GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions

BKD

Description

GASB Issues Final Rules Governing Reporting for

Postemployment Benefits Other Than Pensions

. GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions

Table of Contents

EXECUTIVE SUMMARY ........................................................................................................................................... 3

GASB 75 – EMPLOYER STANDARD.......................................................................................................................... 5

BACKGROUND & IMPACT OF CHANGE ................................................................................................................................5

SCOPE ..........................................................................................................................................................................5

CALCULATING OPEB LIABILITIES & EXPENSE .......................................................................................................................7

Total OPEB Liability ...............................................................................................................................................8

Projecting Total OPEB Liability ..............................................................................................................................8

Discounting .........................................................................................................................................................11

Allocating ............................................................................................................................................................11

NET OPEB LIABILITY.....................................................................................................................................................11

Cost-Sharing Employers ......................................................................................................................................12

Special Funding Situation ....................................................................................................................................12

NOTES TO FINANCIAL STATEMENTS & REQUIRED SUPPLEMENTARY INFORMATION ....................................................................12

IMPLEMENTATION & TRANSITION ....................................................................................................................................13

CONTRIBUTOR ..................................................................................................................................................... 13

SUMMARY SCOPE & EFFECTIVE DATES OF GASB STATEMENTS NO.

75 & NO. 74 ................................................. 14 2 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Executive Summary The Governmental Accounting Standards Board (GASB) has issued GASB Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions (GASB 75). For reporting periods beginning after June 15, 2017, governments will recognize their unfunded accrued other postemployment benefits (OPEB) obligation on the face of their financial statements. OPEB comprises mostly postemployment health care benefits and can represent a very significant liability for many state and local governments, especially if the government has set aside few assets to pay for those benefits.

OPEB also may include death benefits, life insurance, disability and long-term care. The new reporting requirements on OPEB parallel the changes for pension plan accounting included in Statement No. 67, Financial Reporting for Pension Plans—an amendment of GASB Statement No. 25, and Statement No.

68, Accounting and Financial Reporting for Pensions—an amendment of GASB Statement No. 27. Together, the standards provide consistent and comprehensive guidance to state and local governments for all postemployment benefits.

State and local governments currently are implementing the new pension standards, and financial statement users soon should have a more thorough understanding of the cost of significant pension and OPEB obligations. In addition to looking at GASB 75, this paper provides a brief overview of Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans, and Statement No. 73, Accounting and Financial Reporting for Pensions and Related Assets That Are Not within the Scope of GASB Statement 68, and Amendments to Certain Provisions of GASB Statements 67 and 68.

Although Statement 75 is effective for periods beginning after June 15, 2017, earlier application is encouraged. GASB 75—the standard for employers providing OPEB—addresses accounting and financial reporting for OPEB provided to the employees of state and local governmental employers and governments that finance OPEB plans for employees of other governments. The effects of GASB 75 are different for each type of OPEB plan:  Governments responsible only for OPEB liabilities related to their own employees and that provide OPEB through a defined benefit OPEB plan administered through a trust meeting specified criteria will report a net OPEB liability. The net OPEB liability represents the difference between the total OPEB liability and assets accumulated in a trust restricted to making benefit payments, where contributions are irrevocable and the OPEB plan assets are beyond the reach of creditors.  Governments participating in a cost-sharing OPEB plan administered through a trust that meets the specified criteria will report a liability equal to their proportionate share of the collective OPEB liability for all entities participating in the cost-sharing plan.  Governments that do not provide OPEB through a trust meeting the specified criteria will report the total OPEB liability related to their employees.  Governments legally responsible to make contributions directly to an OPEB plan or make benefit payments directly as OPEB comes due for employees of other governments—in certain circumstances called special funding situations—are required to recognize in their financial statements a share of the other government’s net OPEB liability. 3 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions The method a government will use to report and calculate its OPEB liability and annual expense for defined benefit OPEB plans administered through a trust meeting specified criteria will change significantly. For defined benefit OPEB, GASB 75 identifies the methods and assumptions required to project benefit payments, discount projected benefit payments to their actuarial present value and attribute that present value to periods of employee service. The changes include the following:  Requiring projected benefit payments to be discounted to their actuarial present value using a single rate that reflects the following: • • A long-term expected rate of return on OPEB plan investments, to the extent the OPEB plan’s fiduciary net position is projected to be sufficient to make projected benefit payments and OPEB plan assets are expected to be invested using a strategy to achieve that return A tax-exempt, high-quality municipal bond rate, to the extent the conditions for use of the longterm expected rate of return are not met  Requiring the use of a single actuarial cost allocation method: the “entry age actuarial cost method”  Requiring governments in all types of OPEB plans to present more extensive note disclosures and required supplementary information (RSI) about their OPEB liabilities GASB 75 carries forward from GASB 45 the option to use a specified alternative measurement method instead of an actuarial valuation for purposes of determining the total OPEB liability for benefits provided through OPEB plans in which there are fewer than 100 plan members (active and inactive). GASB 74—the standard for OPEB plans—provides guidance for reporting by OPEB plans that administer the OPEB benefits on behalf of governments. Its provisions are effective for financial statements for periods beginning after June 15, 2016 (one year earlier than GASB 75), with earlier application also encouraged. Similar to GASB 75 for employers, GASB 74 addresses the financial reports of defined benefit OPEB plans administered through trusts meeting defined criteria and addresses how plans should report assets accumulated through defined benefit OPEB plans not administered through trusts meeting the criteria. GASB 74 also requires certain note disclosure for defined contribution OPEB plans administered through trusts meeting the defined criteria. OPEB plans within the scope of GASB 74 will prepare a statement of fiduciary net position and a statement of changes in fiduciary net position.

Similar to GASB 75, GASB 74 requires more extensive note disclosures and RSI related to the measurement of the OPEB liabilities for which assets have been accumulated, including information about the annual money-weighted rates of return on plan investments. GASB 73—the supplemental pension standard—provides standards for pensions and pension plans not covered by GASB 67 and 68 (plans not administered through a trust meeting specified criteria). GASB 73 completes the suite of pension standards. The requirements in GASB 73 for reporting pensions generally are the same as GASB 68. However, similar to GASB 75, measurement differences are applicable to a pension plan not administered through a trust meeting specified criteria. 4 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions GASB 75 – Employer Standard Background & Impact of Change Under extant GASB 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions, a government is required to estimate and record the cost of benefits promised to employees as those employees provide services to the government and its constituents. GASB 75 enhances the accuracy of the information about the total cost of service a government provides to its constituents. For governments that do not pay or contribute for OPEB but defer the costs to future periods, the financial statements of these entities will continue to reflect a higher OPEB liability than those governments funding their obligations on an annual basis as OPEB costs are incurred. OPEB liabilities—similar to pension liabilities—are amounts disclosing the cash-flow demands on the government and its taxpayers or rate payers in future years; these have only gained importance to the diverse users of a government’s financial statements since GASB 45. The significance of GASB 75 is the change in definition of a government’s OPEB liability, measurement requirements of a government’s OPEB liability and its effects on annual OPEB cost recognition, particularly in the year of implementation. Under GASB 45, a government’s unfunded OPEB obligation (unfunded actuarial accrued liability) is disclosed in the footnotes. A government’s accrual-based liability (net OPEB obligation) recorded on the face of the financial statements represents the amount its actual OPEB contributions is less than its annual OPEB cost—the employer’s annual required contribution (ARC) to the plan—with certain adjustments if the employer has a net OPEB obligation for past undercontributions or overcontributions. In the initial year of adoption of GASB 75, however, governments generally will immediately report a financial statement liability for its share of the entire unfunded OPEB liability (net OPEB liability), with certain adjustments for amortizable items.

GASB 75 will particularly affect employer and nonemployer governments participating in cost-sharing OPEB plans. GASB 75 brings the liability up to the face of the financial statements. For governments with a pay-as-you-go OPEB financing system, the net OPEB obligation accumulated rapidly since GASB 45 and will continue to do so under GASB 75. Likewise, the requirement under GASB 45 to disclose information about the funded status of a plan still exists.

The unfunded liability, however, will be reported on the face of the financial statements under GASB 75. In governmental fund financial statements, the measurement focus is on current financial resources; statements are prepared under the modified accrual basis of accounting (as opposed to governmentwide financial statements where the measurement focus is on economic resources and statements are prepared under the accrual basis of accounting). As such, governmental funds will recognize a net OPEB liability to the extent the liability is normally expected to be liquidated with expendable available financial resources (benefit payments have matured and the OPEB plan’s fiduciary net position is not sufficient for payment of those benefits). OPEB expenditures are recognized equal to the total of the following:  Amounts paid by the employer to the OPEB plan, including amounts paid for OPEB as benefits come due  The change between the beginning and ending balances of amounts normally expected to be liquidated with expendable available financial resources Scope As with superseded GASB 45, the new OPEB standard does not enforce OPEB funding or payment obligations—a policy decision made by government officials—instead, it establishes new measurement and reporting requirements to more clearly depict the government’s financial position.

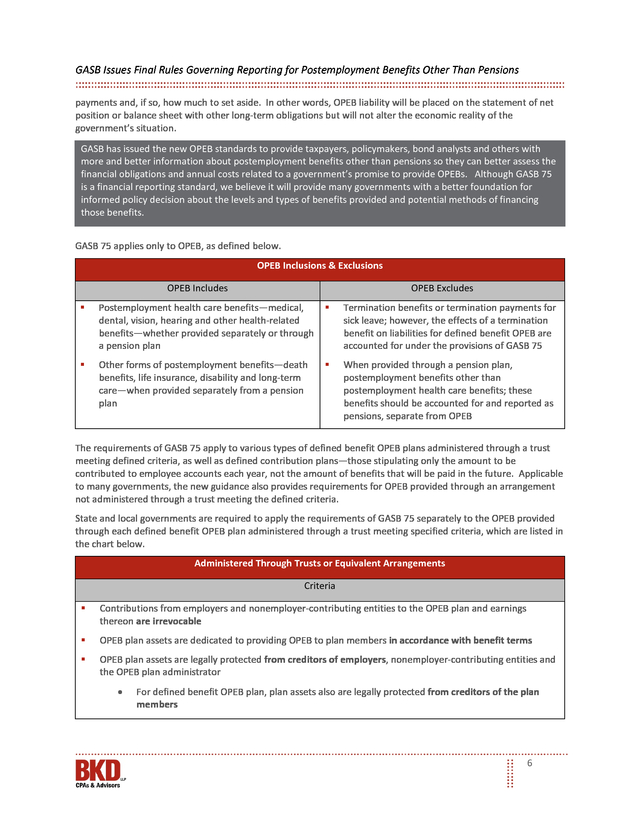

Likewise, the standards do not address how a government measures OPEB for the purpose of determining whether to set assets aside to fund future OPEB 5 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions payments and, if so, how much to set aside. In other words, OPEB liability will be placed on the statement of net position or balance sheet with other long-term obligations but will not alter the economic reality of the government’s situation. GASB has issued the new OPEB standards to provide taxpayers, policymakers, bond analysts and others with more and better information about postemployment benefits other than pensions so they can better assess the financial obligations and annual costs related to a government’s promise to provide OPEBs. Although GASB 75 is a financial reporting standard, we believe it will provide many governments with a better foundation for informed policy decision about the levels and types of benefits provided and potential methods of financing those benefits. GASB 75 applies only to OPEB, as defined below. OPEB Inclusions & Exclusions OPEB Includes OPEB Excludes  Postemployment health care benefits—medical, dental, vision, hearing and other health-related benefits—whether provided separately or through a pension plan  Termination benefits or termination payments for sick leave; however, the effects of a termination benefit on liabilities for defined benefit OPEB are accounted for under the provisions of GASB 75  Other forms of postemployment benefits—death benefits, life insurance, disability and long-term care—when provided separately from a pension plan  When provided through a pension plan, postemployment benefits other than postemployment health care benefits; these benefits should be accounted for and reported as pensions, separate from OPEB The requirements of GASB 75 apply to various types of defined benefit OPEB plans administered through a trust meeting defined criteria, as well as defined contribution plans—those stipulating only the amount to be contributed to employee accounts each year, not the amount of benefits that will be paid in the future. Applicable to many governments, the new guidance also provides requirements for OPEB provided through an arrangement not administered through a trust meeting the defined criteria. State and local governments are required to apply the requirements of GASB 75 separately to the OPEB provided through each defined benefit OPEB plan administered through a trust meeting specified criteria, which are listed in the chart below. Administered Through Trusts or Equivalent Arrangements Criteria  Contributions from employers and nonemployer-contributing entities to the OPEB plan and earnings thereon are irrevocable  OPEB plan assets are dedicated to providing OPEB to plan members in accordance with benefit terms  OPEB plan assets are legally protected from creditors of employers, nonemployer-contributing entities and the OPEB plan administrator • For defined benefit OPEB plan, plan assets also are legally protected from creditors of the plan members 6 .

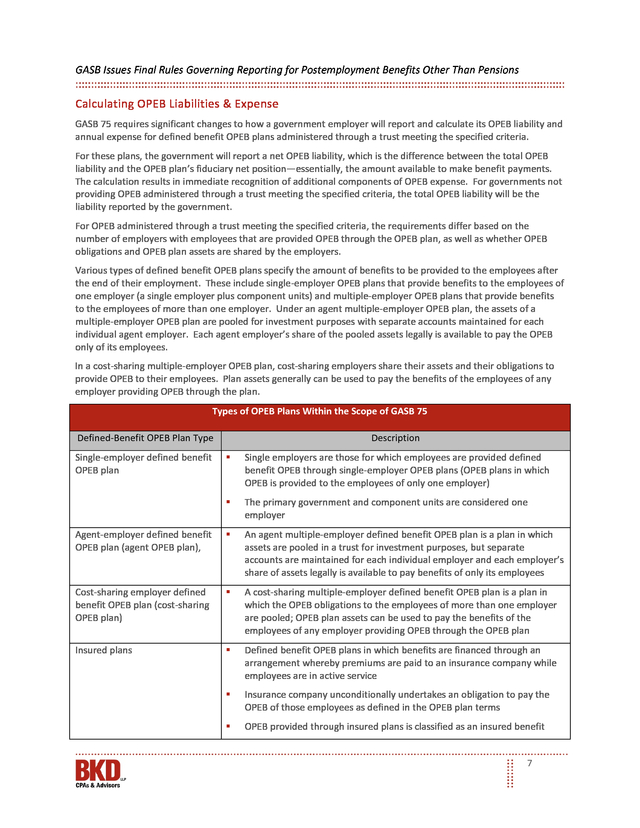

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Calculating OPEB Liabilities & Expense GASB 75 requires significant changes to how a government employer will report and calculate its OPEB liability and annual expense for defined benefit OPEB plans administered through a trust meeting the specified criteria. For these plans, the government will report a net OPEB liability, which is the difference between the total OPEB liability and the OPEB plan’s fiduciary net position—essentially, the amount available to make benefit payments. The calculation results in immediate recognition of additional components of OPEB expense. For governments not providing OPEB administered through a trust meeting the specified criteria, the total OPEB liability will be the liability reported by the government. For OPEB administered through a trust meeting the specified criteria, the requirements differ based on the number of employers with employees that are provided OPEB through the OPEB plan, as well as whether OPEB obligations and OPEB plan assets are shared by the employers. Various types of defined benefit OPEB plans specify the amount of benefits to be provided to the employees after the end of their employment. These include single-employer OPEB plans that provide benefits to the employees of one employer (a single employer plus component units) and multiple-employer OPEB plans that provide benefits to the employees of more than one employer. Under an agent multiple-employer OPEB plan, the assets of a multiple-employer OPEB plan are pooled for investment purposes with separate accounts maintained for each individual agent employer.

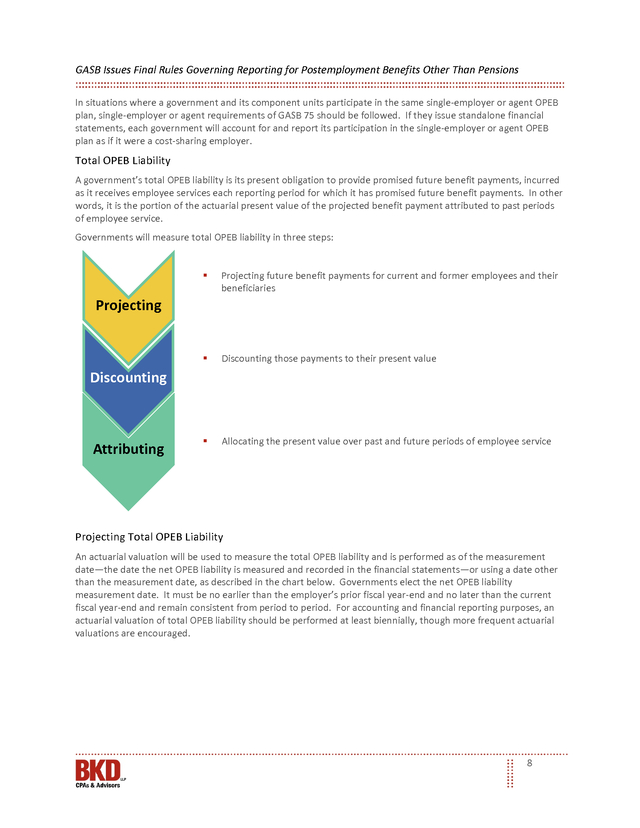

Each agent employer’s share of the pooled assets legally is available to pay the OPEB only of its employees. In a cost-sharing multiple-employer OPEB plan, cost-sharing employers share their assets and their obligations to provide OPEB to their employees. Plan assets generally can be used to pay the benefits of the employees of any employer providing OPEB through the plan. Types of OPEB Plans Within the Scope of GASB 75 Defined-Benefit OPEB Plan Type Single-employer defined benefit OPEB plan Description  Single employers are those for which employees are provided defined benefit OPEB through single-employer OPEB plans (OPEB plans in which OPEB is provided to the employees of only one employer)  The primary government and component units are considered one employer Agent-employer defined benefit OPEB plan (agent OPEB plan),  An agent multiple-employer defined benefit OPEB plan is a plan in which assets are pooled in a trust for investment purposes, but separate accounts are maintained for each individual employer and each employer’s share of assets legally is available to pay benefits of only its employees Cost-sharing employer defined benefit OPEB plan (cost-sharing OPEB plan)  A cost-sharing multiple-employer defined benefit OPEB plan is a plan in which the OPEB obligations to the employees of more than one employer are pooled; OPEB plan assets can be used to pay the benefits of the employees of any employer providing OPEB through the OPEB plan Insured plans  Defined benefit OPEB plans in which benefits are financed through an arrangement whereby premiums are paid to an insurance company while employees are in active service  Insurance company unconditionally undertakes an obligation to pay the OPEB of those employees as defined in the OPEB plan terms  OPEB provided through insured plans is classified as an insured benefit 7 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions In situations where a government and its component units participate in the same single-employer or agent OPEB plan, single-employer or agent requirements of GASB 75 should be followed. If they issue standalone financial statements, each government will account for and report its participation in the single-employer or agent OPEB plan as if it were a cost-sharing employer. Total OPEB Liability A government’s total OPEB liability is its present obligation to provide promised future benefit payments, incurred as it receives employee services each reporting period for which it has promised future benefit payments. In other words, it is the portion of the actuarial present value of the projected benefit payment attributed to past periods of employee service. Governments will measure total OPEB liability in three steps:  Projecting future benefit payments for current and former employees and their beneficiaries  Discounting those payments to their present value  Allocating the present value over past and future periods of employee service Projecting Discounting Attributing Projecting Total OPEB Liability An actuarial valuation will be used to measure the total OPEB liability and is performed as of the measurement date—the date the net OPEB liability is measured and recorded in the financial statements—or using a date other than the measurement date, as described in the chart below. Governments elect the net OPEB liability measurement date.

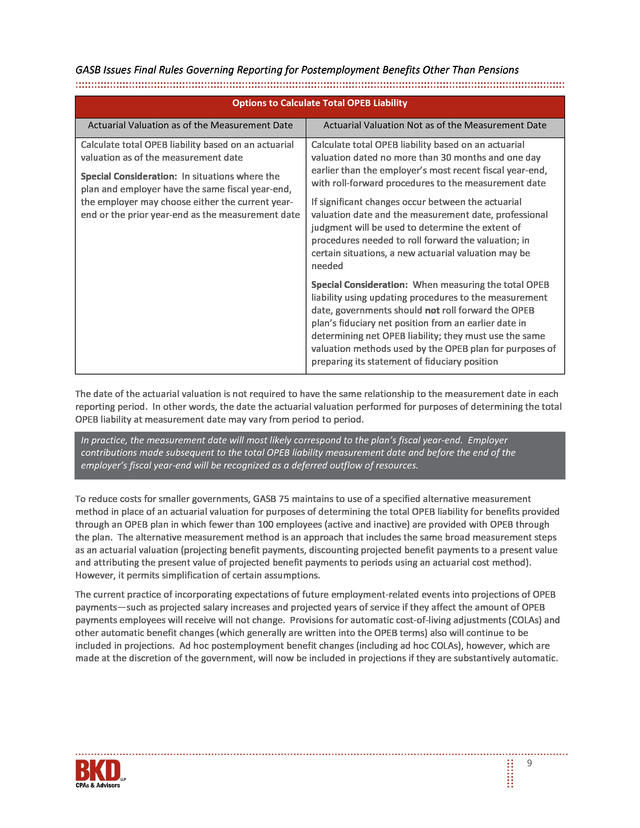

It must be no earlier than the employer’s prior fiscal year-end and no later than the current fiscal year-end and remain consistent from period to period. For accounting and financial reporting purposes, an actuarial valuation of total OPEB liability should be performed at least biennially, though more frequent actuarial valuations are encouraged. 8 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Options to Calculate Total OPEB Liability Actuarial Valuation as of the Measurement Date Actuarial Valuation Not as of the Measurement Date Calculate total OPEB liability based on an actuarial valuation as of the measurement date Calculate total OPEB liability based on an actuarial valuation dated no more than 30 months and one day earlier than the employer’s most recent fiscal year-end, with roll-forward procedures to the measurement date Special Consideration: In situations where the plan and employer have the same fiscal year-end, the employer may choose either the current yearend or the prior year-end as the measurement date If significant changes occur between the actuarial valuation date and the measurement date, professional judgment will be used to determine the extent of procedures needed to roll forward the valuation; in certain situations, a new actuarial valuation may be needed Special Consideration: When measuring the total OPEB liability using updating procedures to the measurement date, governments should not roll forward the OPEB plan’s fiduciary net position from an earlier date in determining net OPEB liability; they must use the same valuation methods used by the OPEB plan for purposes of preparing its statement of fiduciary position The date of the actuarial valuation is not required to have the same relationship to the measurement date in each reporting period. In other words, the date the actuarial valuation performed for purposes of determining the total OPEB liability at measurement date may vary from period to period. In practice, the measurement date will most likely correspond to the plan’s fiscal year-end. Employer contributions made subsequent to the total OPEB liability measurement date and before the end of the employer’s fiscal year-end will be recognized as a deferred outflow of resources. To reduce costs for smaller governments, GASB 75 maintains to use of a specified alternative measurement method in place of an actuarial valuation for purposes of determining the total OPEB liability for benefits provided through an OPEB plan in which fewer than 100 employees (active and inactive) are provided with OPEB through the plan. The alternative measurement method is an approach that includes the same broad measurement steps as an actuarial valuation (projecting benefit payments, discounting projected benefit payments to a present value and attributing the present value of projected benefit payments to periods using an actuarial cost method). However, it permits simplification of certain assumptions. The current practice of incorporating expectations of future employment-related events into projections of OPEB payments—such as projected salary increases and projected years of service if they affect the amount of OPEB payments employees will receive will not change.

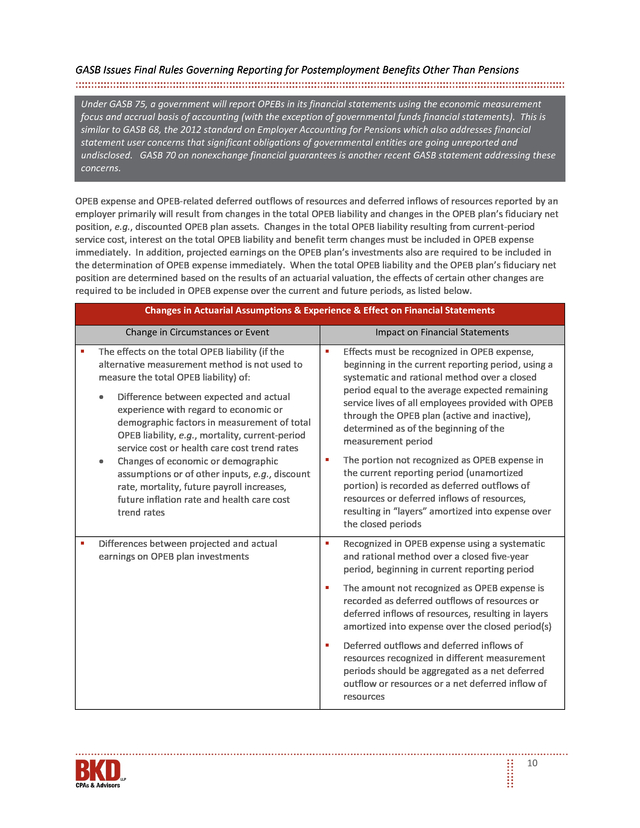

Provisions for automatic cost-of-living adjustments (COLAs) and other automatic benefit changes (which generally are written into the OPEB terms) also will continue to be included in projections. Ad hoc postemployment benefit changes (including ad hoc COLAs), however, which are made at the discretion of the government, will now be included in projections if they are substantively automatic. 9 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Under GASB 75, a government will report OPEBs in its financial statements using the economic measurement focus and accrual basis of accounting (with the exception of governmental funds financial statements). This is similar to GASB 68, the 2012 standard on Employer Accounting for Pensions which also addresses financial statement user concerns that significant obligations of governmental entities are going unreported and undisclosed. GASB 70 on nonexchange financial guarantees is another recent GASB statement addressing these concerns. OPEB expense and OPEB-related deferred outflows of resources and deferred inflows of resources reported by an employer primarily will result from changes in the total OPEB liability and changes in the OPEB plan’s fiduciary net position, e.g., discounted OPEB plan assets. Changes in the total OPEB liability resulting from current-period service cost, interest on the total OPEB liability and benefit term changes must be included in OPEB expense immediately.

In addition, projected earnings on the OPEB plan’s investments also are required to be included in the determination of OPEB expense immediately. When the total OPEB liability and the OPEB plan’s fiduciary net position are determined based on the results of an actuarial valuation, the effects of certain other changes are required to be included in OPEB expense over the current and future periods, as listed below. Changes in Actuarial Assumptions & Experience & Effect on Financial Statements Change in Circumstances or Event  The effects on the total OPEB liability (if the alternative measurement method is not used to measure the total OPEB liability) of: • •  Difference between expected and actual experience with regard to economic or demographic factors in measurement of total OPEB liability, e.g., mortality, current-period service cost or health care cost trend rates Changes of economic or demographic assumptions or of other inputs, e.g., discount rate, mortality, future payroll increases, future inflation rate and health care cost trend rates Differences between projected and actual earnings on OPEB plan investments Impact on Financial Statements  Effects must be recognized in OPEB expense, beginning in the current reporting period, using a systematic and rational method over a closed period equal to the average expected remaining service lives of all employees provided with OPEB through the OPEB plan (active and inactive), determined as of the beginning of the measurement period  The portion not recognized as OPEB expense in the current reporting period (unamortized portion) is recorded as deferred outflows of resources or deferred inflows of resources, resulting in “layers” amortized into expense over the closed periods  Recognized in OPEB expense using a systematic and rational method over a closed five-year period, beginning in current reporting period  The amount not recognized as OPEB expense is recorded as deferred outflows of resources or deferred inflows of resources, resulting in layers amortized into expense over the closed period(s)  Deferred outflows and deferred inflows of resources recognized in different measurement periods should be aggregated as a net deferred outflow or resources or a net deferred inflow of resources 10 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Governments will report employer contributions, subsequent to the net OPEB liability measurement date and before the end of the reporting period, on the Statement of Net Position (Balance Sheet) as deferred outflows of resources. In the year immediately following recognition of the deferred outflow of resources, the government will recognize the contribution as a reduction of the net OPEB liability. Discounting GASB 75 has specified the discount rate government employers will use to discount projected benefit payments or projected total OPEB liability. As long as plan assets related to current active and inactive employees and their beneficiaries are projected to be sufficient to make the projected benefit payments for those individuals, governments will discount those projected benefit payments using the long-term expected rate of return on OPEB plan investments (net of investment expenses). In this case, OPEB plan assets must be expected to be invested using a strategy that will achieve that return. However, some governments will have a crossover point at which the plan assets are projected to be insufficient to make projected benefit payments to current active and inactive employees and their beneficiaries.

GASB believes the projected benefit payments occurring thereafter are similar to other forms of debt. In this circumstance, the discount rate will be based on a tax-exempt, high-quality 20-year tax-exempt general obligation municipal bond yield or index rate. (High quality would be defined as rated at least AA/Aa or an equivalent rating.) In a situation where no assets have been accumulated in an OPEB trust—which is not uncommon—all projected benefit payments will be discounted using the municipal bond rate.

Accordingly, underfunded plans will use the municipal bond rate for at least a portion of discounting. The lower municipal bond rate will result in an increased total OPEB liability compared to well-funded plans using the long-term expected rate of return on OPEB plan investments. Allocating Under current requirements, governments can choose from six methods for attributing the present value of benefit payments to specific years either in level dollar amounts, similar to a mortgage, or as a level percentage of projected payroll. GASB 75 requires all governments to use the entry age actuarial cost method to allocate present value and to do so as a level percentage of pay.

The actuarial present value will be attributed to each employee individually, from the first period in which the employee provides services under the benefit terms through the period in which the employee exits active service, e.g., the expected period of employment. GASB believes this pattern reflects the ongoing annual exchange of service for benefits over the course of an employee’s period of employment in amounts that keep pace with the employee’s projected salary over that period. Net OPEB Liability A government is only required to recognize its actual OPEB liability, meaning it will net the discounted projected benefit payments (discounted total OPEB liability) against the OPEB plan’s fiduciary net position—the primary resources that will be used to pay the OPEB. This liability is referred to as the net OPEB liability. As previously mentioned, in financial statements prepared using the economic resources measurement focus and accrual basis of accounting, a single or agent employer without a special funding situation must recognize a liability equal to the net OPEB liability.

The net OPEB liability is required to be measured as of a date no earlier than the employer’s prior fiscal year-end and no later than the current fiscal year-end (the measurement date), consistently applied from period to period. Governments must ensure the “OPEB plan’s fiduciary net position” is calculated using the same valuation methods as the OPEB plan for purposes of preparing its statement of fiduciary net position. For footnote disclosure purposes, employers may refer to the OPEB plan’s basic financial statements, with respect to the fiduciary net position, if the OPEB plan’s financial statements are available online. 11 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Cost-Sharing Employers Cost-sharing governmental employers without a special funding situation will recognize a liability for their proportionate share of the collective net OPEB liability, e.g., the net liability of all employers for benefits provided through the OPEB plan, measured using the same measurement date criteria as single and agent plans. The basis for determining each employer’s proportion should be consistent with the manner in which contributions to the OPEB plan are determined. Use of the employer’s projected long-term contribution effort to the OPEB plan compared to the total projected long-term contribution effort of all employers and all nonemployer contributing entities is encouraged. Special provisions apply to governmental fund financial statements. Under the new guidance, a cost-sharing employer is required to recognize a liability for its proportionate share of the collective net pension liability.

Thus, similar to GASB 68, cost-sharing employers without a special funding situation are expected to experience the largest impact of GASB 75 due to previously unrecorded liabilities. As a result, entities may need to evaluate their ability to continue as a going concern under GASB 56 and consider, as applicable, having going concern discussions with their auditors. However, the going concern evaluation prescribed in GASB 56 suggests a 15-month period subsequent to the current year-end is sufficient for a going concern evaluation; the current portion of the OPEB liability probably will not be significant enough to create a going concern uncertainty in most instances. Special Funding Situation An employer with a special funding situation for a defined benefit OPEB will recognize an OPEB liability and deferred outflows of resources or deferred inflows of resources related to OPEB, with adjustments for the involvement of nonemployer contributing entities. For a single or agent employer with a special funding situation, its net OPEB liability represents the employer’s proportionate share of the collective net OPEB liability.

Special funding situations are circumstances in which a nonemployer entity legally is responsible for providing financial support for OPEB of the employees of another entity by making contributions directly to an OPEB plan administered through a trust or, if not administered through a trust, by making benefit payments directly as the OPEB comes due. Notes to Financial Statements & Required Supplementary Information GASB 75 requires governments in all types of OPEB plans to present more extensive note disclosures and RSI about their OPEB liabilities. Single and agent employers will include descriptive information, such as the types of benefits provided and the number and classes of employees covered by the benefit terms. Additional disclosures include, among numerous other disclosures, the following:  For the current year, sources of changes in the net OPEB liability  Significant assumptions and other inputs used to calculate the total OPEB liability, including those about inflation, the health care cost trend rate, salary changes, ad hoc postemployment benefit changes (including ad hoc COLAs) and inputs to the discount rate, as well as certain information about mortality assumptions and the dates of experience studies, e.g., a description of the effect on the reported OPEB liability of using a discount rate and a health care cost trend rate that are one percentage point higher and one percentage point lower than assumed by the government  The date of the actuarial valuation or calculation using the alternative measurement method used to determine the total OPEB liability, information about changes of assumptions or other inputs and benefit terms, the basis for determining employer contributions to the OPEB plan and information about the purchase, if any, of allocated insurance contracts 12 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Single and agent employers must present the following in RSI, determined as of the measurement date, for each of the 10 most recent fiscal years:  A schedule of changes in the net OPEB liability  Components of the net OPEB liability and related ratios, including the OPEB plan’s fiduciary net position as a percentage of the total OPEB liability, and the net OPEB liability as a percentage of covered-employee payroll The two schedules above can be combined into one schedule. Significant methods and assumptions used in calculating the actuarially determined contributions, if applicable, are required to be presented as notes to the RSI. In addition, the employer must explain certain factors significantly affecting trends in the amounts reported in the schedules. For actuarially determined contributions, a single or agent employer is required to present a schedule covering each of the 10 most recent fiscal years including the actuarially determined contribution, contributions to the OPEB plan and related ratios. If a single or agent employer instead has a contribution requirement established by statute or contract, the employer must present a schedule covering each of the 10 most recent fiscal years including information about the statutorily or contractually required contribution rates, contributions to the OPEB plan and related ratios. Amounts for these schedules should be determined as of the employer’s most recent fiscal year-end. Cost-sharing employers’ RSI will include a 10-year schedule showing certain proportionate share information and a 10-year schedule if contribution requirements of the employer are statutorily or contractually established. Implementation & Transition Until GASB 75 becomes effective in fiscal years beginning after June 15, 2017, or earlier if the provisions are adopted early, all provisions of GASB 45 for accounting and reporting of OPEBs remain in effect. Changes adopted to conform to the provisions of this statement should be applied retroactively by restating financial statements, if practical, for all prior periods presented.

Special transition provisions are provided for deferred inflows of resources and deferred outflows of resources. If restatement of all prior periods presented is not practical, the cumulative effect, if any, of applying GASB 75 should be reported as a restatement of beginning net position (or fund balance or fund net position, as applicable) for the earliest period restated. In the first period for which GASB 75 is applied, the notes to the financial statements should disclose the nature of the restatement and its effect, including whether restatement of beginning balances includes deferred outflows of resources or deferred inflows of resources, as applicable. The reason for not restating prior periods presented should be disclosed. During the transition period, when information for the RSI required 10-year schedules is not available for all fiscal years, that information should be presented for as many years as available.

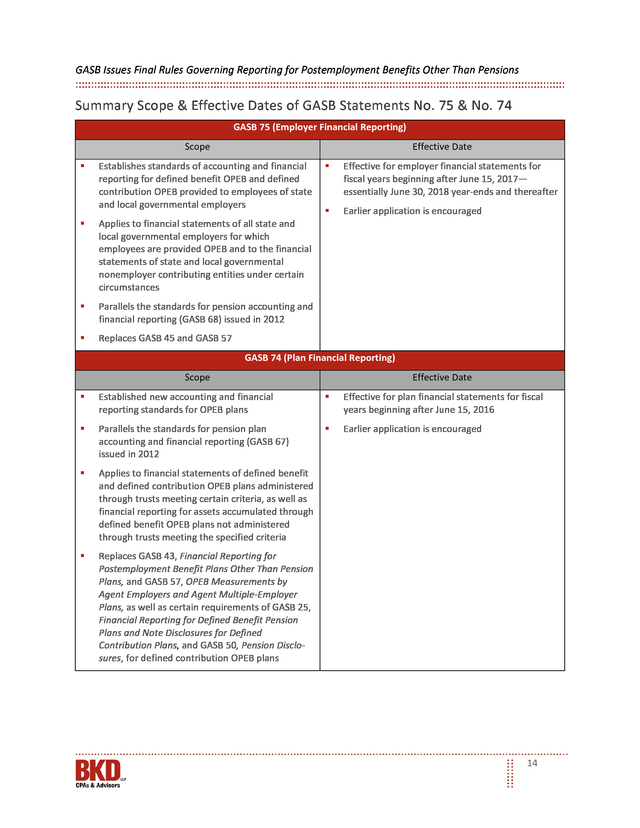

The schedules should not include information not measured in accordance with statement requirements. For further information, contact your BKD advisor. Contributor Connie Spinelli Director 303.861.4545 cspinelli@bkd.com 13 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Summary Scope & Effective Dates of GASB Statements No. 75 & No. 74 GASB 75 (Employer Financial Reporting) Scope Effective Date  Establishes standards of accounting and financial reporting for defined benefit OPEB and defined contribution OPEB provided to employees of state and local governmental employers  Applies to financial statements of all state and local governmental employers for which employees are provided OPEB and to the financial statements of state and local governmental nonemployer contributing entities under certain circumstances  Parallels the standards for pension accounting and financial reporting (GASB 68) issued in 2012   Effective for employer financial statements for fiscal years beginning after June 15, 2017— essentially June 30, 2018 year-ends and thereafter  Earlier application is encouraged Replaces GASB 45 and GASB 57 GASB 74 (Plan Financial Reporting) Scope Effective Date  Established new accounting and financial reporting standards for OPEB plans  Effective for plan financial statements for fiscal years beginning after June 15, 2016  Parallels the standards for pension plan accounting and financial reporting (GASB 67) issued in 2012  Earlier application is encouraged  Applies to financial statements of defined benefit and defined contribution OPEB plans administered through trusts meeting certain criteria, as well as financial reporting for assets accumulated through defined benefit OPEB plans not administered through trusts meeting the specified criteria  Replaces GASB 43, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans, and GASB 57, OPEB Measurements by Agent Employers and Agent Multiple-Employer Plans, as well as certain requirements of GASB 25, Financial Reporting for Defined Benefit Pension Plans and Note Disclosures for Defined Contribution Plans, and GASB 50, Pension Disclosures, for defined contribution OPEB plans 14 .

75 & NO. 74 ................................................. 14 2 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Executive Summary The Governmental Accounting Standards Board (GASB) has issued GASB Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions (GASB 75). For reporting periods beginning after June 15, 2017, governments will recognize their unfunded accrued other postemployment benefits (OPEB) obligation on the face of their financial statements. OPEB comprises mostly postemployment health care benefits and can represent a very significant liability for many state and local governments, especially if the government has set aside few assets to pay for those benefits.

OPEB also may include death benefits, life insurance, disability and long-term care. The new reporting requirements on OPEB parallel the changes for pension plan accounting included in Statement No. 67, Financial Reporting for Pension Plans—an amendment of GASB Statement No. 25, and Statement No.

68, Accounting and Financial Reporting for Pensions—an amendment of GASB Statement No. 27. Together, the standards provide consistent and comprehensive guidance to state and local governments for all postemployment benefits.

State and local governments currently are implementing the new pension standards, and financial statement users soon should have a more thorough understanding of the cost of significant pension and OPEB obligations. In addition to looking at GASB 75, this paper provides a brief overview of Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans, and Statement No. 73, Accounting and Financial Reporting for Pensions and Related Assets That Are Not within the Scope of GASB Statement 68, and Amendments to Certain Provisions of GASB Statements 67 and 68.

Although Statement 75 is effective for periods beginning after June 15, 2017, earlier application is encouraged. GASB 75—the standard for employers providing OPEB—addresses accounting and financial reporting for OPEB provided to the employees of state and local governmental employers and governments that finance OPEB plans for employees of other governments. The effects of GASB 75 are different for each type of OPEB plan:  Governments responsible only for OPEB liabilities related to their own employees and that provide OPEB through a defined benefit OPEB plan administered through a trust meeting specified criteria will report a net OPEB liability. The net OPEB liability represents the difference between the total OPEB liability and assets accumulated in a trust restricted to making benefit payments, where contributions are irrevocable and the OPEB plan assets are beyond the reach of creditors.  Governments participating in a cost-sharing OPEB plan administered through a trust that meets the specified criteria will report a liability equal to their proportionate share of the collective OPEB liability for all entities participating in the cost-sharing plan.  Governments that do not provide OPEB through a trust meeting the specified criteria will report the total OPEB liability related to their employees.  Governments legally responsible to make contributions directly to an OPEB plan or make benefit payments directly as OPEB comes due for employees of other governments—in certain circumstances called special funding situations—are required to recognize in their financial statements a share of the other government’s net OPEB liability. 3 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions The method a government will use to report and calculate its OPEB liability and annual expense for defined benefit OPEB plans administered through a trust meeting specified criteria will change significantly. For defined benefit OPEB, GASB 75 identifies the methods and assumptions required to project benefit payments, discount projected benefit payments to their actuarial present value and attribute that present value to periods of employee service. The changes include the following:  Requiring projected benefit payments to be discounted to their actuarial present value using a single rate that reflects the following: • • A long-term expected rate of return on OPEB plan investments, to the extent the OPEB plan’s fiduciary net position is projected to be sufficient to make projected benefit payments and OPEB plan assets are expected to be invested using a strategy to achieve that return A tax-exempt, high-quality municipal bond rate, to the extent the conditions for use of the longterm expected rate of return are not met  Requiring the use of a single actuarial cost allocation method: the “entry age actuarial cost method”  Requiring governments in all types of OPEB plans to present more extensive note disclosures and required supplementary information (RSI) about their OPEB liabilities GASB 75 carries forward from GASB 45 the option to use a specified alternative measurement method instead of an actuarial valuation for purposes of determining the total OPEB liability for benefits provided through OPEB plans in which there are fewer than 100 plan members (active and inactive). GASB 74—the standard for OPEB plans—provides guidance for reporting by OPEB plans that administer the OPEB benefits on behalf of governments. Its provisions are effective for financial statements for periods beginning after June 15, 2016 (one year earlier than GASB 75), with earlier application also encouraged. Similar to GASB 75 for employers, GASB 74 addresses the financial reports of defined benefit OPEB plans administered through trusts meeting defined criteria and addresses how plans should report assets accumulated through defined benefit OPEB plans not administered through trusts meeting the criteria. GASB 74 also requires certain note disclosure for defined contribution OPEB plans administered through trusts meeting the defined criteria. OPEB plans within the scope of GASB 74 will prepare a statement of fiduciary net position and a statement of changes in fiduciary net position.

Similar to GASB 75, GASB 74 requires more extensive note disclosures and RSI related to the measurement of the OPEB liabilities for which assets have been accumulated, including information about the annual money-weighted rates of return on plan investments. GASB 73—the supplemental pension standard—provides standards for pensions and pension plans not covered by GASB 67 and 68 (plans not administered through a trust meeting specified criteria). GASB 73 completes the suite of pension standards. The requirements in GASB 73 for reporting pensions generally are the same as GASB 68. However, similar to GASB 75, measurement differences are applicable to a pension plan not administered through a trust meeting specified criteria. 4 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions GASB 75 – Employer Standard Background & Impact of Change Under extant GASB 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions, a government is required to estimate and record the cost of benefits promised to employees as those employees provide services to the government and its constituents. GASB 75 enhances the accuracy of the information about the total cost of service a government provides to its constituents. For governments that do not pay or contribute for OPEB but defer the costs to future periods, the financial statements of these entities will continue to reflect a higher OPEB liability than those governments funding their obligations on an annual basis as OPEB costs are incurred. OPEB liabilities—similar to pension liabilities—are amounts disclosing the cash-flow demands on the government and its taxpayers or rate payers in future years; these have only gained importance to the diverse users of a government’s financial statements since GASB 45. The significance of GASB 75 is the change in definition of a government’s OPEB liability, measurement requirements of a government’s OPEB liability and its effects on annual OPEB cost recognition, particularly in the year of implementation. Under GASB 45, a government’s unfunded OPEB obligation (unfunded actuarial accrued liability) is disclosed in the footnotes. A government’s accrual-based liability (net OPEB obligation) recorded on the face of the financial statements represents the amount its actual OPEB contributions is less than its annual OPEB cost—the employer’s annual required contribution (ARC) to the plan—with certain adjustments if the employer has a net OPEB obligation for past undercontributions or overcontributions. In the initial year of adoption of GASB 75, however, governments generally will immediately report a financial statement liability for its share of the entire unfunded OPEB liability (net OPEB liability), with certain adjustments for amortizable items.

GASB 75 will particularly affect employer and nonemployer governments participating in cost-sharing OPEB plans. GASB 75 brings the liability up to the face of the financial statements. For governments with a pay-as-you-go OPEB financing system, the net OPEB obligation accumulated rapidly since GASB 45 and will continue to do so under GASB 75. Likewise, the requirement under GASB 45 to disclose information about the funded status of a plan still exists.

The unfunded liability, however, will be reported on the face of the financial statements under GASB 75. In governmental fund financial statements, the measurement focus is on current financial resources; statements are prepared under the modified accrual basis of accounting (as opposed to governmentwide financial statements where the measurement focus is on economic resources and statements are prepared under the accrual basis of accounting). As such, governmental funds will recognize a net OPEB liability to the extent the liability is normally expected to be liquidated with expendable available financial resources (benefit payments have matured and the OPEB plan’s fiduciary net position is not sufficient for payment of those benefits). OPEB expenditures are recognized equal to the total of the following:  Amounts paid by the employer to the OPEB plan, including amounts paid for OPEB as benefits come due  The change between the beginning and ending balances of amounts normally expected to be liquidated with expendable available financial resources Scope As with superseded GASB 45, the new OPEB standard does not enforce OPEB funding or payment obligations—a policy decision made by government officials—instead, it establishes new measurement and reporting requirements to more clearly depict the government’s financial position.

Likewise, the standards do not address how a government measures OPEB for the purpose of determining whether to set assets aside to fund future OPEB 5 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions payments and, if so, how much to set aside. In other words, OPEB liability will be placed on the statement of net position or balance sheet with other long-term obligations but will not alter the economic reality of the government’s situation. GASB has issued the new OPEB standards to provide taxpayers, policymakers, bond analysts and others with more and better information about postemployment benefits other than pensions so they can better assess the financial obligations and annual costs related to a government’s promise to provide OPEBs. Although GASB 75 is a financial reporting standard, we believe it will provide many governments with a better foundation for informed policy decision about the levels and types of benefits provided and potential methods of financing those benefits. GASB 75 applies only to OPEB, as defined below. OPEB Inclusions & Exclusions OPEB Includes OPEB Excludes  Postemployment health care benefits—medical, dental, vision, hearing and other health-related benefits—whether provided separately or through a pension plan  Termination benefits or termination payments for sick leave; however, the effects of a termination benefit on liabilities for defined benefit OPEB are accounted for under the provisions of GASB 75  Other forms of postemployment benefits—death benefits, life insurance, disability and long-term care—when provided separately from a pension plan  When provided through a pension plan, postemployment benefits other than postemployment health care benefits; these benefits should be accounted for and reported as pensions, separate from OPEB The requirements of GASB 75 apply to various types of defined benefit OPEB plans administered through a trust meeting defined criteria, as well as defined contribution plans—those stipulating only the amount to be contributed to employee accounts each year, not the amount of benefits that will be paid in the future. Applicable to many governments, the new guidance also provides requirements for OPEB provided through an arrangement not administered through a trust meeting the defined criteria. State and local governments are required to apply the requirements of GASB 75 separately to the OPEB provided through each defined benefit OPEB plan administered through a trust meeting specified criteria, which are listed in the chart below. Administered Through Trusts or Equivalent Arrangements Criteria  Contributions from employers and nonemployer-contributing entities to the OPEB plan and earnings thereon are irrevocable  OPEB plan assets are dedicated to providing OPEB to plan members in accordance with benefit terms  OPEB plan assets are legally protected from creditors of employers, nonemployer-contributing entities and the OPEB plan administrator • For defined benefit OPEB plan, plan assets also are legally protected from creditors of the plan members 6 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Calculating OPEB Liabilities & Expense GASB 75 requires significant changes to how a government employer will report and calculate its OPEB liability and annual expense for defined benefit OPEB plans administered through a trust meeting the specified criteria. For these plans, the government will report a net OPEB liability, which is the difference between the total OPEB liability and the OPEB plan’s fiduciary net position—essentially, the amount available to make benefit payments. The calculation results in immediate recognition of additional components of OPEB expense. For governments not providing OPEB administered through a trust meeting the specified criteria, the total OPEB liability will be the liability reported by the government. For OPEB administered through a trust meeting the specified criteria, the requirements differ based on the number of employers with employees that are provided OPEB through the OPEB plan, as well as whether OPEB obligations and OPEB plan assets are shared by the employers. Various types of defined benefit OPEB plans specify the amount of benefits to be provided to the employees after the end of their employment. These include single-employer OPEB plans that provide benefits to the employees of one employer (a single employer plus component units) and multiple-employer OPEB plans that provide benefits to the employees of more than one employer. Under an agent multiple-employer OPEB plan, the assets of a multiple-employer OPEB plan are pooled for investment purposes with separate accounts maintained for each individual agent employer.

Each agent employer’s share of the pooled assets legally is available to pay the OPEB only of its employees. In a cost-sharing multiple-employer OPEB plan, cost-sharing employers share their assets and their obligations to provide OPEB to their employees. Plan assets generally can be used to pay the benefits of the employees of any employer providing OPEB through the plan. Types of OPEB Plans Within the Scope of GASB 75 Defined-Benefit OPEB Plan Type Single-employer defined benefit OPEB plan Description  Single employers are those for which employees are provided defined benefit OPEB through single-employer OPEB plans (OPEB plans in which OPEB is provided to the employees of only one employer)  The primary government and component units are considered one employer Agent-employer defined benefit OPEB plan (agent OPEB plan),  An agent multiple-employer defined benefit OPEB plan is a plan in which assets are pooled in a trust for investment purposes, but separate accounts are maintained for each individual employer and each employer’s share of assets legally is available to pay benefits of only its employees Cost-sharing employer defined benefit OPEB plan (cost-sharing OPEB plan)  A cost-sharing multiple-employer defined benefit OPEB plan is a plan in which the OPEB obligations to the employees of more than one employer are pooled; OPEB plan assets can be used to pay the benefits of the employees of any employer providing OPEB through the OPEB plan Insured plans  Defined benefit OPEB plans in which benefits are financed through an arrangement whereby premiums are paid to an insurance company while employees are in active service  Insurance company unconditionally undertakes an obligation to pay the OPEB of those employees as defined in the OPEB plan terms  OPEB provided through insured plans is classified as an insured benefit 7 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions In situations where a government and its component units participate in the same single-employer or agent OPEB plan, single-employer or agent requirements of GASB 75 should be followed. If they issue standalone financial statements, each government will account for and report its participation in the single-employer or agent OPEB plan as if it were a cost-sharing employer. Total OPEB Liability A government’s total OPEB liability is its present obligation to provide promised future benefit payments, incurred as it receives employee services each reporting period for which it has promised future benefit payments. In other words, it is the portion of the actuarial present value of the projected benefit payment attributed to past periods of employee service. Governments will measure total OPEB liability in three steps:  Projecting future benefit payments for current and former employees and their beneficiaries  Discounting those payments to their present value  Allocating the present value over past and future periods of employee service Projecting Discounting Attributing Projecting Total OPEB Liability An actuarial valuation will be used to measure the total OPEB liability and is performed as of the measurement date—the date the net OPEB liability is measured and recorded in the financial statements—or using a date other than the measurement date, as described in the chart below. Governments elect the net OPEB liability measurement date.

It must be no earlier than the employer’s prior fiscal year-end and no later than the current fiscal year-end and remain consistent from period to period. For accounting and financial reporting purposes, an actuarial valuation of total OPEB liability should be performed at least biennially, though more frequent actuarial valuations are encouraged. 8 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Options to Calculate Total OPEB Liability Actuarial Valuation as of the Measurement Date Actuarial Valuation Not as of the Measurement Date Calculate total OPEB liability based on an actuarial valuation as of the measurement date Calculate total OPEB liability based on an actuarial valuation dated no more than 30 months and one day earlier than the employer’s most recent fiscal year-end, with roll-forward procedures to the measurement date Special Consideration: In situations where the plan and employer have the same fiscal year-end, the employer may choose either the current yearend or the prior year-end as the measurement date If significant changes occur between the actuarial valuation date and the measurement date, professional judgment will be used to determine the extent of procedures needed to roll forward the valuation; in certain situations, a new actuarial valuation may be needed Special Consideration: When measuring the total OPEB liability using updating procedures to the measurement date, governments should not roll forward the OPEB plan’s fiduciary net position from an earlier date in determining net OPEB liability; they must use the same valuation methods used by the OPEB plan for purposes of preparing its statement of fiduciary position The date of the actuarial valuation is not required to have the same relationship to the measurement date in each reporting period. In other words, the date the actuarial valuation performed for purposes of determining the total OPEB liability at measurement date may vary from period to period. In practice, the measurement date will most likely correspond to the plan’s fiscal year-end. Employer contributions made subsequent to the total OPEB liability measurement date and before the end of the employer’s fiscal year-end will be recognized as a deferred outflow of resources. To reduce costs for smaller governments, GASB 75 maintains to use of a specified alternative measurement method in place of an actuarial valuation for purposes of determining the total OPEB liability for benefits provided through an OPEB plan in which fewer than 100 employees (active and inactive) are provided with OPEB through the plan. The alternative measurement method is an approach that includes the same broad measurement steps as an actuarial valuation (projecting benefit payments, discounting projected benefit payments to a present value and attributing the present value of projected benefit payments to periods using an actuarial cost method). However, it permits simplification of certain assumptions. The current practice of incorporating expectations of future employment-related events into projections of OPEB payments—such as projected salary increases and projected years of service if they affect the amount of OPEB payments employees will receive will not change.

Provisions for automatic cost-of-living adjustments (COLAs) and other automatic benefit changes (which generally are written into the OPEB terms) also will continue to be included in projections. Ad hoc postemployment benefit changes (including ad hoc COLAs), however, which are made at the discretion of the government, will now be included in projections if they are substantively automatic. 9 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Under GASB 75, a government will report OPEBs in its financial statements using the economic measurement focus and accrual basis of accounting (with the exception of governmental funds financial statements). This is similar to GASB 68, the 2012 standard on Employer Accounting for Pensions which also addresses financial statement user concerns that significant obligations of governmental entities are going unreported and undisclosed. GASB 70 on nonexchange financial guarantees is another recent GASB statement addressing these concerns. OPEB expense and OPEB-related deferred outflows of resources and deferred inflows of resources reported by an employer primarily will result from changes in the total OPEB liability and changes in the OPEB plan’s fiduciary net position, e.g., discounted OPEB plan assets. Changes in the total OPEB liability resulting from current-period service cost, interest on the total OPEB liability and benefit term changes must be included in OPEB expense immediately.

In addition, projected earnings on the OPEB plan’s investments also are required to be included in the determination of OPEB expense immediately. When the total OPEB liability and the OPEB plan’s fiduciary net position are determined based on the results of an actuarial valuation, the effects of certain other changes are required to be included in OPEB expense over the current and future periods, as listed below. Changes in Actuarial Assumptions & Experience & Effect on Financial Statements Change in Circumstances or Event  The effects on the total OPEB liability (if the alternative measurement method is not used to measure the total OPEB liability) of: • •  Difference between expected and actual experience with regard to economic or demographic factors in measurement of total OPEB liability, e.g., mortality, current-period service cost or health care cost trend rates Changes of economic or demographic assumptions or of other inputs, e.g., discount rate, mortality, future payroll increases, future inflation rate and health care cost trend rates Differences between projected and actual earnings on OPEB plan investments Impact on Financial Statements  Effects must be recognized in OPEB expense, beginning in the current reporting period, using a systematic and rational method over a closed period equal to the average expected remaining service lives of all employees provided with OPEB through the OPEB plan (active and inactive), determined as of the beginning of the measurement period  The portion not recognized as OPEB expense in the current reporting period (unamortized portion) is recorded as deferred outflows of resources or deferred inflows of resources, resulting in “layers” amortized into expense over the closed periods  Recognized in OPEB expense using a systematic and rational method over a closed five-year period, beginning in current reporting period  The amount not recognized as OPEB expense is recorded as deferred outflows of resources or deferred inflows of resources, resulting in layers amortized into expense over the closed period(s)  Deferred outflows and deferred inflows of resources recognized in different measurement periods should be aggregated as a net deferred outflow or resources or a net deferred inflow of resources 10 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Governments will report employer contributions, subsequent to the net OPEB liability measurement date and before the end of the reporting period, on the Statement of Net Position (Balance Sheet) as deferred outflows of resources. In the year immediately following recognition of the deferred outflow of resources, the government will recognize the contribution as a reduction of the net OPEB liability. Discounting GASB 75 has specified the discount rate government employers will use to discount projected benefit payments or projected total OPEB liability. As long as plan assets related to current active and inactive employees and their beneficiaries are projected to be sufficient to make the projected benefit payments for those individuals, governments will discount those projected benefit payments using the long-term expected rate of return on OPEB plan investments (net of investment expenses). In this case, OPEB plan assets must be expected to be invested using a strategy that will achieve that return. However, some governments will have a crossover point at which the plan assets are projected to be insufficient to make projected benefit payments to current active and inactive employees and their beneficiaries.

GASB believes the projected benefit payments occurring thereafter are similar to other forms of debt. In this circumstance, the discount rate will be based on a tax-exempt, high-quality 20-year tax-exempt general obligation municipal bond yield or index rate. (High quality would be defined as rated at least AA/Aa or an equivalent rating.) In a situation where no assets have been accumulated in an OPEB trust—which is not uncommon—all projected benefit payments will be discounted using the municipal bond rate.

Accordingly, underfunded plans will use the municipal bond rate for at least a portion of discounting. The lower municipal bond rate will result in an increased total OPEB liability compared to well-funded plans using the long-term expected rate of return on OPEB plan investments. Allocating Under current requirements, governments can choose from six methods for attributing the present value of benefit payments to specific years either in level dollar amounts, similar to a mortgage, or as a level percentage of projected payroll. GASB 75 requires all governments to use the entry age actuarial cost method to allocate present value and to do so as a level percentage of pay.

The actuarial present value will be attributed to each employee individually, from the first period in which the employee provides services under the benefit terms through the period in which the employee exits active service, e.g., the expected period of employment. GASB believes this pattern reflects the ongoing annual exchange of service for benefits over the course of an employee’s period of employment in amounts that keep pace with the employee’s projected salary over that period. Net OPEB Liability A government is only required to recognize its actual OPEB liability, meaning it will net the discounted projected benefit payments (discounted total OPEB liability) against the OPEB plan’s fiduciary net position—the primary resources that will be used to pay the OPEB. This liability is referred to as the net OPEB liability. As previously mentioned, in financial statements prepared using the economic resources measurement focus and accrual basis of accounting, a single or agent employer without a special funding situation must recognize a liability equal to the net OPEB liability.

The net OPEB liability is required to be measured as of a date no earlier than the employer’s prior fiscal year-end and no later than the current fiscal year-end (the measurement date), consistently applied from period to period. Governments must ensure the “OPEB plan’s fiduciary net position” is calculated using the same valuation methods as the OPEB plan for purposes of preparing its statement of fiduciary net position. For footnote disclosure purposes, employers may refer to the OPEB plan’s basic financial statements, with respect to the fiduciary net position, if the OPEB plan’s financial statements are available online. 11 . GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Cost-Sharing Employers Cost-sharing governmental employers without a special funding situation will recognize a liability for their proportionate share of the collective net OPEB liability, e.g., the net liability of all employers for benefits provided through the OPEB plan, measured using the same measurement date criteria as single and agent plans. The basis for determining each employer’s proportion should be consistent with the manner in which contributions to the OPEB plan are determined. Use of the employer’s projected long-term contribution effort to the OPEB plan compared to the total projected long-term contribution effort of all employers and all nonemployer contributing entities is encouraged. Special provisions apply to governmental fund financial statements. Under the new guidance, a cost-sharing employer is required to recognize a liability for its proportionate share of the collective net pension liability.

Thus, similar to GASB 68, cost-sharing employers without a special funding situation are expected to experience the largest impact of GASB 75 due to previously unrecorded liabilities. As a result, entities may need to evaluate their ability to continue as a going concern under GASB 56 and consider, as applicable, having going concern discussions with their auditors. However, the going concern evaluation prescribed in GASB 56 suggests a 15-month period subsequent to the current year-end is sufficient for a going concern evaluation; the current portion of the OPEB liability probably will not be significant enough to create a going concern uncertainty in most instances. Special Funding Situation An employer with a special funding situation for a defined benefit OPEB will recognize an OPEB liability and deferred outflows of resources or deferred inflows of resources related to OPEB, with adjustments for the involvement of nonemployer contributing entities. For a single or agent employer with a special funding situation, its net OPEB liability represents the employer’s proportionate share of the collective net OPEB liability.

Special funding situations are circumstances in which a nonemployer entity legally is responsible for providing financial support for OPEB of the employees of another entity by making contributions directly to an OPEB plan administered through a trust or, if not administered through a trust, by making benefit payments directly as the OPEB comes due. Notes to Financial Statements & Required Supplementary Information GASB 75 requires governments in all types of OPEB plans to present more extensive note disclosures and RSI about their OPEB liabilities. Single and agent employers will include descriptive information, such as the types of benefits provided and the number and classes of employees covered by the benefit terms. Additional disclosures include, among numerous other disclosures, the following:  For the current year, sources of changes in the net OPEB liability  Significant assumptions and other inputs used to calculate the total OPEB liability, including those about inflation, the health care cost trend rate, salary changes, ad hoc postemployment benefit changes (including ad hoc COLAs) and inputs to the discount rate, as well as certain information about mortality assumptions and the dates of experience studies, e.g., a description of the effect on the reported OPEB liability of using a discount rate and a health care cost trend rate that are one percentage point higher and one percentage point lower than assumed by the government  The date of the actuarial valuation or calculation using the alternative measurement method used to determine the total OPEB liability, information about changes of assumptions or other inputs and benefit terms, the basis for determining employer contributions to the OPEB plan and information about the purchase, if any, of allocated insurance contracts 12 .

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Single and agent employers must present the following in RSI, determined as of the measurement date, for each of the 10 most recent fiscal years:  A schedule of changes in the net OPEB liability  Components of the net OPEB liability and related ratios, including the OPEB plan’s fiduciary net position as a percentage of the total OPEB liability, and the net OPEB liability as a percentage of covered-employee payroll The two schedules above can be combined into one schedule. Significant methods and assumptions used in calculating the actuarially determined contributions, if applicable, are required to be presented as notes to the RSI. In addition, the employer must explain certain factors significantly affecting trends in the amounts reported in the schedules. For actuarially determined contributions, a single or agent employer is required to present a schedule covering each of the 10 most recent fiscal years including the actuarially determined contribution, contributions to the OPEB plan and related ratios. If a single or agent employer instead has a contribution requirement established by statute or contract, the employer must present a schedule covering each of the 10 most recent fiscal years including information about the statutorily or contractually required contribution rates, contributions to the OPEB plan and related ratios. Amounts for these schedules should be determined as of the employer’s most recent fiscal year-end. Cost-sharing employers’ RSI will include a 10-year schedule showing certain proportionate share information and a 10-year schedule if contribution requirements of the employer are statutorily or contractually established. Implementation & Transition Until GASB 75 becomes effective in fiscal years beginning after June 15, 2017, or earlier if the provisions are adopted early, all provisions of GASB 45 for accounting and reporting of OPEBs remain in effect. Changes adopted to conform to the provisions of this statement should be applied retroactively by restating financial statements, if practical, for all prior periods presented.