Description

Boards Move Closer to

Completing Leases Project

With the decisions made at their December 2014 and January 2015 meetings, the Financial Accounting Standards

Board (FASB) and the International Accounting Standards Board (IASB) are nearing completion of redeliberations

on the leases project. At the December 2014 meeting, the boards tentatively agreed on the definition of a lease.

The boards decided against adding an additional requirement to their proposed definition and are moving forward

with the definition decided on at their October 2014 meeting. At the January 2015 meeting, the boards discussed

lessee disclosure requirements. Although converged decisions were not achieved, the boards reaffirmed their

objectives for lessee disclosures from their 2013 proposal.

As redeliberations wind down, companies should evaluate their contracts and determining the potential impact of

the new standard on their financial statements.

The boards still have a few more issues to redeliberate, but they continue to work toward their goal of issuing a final standard by the end of 2015. The following provides more detailed information about the decisions reached by the boards at their December and January meetings. Definition of a Lease At their October 2014 meeting, the boards reaffirmed a lease would be defined as a contract that conveys the right to use an asset (the “identified” asset) for a period of time in exchange for consideration. To determine whether a contract contains a lease, companies would assess both of the following: 1. Whether the use of an identified asset is either explicitly or implicitly specified 2. Whether the contract conveys to the customer the right to control the use of the identified asset throughout the period of use At their December 2014 meeting, the boards decided not to include in the definition of a lease an additional requirement that the customer must have the ability to derive the benefits from directing the use of an identified asset. Accordingly, the definition of a lease decided upon at the October 2014 meeting stands. Customer’s Right to Control the Use of the Identified Asset Regarding the second criterion listed above, a contract would convey the right to control the use of an identified asset if, throughout the period of use, the customer has the right to both direct the use of the identified asset and obtain substantially all of the economic benefits from directing the use of the identified asset.

When a customer has the right to direct how and for what purpose it will use the identified asset—including the right to change how and for what purpose the asset will be used throughout the period of use—the customer is considered to have the right to direct the use of the identified asset. If neither the customer nor the supplier controls how and for what purpose they will use the asset throughout the period of use, the customer is considered to have the right to direct the use of the identified asset if either of the following is true: . Boards Move Closer to Completing Leases Project  The customer has the right to operate the asset or direct others to operate the asset in a manner that it determines (with the supplier having no rights)  The customer designed the asset, or caused the asset to be designed, in a way that predetermines how and for what purpose the asset will be used or operated Supplier’s Rights A supplier’s protective rights, in isolation over the identified asset, would not prevent the customer from having the right to direct the use of an identified asset. Suppliers’ protective rights generally take the form of a specified maximum amount of asset use or a requirement to follow specific operating instructions. In addition, a contract would not involve the use of an identified asset if the supplier has the substantive right (practical ability) to substitute the asset used to fulfill the contract and the supplier can benefit from exercising that right of substitution. Lessee Disclosures During the January 2015 meeting, the boards discussed lessee disclosure requirements. They decided the final leases standard should include a disclosure objective: to enable financial statement users to assess the amount, timing and uncertainty of cash flows arising from leases.

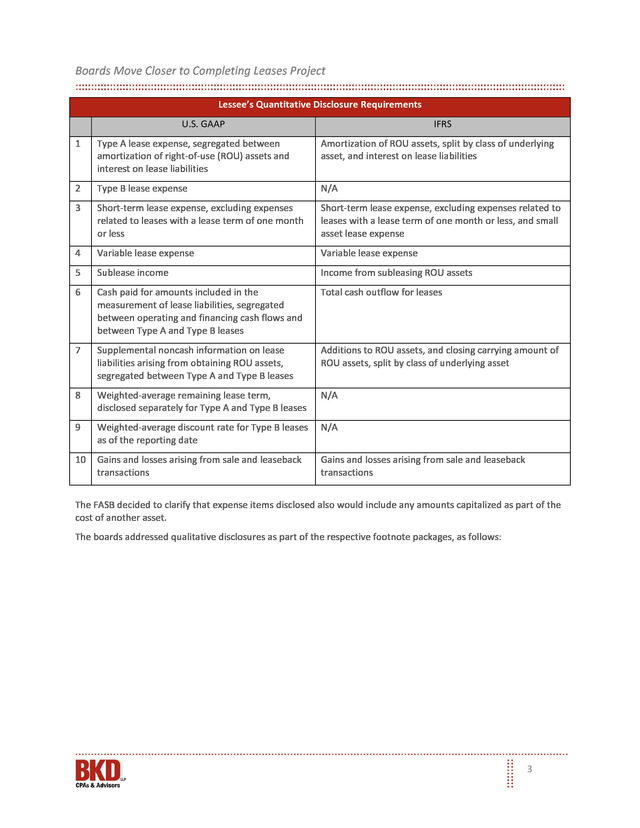

The boards also decided to retain the 2013 Exposure Draft (ED) proposal requiring a lessee to consider the level of detail necessary to satisfy the disclosure objective. The FASB decided to recommend, but not require, a lessee to present lessee disclosures in a tabular format. Voicing a slightly stronger position, IASB decided to require a lessee to present the quantitative lessee disclosures in a tabular format unless another format is more appropriate. The boards tentatively decided to remove a requirement in the 2013 proposal that an entity disclose reconciliations of its opening and closing balances of lease liabilities. FASB did decide to require a maturity analysis of lease liabilities, showing the undiscounted cash flows annually for at least the first five years and a total of the amounts for the remaining years; this analysis also would reconcile the undiscounted cash flows to the discounted lease liabilities recognized in the statement of financial position. IASB voted to rely on the existing disclosure requirements covering financial liabilities (IFRS 7, Financial Instruments: Disclosures) but require a lessee to disclose a maturity analysis of its lease liabilities separately from the maturity analyses of other financial liabilities. FASB decided not to require a lessee to disclose a maturity analysis of commitments for nonlease components related to a lease, nor provide qualitative disclosures about the existence, or terms and conditions of significant nonlease commitments it has taken on resulting from entering lease contracts. Among the new prescriptive quantitative requirements, both boards agreed short-term lease expenses—those stemming from leases at least one month but less than a year in duration—would be on the list of amounts to be presented (Item No.

3 below). The following table lists these disclosures and how U.S. generally accepted accounting principles (GAAP) compares to International Financial Reporting Standards (IFRS): 2 .

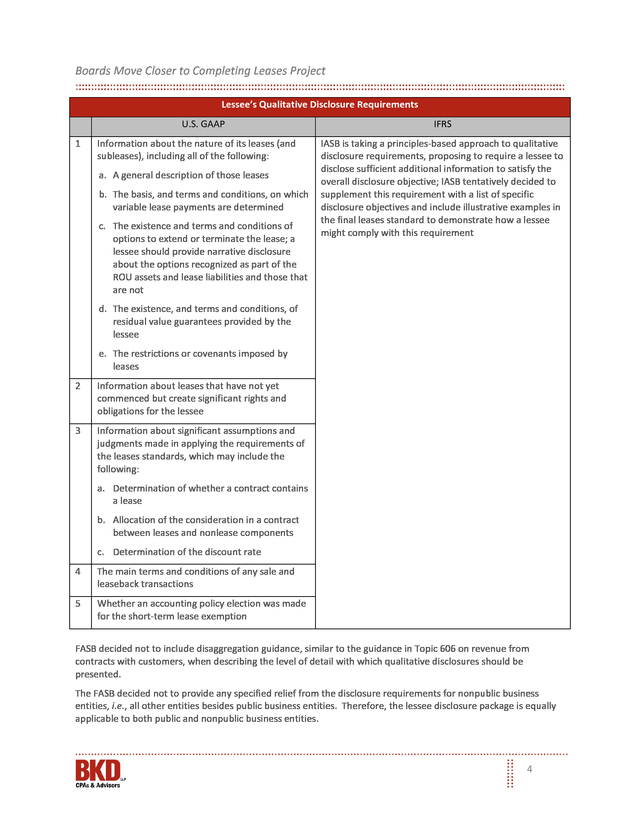

Boards Move Closer to Completing Leases Project Lessee’s Quantitative Disclosure Requirements U.S. GAAP IFRS 1 Type A lease expense, segregated between amortization of right-of-use (ROU) assets and interest on lease liabilities Amortization of ROU assets, split by class of underlying asset, and interest on lease liabilities 2 Type B lease expense N/A 3 Short-term lease expense, excluding expenses related to leases with a lease term of one month or less Short-term lease expense, excluding expenses related to leases with a lease term of one month or less, and small asset lease expense 4 Variable lease expense Variable lease expense 5 Sublease income Income from subleasing ROU assets 6 Cash paid for amounts included in the measurement of lease liabilities, segregated between operating and financing cash flows and between Type A and Type B leases Total cash outflow for leases 7 Supplemental noncash information on lease liabilities arising from obtaining ROU assets, segregated between Type A and Type B leases Additions to ROU assets, and closing carrying amount of ROU assets, split by class of underlying asset 8 Weighted-average remaining lease term, disclosed separately for Type A and Type B leases N/A 9 Weighted-average discount rate for Type B leases as of the reporting date N/A 10 Gains and losses arising from sale and leaseback transactions Gains and losses arising from sale and leaseback transactions The FASB decided to clarify that expense items disclosed also would include any amounts capitalized as part of the cost of another asset. The boards addressed qualitative disclosures as part of the respective footnote packages, as follows: 3 . Boards Move Closer to Completing Leases Project Lessee’s Qualitative Disclosure Requirements U.S. GAAP 1 Information about the nature of its leases (and subleases), including all of the following: a. A general description of those leases b. The basis, and terms and conditions, on which variable lease payments are determined c.

The existence and terms and conditions of options to extend or terminate the lease; a lessee should provide narrative disclosure about the options recognized as part of the ROU assets and lease liabilities and those that are not IFRS IASB is taking a principles-based approach to qualitative disclosure requirements, proposing to require a lessee to disclose sufficient additional information to satisfy the overall disclosure objective; IASB tentatively decided to supplement this requirement with a list of specific disclosure objectives and include illustrative examples in the final leases standard to demonstrate how a lessee might comply with this requirement d. The existence, and terms and conditions, of residual value guarantees provided by the lessee e. The restrictions or covenants imposed by leases 2 Information about leases that have not yet commenced but create significant rights and obligations for the lessee 3 Information about significant assumptions and judgments made in applying the requirements of the leases standards, which may include the following: a.

Determination of whether a contract contains a lease b. Allocation of the consideration in a contract between leases and nonlease components c. Determination of the discount rate 4 The main terms and conditions of any sale and leaseback transactions 5 Whether an accounting policy election was made for the short-term lease exemption FASB decided not to include disaggregation guidance, similar to the guidance in Topic 606 on revenue from contracts with customers, when describing the level of detail with which qualitative disclosures should be presented. The FASB decided not to provide any specified relief from the disclosure requirements for nonpublic business entities, i.e., all other entities besides public business entities.

Therefore, the lessee disclosure package is equally applicable to both public and nonpublic business entities. 4 . Boards Move Closer to Completing Leases Project Major Differences Loom The boards generally are aligned on the balance sheet treatment of lease-related assets and liabilities, tentatively agreeing to recognize all leases on the balance sheet. Major differences still exist between lease classification under IFRS and U.S. GAAP, affecting profit recognition and presentation. To recap, companies will record as liabilities all lease obligations other than short-term lease obligations (leases with a term of 12 months or less). FASB's revised dual-model approach uses criteria very similar to the lease classification tests under today's US GAAP, but without the bright lines, e.g., 75 percent of useful life and 90 percent of fair value.

Under FASB's proposed approach, the majority of today's capital leases would be Type A leases accounted for as financing arrangements (recognizing amortization on the leased asset and interest expense on the lease liability), while the majority of today's operating leases would be classified as Type B leases accounted for under the straight-line lease expense model. Regarding lessor classification, both boards agreed to do away with the receivable and residual approach proposed in the May 2013 ED. Instead, the boards tentatively agreed lessors should determine lease classification and accounting treatment—Type A versus Type B—based on whether the lease is effectively a financing or a sale, rather than an operating lease, again absent the bright lines. A lessor would make that determination by assessing whether the lease transfers substantially all the risks and rewards incidental to ownership of the underlying asset. Under FASB’s approach, companies will need to evaluate Type A leases under the criteria included in the recently issued revenue standard to determine whether a sale has occurred from the customer’s or lessee’s perspective. The absence of bright lines will increase the need to apply judgment in lease classification for both lessors and lessees, particularly when the contract is on the fringes of the old bright lines. Looking Ahead: Information Needs & System Requirements The boards will continue to meet in 2015 with hopes of converging on several issues, including lease classification and lessee expense recognition, as well as sale-leaseback transactions, effective dates and transition. The proposal has been through two exposure periods, and another exposure draft is not expected.

Companies should start evaluating their contracts to determine whether they contain a lease or a sale-leaseback transaction and, for those following U.S. GAAP, whether the lease is Type A or Type B. Both lessees and lessors will need to develop processes and procedures to capture, store and monitor pertinent data so they can determine the initial lease term, identify initial direct costs, separate lease and nonlease components, determine the discount rate and identify subleases and sale and leaseback transactions. For example, when determining the lease term upon lease commencement, lessees and lessors will need to capture all relevant factors that create an economic incentive to exercise an option to extend or not to terminate a lease or execute a purchase option.

Both parties will need to determine whether it is reasonably certain (similar to the current concept of “reasonably assured”) the lessee will exercise the option. This guidance, like other guidance in the tentative decisions, includes subjective language requiring management judgment. Throughout the lease, lessees will be required to monitor factors that could necessitate reassessing the lease term. Such factors include the occurrence of a significant event or a significant change in circumstances that are within the control of the lessee. When the lessee remeasures the lease liability due to reassessment of the lease term, the lessee also will be required to reassess variable lease payments that depend on an index or a rate and reassess the discount rate.

Entities will need procedures to evaluate and document the reasonableness of the index or rates used, as well as monitoring mechanisms to capture triggering events. Both lessees and lessors will need to monitor any change to the contractual terms and conditions not part of the original lease. Depending on the type of lease modification, an entity may account for the modification as a new lease separate from the original or as remeasurement of the existing lease. Entities will need processes to evaluate changes to leases in order to determine the proper accounting for the lease modification. 5 .

Boards Move Closer to Completing Leases Project Another item of high interest is sale-leaseback transactions. The new revenue recognition standard prohibits the recognition of seller’s profit when the seller-lessee determines the leaseback is a Type A lease. Based on the revenue recognition standard’s transfer of control criteria, the existence of a purchase option in a Type B lease also could preclude the seller-lessee from recognizing a sale—especially if the seller-lessee retains physical possession of the asset. Seller-lessees will need to evaluate all sale-leaseback transactions for potential restatement. Companies are encouraged to start preparing for the new standard by gathering contractual documents and cataloguing existing leases.

Companies also should evaluate resource requirements, including information systems, to ensure they have the appropriate infrastructure to successfully implement the new standard. For additional guidance, consult your BKD advisor. Additional Resources BKD Hot Topics: Lease Accounting Contributor Connie Spinelli Director 303.861.4545 cspinelli@bkd.com 6 .

The boards still have a few more issues to redeliberate, but they continue to work toward their goal of issuing a final standard by the end of 2015. The following provides more detailed information about the decisions reached by the boards at their December and January meetings. Definition of a Lease At their October 2014 meeting, the boards reaffirmed a lease would be defined as a contract that conveys the right to use an asset (the “identified” asset) for a period of time in exchange for consideration. To determine whether a contract contains a lease, companies would assess both of the following: 1. Whether the use of an identified asset is either explicitly or implicitly specified 2. Whether the contract conveys to the customer the right to control the use of the identified asset throughout the period of use At their December 2014 meeting, the boards decided not to include in the definition of a lease an additional requirement that the customer must have the ability to derive the benefits from directing the use of an identified asset. Accordingly, the definition of a lease decided upon at the October 2014 meeting stands. Customer’s Right to Control the Use of the Identified Asset Regarding the second criterion listed above, a contract would convey the right to control the use of an identified asset if, throughout the period of use, the customer has the right to both direct the use of the identified asset and obtain substantially all of the economic benefits from directing the use of the identified asset.

When a customer has the right to direct how and for what purpose it will use the identified asset—including the right to change how and for what purpose the asset will be used throughout the period of use—the customer is considered to have the right to direct the use of the identified asset. If neither the customer nor the supplier controls how and for what purpose they will use the asset throughout the period of use, the customer is considered to have the right to direct the use of the identified asset if either of the following is true: . Boards Move Closer to Completing Leases Project  The customer has the right to operate the asset or direct others to operate the asset in a manner that it determines (with the supplier having no rights)  The customer designed the asset, or caused the asset to be designed, in a way that predetermines how and for what purpose the asset will be used or operated Supplier’s Rights A supplier’s protective rights, in isolation over the identified asset, would not prevent the customer from having the right to direct the use of an identified asset. Suppliers’ protective rights generally take the form of a specified maximum amount of asset use or a requirement to follow specific operating instructions. In addition, a contract would not involve the use of an identified asset if the supplier has the substantive right (practical ability) to substitute the asset used to fulfill the contract and the supplier can benefit from exercising that right of substitution. Lessee Disclosures During the January 2015 meeting, the boards discussed lessee disclosure requirements. They decided the final leases standard should include a disclosure objective: to enable financial statement users to assess the amount, timing and uncertainty of cash flows arising from leases.

The boards also decided to retain the 2013 Exposure Draft (ED) proposal requiring a lessee to consider the level of detail necessary to satisfy the disclosure objective. The FASB decided to recommend, but not require, a lessee to present lessee disclosures in a tabular format. Voicing a slightly stronger position, IASB decided to require a lessee to present the quantitative lessee disclosures in a tabular format unless another format is more appropriate. The boards tentatively decided to remove a requirement in the 2013 proposal that an entity disclose reconciliations of its opening and closing balances of lease liabilities. FASB did decide to require a maturity analysis of lease liabilities, showing the undiscounted cash flows annually for at least the first five years and a total of the amounts for the remaining years; this analysis also would reconcile the undiscounted cash flows to the discounted lease liabilities recognized in the statement of financial position. IASB voted to rely on the existing disclosure requirements covering financial liabilities (IFRS 7, Financial Instruments: Disclosures) but require a lessee to disclose a maturity analysis of its lease liabilities separately from the maturity analyses of other financial liabilities. FASB decided not to require a lessee to disclose a maturity analysis of commitments for nonlease components related to a lease, nor provide qualitative disclosures about the existence, or terms and conditions of significant nonlease commitments it has taken on resulting from entering lease contracts. Among the new prescriptive quantitative requirements, both boards agreed short-term lease expenses—those stemming from leases at least one month but less than a year in duration—would be on the list of amounts to be presented (Item No.

3 below). The following table lists these disclosures and how U.S. generally accepted accounting principles (GAAP) compares to International Financial Reporting Standards (IFRS): 2 .

Boards Move Closer to Completing Leases Project Lessee’s Quantitative Disclosure Requirements U.S. GAAP IFRS 1 Type A lease expense, segregated between amortization of right-of-use (ROU) assets and interest on lease liabilities Amortization of ROU assets, split by class of underlying asset, and interest on lease liabilities 2 Type B lease expense N/A 3 Short-term lease expense, excluding expenses related to leases with a lease term of one month or less Short-term lease expense, excluding expenses related to leases with a lease term of one month or less, and small asset lease expense 4 Variable lease expense Variable lease expense 5 Sublease income Income from subleasing ROU assets 6 Cash paid for amounts included in the measurement of lease liabilities, segregated between operating and financing cash flows and between Type A and Type B leases Total cash outflow for leases 7 Supplemental noncash information on lease liabilities arising from obtaining ROU assets, segregated between Type A and Type B leases Additions to ROU assets, and closing carrying amount of ROU assets, split by class of underlying asset 8 Weighted-average remaining lease term, disclosed separately for Type A and Type B leases N/A 9 Weighted-average discount rate for Type B leases as of the reporting date N/A 10 Gains and losses arising from sale and leaseback transactions Gains and losses arising from sale and leaseback transactions The FASB decided to clarify that expense items disclosed also would include any amounts capitalized as part of the cost of another asset. The boards addressed qualitative disclosures as part of the respective footnote packages, as follows: 3 . Boards Move Closer to Completing Leases Project Lessee’s Qualitative Disclosure Requirements U.S. GAAP 1 Information about the nature of its leases (and subleases), including all of the following: a. A general description of those leases b. The basis, and terms and conditions, on which variable lease payments are determined c.

The existence and terms and conditions of options to extend or terminate the lease; a lessee should provide narrative disclosure about the options recognized as part of the ROU assets and lease liabilities and those that are not IFRS IASB is taking a principles-based approach to qualitative disclosure requirements, proposing to require a lessee to disclose sufficient additional information to satisfy the overall disclosure objective; IASB tentatively decided to supplement this requirement with a list of specific disclosure objectives and include illustrative examples in the final leases standard to demonstrate how a lessee might comply with this requirement d. The existence, and terms and conditions, of residual value guarantees provided by the lessee e. The restrictions or covenants imposed by leases 2 Information about leases that have not yet commenced but create significant rights and obligations for the lessee 3 Information about significant assumptions and judgments made in applying the requirements of the leases standards, which may include the following: a.

Determination of whether a contract contains a lease b. Allocation of the consideration in a contract between leases and nonlease components c. Determination of the discount rate 4 The main terms and conditions of any sale and leaseback transactions 5 Whether an accounting policy election was made for the short-term lease exemption FASB decided not to include disaggregation guidance, similar to the guidance in Topic 606 on revenue from contracts with customers, when describing the level of detail with which qualitative disclosures should be presented. The FASB decided not to provide any specified relief from the disclosure requirements for nonpublic business entities, i.e., all other entities besides public business entities.

Therefore, the lessee disclosure package is equally applicable to both public and nonpublic business entities. 4 . Boards Move Closer to Completing Leases Project Major Differences Loom The boards generally are aligned on the balance sheet treatment of lease-related assets and liabilities, tentatively agreeing to recognize all leases on the balance sheet. Major differences still exist between lease classification under IFRS and U.S. GAAP, affecting profit recognition and presentation. To recap, companies will record as liabilities all lease obligations other than short-term lease obligations (leases with a term of 12 months or less). FASB's revised dual-model approach uses criteria very similar to the lease classification tests under today's US GAAP, but without the bright lines, e.g., 75 percent of useful life and 90 percent of fair value.

Under FASB's proposed approach, the majority of today's capital leases would be Type A leases accounted for as financing arrangements (recognizing amortization on the leased asset and interest expense on the lease liability), while the majority of today's operating leases would be classified as Type B leases accounted for under the straight-line lease expense model. Regarding lessor classification, both boards agreed to do away with the receivable and residual approach proposed in the May 2013 ED. Instead, the boards tentatively agreed lessors should determine lease classification and accounting treatment—Type A versus Type B—based on whether the lease is effectively a financing or a sale, rather than an operating lease, again absent the bright lines. A lessor would make that determination by assessing whether the lease transfers substantially all the risks and rewards incidental to ownership of the underlying asset. Under FASB’s approach, companies will need to evaluate Type A leases under the criteria included in the recently issued revenue standard to determine whether a sale has occurred from the customer’s or lessee’s perspective. The absence of bright lines will increase the need to apply judgment in lease classification for both lessors and lessees, particularly when the contract is on the fringes of the old bright lines. Looking Ahead: Information Needs & System Requirements The boards will continue to meet in 2015 with hopes of converging on several issues, including lease classification and lessee expense recognition, as well as sale-leaseback transactions, effective dates and transition. The proposal has been through two exposure periods, and another exposure draft is not expected.

Companies should start evaluating their contracts to determine whether they contain a lease or a sale-leaseback transaction and, for those following U.S. GAAP, whether the lease is Type A or Type B. Both lessees and lessors will need to develop processes and procedures to capture, store and monitor pertinent data so they can determine the initial lease term, identify initial direct costs, separate lease and nonlease components, determine the discount rate and identify subleases and sale and leaseback transactions. For example, when determining the lease term upon lease commencement, lessees and lessors will need to capture all relevant factors that create an economic incentive to exercise an option to extend or not to terminate a lease or execute a purchase option.

Both parties will need to determine whether it is reasonably certain (similar to the current concept of “reasonably assured”) the lessee will exercise the option. This guidance, like other guidance in the tentative decisions, includes subjective language requiring management judgment. Throughout the lease, lessees will be required to monitor factors that could necessitate reassessing the lease term. Such factors include the occurrence of a significant event or a significant change in circumstances that are within the control of the lessee. When the lessee remeasures the lease liability due to reassessment of the lease term, the lessee also will be required to reassess variable lease payments that depend on an index or a rate and reassess the discount rate.

Entities will need procedures to evaluate and document the reasonableness of the index or rates used, as well as monitoring mechanisms to capture triggering events. Both lessees and lessors will need to monitor any change to the contractual terms and conditions not part of the original lease. Depending on the type of lease modification, an entity may account for the modification as a new lease separate from the original or as remeasurement of the existing lease. Entities will need processes to evaluate changes to leases in order to determine the proper accounting for the lease modification. 5 .

Boards Move Closer to Completing Leases Project Another item of high interest is sale-leaseback transactions. The new revenue recognition standard prohibits the recognition of seller’s profit when the seller-lessee determines the leaseback is a Type A lease. Based on the revenue recognition standard’s transfer of control criteria, the existence of a purchase option in a Type B lease also could preclude the seller-lessee from recognizing a sale—especially if the seller-lessee retains physical possession of the asset. Seller-lessees will need to evaluate all sale-leaseback transactions for potential restatement. Companies are encouraged to start preparing for the new standard by gathering contractual documents and cataloguing existing leases.

Companies also should evaluate resource requirements, including information systems, to ensure they have the appropriate infrastructure to successfully implement the new standard. For additional guidance, consult your BKD advisor. Additional Resources BKD Hot Topics: Lease Accounting Contributor Connie Spinelli Director 303.861.4545 cspinelli@bkd.com 6 .