Description

Bullseye

Highlights

Volatility & Diversification

B

y seeking diversification, investors try to reduce risk, increase returns, or ideally, achieve both. Unfortunately,

many investors take the wrong approach to accomplishing these goals. For years, the focus for diversification

has been largely one-sided, with a large emphasis on risk reduction at the expense of the entire portfolio. In

focusing solely on risk reduction, investors tend to seek low-volatility investments in order to moderate the

swings of their equity-heavy exposure.

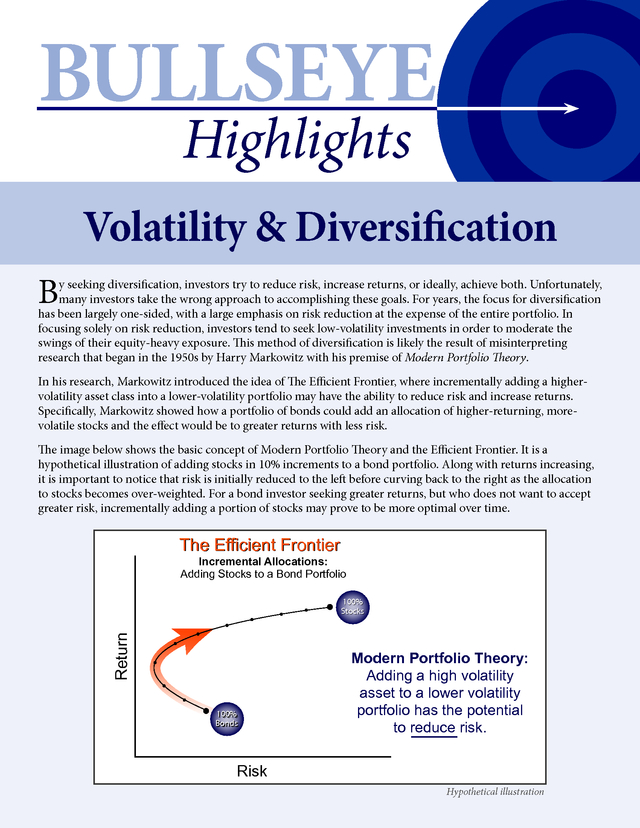

This method of diversification is likely the result of misinterpreting research that began in the 1950s by Harry Markowitz with his premise of Modern Portfolio Theory. In his research, Markowitz introduced the idea of The Efficient Frontier, where incrementally adding a highervolatility asset class into a lower-volatility portfolio may have the ability to reduce risk and increase returns. Specifically, Markowitz showed how a portfolio of bonds could add an allocation of higher-returning, morevolatile stocks and the effect would be to greater returns with less risk. The image below shows the basic concept of Modern Portfolio Theory and the Efficient Frontier. It is a hypothetical illustration of adding stocks in 10% increments to a bond portfolio. Along with returns increasing, it is important to notice that risk is initially reduced to the left before curving back to the right as the allocation to stocks becomes over-weighted.

For a bond investor seeking greater returns, but who does not want to accept greater risk, incrementally adding a portion of stocks may prove to be more optimal over time. The Efficient Frontier Incremental Allocations: Adding Stocks to a Bond Portfolio Return 100% Stocks 100% 100% Bonds Bonds Modern Portfolio Theory: Adding a high volatility asset to a lower volatility portfolio has the potential to reduce risk. Risk Hypothetical illustration . It seems that many of today’s investors have it backwards. They start with a risky portfolio, largely comprised of stocks, and try to add less-volatile assets to reduce risk—and they are often surprised when they also get less return. It would benefit them to heed Markowitz’s guidance. His objective was to lower risk and increase returns by adding higher-volatility asset classes with strong return characteristics. How can adding a volatile asset class such as stocks reduce the risk of a bond portfolio? Most would think that adding stocks would raise the average volatility of the combined portfolio.

But it doesn’t. That’s because of correlation—which measures the relationship of two investments. The lower the correlation, the greater the chance for an asset to provide diversification benefits.

And if investments are going up and down at different times, some of the volatility is cancelled out. The images below illustrate the impact of adding high-returning, high-volatility assets incrementally to a portfolio. If an asset is highly correlated, there will be little or no curve in the frontier—rather, a straight line will form with each allocation, and risk is increased along the way (left image). Provided the high-volatility asset has very low correlation, the curve will be more dramatic, initially reducing risk before it begins increasing (right image). The idea is to find an optimal point where the risk/return level matches an investor’s risk tolerance and objectives. Correlated Volatility Non-Correlated Volatility B Return Return B A Risk Increases at Every Blended Allocation Point Risk Optimal Blend Same Risk, Higher Return A Risk Hypothetical illustrations Quick “CAR” Test: Correlation-Adjusted Risk A simplified “quick check” when comparing investments with similar risk/return characteristics is to multiply the standard deviation by the correlation to a benchmark (like the S&P 500 or a core portfolio). The one with lower resulting CAR score should offer a hint towards the investment with the greater diversification potential. Summary: Not all high-volatility assets are the same.

Some high return/high volatility investments—such as international companies, emerging markets and sectors like technology—also have periods of high correlation to domestic stocks, especially during periods of market stress. But there are some—managed futures, commodities and REITs, for instance—that have a history of maintaining low correlation to domestic stocks, even during market stress. In fact, the more volatile and less correlating an investment is relative to a core portfolio, the less of it you have to use to receive the potential diversification benefits.

When used in concert with correlation, highvolatility assets may enhance returns and lower risk in a well-diversified portfolio. *Correlation-Adjusted Risk (CAR) methodology is not intended as a sole factor for portfolio analysis. Further analysis should occur. Past performance is not indicative of future returns. Images shown are for illustration purposes only and should not be used as a predictive measure for the future return expectations of any investment.The information is subject to change (based on market fluctuation and other conditions) and should not be construed as a recommendation of any specific security or investment product, and was prepared without regard for specific circumstances and objectives of any individual investor.

Traditional, nontraditional and alternative investments involve risks, including the potential for loss of principal. Nontraditional and alternative investments may involve additional risks, including, but not limited to, shorting risks, the use of leverage, the use of derivatives, futures market speculation and regulatory changes. Before investing in any financial product, always read the prospectus and/or offering memorandum for product-specific risks.

Arrow Funds are distributed by an affiliate, Archer Distributors, LLC (member FINRA). AD-110615 .

This method of diversification is likely the result of misinterpreting research that began in the 1950s by Harry Markowitz with his premise of Modern Portfolio Theory. In his research, Markowitz introduced the idea of The Efficient Frontier, where incrementally adding a highervolatility asset class into a lower-volatility portfolio may have the ability to reduce risk and increase returns. Specifically, Markowitz showed how a portfolio of bonds could add an allocation of higher-returning, morevolatile stocks and the effect would be to greater returns with less risk. The image below shows the basic concept of Modern Portfolio Theory and the Efficient Frontier. It is a hypothetical illustration of adding stocks in 10% increments to a bond portfolio. Along with returns increasing, it is important to notice that risk is initially reduced to the left before curving back to the right as the allocation to stocks becomes over-weighted.

For a bond investor seeking greater returns, but who does not want to accept greater risk, incrementally adding a portion of stocks may prove to be more optimal over time. The Efficient Frontier Incremental Allocations: Adding Stocks to a Bond Portfolio Return 100% Stocks 100% 100% Bonds Bonds Modern Portfolio Theory: Adding a high volatility asset to a lower volatility portfolio has the potential to reduce risk. Risk Hypothetical illustration . It seems that many of today’s investors have it backwards. They start with a risky portfolio, largely comprised of stocks, and try to add less-volatile assets to reduce risk—and they are often surprised when they also get less return. It would benefit them to heed Markowitz’s guidance. His objective was to lower risk and increase returns by adding higher-volatility asset classes with strong return characteristics. How can adding a volatile asset class such as stocks reduce the risk of a bond portfolio? Most would think that adding stocks would raise the average volatility of the combined portfolio.

But it doesn’t. That’s because of correlation—which measures the relationship of two investments. The lower the correlation, the greater the chance for an asset to provide diversification benefits.

And if investments are going up and down at different times, some of the volatility is cancelled out. The images below illustrate the impact of adding high-returning, high-volatility assets incrementally to a portfolio. If an asset is highly correlated, there will be little or no curve in the frontier—rather, a straight line will form with each allocation, and risk is increased along the way (left image). Provided the high-volatility asset has very low correlation, the curve will be more dramatic, initially reducing risk before it begins increasing (right image). The idea is to find an optimal point where the risk/return level matches an investor’s risk tolerance and objectives. Correlated Volatility Non-Correlated Volatility B Return Return B A Risk Increases at Every Blended Allocation Point Risk Optimal Blend Same Risk, Higher Return A Risk Hypothetical illustrations Quick “CAR” Test: Correlation-Adjusted Risk A simplified “quick check” when comparing investments with similar risk/return characteristics is to multiply the standard deviation by the correlation to a benchmark (like the S&P 500 or a core portfolio). The one with lower resulting CAR score should offer a hint towards the investment with the greater diversification potential. Summary: Not all high-volatility assets are the same.

Some high return/high volatility investments—such as international companies, emerging markets and sectors like technology—also have periods of high correlation to domestic stocks, especially during periods of market stress. But there are some—managed futures, commodities and REITs, for instance—that have a history of maintaining low correlation to domestic stocks, even during market stress. In fact, the more volatile and less correlating an investment is relative to a core portfolio, the less of it you have to use to receive the potential diversification benefits.

When used in concert with correlation, highvolatility assets may enhance returns and lower risk in a well-diversified portfolio. *Correlation-Adjusted Risk (CAR) methodology is not intended as a sole factor for portfolio analysis. Further analysis should occur. Past performance is not indicative of future returns. Images shown are for illustration purposes only and should not be used as a predictive measure for the future return expectations of any investment.The information is subject to change (based on market fluctuation and other conditions) and should not be construed as a recommendation of any specific security or investment product, and was prepared without regard for specific circumstances and objectives of any individual investor.

Traditional, nontraditional and alternative investments involve risks, including the potential for loss of principal. Nontraditional and alternative investments may involve additional risks, including, but not limited to, shorting risks, the use of leverage, the use of derivatives, futures market speculation and regulatory changes. Before investing in any financial product, always read the prospectus and/or offering memorandum for product-specific risks.

Arrow Funds are distributed by an affiliate, Archer Distributors, LLC (member FINRA). AD-110615 .