Description

Bullseye

Highlights

Scare Markets

M

ost people know about bull markets and bear markets, but may not be familiar with

“scare markets”—bull markets that briefly disguise themselves and scare investors

into thinking it’s the start of a bear market. These scare markets are more commonly

referred to as temporary market corrections.

Corrections are generally understood to be short-term market losses lasting only a few

days, weeks or perhaps a few months. The drawdown from the peak to the lowest point

may be significant, perhaps in the 5% to 15% range, before rebounding upward. These

corrections can be caused by a number of circumstances, but the key factor is that the

period is generally brief and the losses are quickly recovered.

Bear markets are longer-term periods that can last several months and even years, with declines of 20% or more. The recovery time back to the breakeven point can take quite some time in a true bear market. So how can an investor tell the difference between a bear market and a scare market? Without the benefit of hindsight, it’s impossible to say with certainty. But there are some tell-tale signs at the heart of every scare market.

Scare market corrections are often driven by the fear of uncertainty and potential problems with the markets, whereas bear markets tend to be caused by actual problems with the markets. Since the year 2000, there have been two significant bear markets: the “Internet Bubble” (early 2000-2003) and the “Financial Crisis” (late 2007-2008). Those two bear markets had something in common—they were caused by actual fundamental problems with the financial markets. Ultimately, both of those bear markets were followed by significant bullish recovery periods, but it took some time to get back to even. Internet Bubble 140 120 100 80 ery v Reco Financial Crisis ry ove Rec Break Even From 2007 Peak 160 Bull and Bear Markets Since March 2000 Peak Break Even From 2000 Peak 180 60 40 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Year Past performance is no indication of future returns.

S&P 500 Total Return Index data from 3/24/2000 through 9/30/2014. Index performance assumes reinvestment of dividends, but does not include fees. Indexes are not available for direct investment.

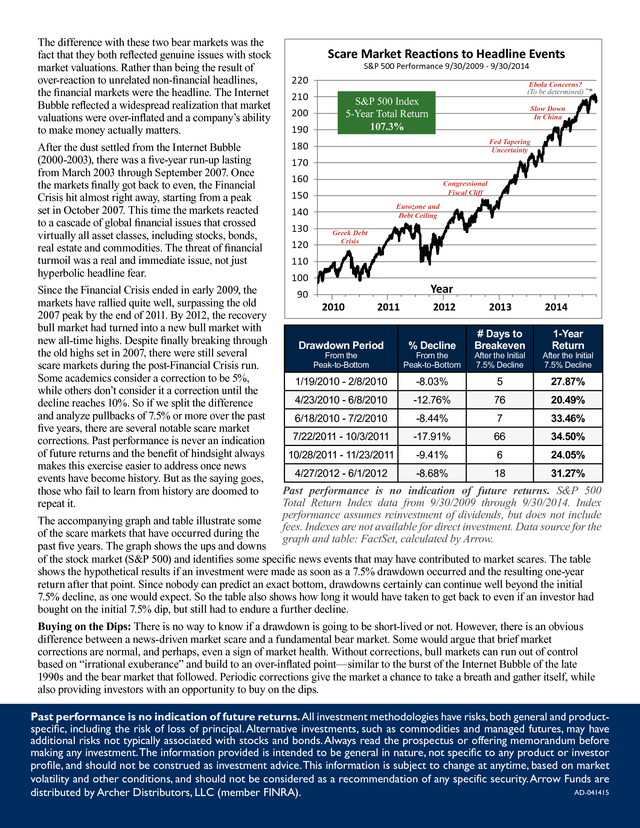

Data source: FactSet, calculated by Arrow. . The difference with these two bear markets was the Scare Market Reactions to Headline Events fact that they both reflected genuine issues with stock S&P 500 Performance 9/30/2009 - 9/30/2014 market valuations. Rather than being the result of 220 over-reaction to unrelated non-financial headlines, Ebola Concerns? (To be determined) the financial markets were the headline. The Internet 210 S&P 500 Index Bubble reflected a widespread realization that market Slow Down 200 5-Year Total Return In China valuations were over-inflated and a company’s ability 107.3% 190 to make money actually matters. Fed Tapering 180 After the dust settled from the Internet Bubble Uncertainty (2000-2003), there was a five-year run-up lasting 170 from March 2003 through September 2007. Once 160 Congressional the markets finally got back to even, the Financial Fiscal Cliff 150 Crisis hit almost right away, starting from a peak Eurozone and set in October 2007.

This time the markets reacted 140 Debt Ceiling to a cascade of global financial issues that crossed 130 Greek Debt virtually all asset classes, including stocks, bonds, Crisis 120 real estate and commodities. The threat of financial turmoil was a real and immediate issue, not just 110 hyperbolic headline fear. 100 Year Since the Financial Crisis ended in early 2009, the 90 markets have rallied quite well, surpassing the old 2010 2011 2012 2013 2014 2007 peak by the end of 2011. By 2012, the recovery bull market had turned into a new bull market with # Days to 1-Year new all-time highs.

Despite finally breaking through Drawdown Period % Decline Breakeven Return the old highs set in 2007, there were still several From the From the After the Initial After the Initial Peak-to-Bottom Peak-to-Bottom 7.5% Decline 7.5% Decline scare markets during the post-Financial Crisis run. Some academics consider a correction to be 5%, 1/19/2010 - 2/8/2010 -8.03% 5 27.87% while others don’t consider it a correction until the 4/23/2010 - 6/8/2010 -12.76% 76 20.49% decline reaches 10%. So if we split the difference and analyze pullbacks of 7.5% or more over the past 6/18/2010 - 7/2/2010 -8.44% 7 33.46% five years, there are several notable scare market 7/22/2011 - 10/3/2011 -17.91% 66 34.50% corrections. Past performance is never an indication of future returns and the benefit of hindsight always 10/28/2011 - 11/23/2011 -9.41% 6 24.05% makes this exercise easier to address once news 4/27/2012 - 6/1/2012 -8.68% 18 31.27% events have become history.

But as the saying goes, Past performance is no indication of future returns. S&P 500 those who fail to learn from history are doomed to Total Return Index data from 9/30/2009 through 9/30/2014. Index repeat it. performance assumes reinvestment of dividends, but does not include The accompanying graph and table illustrate some fees.

Indexes are not available for direct investment. Data source for the of the scare markets that have occurred during the graph and table: FactSet, calculated by Arrow. past five years. The graph shows the ups and downs of the stock market (S&P 500) and identifies some specific news events that may have contributed to market scares.

The table shows the hypothetical results if an investment were made as soon as a 7.5% drawdown occurred and the resulting one-year return after that point. Since nobody can predict an exact bottom, drawdowns certainly can continue well beyond the initial 7.5% decline, as one would expect. So the table also shows how long it would have taken to get back to even if an investor had bought on the initial 7.5% dip, but still had to endure a further decline. Buying on the Dips: There is no way to know if a drawdown is going to be short-lived or not.

However, there is an obvious difference between a news-driven market scare and a fundamental bear market. Some would argue that brief market corrections are normal, and perhaps, even a sign of market health. Without corrections, bull markets can run out of control based on “irrational exuberance” and build to an over-inflated point—similar to the burst of the Internet Bubble of the late 1990s and the bear market that followed.

Periodic corrections give the market a chance to take a breath and gather itself, while also providing investors with an opportunity to buy on the dips. Past performance is no indication of future returns. All investment methodologies have risks, both general and productspecific, including the risk of loss of principal. Alternative investments, such as commodities and managed futures, may have additional risks not typically associated with stocks and bonds.

Always read the prospectus or offering memorandum before making any investment. The information provided is intended to be general in nature, not specific to any product or investor profile, and should not be construed as investment advice. This information is subject to change at anytime, based on market volatility and other conditions, and should not be considered as a recommendation of any specific security.

Arrow Funds are AD-041415 distributed by Archer Distributors, LLC (member FINRA). .

Bear markets are longer-term periods that can last several months and even years, with declines of 20% or more. The recovery time back to the breakeven point can take quite some time in a true bear market. So how can an investor tell the difference between a bear market and a scare market? Without the benefit of hindsight, it’s impossible to say with certainty. But there are some tell-tale signs at the heart of every scare market.

Scare market corrections are often driven by the fear of uncertainty and potential problems with the markets, whereas bear markets tend to be caused by actual problems with the markets. Since the year 2000, there have been two significant bear markets: the “Internet Bubble” (early 2000-2003) and the “Financial Crisis” (late 2007-2008). Those two bear markets had something in common—they were caused by actual fundamental problems with the financial markets. Ultimately, both of those bear markets were followed by significant bullish recovery periods, but it took some time to get back to even. Internet Bubble 140 120 100 80 ery v Reco Financial Crisis ry ove Rec Break Even From 2007 Peak 160 Bull and Bear Markets Since March 2000 Peak Break Even From 2000 Peak 180 60 40 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Year Past performance is no indication of future returns.

S&P 500 Total Return Index data from 3/24/2000 through 9/30/2014. Index performance assumes reinvestment of dividends, but does not include fees. Indexes are not available for direct investment.

Data source: FactSet, calculated by Arrow. . The difference with these two bear markets was the Scare Market Reactions to Headline Events fact that they both reflected genuine issues with stock S&P 500 Performance 9/30/2009 - 9/30/2014 market valuations. Rather than being the result of 220 over-reaction to unrelated non-financial headlines, Ebola Concerns? (To be determined) the financial markets were the headline. The Internet 210 S&P 500 Index Bubble reflected a widespread realization that market Slow Down 200 5-Year Total Return In China valuations were over-inflated and a company’s ability 107.3% 190 to make money actually matters. Fed Tapering 180 After the dust settled from the Internet Bubble Uncertainty (2000-2003), there was a five-year run-up lasting 170 from March 2003 through September 2007. Once 160 Congressional the markets finally got back to even, the Financial Fiscal Cliff 150 Crisis hit almost right away, starting from a peak Eurozone and set in October 2007.

This time the markets reacted 140 Debt Ceiling to a cascade of global financial issues that crossed 130 Greek Debt virtually all asset classes, including stocks, bonds, Crisis 120 real estate and commodities. The threat of financial turmoil was a real and immediate issue, not just 110 hyperbolic headline fear. 100 Year Since the Financial Crisis ended in early 2009, the 90 markets have rallied quite well, surpassing the old 2010 2011 2012 2013 2014 2007 peak by the end of 2011. By 2012, the recovery bull market had turned into a new bull market with # Days to 1-Year new all-time highs.

Despite finally breaking through Drawdown Period % Decline Breakeven Return the old highs set in 2007, there were still several From the From the After the Initial After the Initial Peak-to-Bottom Peak-to-Bottom 7.5% Decline 7.5% Decline scare markets during the post-Financial Crisis run. Some academics consider a correction to be 5%, 1/19/2010 - 2/8/2010 -8.03% 5 27.87% while others don’t consider it a correction until the 4/23/2010 - 6/8/2010 -12.76% 76 20.49% decline reaches 10%. So if we split the difference and analyze pullbacks of 7.5% or more over the past 6/18/2010 - 7/2/2010 -8.44% 7 33.46% five years, there are several notable scare market 7/22/2011 - 10/3/2011 -17.91% 66 34.50% corrections. Past performance is never an indication of future returns and the benefit of hindsight always 10/28/2011 - 11/23/2011 -9.41% 6 24.05% makes this exercise easier to address once news 4/27/2012 - 6/1/2012 -8.68% 18 31.27% events have become history.

But as the saying goes, Past performance is no indication of future returns. S&P 500 those who fail to learn from history are doomed to Total Return Index data from 9/30/2009 through 9/30/2014. Index repeat it. performance assumes reinvestment of dividends, but does not include The accompanying graph and table illustrate some fees.

Indexes are not available for direct investment. Data source for the of the scare markets that have occurred during the graph and table: FactSet, calculated by Arrow. past five years. The graph shows the ups and downs of the stock market (S&P 500) and identifies some specific news events that may have contributed to market scares.

The table shows the hypothetical results if an investment were made as soon as a 7.5% drawdown occurred and the resulting one-year return after that point. Since nobody can predict an exact bottom, drawdowns certainly can continue well beyond the initial 7.5% decline, as one would expect. So the table also shows how long it would have taken to get back to even if an investor had bought on the initial 7.5% dip, but still had to endure a further decline. Buying on the Dips: There is no way to know if a drawdown is going to be short-lived or not.

However, there is an obvious difference between a news-driven market scare and a fundamental bear market. Some would argue that brief market corrections are normal, and perhaps, even a sign of market health. Without corrections, bull markets can run out of control based on “irrational exuberance” and build to an over-inflated point—similar to the burst of the Internet Bubble of the late 1990s and the bear market that followed.

Periodic corrections give the market a chance to take a breath and gather itself, while also providing investors with an opportunity to buy on the dips. Past performance is no indication of future returns. All investment methodologies have risks, both general and productspecific, including the risk of loss of principal. Alternative investments, such as commodities and managed futures, may have additional risks not typically associated with stocks and bonds.

Always read the prospectus or offering memorandum before making any investment. The information provided is intended to be general in nature, not specific to any product or investor profile, and should not be construed as investment advice. This information is subject to change at anytime, based on market volatility and other conditions, and should not be considered as a recommendation of any specific security.

Arrow Funds are AD-041415 distributed by Archer Distributors, LLC (member FINRA). .