’s kick-out rights through partners voting interests, the limited partnership would not meet the requirements for a substantive kick-out right. This limited partnership would be considered a VIE. Variable Interest Entity (VIE) Model Under the VIE model, a controlling financial interest is assessed differently than under the VOE model. A different assessment is required because a controlling financial interest may be achieved other than by ownership of shares or voting interests. Under current U.S.

GAAP and the ASU, a decision maker is determined to be the primary beneficiary of a VIE and could consolidate if it satisfies both of the following power and economics criteria:  The “power” to direct the activities that most significantly impact the VIE’s economic performance  The obligation to absorb the losses of the VIE that could potentially be significant to the VIE, or the right to receive benefits from the VIE that potentially could be significant to the VIE, i.e., the “economics” The ASU replaces guidance for limited partnerships under the voting model (Subtopic 810-20) and introduces a separate analysis in the VIE model (Subtopic 810-10) for evaluating decision-making rights. The previous criteria for determining whether a limited partnership should be consolidated by a general partner now are used to determine whether a limited partnership or similar legal entity is a VIE. Today, a limited partnership typically would be a VIE if the general partner has not invested a substantive amount of equity. Under the new guidance, a limited partnership could be a VIE unless substantive kick-out or participating rights are exercisable either by a single limited partner or by a majority vote of all partners.

A different consolidation conclusion may be reached under the VIE model than under the voting model; additional disclosures would apply. This change would result in more entities being VIEs and have broad application, since limited partnership structures are utilized extensively in the asset management sector and in a number of other sectors such as oil and gas, transportation and real estate development. 7 . Update to Consolidation Guidelines Variable Interest Entities A reporting entity must first determine if it holds a variable interest in a VIE. The standard does not change the definition of a VIE. Variable interest entities:  Do not have sufficient equity to fund their operations  As a group have equity holders that lack any of the following characteristics: • • • The right to receive the expected residual returns Power to direct the activities most significantly impacting the entity’s economic performance The obligation to absorb the expected losses The ASU changes how reporting entities evaluate the decision maker’s fee arrangements, the effect of relatedparty interests on the primary beneficiary determination and the timing of the related-party tiebreaker test, which may lead to different consolidation conclusions. Effect of Noncontrolling Rights on Primary Beneficiary Determination Ownership of a majority voting interest is the usual condition for a controlling financial interest and consolidation. However, exceptions exist when noncontrolling shareholders have “substantive” participating rights. The powers of the majority shareholder or limited partner holding a majority of the kick-out rights may be restricted by approval or veto right granted to noncontrolling shareholders or other limited partners. The assessment of noncontrolling rights should be made at the time a majority voting interest or majority of kickout rights through voting interests is obtained.

Reassessment of noncontrolling interest would occur only if there is a significant change to the terms or the exercisability of the rights. Substantive Participating Rights To overcome the presumption of consolidation by the majority voting interest, the noncontrolling rights— individually or in the aggregate—must allow the noncontrolling shareholder or limited partner to effectively participate in certain significant investee financial and operating decisions in the ordinary course of business. For example, noncontrolling shareholders may be allowed to approve the operating budget, set management’s compensation or select and terminate management. These rights could preclude a majority shareholder from consolidating an entity due to substantive participating rights by the noncontrolling shareholder.

The factors for evaluating if participating rights are substantive remain unchanged from current GAAP, except for the inclusion of limited partner language. The factors are as follows:  Size of ownership interest in investee  Governing documents that indicate at what level decisions are made—at the shareholder, limited partner level or at the board level  Related-party relationships between the major and noncontrolling shareholders or partners  Noncontrolling rights covering insignificant business operations, e.g., location of headquarters, investee’s name, selection of auditors or accounting principles  Noncontrolling rights with a remote chance of occurring  Buyout rights The likelihood that a veto right will be exercised should not be considered when assessing whether that right is substantive. 8 . Update to Consolidation Guidelines Participating Rights – VIE Model – Partnerships Current U.S. GAAP The ability to block the actions through which a reporting entity exercises the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance New Model The ability to block or participate in the actions through which an entity exercises the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance Holders of participating rights are not required to have the ability to initiate actions Protective Rights Protective rights are designed to protect the interests of the rights holder without giving that party a controlling interest. Such rights allow the holder to block corporate or partnership actions. Examples of noncontrolling protective rights include, but are not limited to:  Amendments to articles of incorporation or partnership agreements  Transaction pricing on self-dealing activities  Liquidation of the investee  Acquisitions and dispositions not in the ordinary course of business  Issuance or repurchase of equity interests Protective rights alone would not overcome the presumption of consolidation by the majority voting interest or the limited partner with a majority of kick-out rights.

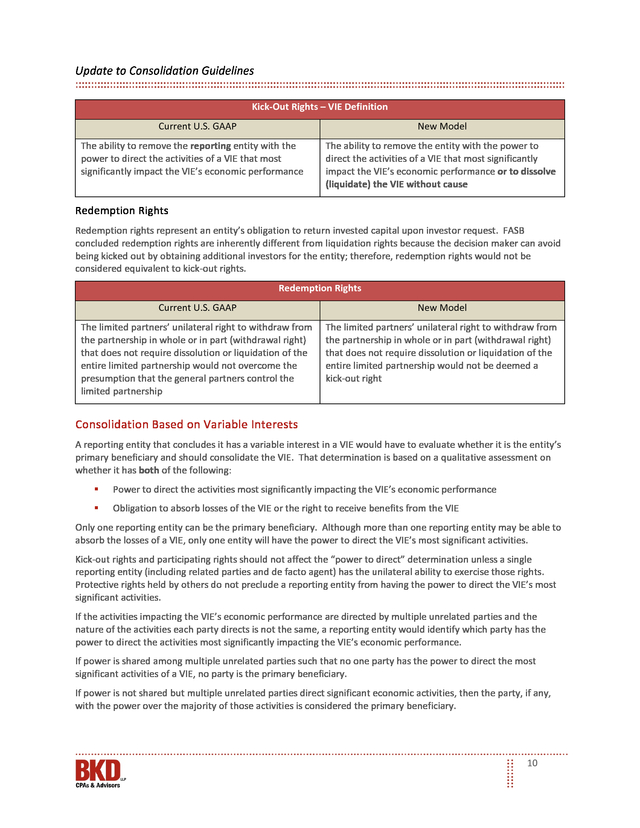

However, other rights that allow participation in significant financial and operating decisions, although also protective in nature, could overcome the presumption of consolidation by the majority voting interest. The assessment of noncontrolling rights is a matter of judgment that will depend on facts and circumstances. Kick-Out Rights The right to remove the general partner is considered a kick-out right. In addition, if a general partner has outsourced management, a limited partner’s right to terminate management may be a substantive participating right. Judgment will be required to determine whether kick-out rights are substantive.

For kick-out rights to be considered substantive, there can be no significant barrier for the limited partner to exercise those rights. Examples of barriers include:  Narrow limits on timing of exercise  Financial penalties or operational barriers to liquidating the partnership or replacing general partners  Lack of qualified replacement general partners or inadequate compensation for qualified replacement general partners  Limited ability for limited partners to call for and conduct vote to exercise rights  Lack of information for limited partners to exercise rights 9 . Update to Consolidation Guidelines Kick-Out Rights – VIE Definition Current U.S. GAAP New Model The ability to remove the reporting entity with the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance The ability to remove the entity with the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance or to dissolve (liquidate) the VIE without cause Redemption Rights Redemption rights represent an entity’s obligation to return invested capital upon investor request. FASB concluded redemption rights are inherently different from liquidation rights because the decision maker can avoid being kicked out by obtaining additional investors for the entity; therefore, redemption rights would not be considered equivalent to kick-out rights. Redemption Rights Current U.S. GAAP New Model The limited partners’ unilateral right to withdraw from the partnership in whole or in part (withdrawal right) that does not require dissolution or liquidation of the entire limited partnership would not overcome the presumption that the general partners control the limited partnership The limited partners’ unilateral right to withdraw from the partnership in whole or in part (withdrawal right) that does not require dissolution or liquidation of the entire limited partnership would not be deemed a kick-out right Consolidation Based on Variable Interests A reporting entity that concludes it has a variable interest in a VIE would have to evaluate whether it is the entity’s primary beneficiary and should consolidate the VIE.

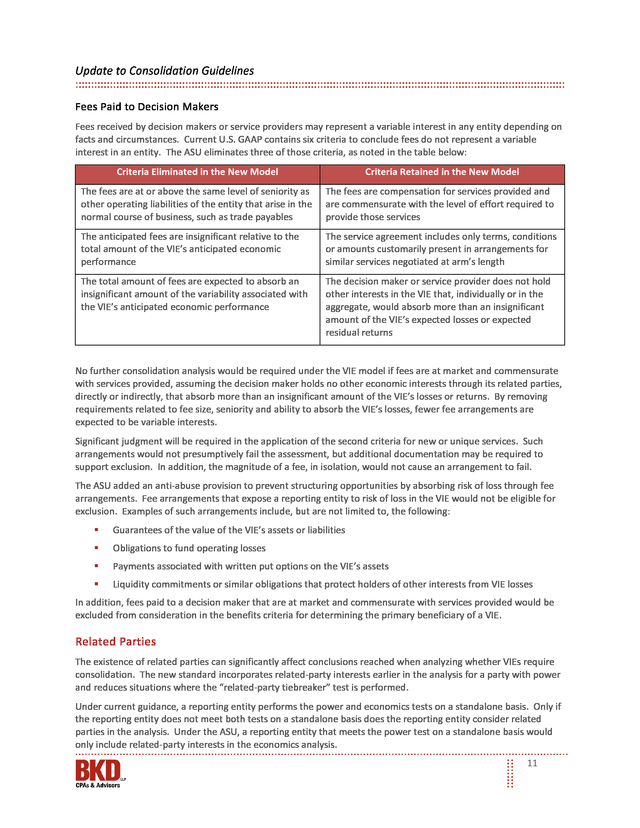

That determination is based on a qualitative assessment on whether it has both of the following:  Power to direct the activities most significantly impacting the VIE’s economic performance  Obligation to absorb losses of the VIE or the right to receive benefits from the VIE Only one reporting entity can be the primary beneficiary. Although more than one reporting entity may be able to absorb the losses of a VIE, only one entity will have the power to direct the VIE’s most significant activities. Kick-out rights and participating rights should not affect the “power to direct” determination unless a single reporting entity (including related parties and de facto agent) has the unilateral ability to exercise those rights. Protective rights held by others do not preclude a reporting entity from having the power to direct the VIE’s most significant activities. If the activities impacting the VIE’s economic performance are directed by multiple unrelated parties and the nature of the activities each party directs is not the same, a reporting entity would identify which party has the power to direct the activities most significantly impacting the VIE’s economic performance. If power is shared among multiple unrelated parties such that no one party has the power to direct the most significant activities of a VIE, no party is the primary beneficiary. If power is not shared but multiple unrelated parties direct significant economic activities, then the party, if any, with the power over the majority of those activities is considered the primary beneficiary. 10 . Update to Consolidation Guidelines Fees Paid to Decision Makers Fees received by decision makers or service providers may represent a variable interest in any entity depending on facts and circumstances. Current U.S. GAAP contains six criteria to conclude fees do not represent a variable interest in an entity. The ASU eliminates three of those criteria, as noted in the table below: Criteria Eliminated in the New Model Criteria Retained in the New Model The fees are at or above the same level of seniority as other operating liabilities of the entity that arise in the normal course of business, such as trade payables The fees are compensation for services provided and are commensurate with the level of effort required to provide those services The anticipated fees are insignificant relative to the total amount of the VIE’s anticipated economic performance The service agreement includes only terms, conditions or amounts customarily present in arrangements for similar services negotiated at arm’s length The total amount of fees are expected to absorb an insignificant amount of the variability associated with the VIE’s anticipated economic performance The decision maker or service provider does not hold other interests in the VIE that, individually or in the aggregate, would absorb more than an insignificant amount of the VIE’s expected losses or expected residual returns No further consolidation analysis would be required under the VIE model if fees are at market and commensurate with services provided, assuming the decision maker holds no other economic interests through its related parties, directly or indirectly, that absorb more than an insignificant amount of the VIE’s losses or returns.

By removing requirements related to fee size, seniority and ability to absorb the VIE’s losses, fewer fee arrangements are expected to be variable interests. Significant judgment will be required in the application of the second criteria for new or unique services. Such arrangements would not presumptively fail the assessment, but additional documentation may be required to support exclusion. In addition, the magnitude of a fee, in isolation, would not cause an arrangement to fail. The ASU added an anti-abuse provision to prevent structuring opportunities by absorbing risk of loss through fee arrangements.

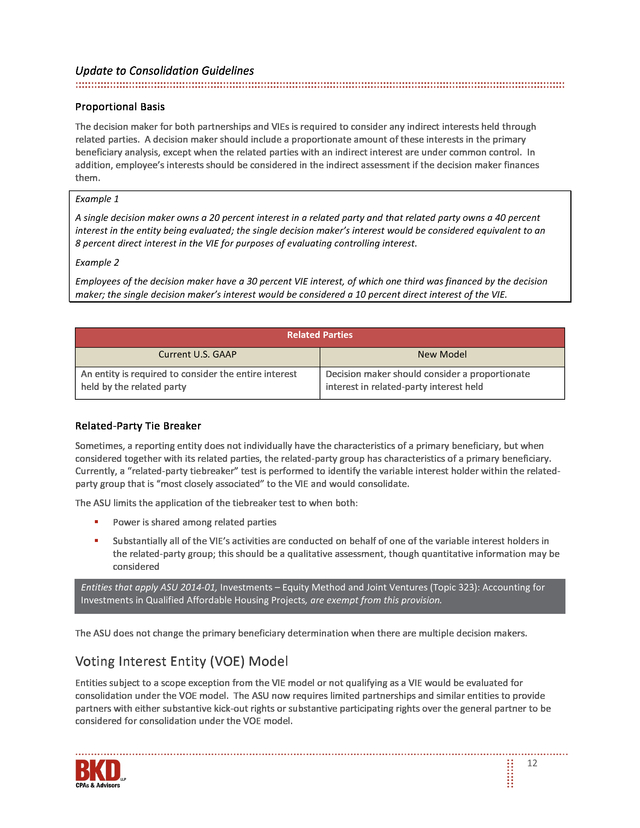

Fee arrangements that expose a reporting entity to risk of loss in the VIE would not be eligible for exclusion. Examples of such arrangements include, but are not limited to, the following:  Guarantees of the value of the VIE’s assets or liabilities  Obligations to fund operating losses  Payments associated with written put options on the VIE’s assets  Liquidity commitments or similar obligations that protect holders of other interests from VIE losses In addition, fees paid to a decision maker that are at market and commensurate with services provided would be excluded from consideration in the benefits criteria for determining the primary beneficiary of a VIE. Related Parties The existence of related parties can significantly affect conclusions reached when analyzing whether VIEs require consolidation. The new standard incorporates related-party interests earlier in the analysis for a party with power and reduces situations where the “related-party tiebreaker” test is performed. Under current guidance, a reporting entity performs the power and economics tests on a standalone basis.

Only if the reporting entity does not meet both tests on a standalone basis does the reporting entity consider related parties in the analysis. Under the ASU, a reporting entity that meets the power test on a standalone basis would only include related-party interests in the economics analysis. 11 . Update to Consolidation Guidelines Proportional Basis The decision maker for both partnerships and VIEs is required to consider any indirect interests held through related parties. A decision maker should include a proportionate amount of these interests in the primary beneficiary analysis, except when the related parties with an indirect interest are under common control. In addition, employee’s interests should be considered in the indirect assessment if the decision maker finances them. Example 1 A single decision maker owns a 20 percent interest in a related party and that related party owns a 40 percent interest in the entity being evaluated; the single decision maker’s interest would be considered equivalent to an 8 percent direct interest in the VIE for purposes of evaluating controlling interest. Example 2 Employees of the decision maker have a 30 percent VIE interest, of which one third was financed by the decision maker; the single decision maker’s interest would be considered a 10 percent direct interest of the VIE. Related Parties Current U.S. GAAP An entity is required to consider the entire interest held by the related party New Model Decision maker should consider a proportionate interest in related-party interest held Related-Party Tie Breaker Sometimes, a reporting entity does not individually have the characteristics of a primary beneficiary, but when considered together with its related parties, the related-party group has characteristics of a primary beneficiary. Currently, a “related-party tiebreaker” test is performed to identify the variable interest holder within the relatedparty group that is “most closely associated” to the VIE and would consolidate. The ASU limits the application of the tiebreaker test to when both:  Power is shared among related parties  Substantially all of the VIE’s activities are conducted on behalf of one of the variable interest holders in the related-party group; this should be a qualitative assessment, though quantitative information may be considered Entities that apply ASU 2014-01, Investments – Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Qualified Affordable Housing Projects, are exempt from this provision. The ASU does not change the primary beneficiary determination when there are multiple decision makers. Voting Interest Entity (VOE) Model Entities subject to a scope exception from the VIE model or not qualifying as a VIE would be evaluated for consolidation under the VOE model.

The ASU now requires limited partnerships and similar entities to provide partners with either substantive kick-out rights or substantive participating rights over the general partner to be considered for consolidation under the VOE model. 12 . Update to Consolidation Guidelines Under the VOE model (for legal entities other than limited partnerships), the usual condition for a controlling financial interest is direct or indirect ownership by one reporting entity of more than 50 percent of the outstanding voting shares of another entity. For limited partnerships, the usual condition for a controlling financial interest is direct or indirect ownership by one limited partner of more than 50 percent of the limited partners’ kick-out rights through voting interests. If noncontrolling shareholders or limited partners have substantive participating rights, the majority shareholder or limited partner with a majority of kick-out rights through voting interests does not have a controlling financial interest. The ASU eliminates the presumption in the current voting model that a general partner controls a limited partnership or similar entity. Under the new guidance, a general partner will not consolidate a partnership or similar entity under the voting model.

In general, only a single limited partner able to exercise substantive kick-out rights will consolidate under the voting model. The ASU does not change the voting model for consolidation of corporations and similar entities. The ASU introduces a separate analysis specific to limited partnerships and similar entities for assessing whether the equity holders at risk lack decision-making rights. Limited partnerships and similar entities will be VIEs unless the limited partners hold substantive kick-out rights or participating rights.

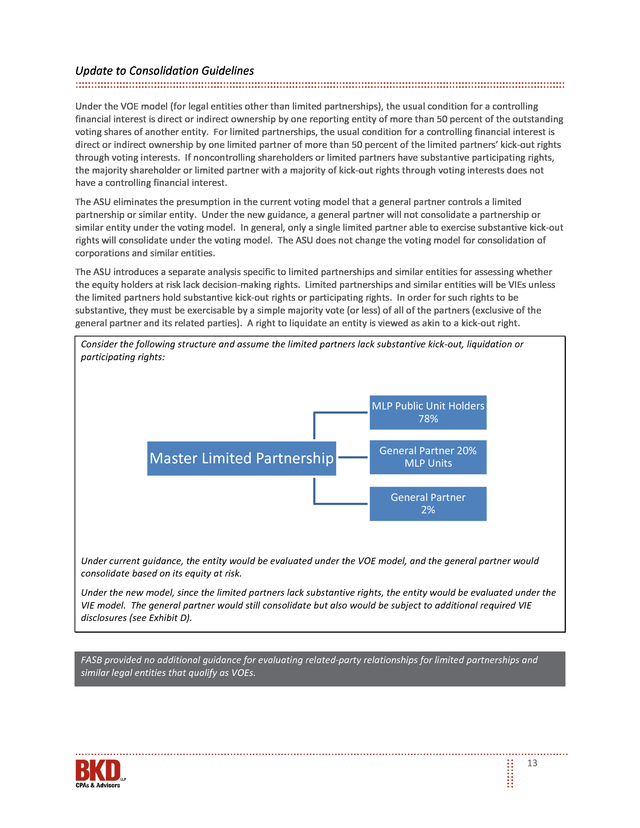

In order for such rights to be substantive, they must be exercisable by a simple majority vote (or less) of all of the partners (exclusive of the general partner and its related parties). A right to liquidate an entity is viewed as akin to a kick-out right. Consider the following structure and assume the limited partners lack substantive kick-out, liquidation or participating rights: MLP Public Unit Holders 78% Master Limited Partnership General Partner 20% MLP Units General Partner 2% Under current guidance, the entity would be evaluated under the VOE model, and the general partner would consolidate based on its equity at risk. Under the new model, since the limited partners lack substantive rights, the entity would be evaluated under the VIE model. The general partner would still consolidate but also would be subject to additional required VIE disclosures (see Exhibit D). FASB provided no additional guidance for evaluating related-party relationships for limited partnerships and similar legal entities that qualify as VOEs. 13 .

Update to Consolidation Guidelines Effective Date & Transition The ASU would be effective for public business entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015. All other entities have an additional year for transition—for fiscal years beginning after December 15, 2016, and for interim periods beginning after December 15, 2017. Early adoption is permitted, including adoption in an interim period. Entities may adopt the changes on a modified retrospective or full retrospective basis:  For entities consolidating for the first time because of the new standard, assets and liabilities will be recognized as of the date of adoption based on the carrying amounts as if the guidance had always been applied. Fair value at the date of adoption is permitted if it is not practical to determine the entity’s carrying amounts of individual assets and liabilities as if the guidance had always been applied. • Entities are permitted to elect the fair value option for financial instruments only if the reporting entity elects the option for all eligible financial assets and liabilities of the newly consolidated entity.

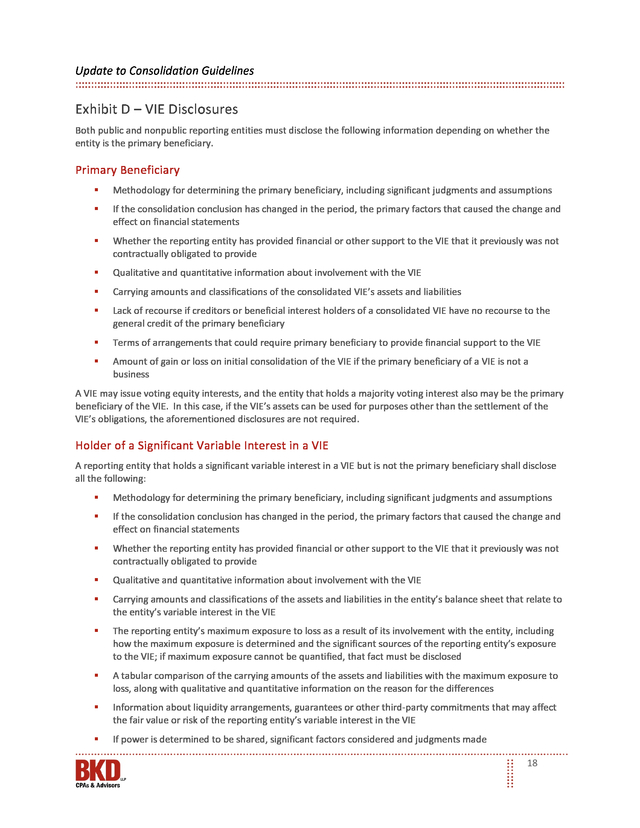

This election is on an entity-by-entity basis.  For entities deconsolidating due to application of the ASU, the carrying amount of any retained interests must be determined based on what that amount would have been had the standard been effective at the time the reporting entity initially became involved with or no longer controlled the entity. Fair value at the date of adoption is permitted if determining the carrying amount of retained interest in the deconsolidated former subsidiary is not practical.  Any difference between the net amount of assets and liabilities of the entities added to or subtracted from the reporting entity’s balance sheet will be recognized as a cumulative-effect adjustment to retained earnings. The ASU provides no alternative recognition, measurement or disclosure alternatives for nonpublic business entities. Contact your BKD advisor to learn more about how this new consolidation guidance affects your organization. Contributor Anne Coughlan Director 317.383.4000 acoughlan@bkd.com 14 . Update to Consolidation Guidelines Exhibit A – Consolidation Analysis in Subtopic 810-10 15 . Update to Consolidation Guidelines Exhibit B – Variable Interest Model 16 . Update to Consolidation Guidelines Exhibit C – Voting Interest Model 17 . Update to Consolidation Guidelines Exhibit D – VIE Disclosures Both public and nonpublic reporting entities must disclose the following information depending on whether the entity is the primary beneficiary. Primary Beneficiary  Methodology for determining the primary beneficiary, including significant judgments and assumptions  If the consolidation conclusion has changed in the period, the primary factors that caused the change and effect on financial statements  Whether the reporting entity has provided financial or other support to the VIE that it previously was not contractually obligated to provide  Qualitative and quantitative information about involvement with the VIE  Carrying amounts and classifications of the consolidated VIE’s assets and liabilities  Lack of recourse if creditors or beneficial interest holders of a consolidated VIE have no recourse to the general credit of the primary beneficiary  Terms of arrangements that could require primary beneficiary to provide financial support to the VIE  Amount of gain or loss on initial consolidation of the VIE if the primary beneficiary of a VIE is not a business A VIE may issue voting equity interests, and the entity that holds a majority voting interest also may be the primary beneficiary of the VIE. In this case, if the VIE’s assets can be used for purposes other than the settlement of the VIE’s obligations, the aforementioned disclosures are not required. Holder of a Significant Variable Interest in a VIE A reporting entity that holds a significant variable interest in a VIE but is not the primary beneficiary shall disclose all the following:  Methodology for determining the primary beneficiary, including significant judgments and assumptions  If the consolidation conclusion has changed in the period, the primary factors that caused the change and effect on financial statements  Whether the reporting entity has provided financial or other support to the VIE that it previously was not contractually obligated to provide  Qualitative and quantitative information about involvement with the VIE  Carrying amounts and classifications of the assets and liabilities in the entity’s balance sheet that relate to the entity’s variable interest in the VIE  The reporting entity’s maximum exposure to loss as a result of its involvement with the entity, including how the maximum exposure is determined and the significant sources of the reporting entity’s exposure to the VIE; if maximum exposure cannot be quantified, that fact must be disclosed  A tabular comparison of the carrying amounts of the assets and liabilities with the maximum exposure to loss, along with qualitative and quantitative information on the reason for the differences  Information about liquidity arrangements, guarantees or other third-party commitments that may affect the fair value or risk of the reporting entity’s variable interest in the VIE  If power is determined to be shared, significant factors considered and judgments made 18 .

5 SCOPE EXCEPTIONS.........................................................................................................................................................5 Money Market Funds ............................................................................................................................................5 EVALUATING PARTNERSHIPS & SIMILAR ENTITIES ................................................................................................. 6 VARIABLE INTEREST ENTITY (VIE) MODEL .............................................................................................................. 7 VARIABLE INTEREST ENTITIES ............................................................................................................................................8 EFFECT OF NONCONTROLLING RIGHTS ON PRIMARY BENEFICIARY DETERMINATION ....................................................................8 Substantive Participating Rights ...........................................................................................................................8 Protective Rights ...................................................................................................................................................9 Kick-Out Rights ......................................................................................................................................................9 Redemption Rights ..............................................................................................................................................10 CONSOLIDATION BASED ON VARIABLE INTERESTS ...............................................................................................................10 Fees Paid to Decision Makers..............................................................................................................................11 RELATED PARTIES .........................................................................................................................................................11 Proportional Basis ...............................................................................................................................................12 Related-Party Tie Breaker ...................................................................................................................................12 VOTING INTEREST ENTITY (VOE) MODEL..............................................................................................................

12 EFFECTIVE DATE & TRANSITION ........................................................................................................................... 14 CONTRIBUTOR ..................................................................................................................................................... 14 EXHIBIT A – CONSOLIDATION ANALYSIS IN SUBTOPIC 810-10 ..............................................................................

15 EXHIBIT B – VARIABLE INTEREST MODEL ............................................................................................................. 16 EXHIBIT C – VOTING INTEREST MODEL................................................................................................................. 17 EXHIBIT D – VIE DISCLOSURES ..............................................................................................................................

18 PRIMARY BENEFICIARY ..................................................................................................................................................18 HOLDER OF A SIGNIFICANT VARIABLE INTEREST IN A VIE ......................................................................................................18 2 . Update to Consolidation Guidelines Introduction On February 18, 2015, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2015-02, Consolidation (Topic 810): Amendments to the Consolidation Analysis. The new standard makes targeted changes to the current consolidation guidance and ends a deferral available for investment companies. All entities will have a new way to evaluate consolidation; consolidation conclusions and disclosure may change, with partnerships and investment companies being the most affected. Entities also should consider the effects of the revised guidance as they enter into new transactions. The ASU modifies the evaluation of whether limited partnerships and similar legal entities are variable interest entities (VIE) or voting interest entities (VOE).

Consolidation conclusions may change for entities that are already VIEs due to changes in how entities would analyze related-party relationships and fee arrangements. The standard relaxes existing criteria for determining when fees paid to a decision maker or service provider do not represent a variable interest by focusing on whether those fees are “at market.” The ASU eliminates both the consolidation model specific to limited partnerships and the current presumption that a general partner controls a limited partnership. Application of the new standard could result in some entities being deconsolidated or considered a VIE and subject to additional disclosures.

Real estate, oil/gas and transportation entities may be more affected due to their use of limited partnerships. Entities consolidating for the first time under the new standard may need to update information systems and internal controls to meet the disclosure requirements. Project Timeline 2003 2004 2009 2010 2011 2015 2016 2017 • Interpretation No. 46, Consolidation of Variable Interest Entities • IASB and FASB agree to develop a common, high-quality standard on consolidation policy • June – FASB issues Statement No.

167, codified as ASU 2009-17 • ASU 2010-10 defers effective date of No. 167 for certain entities (money market funds) • November – FASB issues exposure draft, Consolidation (Topic 810): Principal versus Agent Analysis • February – Final standard • Effective date for public business entities • Effective date for all other entities—private companies and NFPs 3 . Update to Consolidation Guidelines Background Consolidation is a complex area of accounting guidance. When one entity consolidates another, it reports the other entity’s assets, liabilities, revenues and expenses together with its own as if they are a single economic unit. The consolidation decision affects leverage ratios, results of operations and cash flows of the consolidating entity. Under the original consolidation standard, ARB 51, issued in 1959, control generally was demonstrated by holding a majority of an entity’s voting rights. In the 1980s and 1990s, it was common for companies to control assets in businesses without maintaining a majority voting interest. Companies used securitizations where the common stock or other voting interests were separated from economic benefits.

This allowed companies to avoid consolidation and kept special purpose vehicles’ assets and liabilities off their financial statements. Consolidation based solely on equity did not reflect the true nature of these relationships. In 2003, FASB issued Interpretation No. 46, Consolidation of Variable Interest Entities, (FIN 46R) (now included in Subtopic 810-10), which closed the loophole in ARB 51 by defining tests to identify a controlling financial interest beyond just equity ownership and voting rights, with a risk and rewards model.

Under FIN 46R, the first step is to determine if a reporting entity has a variable interest in another entity. A variable interest is one that increases or decreases in value according to changes in expected cash flows from the entity’s assets and liabilities. Once a variable interest is established, the second step is to determine who is the primary beneficiary of the VIE.

The primary beneficiary is the entity, if any, that holds the majority of the risks and rewards associated with the VIE. Once a primary beneficiary is identified, it is deemed to have a controlling financial interest in the VIE and must consolidate the VIE, whether or not it holds a majority voting interest. FIN 46 (R) Risk Rewards In June 2009, FASB issued Statement No. 167, which was subsequently codified into ASU 2009-17, Consolidation (Topic 810): Improvements to Financial Reporting by Enterprises Involved with Variable Interest Entities. The control definition changed from a quantitative risks and rewards model to a model focused on having both the power to direct an entity’s key activities and exposure to potentially significant gains and losses.

Entities were required to perform a qualitative evaluation of an entity’s power and economics to determine whether it should consolidate a VIE. An entity would identify the activities most significantly affecting the VIE’s economic performance and determine whether it has the power to direct those activities. The guidance in ASU 2009-17 would have resulted in asset managers consolidating many of the investment funds they manage.

To avoid this unintended consequence, FASB issued ASU 2010-10, indefinitely deferring the application of ASU 2009-17 for certain money market mutual funds. For funds eligible for the deferral, the risk and rewards model continued to apply. ASU 2009-17 Power/Decision Maker Economics/Benefits 4 . Update to Consolidation Guidelines The current VIE model includes two consolidation approaches—one focused on risk and rewards and the other focused on decision-making power and economic exposure. In addition, the original voting interest model continues to apply. This can result in inconsistent consolidation decisions. FASB’s goal in issuing this new standard is to better align its consolidation models to achieve appropriate consolidation outcomes. Scope The standard would affect all entities required to evaluate whether they should consolidate another entity.

The impact will be greatest on entities that have VIEs and limited partnerships that previously were not VIEs. The ASU changes the evaluation of whether an entity is a VIE. Entities that historically were not evaluated under the VIE subsections in Subtopic 810-10 may require evaluation for consolidation under that guidance, while other entities may no longer require evaluation under that guidance.

For example, the ASU replaces guidance for limited partnerships under the voting model (Subtopic 810-20) and introduces a separate analysis in Subtopic 810-10 for evaluating decision-making rights. Today, a limited partnership typically would be a VIE if the general partner has not invested a substantive amount of equity. Under the new guidance, a limited partnership could be a VIE unless substantive kick-out or participating rights can be exercised by a single limited partner or a majority vote of all partners.

The ASU places more emphasis on risk of loss when determining a primary beneficiary; changes to the criteria on evaluating fee arrangements could result in fewer consolidations. Scope Exceptions The ASU carries forward the existing scope exceptions from consolidation under Topic 810-10:  Employee benefit plans covered by Topic 712 or 715  Investment companies covered by Topic 946  Certain governmental organizations As BKD previously reported, construction and extractive industries may continue to apply pro rata consolidation. In addition, entities applying ASU 2014-01, Investments – Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Qualified Affordable Housing Projects, would be exempt from one of the relatedparty tiebreaker requirements, which could result in a limited partner consolidating (see page 12). Research and development arrangements will continue to be evaluated under Subtopic 810-30. Money Market Funds The ASU rescinds the deferral in ASU 2010-10 for certain investment companies. Instead, money market funds registered with the Securities and Exchange Commission (SEC) under Rule 2a-7 of the Investment Company Act of 1940, as well as “similar” unregistered money market funds will be subject to a new scope exception.

To be considered similar, an unregistered money market fund’s structure and targeted outcome must be consistent with that of a registered money market fund. Entities must evaluate the fund’s purpose and design as well as the risks that pass to investees. An unregistered fund’s redemption rights, credit risk exposure, maturity and diversification must be similar to a registered money market fund.

This scope exception includes series mutual funds, as demonstrated by the example provided in the illustrative guidance portion of the standard. Under normal market conditions, a sponsor is able to maintain a stable net asset value (NAV) while still accommodating investor redemption requests. During the financial crisis, several fund sponsors provided financial support to maintain the fund’s $1 NAV, while many more sponsors stood ready to inject financial support if a fund’s NAV dropped below $1 per share. FASB felt this information was critical to financial statement users; the ASU requires increased disclosure for money market fund managers qualifying for the scope exception, as follows:  Information about past financial support provided to the funds for all periods presented; financial support could include capital contributions, standby letters of credit, guarantees of principal and interest, agreements to purchase troubled securities at amortized cost or par and waiver of fees  Explicit commitments to provide financial support in the future 5 .

Update to Consolidation Guidelines Evaluating Partnerships & Similar Entities FASB concluded limited partnerships, due to their unique purpose and design, warranted an assessment separate from corporations. A general partner, through its general partner interest, has the ability to direct activities that significantly impact the economic performance of a limited partnership. This is different from a corporation, where majority shareholders usually direct management who operate the entity. In certain situations, limited partners may have kick-out rights to remove the general partner or participation rights in certain significant business decisions. Current U.S.

GAAP presumes that a general partner in a limited partnership controls (and therefore consolidates) the limited partnership unless substantive kick-out or participating rights exist to overcome that presumption. The ASU eliminates the presumption that a general partner has control; a limited partner would control a limited partnership or similar entity if it could exercise a simple majority of kick-out rights through the partnership interest it holds. Entities that previously applied Subtopic 810-20, Control of Partnerships and Similar Entities, now would apply the limited partnership and similar legal entity guidance within 810-10. FASB eliminated the consolidation model created specifically for limited partnerships contained in Subtopic 810-20.

That model was replaced with an additional requirement for limited partnerships and similar entities to provide partners with either substantive kick-out rights or substantive participating rights over the general partner in order to qualify as VOEs. Limited partnerships that provide limited partners with neither substantive kick-out rights nor substantive participating rights should be evaluated for consolidation as VIEs. A reporting entity that holds a variable interest in a VIE may be required to provide certain disclosures even if it is not the primary beneficiary of the VIE (see Exhibit D). Determining whether substantive kick-out rights exist in a limited partnership would be restricted only to kick-out rights held by limited partners. When determining whether a limited partnership is a VIE, the general partner, entities under common control with the general partner and other parties acting on behalf of the general partner would be excluded from the simple majority or lower threshold of voting interests to exercise kick-out rights.

In addition, participating rights held by the general partner or its related parties are not considered substantive. A general partner able to deconsolidate a business as a result of the new guidance should give careful consideration to goodwill, segment reporting and impairment testing. 6 . Update to Consolidation Guidelines Today, a general partner contributing substantive equity (greater than 1 percent) is grouped with other investors to determine if the equity investors as a group have decision-making power over the most significant activities. As a result, the limited partnership typically is a VOE. The ASU disregards the equity provided by the general partner and focuses instead on the voting rights of the limited partners. Since many limited partners do not hold kick-out or participating rights, more partnerships may be considered VIEs. Case A A limited partnership has three limited partners who have no relationship to the general partners, with each holding an equal amount of the limited partnership’s kick-out rights through voting interests. The partnership agreement requires a simple majority (two of three limited partners) to remove the general partners.

The kickout rights are assumed to be substantive. The partners have the power through voting rights to direct the activities of the partnership that most significantly impact the partnership’s economic performance for a substantive kick-out right. The limited partnership would be considered a VOE. Case B Case B has the same facts as above except that a vote of all three limited partners is required to remove the general partner and the limited partners do not possess substantive participating rights. Because the required vote is greater than a simple majority of the limited partnership’s kick-out rights through partners voting interests, the limited partnership would not meet the requirements for a substantive kick-out right. This limited partnership would be considered a VIE. Variable Interest Entity (VIE) Model Under the VIE model, a controlling financial interest is assessed differently than under the VOE model. A different assessment is required because a controlling financial interest may be achieved other than by ownership of shares or voting interests. Under current U.S.

GAAP and the ASU, a decision maker is determined to be the primary beneficiary of a VIE and could consolidate if it satisfies both of the following power and economics criteria:  The “power” to direct the activities that most significantly impact the VIE’s economic performance  The obligation to absorb the losses of the VIE that could potentially be significant to the VIE, or the right to receive benefits from the VIE that potentially could be significant to the VIE, i.e., the “economics” The ASU replaces guidance for limited partnerships under the voting model (Subtopic 810-20) and introduces a separate analysis in the VIE model (Subtopic 810-10) for evaluating decision-making rights. The previous criteria for determining whether a limited partnership should be consolidated by a general partner now are used to determine whether a limited partnership or similar legal entity is a VIE. Today, a limited partnership typically would be a VIE if the general partner has not invested a substantive amount of equity. Under the new guidance, a limited partnership could be a VIE unless substantive kick-out or participating rights are exercisable either by a single limited partner or by a majority vote of all partners.

A different consolidation conclusion may be reached under the VIE model than under the voting model; additional disclosures would apply. This change would result in more entities being VIEs and have broad application, since limited partnership structures are utilized extensively in the asset management sector and in a number of other sectors such as oil and gas, transportation and real estate development. 7 . Update to Consolidation Guidelines Variable Interest Entities A reporting entity must first determine if it holds a variable interest in a VIE. The standard does not change the definition of a VIE. Variable interest entities:  Do not have sufficient equity to fund their operations  As a group have equity holders that lack any of the following characteristics: • • • The right to receive the expected residual returns Power to direct the activities most significantly impacting the entity’s economic performance The obligation to absorb the expected losses The ASU changes how reporting entities evaluate the decision maker’s fee arrangements, the effect of relatedparty interests on the primary beneficiary determination and the timing of the related-party tiebreaker test, which may lead to different consolidation conclusions. Effect of Noncontrolling Rights on Primary Beneficiary Determination Ownership of a majority voting interest is the usual condition for a controlling financial interest and consolidation. However, exceptions exist when noncontrolling shareholders have “substantive” participating rights. The powers of the majority shareholder or limited partner holding a majority of the kick-out rights may be restricted by approval or veto right granted to noncontrolling shareholders or other limited partners. The assessment of noncontrolling rights should be made at the time a majority voting interest or majority of kickout rights through voting interests is obtained.

Reassessment of noncontrolling interest would occur only if there is a significant change to the terms or the exercisability of the rights. Substantive Participating Rights To overcome the presumption of consolidation by the majority voting interest, the noncontrolling rights— individually or in the aggregate—must allow the noncontrolling shareholder or limited partner to effectively participate in certain significant investee financial and operating decisions in the ordinary course of business. For example, noncontrolling shareholders may be allowed to approve the operating budget, set management’s compensation or select and terminate management. These rights could preclude a majority shareholder from consolidating an entity due to substantive participating rights by the noncontrolling shareholder.

The factors for evaluating if participating rights are substantive remain unchanged from current GAAP, except for the inclusion of limited partner language. The factors are as follows:  Size of ownership interest in investee  Governing documents that indicate at what level decisions are made—at the shareholder, limited partner level or at the board level  Related-party relationships between the major and noncontrolling shareholders or partners  Noncontrolling rights covering insignificant business operations, e.g., location of headquarters, investee’s name, selection of auditors or accounting principles  Noncontrolling rights with a remote chance of occurring  Buyout rights The likelihood that a veto right will be exercised should not be considered when assessing whether that right is substantive. 8 . Update to Consolidation Guidelines Participating Rights – VIE Model – Partnerships Current U.S. GAAP The ability to block the actions through which a reporting entity exercises the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance New Model The ability to block or participate in the actions through which an entity exercises the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance Holders of participating rights are not required to have the ability to initiate actions Protective Rights Protective rights are designed to protect the interests of the rights holder without giving that party a controlling interest. Such rights allow the holder to block corporate or partnership actions. Examples of noncontrolling protective rights include, but are not limited to:  Amendments to articles of incorporation or partnership agreements  Transaction pricing on self-dealing activities  Liquidation of the investee  Acquisitions and dispositions not in the ordinary course of business  Issuance or repurchase of equity interests Protective rights alone would not overcome the presumption of consolidation by the majority voting interest or the limited partner with a majority of kick-out rights.

However, other rights that allow participation in significant financial and operating decisions, although also protective in nature, could overcome the presumption of consolidation by the majority voting interest. The assessment of noncontrolling rights is a matter of judgment that will depend on facts and circumstances. Kick-Out Rights The right to remove the general partner is considered a kick-out right. In addition, if a general partner has outsourced management, a limited partner’s right to terminate management may be a substantive participating right. Judgment will be required to determine whether kick-out rights are substantive.

For kick-out rights to be considered substantive, there can be no significant barrier for the limited partner to exercise those rights. Examples of barriers include:  Narrow limits on timing of exercise  Financial penalties or operational barriers to liquidating the partnership or replacing general partners  Lack of qualified replacement general partners or inadequate compensation for qualified replacement general partners  Limited ability for limited partners to call for and conduct vote to exercise rights  Lack of information for limited partners to exercise rights 9 . Update to Consolidation Guidelines Kick-Out Rights – VIE Definition Current U.S. GAAP New Model The ability to remove the reporting entity with the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance The ability to remove the entity with the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance or to dissolve (liquidate) the VIE without cause Redemption Rights Redemption rights represent an entity’s obligation to return invested capital upon investor request. FASB concluded redemption rights are inherently different from liquidation rights because the decision maker can avoid being kicked out by obtaining additional investors for the entity; therefore, redemption rights would not be considered equivalent to kick-out rights. Redemption Rights Current U.S. GAAP New Model The limited partners’ unilateral right to withdraw from the partnership in whole or in part (withdrawal right) that does not require dissolution or liquidation of the entire limited partnership would not overcome the presumption that the general partners control the limited partnership The limited partners’ unilateral right to withdraw from the partnership in whole or in part (withdrawal right) that does not require dissolution or liquidation of the entire limited partnership would not be deemed a kick-out right Consolidation Based on Variable Interests A reporting entity that concludes it has a variable interest in a VIE would have to evaluate whether it is the entity’s primary beneficiary and should consolidate the VIE.

That determination is based on a qualitative assessment on whether it has both of the following:  Power to direct the activities most significantly impacting the VIE’s economic performance  Obligation to absorb losses of the VIE or the right to receive benefits from the VIE Only one reporting entity can be the primary beneficiary. Although more than one reporting entity may be able to absorb the losses of a VIE, only one entity will have the power to direct the VIE’s most significant activities. Kick-out rights and participating rights should not affect the “power to direct” determination unless a single reporting entity (including related parties and de facto agent) has the unilateral ability to exercise those rights. Protective rights held by others do not preclude a reporting entity from having the power to direct the VIE’s most significant activities. If the activities impacting the VIE’s economic performance are directed by multiple unrelated parties and the nature of the activities each party directs is not the same, a reporting entity would identify which party has the power to direct the activities most significantly impacting the VIE’s economic performance. If power is shared among multiple unrelated parties such that no one party has the power to direct the most significant activities of a VIE, no party is the primary beneficiary. If power is not shared but multiple unrelated parties direct significant economic activities, then the party, if any, with the power over the majority of those activities is considered the primary beneficiary. 10 . Update to Consolidation Guidelines Fees Paid to Decision Makers Fees received by decision makers or service providers may represent a variable interest in any entity depending on facts and circumstances. Current U.S. GAAP contains six criteria to conclude fees do not represent a variable interest in an entity. The ASU eliminates three of those criteria, as noted in the table below: Criteria Eliminated in the New Model Criteria Retained in the New Model The fees are at or above the same level of seniority as other operating liabilities of the entity that arise in the normal course of business, such as trade payables The fees are compensation for services provided and are commensurate with the level of effort required to provide those services The anticipated fees are insignificant relative to the total amount of the VIE’s anticipated economic performance The service agreement includes only terms, conditions or amounts customarily present in arrangements for similar services negotiated at arm’s length The total amount of fees are expected to absorb an insignificant amount of the variability associated with the VIE’s anticipated economic performance The decision maker or service provider does not hold other interests in the VIE that, individually or in the aggregate, would absorb more than an insignificant amount of the VIE’s expected losses or expected residual returns No further consolidation analysis would be required under the VIE model if fees are at market and commensurate with services provided, assuming the decision maker holds no other economic interests through its related parties, directly or indirectly, that absorb more than an insignificant amount of the VIE’s losses or returns.

By removing requirements related to fee size, seniority and ability to absorb the VIE’s losses, fewer fee arrangements are expected to be variable interests. Significant judgment will be required in the application of the second criteria for new or unique services. Such arrangements would not presumptively fail the assessment, but additional documentation may be required to support exclusion. In addition, the magnitude of a fee, in isolation, would not cause an arrangement to fail. The ASU added an anti-abuse provision to prevent structuring opportunities by absorbing risk of loss through fee arrangements.

Fee arrangements that expose a reporting entity to risk of loss in the VIE would not be eligible for exclusion. Examples of such arrangements include, but are not limited to, the following:  Guarantees of the value of the VIE’s assets or liabilities  Obligations to fund operating losses  Payments associated with written put options on the VIE’s assets  Liquidity commitments or similar obligations that protect holders of other interests from VIE losses In addition, fees paid to a decision maker that are at market and commensurate with services provided would be excluded from consideration in the benefits criteria for determining the primary beneficiary of a VIE. Related Parties The existence of related parties can significantly affect conclusions reached when analyzing whether VIEs require consolidation. The new standard incorporates related-party interests earlier in the analysis for a party with power and reduces situations where the “related-party tiebreaker” test is performed. Under current guidance, a reporting entity performs the power and economics tests on a standalone basis.

Only if the reporting entity does not meet both tests on a standalone basis does the reporting entity consider related parties in the analysis. Under the ASU, a reporting entity that meets the power test on a standalone basis would only include related-party interests in the economics analysis. 11 . Update to Consolidation Guidelines Proportional Basis The decision maker for both partnerships and VIEs is required to consider any indirect interests held through related parties. A decision maker should include a proportionate amount of these interests in the primary beneficiary analysis, except when the related parties with an indirect interest are under common control. In addition, employee’s interests should be considered in the indirect assessment if the decision maker finances them. Example 1 A single decision maker owns a 20 percent interest in a related party and that related party owns a 40 percent interest in the entity being evaluated; the single decision maker’s interest would be considered equivalent to an 8 percent direct interest in the VIE for purposes of evaluating controlling interest. Example 2 Employees of the decision maker have a 30 percent VIE interest, of which one third was financed by the decision maker; the single decision maker’s interest would be considered a 10 percent direct interest of the VIE. Related Parties Current U.S. GAAP An entity is required to consider the entire interest held by the related party New Model Decision maker should consider a proportionate interest in related-party interest held Related-Party Tie Breaker Sometimes, a reporting entity does not individually have the characteristics of a primary beneficiary, but when considered together with its related parties, the related-party group has characteristics of a primary beneficiary. Currently, a “related-party tiebreaker” test is performed to identify the variable interest holder within the relatedparty group that is “most closely associated” to the VIE and would consolidate. The ASU limits the application of the tiebreaker test to when both:  Power is shared among related parties  Substantially all of the VIE’s activities are conducted on behalf of one of the variable interest holders in the related-party group; this should be a qualitative assessment, though quantitative information may be considered Entities that apply ASU 2014-01, Investments – Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Qualified Affordable Housing Projects, are exempt from this provision. The ASU does not change the primary beneficiary determination when there are multiple decision makers. Voting Interest Entity (VOE) Model Entities subject to a scope exception from the VIE model or not qualifying as a VIE would be evaluated for consolidation under the VOE model.