Description

Bullseye

Highlights

Tactical Beta

I

nvestment planning can be similar to planning a trip. A road might look perfectly straight on a map, but it doesn’t show the bumps along

the way. And as we all know, it’s very hard to reach your destination if the journey is too difficult. Most diversified investment strategies

attempt to provide positive returns with varying degrees of risk over time.

But Tactical Asset Allocation tries to create a smoother ride by looking for a path with fewer bumps along the way. There are two basic approaches to asset allocation: Strategic (passive) and Tactical (active). Generally, a Strategic Asset Allocation approach identifies a mix of asset classes based on long-term averages and periodically rebalances the portfolio, typically on a calendar basis. Strategic Asset Allocation tries to achieve passive returns by moving up and down in step with the markets. When an investment moves in conjunction with an overall market it is known as having Beta.

For example, having a higher Beta of 1.0 means you would expect performance equal to 100% of the stock market. Whereas a relatively lower Beta of 0.2 might indicate only 20% of market performance. The basic idea of Tactical Asset Allocation is to seek high Beta when markets are doing well and avoid it when they aren’t—in other words, Tactical Beta. This may seem like an obvious approach, but Strategic models generally don’t follow that logic. Instead, Strategic models seem to follow the philosophy that markets go up and down, but things will eventually average out over time.

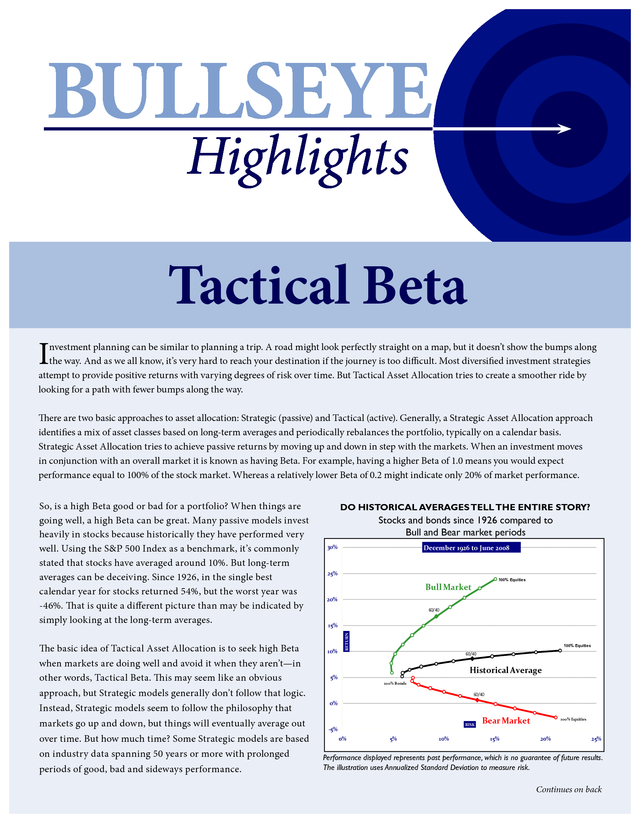

But how much time? Some Strategic models are based on industry data spanning 50 years or more with prolonged periods of good, bad and sideways performance. DO HISTORICAL AVERAGES TELL THE ENTIRE STORY? Stocks and bonds since 1926 compared to Bull and Bear market periods December 1926 to June 2008 30% 25% 100% Equities Bull Market 20% 60/40 15% 10% RETURN So, is a high Beta good or bad for a portfolio? When things are going well, a high Beta can be great. Many passive models invest heavily in stocks because historically they have performed very well. Using the S&P 500 Index as a benchmark, it’s commonly stated that stocks have averaged around 10%.

But long-term averages can be deceiving. Since 1926, in the single best calendar year for stocks returned 54%, but the worst year was -46%. That is quite a different picture than may be indicated by simply looking at the long-term averages. 100% Equities 60/40 Historical Average 5% 100% Bonds 60/40 0% RISK -5% 0% 5% 10% Bear Market 15% 100% Equities 20% 25% Performance displayed represents past performance, which is no guarantee of future results. The illustration uses Annualized Standard Deviation to measure risk. Continues on back .

It is important not to confuse the word Tactical with speculation or market timing. Many Tactical models don’t try to predict the future. Instead, they simply react to changes in the current market. Short-term volatility swings and “choppy markets” will likely be felt by any asset allocation approach, either Strategic or Tactical.

But for an investor with a three-, five- or 10-year time horizon, prolonged sideways or negative periods may never be offset if they invest at the wrong time. And for investors with a much longer time horizon, they may not be able to endure the prolonged volatility while the markets average out in their favor. From January 2000 to December 2006, the stock market had both good and bad periods.

The first three years were considered a Bear Market after the “internet bubble” burst. However, the following three-year Bull Market showed consistent growth as stocks once again rebounded. During that full six-year period, the 60/40 portfolio risk levels averaged 8.19 standard deviation (a statistic used to measure risk). Over that time period, a passive 60/40 portfolio would have taken on the most risk in the worst three years and the least risk in the best three years. The resulting risk levels were nothing more than a simple by-product of predetermined Beta exposure.

A basic Tactical approach of more frequent rebalancing and seeking out stronger asset classes may have likely improved the 60/40 results. Today, many Strategic Asset Allocation portfolios try to reduce volatility through basic diversification by adding asset classes that are not historically correlated to stocks. But as the old saying goes, “The only thing that goes up during a bear market is correlation.” The returns for most investable asset classes are cyclical as they fall in and out of favor. And their Beta relative to the stock market can fluctuate depending on the market environment, as illustrated in the table below. Returns, Risk and Beta of Multiple Asset Classes From January 2000 to December 2006 Combined Bull & Bear Market Periods Jan 2000 - Dec 2006 Return Risk U.S.

Stocks -0.8% Bonds 6.3% International Stocks Bear Market Jan 2000 - Mar 2003 Beta Return Risk 14.69 1.00 -16.1% 4.1 -0.08 9.8% 3.1% 15.7 0.87 Growth Stocks -7.1% 18.92 Value Stocks 7.2% 13.94 Emerging Markets 10.8% Commodities 13.1% Gold 13.2% 15.6 Real Estate 23.4% 18.07 60/40 Portfolio 2.3% 8.19 Tactical Portfolio 8.5% 9.19 Bull Market Apr 2003 - Dec 2006 Beta Return Risk Beta 15.3 1.00 17.2% 10.22 1.00 3.71 -0.08 2.9% 4.25 -0.01 -19.3% 13.02 0.75 31.7% 13.94 1.02 1.28 -25.5% 19.82 1.33 15.8% 11.35 1.07 0.79 -6.1% 14.31 0.72 22.5% 11.32 1.03 24.49 1.17 -16.3% 20.45 1.04 46.7% 24.07 1.38 26.49 -0.01 7.7% 26.7 0.01 18.8% 26.44 -0.25 0.00 6.6% 13.49 -0.13 20.2% 17.74 0.30 0.27 14.5% 15.15 0.11 33.1% 20.96 0.77 0.54 -6.0% 8.91 0.53 11.3% 6.03 0.59 0.39 -0.5% 8.26 0.31 18.3% 9.44 0.65 Performance displayed represents past performance, which is no guarantee of future results.The illustration uses annualized standard deviation to measure risk. Unlike a passive approach, a Tactical Beta strategy use active management to adjust the Beta exposure of various asset classes as the market environment dictates. It’s true that basic diversification through the use of noncorrelated assets may provide the potential benefit of alternate sources of returns during good times. But there is an even greater potential benefit when the model also has the flexibility to avoid those asset classes when things are bad.

It would be incorrect to assume that Tactical models always outperform Strategic models. In fact, a Strategic model with a large allocation to stocks may show very strong performance during bull markets. The performance may also average out quite nicely over the long-term as well. But there may also be prolonged periods of erratic volatility swings in between.

A Tactical Asset Allocation model’s objective is not necessarily to outperform a Strategic model at any specific time. Instead, the idea is to seek better long-term risk-adjusted returns. The destination remains the same.

But hopefully the ride is smooth enough that investors are actually able to finish the journey. Disclosure Performance displayed represents past performance, which is no guarantee of future results. Source: Bloomberg, calculated by Arrow Funds using data through 6/30/2008. Equities are represented by the S&P 500 Index.

Bonds are represented by the Lehman Aggregate Bond Index. International Stocks are represented by the EAFE Index. Commodities are represented by the GSCI Index.

Growth stocks and Value stocks are represented by their respective Russell 3000 Index. REITs are represented by the DJ Wilshire REIT Index. The Strategic Portfolio is a 60/40 blend of equities and bonds.

The Tactical Portfolio is based on a proprietary model using relative strength, tactical rebalancing and other factors (for more information, contact Arrow Funds). Index returns assume re-investment of all dividends and do not reflect any management fees, transaction costs or expenses. The indices are unmanaged and are not available for direct investment. 0891-NLD-8/28/2008 .

But Tactical Asset Allocation tries to create a smoother ride by looking for a path with fewer bumps along the way. There are two basic approaches to asset allocation: Strategic (passive) and Tactical (active). Generally, a Strategic Asset Allocation approach identifies a mix of asset classes based on long-term averages and periodically rebalances the portfolio, typically on a calendar basis. Strategic Asset Allocation tries to achieve passive returns by moving up and down in step with the markets. When an investment moves in conjunction with an overall market it is known as having Beta.

For example, having a higher Beta of 1.0 means you would expect performance equal to 100% of the stock market. Whereas a relatively lower Beta of 0.2 might indicate only 20% of market performance. The basic idea of Tactical Asset Allocation is to seek high Beta when markets are doing well and avoid it when they aren’t—in other words, Tactical Beta. This may seem like an obvious approach, but Strategic models generally don’t follow that logic. Instead, Strategic models seem to follow the philosophy that markets go up and down, but things will eventually average out over time.

But how much time? Some Strategic models are based on industry data spanning 50 years or more with prolonged periods of good, bad and sideways performance. DO HISTORICAL AVERAGES TELL THE ENTIRE STORY? Stocks and bonds since 1926 compared to Bull and Bear market periods December 1926 to June 2008 30% 25% 100% Equities Bull Market 20% 60/40 15% 10% RETURN So, is a high Beta good or bad for a portfolio? When things are going well, a high Beta can be great. Many passive models invest heavily in stocks because historically they have performed very well. Using the S&P 500 Index as a benchmark, it’s commonly stated that stocks have averaged around 10%.

But long-term averages can be deceiving. Since 1926, in the single best calendar year for stocks returned 54%, but the worst year was -46%. That is quite a different picture than may be indicated by simply looking at the long-term averages. 100% Equities 60/40 Historical Average 5% 100% Bonds 60/40 0% RISK -5% 0% 5% 10% Bear Market 15% 100% Equities 20% 25% Performance displayed represents past performance, which is no guarantee of future results. The illustration uses Annualized Standard Deviation to measure risk. Continues on back .

It is important not to confuse the word Tactical with speculation or market timing. Many Tactical models don’t try to predict the future. Instead, they simply react to changes in the current market. Short-term volatility swings and “choppy markets” will likely be felt by any asset allocation approach, either Strategic or Tactical.

But for an investor with a three-, five- or 10-year time horizon, prolonged sideways or negative periods may never be offset if they invest at the wrong time. And for investors with a much longer time horizon, they may not be able to endure the prolonged volatility while the markets average out in their favor. From January 2000 to December 2006, the stock market had both good and bad periods.

The first three years were considered a Bear Market after the “internet bubble” burst. However, the following three-year Bull Market showed consistent growth as stocks once again rebounded. During that full six-year period, the 60/40 portfolio risk levels averaged 8.19 standard deviation (a statistic used to measure risk). Over that time period, a passive 60/40 portfolio would have taken on the most risk in the worst three years and the least risk in the best three years. The resulting risk levels were nothing more than a simple by-product of predetermined Beta exposure.

A basic Tactical approach of more frequent rebalancing and seeking out stronger asset classes may have likely improved the 60/40 results. Today, many Strategic Asset Allocation portfolios try to reduce volatility through basic diversification by adding asset classes that are not historically correlated to stocks. But as the old saying goes, “The only thing that goes up during a bear market is correlation.” The returns for most investable asset classes are cyclical as they fall in and out of favor. And their Beta relative to the stock market can fluctuate depending on the market environment, as illustrated in the table below. Returns, Risk and Beta of Multiple Asset Classes From January 2000 to December 2006 Combined Bull & Bear Market Periods Jan 2000 - Dec 2006 Return Risk U.S.

Stocks -0.8% Bonds 6.3% International Stocks Bear Market Jan 2000 - Mar 2003 Beta Return Risk 14.69 1.00 -16.1% 4.1 -0.08 9.8% 3.1% 15.7 0.87 Growth Stocks -7.1% 18.92 Value Stocks 7.2% 13.94 Emerging Markets 10.8% Commodities 13.1% Gold 13.2% 15.6 Real Estate 23.4% 18.07 60/40 Portfolio 2.3% 8.19 Tactical Portfolio 8.5% 9.19 Bull Market Apr 2003 - Dec 2006 Beta Return Risk Beta 15.3 1.00 17.2% 10.22 1.00 3.71 -0.08 2.9% 4.25 -0.01 -19.3% 13.02 0.75 31.7% 13.94 1.02 1.28 -25.5% 19.82 1.33 15.8% 11.35 1.07 0.79 -6.1% 14.31 0.72 22.5% 11.32 1.03 24.49 1.17 -16.3% 20.45 1.04 46.7% 24.07 1.38 26.49 -0.01 7.7% 26.7 0.01 18.8% 26.44 -0.25 0.00 6.6% 13.49 -0.13 20.2% 17.74 0.30 0.27 14.5% 15.15 0.11 33.1% 20.96 0.77 0.54 -6.0% 8.91 0.53 11.3% 6.03 0.59 0.39 -0.5% 8.26 0.31 18.3% 9.44 0.65 Performance displayed represents past performance, which is no guarantee of future results.The illustration uses annualized standard deviation to measure risk. Unlike a passive approach, a Tactical Beta strategy use active management to adjust the Beta exposure of various asset classes as the market environment dictates. It’s true that basic diversification through the use of noncorrelated assets may provide the potential benefit of alternate sources of returns during good times. But there is an even greater potential benefit when the model also has the flexibility to avoid those asset classes when things are bad.

It would be incorrect to assume that Tactical models always outperform Strategic models. In fact, a Strategic model with a large allocation to stocks may show very strong performance during bull markets. The performance may also average out quite nicely over the long-term as well. But there may also be prolonged periods of erratic volatility swings in between.

A Tactical Asset Allocation model’s objective is not necessarily to outperform a Strategic model at any specific time. Instead, the idea is to seek better long-term risk-adjusted returns. The destination remains the same.

But hopefully the ride is smooth enough that investors are actually able to finish the journey. Disclosure Performance displayed represents past performance, which is no guarantee of future results. Source: Bloomberg, calculated by Arrow Funds using data through 6/30/2008. Equities are represented by the S&P 500 Index.

Bonds are represented by the Lehman Aggregate Bond Index. International Stocks are represented by the EAFE Index. Commodities are represented by the GSCI Index.

Growth stocks and Value stocks are represented by their respective Russell 3000 Index. REITs are represented by the DJ Wilshire REIT Index. The Strategic Portfolio is a 60/40 blend of equities and bonds.

The Tactical Portfolio is based on a proprietary model using relative strength, tactical rebalancing and other factors (for more information, contact Arrow Funds). Index returns assume re-investment of all dividends and do not reflect any management fees, transaction costs or expenses. The indices are unmanaged and are not available for direct investment. 0891-NLD-8/28/2008 .