Description

Getting Started Guide

For Community Banks

06/27/2011

. Welcome to the Getting Started Guide for the Small

Business Lending Fund. This guidebook is an overview

designed specifically for community banks – a term used

here to include banks, thrifts, and bank and thrift holding

companies with assets of less than $10 billion.

Small businesses are a vital part

of the American economy. Their success

is a necessary component of the

economic recovery. Currently, many small

businesses face challenges in accessing

the credit they need.

Enacted into law as part of the Small Business Jobs Act of 2010 This guidebook is divided into four chapters. Chapter One provides a general overview of Small Business Lending Fund benefits, eligibility, and terms. Chapter Two provides information relating to the application process.

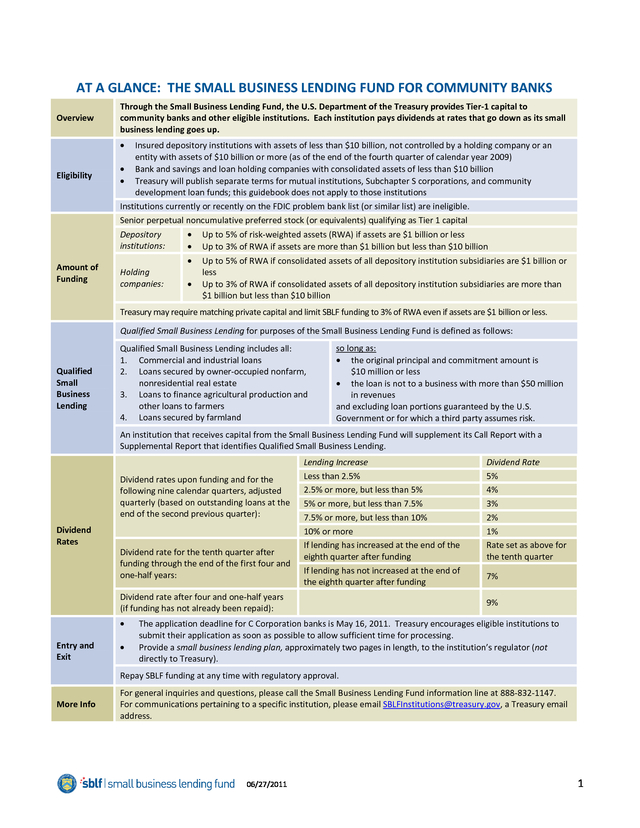

Chapter Three provides more detailed information about how the Small Business Lending Fund works – specifically, what qualifies as small business lending, how dividends are calculated, and how to address applicable reporting requirements. Chapter Four describes what happens after an institution receives SBLF funding. If you have questions at any point, please contact the information line for the Small Business Lending Fund at 888-832-1147 (Monday-Friday, 9:00 AM-7:00 PM ET). to increase small business lending, the Small Business Lending Fund is designed to provide up to $30 billion in capital to qualified community banks and other eligible financial institutions. The Small Business Lending Fund will help TABLE OF CONTENTS AT A GLANCE: The Small Business Lending Fund for Community Banks 1 CHAPTER ONE: Introduction 2 CHAPTER TWO: How to Apply to the Small Business Lending Fund 6 create jobs and promote economic growth in local communities across the nation while enabling Main Street banks to better extend credit to their customers by utilizing 06/27/2011 CHAPTER THREE: How the Small Business Lending Fund Works 11 CHAPTER FOUR: After Your Bank Receives Funding the incentives that the Fund provides. 17 . AT A GLANCE: THE SMALL BUSINESS LENDING FUND FOR COMMUNITY BANKS Overview Through the Small Business Lending Fund, the U.S. Department of the Treasury provides Tier-1 capital to community banks and other eligible institutions. Each institution pays dividends at rates that go down as its small business lending goes up. • Eligibility Insured depository institutions with assets of less than $10 billion, not controlled by a holding company or an entity with assets of $10 billion or more (as of the end of the fourth quarter of calendar year 2009) • Bank and savings and loan holding companies with consolidated assets of less than $10 billion • Treasury will publish separate terms for mutual institutions, Subchapter S corporations, and community development loan funds; this guidebook does not apply to those institutions Institutions currently or recently on the FDIC problem bank list (or similar list) are ineligible. Senior perpetual noncumulative preferred stock (or equivalents) qualifying as Tier 1 capital Amount of Funding Holding companies: • • Up to 5% of risk-weighted assets (RWA) if assets are $1 billion or less Up to 3% of RWA if assets are more than $1 billion but less than $10 billion • Depository institutions: Up to 5% of RWA if consolidated assets of all depository institution subsidiaries are $1 billion or less Up to 3% of RWA if consolidated assets of all depository institution subsidiaries are more than $1 billion but less than $10 billion • Treasury may require matching private capital and limit SBLF funding to 3% of RWA even if assets are $1 billion or less. Qualified Small Business Lending for purposes of the Small Business Lending Fund is defined as follows: Qualified Small Business Lending Qualified Small Business Lending includes all: 1. Commercial and industrial loans 2.

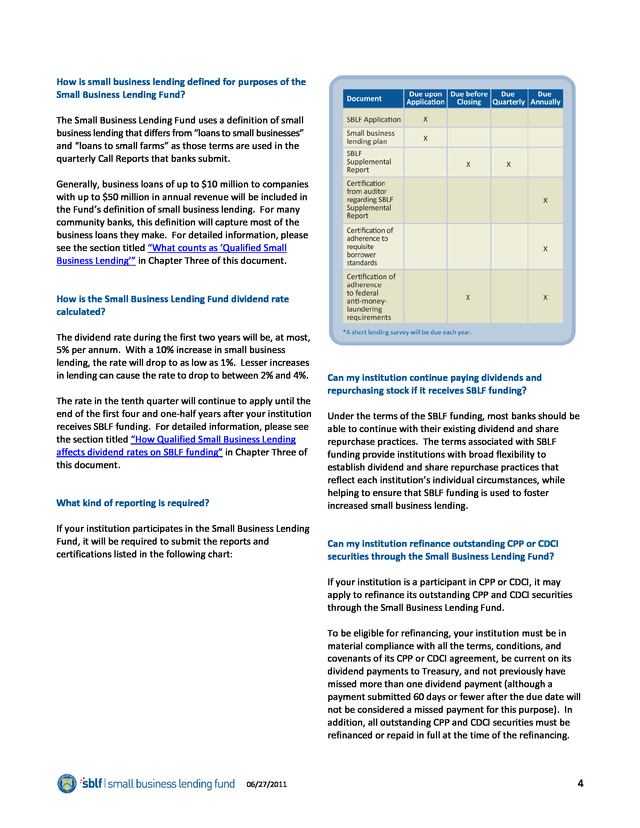

Loans secured by owner-occupied nonfarm, nonresidential real estate 3. Loans to finance agricultural production and other loans to farmers 4. Loans secured by farmland so long as: • the original principal and commitment amount is $10 million or less • the loan is not to a business with more than $50 million in revenues and excluding loan portions guaranteed by the U.S. Government or for which a third party assumes risk. An institution that receives capital from the Small Business Lending Fund will supplement its Call Report with a Supplemental Report that identifies Qualified Small Business Lending. Dividend rates upon funding and for the following nine calendar quarters, adjusted quarterly (based on outstanding loans at the end of the second previous quarter): Dividend Rates Dividend rate for the tenth quarter after funding through the end of the first four and one-half years: Lending Increase Less than 2.5% 2.5% or more, but less than 5% 5% or more, but less than 7.5% 7.5% or more, but less than 10% 10% or more If lending has increased at the end of the eighth quarter after funding If lending has not increased at the end of the eighth quarter after funding Dividend rate after four and one-half years (if funding has not already been repaid): • Entry and Exit • Dividend Rate 5% 4% 3% 2% 1% Rate set as above for the tenth quarter 7% 9% The application deadline for C Corporation banks is May 16, 2011.

Treasury encourages eligible institutions to submit their application as soon as possible to allow sufficient time for processing. Provide a small business lending plan, approximately two pages in length, to the institution’s regulator (not directly to Treasury). Repay SBLF funding at any time with regulatory approval. More Info For general inquiries and questions, please call the Small Business Lending Fund information line at 888-832-1147. For communications pertaining to a specific institution, please email SBLFInstitutions@treasury.gov, a Treasury email address. 06/27/2011 1 . CHAPTER ONE: INTRODUCTION This chapter provides an overview of the Small Business Lending Fund, which is administered by the U.S. Department of the Treasury. The chapter is designed to provide answers to general questions your institution might have about the Small Business Lending Fund, including: • What is the Small Business Lending Fund? • Which institutions does this guidebook address? • How can the Small Business Lending Fund help my institution? • Is my institution eligible to apply to participate in the Small Business Lending Fund? The more a bank increases its small business lending, the lower the rate it will pay for the SBLF funding. Through the Small Business Lending Fund, community banks and small businesses can work together to create jobs and promote local economic growth in neighborhoods across the nation. Many loans made by community banks will qualify as small business lending under the Jobs Act. The law defines small business lending to include loans of up to $10 million to businesses with up to $50 million in annual revenue. Those loans include: • Commercial and industrial loans • Loans secured by owner-occupied nonfarm, nonresidential real estate • Loans to finance agricultural production and other loans to farmers • Loans secured by farmland • How much funding can my institution receive? • If my institution’s Small Business Lending Fund application is approved, is it obligated to participate? • After receiving capital, can my institution exit the Small Business Lending Fund at any time? • How is small business lending defined for purposes of the Small Business Lending Fund? • How is the Small Business Lending Fund dividend rate calculated? • What kind of reporting is required? • Can my institution continue paying dividends and repurchasing stock if it receives SBLF funding? • Can my institution refinance outstanding CPP or CDCI securities through the Small Business Lending Fund? • Is the Small Business Lending Fund related to the Troubled Asset Relief Program (TARP)? What is the Small Business Lending Fund? Enacted into law as part of the Small Business Jobs Act of 2010 (the Jobs Act), the Small Business Lending Fund encourages lending to small businesses by providing capital to community banks with under $10 billion in assets. Which institutions does this guidebook address? This material applies to community banks and community development loan funds that have total assets of less than $10 billion. For purposes of this guidebook, the terms “community bank” and “bank” encompass banks, thrifts, and bank and thrift holding companies with consolidated assets of less than $10 billion. This guidebook does not apply to mutual institutions, Subchapter S Corporations, or community development loan funds. How can the Small Business Lending Fund help my institution? The Small Business Lending Fund aims to stimulate small business lending by reducing the dividend rate paid by a community bank on SBLF funding as the bank increases its lending. The cost of capital provided through the Small Business Lending Fund will start no higher than 5%.

If your community bank’s small business lending increases by 10% or more, then the rate will fall to as low as 1%. For increases in small business lending that are less than 10%, the rate can fall to between 2% and 4%. Treasury will make SBLF funding available by purchasing senior preferred stock or equivalents in institutions that 06/27/2011 2 . apply and are approved for participation in the Fund. SBLF funding will be Tier-1 capital. Participation in the Small Business Lending Fund is entirely voluntary. Banks may repay their SBLF funding at any time with regulatory approval. Access to capital through the Small Business Lending Fund can boost your institution’s lending capacity while helping to create jobs and promote economic growth in local communities across the nation. The Small Business Lending Fund: • supports Main Street banks and small businesses Treasury will publish separate terms for mutual institutions, Subchapter S corporations, and community development loan funds (CDLFs). Terms for such institutions may vary from those described in this guidebook. An institution is not eligible if it is on the FDIC’s problem bank list (or similar list) or has been removed from that list in the previous 90 days. The Small Business Lending Fund also provides an option for community banks to refinance preferred stock issued to Treasury through the Capital Purchase Program (CPP) or the Community Development Capital Initiative (CDCI) under certain conditions.

However, simultaneous participation in CPP or CDCI and the Small Business Lending Fund is not permitted. • is available only to community banks and community development loan funds How much funding can my institution receive? • enables eligible community banks to access Tier 1 capital at rates as low as 1% • carries no compensation restrictions and does not require the issuance of any warrants • is focused on generating increases in lending to small businesses If your institution has total assets of $1 billion or less, it may apply for SBLF funding that equals up to 5% of its riskweighted assets (as reported in the Call Report immediately preceding the date of application). If your institution has assets of more than $1 billion, but less than $10 billion, it may apply for funding that equals up to 3% of its riskweighted assets. Is my institution eligible to apply to participate in the Small Business Lending Fund? If my institution’s Small Business Lending Fund application is approved, is it obligated to participate? Your institution is eligible if it has total assets of less than $10 billion (as of the end of the fourth quarter of calendar year 2009) and it meets the other requirements for participation. If your institution is controlled by a holding company, the combined assets of the holding company determine eligibility and your holding company must apply. For detailed information on eligibility, please see the section titled “What counts as ‘Qualified Small Business Lending’” in Chapter Three. No.

Submitting an application to the Small Business Lending Fund does not create any obligation on the part of your institution or Treasury. In the case of an insured depository institution that is controlled by a bank holding company, the bank holding company must apply and at least 90% of the funds must be immediately downstreamed. After receiving capital, can my institution exit the Small Business Lending Fund at any time? Bank holding companies that are organized as limited liability companies may participate in the Small Business Lending Fund. The terms published on the SBLF website, www.treasury.gov/SBLF, will generally apply. 06/27/2011 Once approved, your institution will have a reasonable amount of time to decide whether it would like to participate in the Small Business Lending Fund and enter into a definitive agreement with Treasury. Yes. Subject to the approval of your regulator, your institution can exit the Small Business Lending Fund at any time simply by repaying the funding provided along with any accrued dividends.

There is no prepayment penalty. If your institution wishes to repay its SBLF funding in partial payments, each partial payment must be at least 25% of the original funding amount. 3 . How is small business lending defined for purposes of the Small Business Lending Fund? The Small Business Lending Fund uses a definition of small business lending that differs from “loans to small businesses” and “loans to small farms” as those terms are used in the quarterly Call Reports that banks submit. Generally, business loans of up to $10 million to companies with up to $50 million in annual revenue will be included in the Fund’s definition of small business lending. For many community banks, this definition will capture most of the business loans they make. For detailed information, please see the section titled “What counts as ‘Qualified Small Business Lending’” in Chapter Three of this document. How is the Small Business Lending Fund dividend rate calculated? The dividend rate during the first two years will be, at most, 5% per annum. With a 10% increase in small business lending, the rate will drop to as low as 1%.

Lesser increases in lending can cause the rate to drop to between 2% and 4%. The rate in the tenth quarter will continue to apply until the end of the first four and one-half years after your institution receives SBLF funding. For detailed information, please see the section titled “How Qualified Small Business Lending affects dividend rates on SBLF funding” in Chapter Three of this document. Can my institution continue paying dividends and repurchasing stock if it receives SBLF funding? What kind of reporting is required? Under the terms of the SBLF funding, most banks should be able to continue with their existing dividend and share repurchase practices. The terms associated with SBLF funding provide institutions with broad flexibility to establish dividend and share repurchase practices that reflect each institution’s individual circumstances, while helping to ensure that SBLF funding is used to foster increased small business lending. If your institution participates in the Small Business Lending Fund, it will be required to submit the reports and certifications listed in the following chart: Can my institution refinance outstanding CPP or CDCI securities through the Small Business Lending Fund? If your institution is a participant in CPP or CDCI, it may apply to refinance its outstanding CPP and CDCI securities through the Small Business Lending Fund. To be eligible for refinancing, your institution must be in material compliance with all the terms, conditions, and covenants of its CPP or CDCI agreement, be current on its dividend payments to Treasury, and not previously have missed more than one dividend payment (although a payment submitted 60 days or fewer after the due date will not be considered a missed payment for this purpose).

In addition, all outstanding CPP and CDCI securities must be refinanced or repaid in full at the time of the refinancing. 06/27/2011 4 . Please consult the Summary of Terms for Current CPP and CDCI Participants for further detail. If your institution applies for refinancing, its application will be evaluated by Treasury under the same process used for other applicants. (Read more about refinancing requirements and how applications are evaluated in Chapter Two). Warrants issued in connection with CPP investments will remain outstanding. Is the Small Business Lending Fund related to the Troubled Asset Relief Program (TARP)? No. The Small Business Lending Fund is not related to TARP.

Congress authorized the Small Business Lending Fund as part of the Small Business Jobs Act of 2010, with the objective of increasing the availability of credit to small businesses. The Small Business Lending Fund draws from a source of funding separate from TARP, and it is administered by a separate organization in Treasury. Participation in the Small Business Lending Fund carries no executive compensation restrictions and does not require the issuance of any warrants. Any institution will not be considered a TARP recipient by virtue of participating in the Small Business Lending Fund. 06/27/2011 5 . CHAPTER TWO: HOW TO APPLY TO THE SMALL BUSINESS LENDING FUND submit a completed application to Treasury at SBLFApps@treasury.gov. Submitting an application to the Small Business Lending Fund is easy. In the following section you will find what you need to know about how to apply, including: The application deadline for C Corporation banks is May 16, 2011. Treasury encourages eligible institutions to submit their application as soon as possible to allow sufficient time for processing. How does the application process work? What should be in the small business lending plan? May my institution change the amount of capital requested after it has applied for funding? May my bank withdraw its application and resubmit a new application if a more favorable Call Report is available? How will Treasury evaluate applications? How much time will my institution have after receiving preliminary approval from Treasury to decide whether to participate? What is the closing process? What are the requirements for raising separate matching funds? What are the requirements for refinancing outstanding CPP or CDCI securities? Are there any application fees or other fees associated with the Small Business Lending Fund? When will my institution learn whether it has been approved for SBLF funding? May my bank apply more than once for SBLF funding or schedule more than one closing? For your convenience, the application form is available on the Small Business Lending Fund website at www.treasury.gov/SBLF. If you have any questions, please contact the SBLF information line at 888-832-1147 (Monday-Friday, 9:00 AM-7:00 PM ET). How does the application process work? If your institution is eligible and wants to apply to participate in the Small Business Lending Fund, it must 06/27/2011 In general, applicants may reduce the amount of capital requested at any time prior to closing, but may not increase the amount of capital requested once an application has been submitted.

Applicants approved for funding with matching capital may only reduce the amount of capital requested if they raise an equivalent amount of incremental private investment (i.e., In addition to the amount of private investment initially specified in Treasury’s approval notice). Submitting an application does not obligate your institution to participate in the Small Business Lending Fund if approved. Your institution may withdraw its application at any time prior to entering into to a definitive agreement with Treasury. Additionally, after your institution has received SBLF funding, it may exit the Small Business Lending Fund at any time simply by repaying the funding provided along with any accrued dividends (with the approval of its regulator). Please note that if your institution wants to apply to participate in the Small Business Lending Fund, in addition to submitting an application to Treasury, it must submit a small business lending plan of approximately two pages in length to its primary federal regulator and to its state regulator, if applicable.

If your institution is a holding company, it must also submit the lending plan to the primary federal regulator (and state regulator, if applicable) of each of its insured depository institution subsidiaries. The lending plan should not be sent directly to Treasury. (Your institution’s federal regulator will forward it to Treasury.) What should be in the small business lending plan? Each lending plan should: 1. Address the needs of small businesses The lending plan should describe how your institution intends to use funding from the Small Business Lending Fund to address the needs of small businesses in the communities it serves. Your institution should provide 6 .

a description of the basis for its lending goals and how it intends to achieve these goals. The lending plan should explain why the projected increase in small business lending is reasonable in the context of the size of your institution and the market it serves. To the extent practicable, the lending plan should include a description of the types of loans anticipated and customers served. 2. Specify the projected increase in small business lending The lending plan should include the increase in qualified small business lending (as defined in the Fund’s summary of terms) that your institution expects to achieve two years after the investment. It is acceptable to provide a projected range. While this projection should be based upon your institution’s estimate of qualified small business lending, your institution does not need to formally calculate such lending at the time of application.

Each bank will be required to calculate such lending only as part of the closing process, after receiving preliminary approval for participation in the Fund. Prior to closing, your institution will be asked to revalidate the projection provided in this lending plan on the basis of its formal calculation of qualified small business lending. The lending plan is not intended to be an official business plan in the sense of those submitted to your institution’s primary federal regulator. As a result, Treasury does not require the submission of a pro forma income statement or balance sheet. 3.

Provide for community outreach The Small Business Jobs Act of 2010 requires banks participating in the Small Business Lending Fund to provide outreach and advertising describing the availability and application process for receiving small business loans. Your institution should submit its lending plan to its regulator(s) at the same time it submits its Small Business Lending Fund application to Treasury. Guidance, including instructions for submitting the lending plan to the appropriate regulators, and a form for an applicant’s lending plan submission can be found at http://www.treasury.gov/SBLF. Again, please note that the lending plan should not be sent directly to Treasury. 06/27/2011 May my institution change the amount of capital requested after it has applied for funding? In general, applicants may reduce the amount of capital requested at any time prior to the closing, but may not increase the amount of capital requested once an application has been submitted. May my bank withdraw its application and resubmit a new application if a more favorable Call Report is available? Institutions may only resubmit an application to correct errors on the original application, at the discretion of Treasury. Treasury will consult with appropriate federal and state regulators before approving an application. How will Treasury evaluate applications? Treasury will coordinate with the federal bank regulatory agencies and (as applicable) state regulatory agencies to review your institution’s application.

Specifically, Treasury will consult with the federal banking agencies in determining whether your institution is qualified to receive capital from the Small Business Lending Fund. If your institution is a state-chartered bank, Treasury also will consider the views of your state banking regulator regarding the financial condition of your bank. 7 . Treasury will notify your institution of its decision as one of the following three options: 1. Preliminary approval After reviewing the application, Treasury may determine that your institution is eligible for and qualified to participate in the Small Business Lending Fund. If your institution elects to continue with the process, Treasury will assign a law firm as its representative to work with your institution to complete the closing and funding processes. 2. Preliminary approval contingent on matched funding As a result of its review of the application, Treasury may determine that your institution is eligible and should be considered for participation in the Small Business Lending Fund, provided it raises separate matching funds from private, nongovernmental sources.

Such matched funding will need to be received either prior to or concurrent with Treasury’s SBLF funding. (Generally, capital raised after September 27, 2010 may be included). If your institution would like to continue with the process, Treasury will assign a law firm as its representative to work with your institution to complete the closing and funding processes. 3.

Considered withdrawn Following its review of the application, Treasury may determine that your institution is not eligible or otherwise will not qualify for participation in the Small Business Lending Fund. In such a case, your institution’s application will be considered withdrawn. How much time will my institution have after receiving preliminary approval from Treasury to decide whether to participate in the Small Business Lending Fund? What is the closing process? The closing process for institutions that decide to proceed after receiving either a “preliminary approval” or a “preliminary approval contingent on matched funding” determination includes working with a law firm representing Treasury to enter into a Securities Purchase Agreement with Treasury. As explained in Chapter Three, an institution that participates in the Small Business Lending Fund is required to submit an Initial Supplemental Report and regular Quarterly Supplemental Reports, which will be used for measuring changes in Qualified Small Business Lending. The Initial Supplemental Report is due no later than five (5) business days before closing. If the closing date occurs after the Call Report is due in a calendar quarter, the first regular Quarterly Supplemental Report is also due no later than five (5) business days before closing. What are the requirements for raising separate matching funds? Treasury will only require an institution to raise matching private investment as a condition for approval if the institution would not otherwise qualify to receive SBLF funding absent such capital. If an institution is required to raise matching funds as a condition for receiving SBLF funding, the following will apply: 1.

Treasury will notify the institution of the amount of private funds it must raise to qualify for SBLF funding at the time of preliminary approval; 2. The maximum amount of SBLF funding provided by Treasury will be equal to 3% of the institution’s riskweighted assets; An institution will have 30 days after the date of Treasury’s notice of preliminary approval to decide whether it would like to participate in the Small Business Lending Fund and schedule a closing with Treasury. 3. The source of the private investment must not be an institution that has received or applied to receive capital from the Small Business Lending Fund; and For institutions that receive preliminary approval contingent on raising matching capital, Treasury will normally grant extensions if matching capital cannot be raised within the thirty (30) day period. 4.

The private investment must be subordinate to the SBLF capital and carry terms satisfactory to Treasury (although Treasury may approve a dividend rate for the private investment that is higher than the SBLF rate). An institution may notify Treasury at any time prior to closing that it has decided not to participate in the Small Business Lending Fund and withdraw its application. 06/27/2011 In determining eligibility for matched funding, Treasury will consider as matching funds any capital raised after 8 . September 27, 2010, net of subsequent dividends, repurchases, and redemptions. through the Small Business Lending Fund, unless you repurchase them. Applicants approved for funding with matching capital may only reduce the amount of capital requested if they raise an equivalent amount of incremental private investment (i.e., in addition to the amount of private investment initially specified in Treasury’s approval notice). Institutions applying to refinance CPP or CDCI securities will not be considered for approval on a “matched funding” basis (although they are not prohibited from raising capital if they choose). What are the requirements for refinancing outstanding CPP or CDCI securities? To be considered for refinancing, your institution must meet all of the eligibility requirements that otherwise apply to Small Business Lending Fund participants, plus the following additional requirements: • The institution must be in material compliance with all the terms, conditions, and covenants of any CPP or CDCI agreement and financial instrument; • The institution must not have missed more than one dividend payment under CPP or CDCI (where a missed payment is defined as a payment submitted more than 60 days after the due date); and • The institution must pay, in immediately available funds, the amount of any unpaid dividends for the payment period prior to the SBLF closing date, plus accrued and unpaid dividends as of the date of refinancing for the payment period that includes the closing date. The maximum amount of available SBLF funding for CPP or CDCI refinancing is the same as it is for regular SBLF participants. It is based on the size of your institution. If your institution has up to $1 billion in assets, the maximum will be 5% of its riskweighted assets. If your institution has more than $1 billion and less than $10 billion in assets, the maximum will be 3%. If your institution has CPP or CDCI stock with an aggregate liquidation preference greater than the maximum amount of permissible SBLF funding, your bank must redeem the additional CPP or CDCI stock in immediately available funds on or before the date it receives SBLF funding. All outstanding CPP and CDCI securities must be refinanced or repaid in full at the time of the refinancing. In addition, the SBLF funding must be at least 1% of your institution’s risk-weighted assets. Any warrants that your institution has issued to Treasury under CPP will remain outstanding after CPP refinancing 06/27/2011 Institutions that are refinancing CPP investments must increase their small business lending to receive an economic benefit from refinancing.

If at the beginning of the tenth full calendar quarter after the date on which a bank receives SBLF funding, the bank’s Qualified Small Business Lending as reported in the ninth quarter has not increased relative to its baseline amount, then the bank will be required to pay, at the beginning of the fifth anniversary of the CPP investment, a repayment incentive fee equal to 2% per year on the total amount of outstanding SBLF funding. (If your bank received CPP funding on two separate funding dates, the 2% annual lending incentive fee will apply as of the fifth anniversary of the date of the initial CPP funding, and will be calculated based on the current outstanding amount of SBLF funding as of that date.) This fee will extend through the date four and one-half years following the institution’s receipt of SBLF funding. Are there any application fees or other fees associated with the Small Business Lending Fund? Treasury does not charge any application fees or other fees or closing costs associated with closing a transaction with the Small Business Lending Fund. In addition, there are no fees or penalties for repayment or prepayment of SBLF funding. For current CPP banks that refinance into the SBLF program, there is a 2% annual Lending Incentive Fee that will apply if the institution does not increase its small business lending. This fee will extend through the date four and one-half years following the institution’s receipt of SBLF funding. This is discussed in further detail in the Summary of Terms for Current CPP and CDCI Participants. When will my institution learn whether it has been approved for SBLF Funding? Treasury is committed to the prompt and efficient review of all applications to the Fund with the goal of providing funding decisions to institutions as quickly as possible. Working with the appropriate federal and state banking regulators, Treasury conducts a thorough analysis of each 9 .

application. Each application is evaluated independently. Because institutions vary in their circumstances and complexity, Treasury cannot provide an indication of whether or when any specific application may be approved. Treasury will fund institutions on a rolling basis. May my bank apply more than once for SBLF funding or schedule more than one closing? Institutions may only submit a single application for the program. Each approved institution will receive all of its SBLF funding in a single closing and funding. Institutions whose applications have been withdrawn may not reapply. 06/27/2011 10 .

CHAPTER THREE: HOW THE SMALL BUSINESS LENDING FUND WORKS following four categories, among others, which form the 1 basis of what counts as Qualified Small Business Lending: The basic premise of the Small Business Lending Fund is simple: The dividend rate paid by a community bank on SBLF capital is reduced as the bank increases its lending to small businesses to get the U.S economy growing. To help community banks understand how the Small Business Lending Fund works, this chapter explains key definitions and calculations. Specifically, it provides the following information: • Where to find information about Small Business Lending Fund investment terms; • What counts as “Qualified Small Business Lending”; • How Qualified Small Business Lending affects dividend rates on SBLF funding; and • How to calculate changes in Qualified Small Business Lending and resulting dividend rate. Where to find information about Small Business Lending Fund investment terms The complete Small Business Lending Fund summary of terms can be found on the Small Business Lending Fund website at www.treasury.gov/SBLF. Treasury is currently developing terms and guidance for mutual institutions, Subchapter S corporations, and community development loan funds. Terms for such institutions may vary from those described in this guide. In determining whether a loan’s original principal and commitment amount is $10 million or less, a group of loans to the same borrower or any of its affiliates will be treated as a single loan.

The total amount of the loans in the group may not exceed $10 million for the loans to qualify. What counts as “Qualified Small Business Lending?” In determining whether a loan goes to a business with more than $50 million in revenues, the recipient’s revenues are measured for the most recent fiscal year that had ended when the loan originated (using the recipient’s ultimate parent company, where applicable). Your institution can lower the cost of capital it obtains through the Small Business Lending Fund by increasing the amount of its “Qualified Small Business Lending.” Accordingly, it is important to understand what counts as Qualified Small Business Lending. For purposes of the Small Business Lending Fund, small business lending includes more loans than the Call Report categories of “loans to small businesses” and “loans to small farms.” In Call Reports, institutions report overall amounts of business loans in the If any part of a loan is guaranteed by a U.S. government agency or enterprise, the guaranteed portion is subtracted from the loan amounts.

If a third party has assumed an economic interest in any part of a loan, that portion is subtracted. 1 06/27/2011 These categories of loans are reported in the Consolidated Reports of Condition and Income submitted by banks. For eligible institutions that are savings and loan associations, the Thrift Financial Report (which uses different labels for categories of loans reported) should be used in cases where this document references a Call Report. 11 . If your institution is a holding company, its Qualified Small Business Lending consists of the combined Qualified Small Business Lending of all of its insured depository institution subsidiaries. How Qualified Small Business Lending affects dividend rates on SBLF funding If your institution’s application to the Small Business Lending Fund is approved and it elects to participate, Treasury will provide funds to your institution, receiving shares of preferred stock (or equivalents) in return. Your institution will pay dividends on the funding at rates that will go down if the amount of its Qualified Small Business Lending goes up. Summary of Loan Categories Included in Qualified Small Business Lending Loans that meet the applicable conditions, including the $10 million loan amount limit and the $50 million revenue limit, qualify as small business lending if they are within any of the four categories of loans previously described. Although your institution’s Call Report instructions provide full descriptions, the categories may be briefly summarized as follows: Commercial and industrial loans Commercial and industrial loans, as reported on Call Reports, include loans for commercial and industrial purposes to sole proprietorships, partnerships, corporations, and other business enterprises. Potential recipients include manufacturing companies, construction companies, transportation and communication companies, wholesale and retail trade enterprises, service enterprises, and various other types of businesses.

The category also includes loans to individuals for commercial, industrial, and professional purposes, but not for investment or personal expenditure purposes. The loans may be secured or unsecured, but the category excludes loans secured by real estate. Loans secured by owner-occupied nonfarm, nonresidential real estate The dividend rate during the first two years will be, at most, 5% per annum. With a 10% increase in small business lending, the rate will drop to only 1%.

Lesser increases in lending can cause the rate to drop to between 2% and 4%. The rate in the tenth quarter after the closing date will continue to apply until the end of the four-and-one-halfyear period after your institution receives SBLF funding. In most cases, this rate will not exceed 5%. If your institution’s small business lending does not increase at all by the tenth quarter, however, the rate will rise to 7%. Four and one-half years following Treasury’s initial funding, if the capital has not been repaid, the rate will increase to 9%.

Your institution may repay the capital at any time with the approval of its regulator. The amount of your institution’s increase in small business lending is measured by the stock of loans outstanding each quarter versus the amount that was outstanding in the four quarters ending June 30, 2010. The dividend rate your institution pays is determined by its aggregate increase in small business lending. The Small Business Lending Fund does not distinguish between refinanced loans and new loans – or require any “loan-byloan” review. 06/27/2011 Loans secured by real estate, as reported on Call Reports, include a subcategory for loans secured by owner-occupied nonfarm, nonresidential properties. A loan secured by real estate is one for which a lien on the real estate was central to the extension of the credit.

The subcategory of loans secured by owner-occupied nonfarm, nonresidential properties consists of nonfarm, nonresidential real estate loans for which the primary source of repayment is the cash flow from the ongoing operations of the owner of the property (or its affiliate). Loans to finance agricultural production and other loans to farmers Loans to finance agricultural production and other loans to farmers, as reported on Call Reports, include a variety of agricultural loans. Potential recipients include farm and ranch owners, operators (including tenants), and non-farmers. The category includes loans that finance crops and livestock, fisheries and forestries, and equipment used in agricultural activities.

The loans may be secured or unsecured, but the category excludes loans secured by real estate. Loans secured by farmland Loans secured by real estate, as reported on Call Reports, include a subcategory for loans secured by farmland. As noted above, a loan secured by real estate is one for which a lien on the real estate was central to the extension of the credit. The subcategory of loans secured by farmland includes land used for crops or livestock, including grazing or pasture land, and loans secured by improvements on the land. 12 .

To measure this increase, your bank will establish its “baseline” level of small business lending at the time it receives SBLF funding (equal to the average amount outstanding in the four quarters ending June 30, 2010). In each quarter after your bank receives SBLF funding, its amount of small business loans outstanding (with certain adjustments) will be compared to this baseline number. That comparison, in turn, determines the dividend rate your institution will pay on its SBLF funding. Your bank will calculate these measures – both the baseline and its quarterly lending – using Supplemental Reports that are submitted to Treasury. There are two types of Supplemental Reports: • The Initial Supplemental Report, due no later than five (5) business days before closing, which calculates your institution’s baseline, as well as its initial dividend rate. • The Quarterly Supplemental Report, due in the calendar quarter in which closing occurs and in each of the next nine quarters, which calculates your institution’s dividend rate for the quarter following submission of the report (and, in the case of the tenth Quarterly Supplemental Report, the rate that continues until four and one-half years after closing). 1. Baseline The baseline for measuring changes in an institution’s Qualified Small Business Lending will be the quarterly average of Qualified Small Business Lending for the four quarters ending June 30, 2010. The initial baseline will be established at the time your institution receives SBLF funding.

This initial baseline amount will be adjusted to take into account any gains in Qualified Small Business Lending during the baseline quarters resulting from mergers, acquisitions, and loan purchases. 2. Dividend rate through the first nine quarters During the quarter in which it receives SBLF funding, your institution’s initial dividend rate will be 5% or less. Whether it is less will depend on whether your institution has achieved a sufficient increase (from its baseline) in Qualified Small Business Lending as reflected in the Initial Supplemental Report which, in turn, is derived from the Call Report that is published in the calendar quarter before your institution receives funding. Because Call Reports pertain to the quarter before the one in which they are published, the SBLF Supplemental Report derived from the Call Report published in the quarter preceding the receipt of SBLF capital will reflect the amount of loans outstanding at the end of the second preceding quarter. For example, if the closing date occurs in the second quarter of 2011, the initial dividend rate will depend on the amount of Qualified Small Business Lending reflected in the SBLF Supplemental Report that was derived from the Call Report published in the first quarter of 2011, which will be the amount of qualified loans that were outstanding at the end of the fourth quarter of 2010. For the first nine calendar quarters after the closing date, the dividend rate for each quarter will be similarly determined.

The amount of Qualified Small Business Lending derived from the Call Report published in the preceding quarter will be compared to the baseline. This amount will reflect qualified loans that were outstanding at the end of the second preceding quarter. In the example above, the dividend rate for the third quarter of 2011 will depend on the amount of Qualified Small Business Lending reflected in the Supplemental Report derived from the Call Report published in the second quarter of 2011. This amount will reflect qualified loans at the end of the first quarter of 2011. 3. Dividend rate after the first nine quarters The baseline will remain constant each quarter after receiving SBLF funding.

However, if your institution’s Qualified Small Business Lending subsequently increases in a given quarter as a result of mergers, acquisitions, or loan purchases, its baseline will be increased in that quarter (and in subsequent quarters) to reflect that increase. These adjustments will be made cumulatively from the quarter ending September 30, 2010. This is to help ensure that rate reductions for SBLF funding correspond to additional lending to small businesses, rather than acquisitions of existing loans. 06/27/2011 The dividend rate that applies in the tenth calendar quarter after the closing date will remain in effect until four and one-half years after the closing date. If the amount of Qualified Small Business Lending as of the end of the eighth quarter after the closing date, as reflected in the Quarterly Supplemental Report submitted in the ninth quarter, reflects no increase at all over the baseline (that is, if such lending is the same as or less than the baseline), then the dividend rate will become 7% in the tenth quarter, continuing until the 13 .

end of the four-and-one-half-year period after the closing date. Following the four-and-one-half-year period, the rate will increase to 9% if the funding has not already been repaid. For example, if the closing date occurs on May 1, 2011, the dividend rate that applies in the fourth quarter of 2013 – which is the tenth quarter after the investment date – will remain in effect until November 1, 2015, which is four and one-half years after the closing date. If the institution’s Qualified Small Business Lending in the second quarter of 2013 is the same as or less than the baseline, however, the dividend rate will be 7% in the fourth quarter of 2013. In either case, on November 1, 2015, the dividend rate will increase to 9% if the institution has not redeemed its SBLF funding by then. The following table of adjustments shows the dividend rates that apply with specified increases from the baseline. If your institution uses SBLF funding to refinance a CPP investment, an added fee will apply if the bank’s small business lending has not increased relative to its baseline amount in the eighth quarter after SBLF funding is received, as reflected in the Supplemental Report submitted in the ninth quarter after the SBLF funding is received. In such a case, your bank will be required to pay a quarterly lending incentive fee equal to 2% per annum on the total amount of outstanding SBLF funding, starting at the beginning of the first quarter after the fifth anniversary of the CPP investment and ending four and one-half years following the date your institution refinances into SBLF. 4. Dividend rates and lending amounts If the amount of Qualified Small Business Lending by your institution has increased from the baseline by a sufficient percentage to result in a lower dividend rate, the lower rate will apply to a dollar amount of SBLF capital only up to the amount by which Qualified Small Business Lending has increased. For example, assume that the amount of SBLF funding received is $5 million, qualified lending has increased by $4 million in the two years after receiving the capital, and this amount represents a 10% increase over the baseline, resulting in a 1% dividend rate. On these assumptions, the 1% rate applies to $4 million of the SBLF funding and a 5% rate applies to the remaining $1 million.

If Qualified Small Business Lending had increased by at least $5 million, which is the amount of the SBLF funding received, the 1% rate would have applied to the entire amount. How to calculate changes in Qualified Small Business Lending and resulting dividend rate Your bank will calculate changes in Qualified Small Business Lending – both baseline and quarterly lending – using Supplemental Reports that are submitted to Treasury. The Supplemental Reports are based in part on information your institution already provides in its quarterly Call Report. This calculation is important, because your institution’s increase in Qualified Small Business Lending can lower the dividend rate your institution pays. 06/27/2011 14 . greater than $50 million), and the portion of any loans guaranteed by the U.S. government or for which the risk is assumed by a third party, are subtracted. The resulting amount is the Adjusted Small Business Lending Baseline. The reports then determine the quarter-end Qualified Small Business Lending by taking the balances reported on your institution’s Call Report and adding back your institution’s cumulative net charge-offs with respect to such loans since July 1, 2010. This is done so as not to penalize banks for appropriately charging off loans.

The resulting sum constitutes your Quarter-End Adjusted Qualified Small Business Lending. The reports provide the calculation your institution will use to determine the dividend rate it will pay for its SBLF funding by comparing its Adjusted Quarter-End Qualified Small Business Lending to its Adjusetd Small Business Lending Baseline. There are two types of Supplemental Reports, Initial and Quarterly. These reports start with information already presented in your institution’s Call Report or Thrift Financial Reports (TFRs) or, for thrift holding companies, in your subsidiaries’ TFRs. These reports take the outstanding amount of lending reflected in the following four categories: Because your institution’s baseline is based on the four quarters ending June 30, 2010, your bank may already qualify for a lower dividend rate based on the growth of qualified lending between July 1, 2010, and the second calendar quarter preceding the SBLF closing date.

See the following chart for such an example, where the SBLF funding is received in the second quarter of 2011: • Commercial and industrial loans; • Owner-occupied nonfarm, nonresidential real estate loans; • Loans to finance agricultural production and other loans to farmers; and • Loans secured by farmland. The baseline is the average amount of Qualified Small Business Lending your institution had outstanding for the four quarters ending June 30, 2010 for each of these four types of loans, as reflected on your institution’s Call Reports (or TFRs). However, this baseline will be adjusted from the onset and each subsequent quarter by adding any increases in Qualified Small Business Lending obtained through mergers and acquisitions or loan purchases. The purpose of adjusting the baseline in this way is so that no institution is unduly rewarded for simply purchasing or acquiring qualified loans. From these amounts, large loans (defined as any loan or group of loans greater than $10 million), loans to large businesses (defined as businesses with annual revenues 06/27/2011 If your initial Qualified Small Business Lending exceeds the baseline, as adjusted, by a sufficient percentage, your institution will qualify for a lower dividend rate. The Initial Supplemental Report, due no later than five business days before the closing date, will be used to calculate the dividend rate that will apply initially after closing. The Quarterly Supplemental Reports will be used to determine the new dividend rate for the following quarter. The Quarterly Supplemental Report will be due each quarter when the Call Report is due, no more than 15 .

30 calendar days after the quarter to which it pertains. If the closing date occurs after the Call Report for the quarter is due, the institution will be required to submit its first Quarterly Supplemental Report no later than five days before the closing date. Although Quarterly Supplemental Reports will be submitted at the same time Call Reports are submitted, the process for filing Supplemental Reports differs from the Call Report processes. Supplemental Reports are not filed with Call Reports. Rather, your institution will be required to submit its completed Supplemental Reports by email to Treasury. The applicable email addresses are provided in the instructions for the Supplemental Reports. As with the Call Report, different types of institutions use slightly different forms.

There are four different versions of each Supplemental Report, each of which tries to leverage the content and format of whichever form of Call Report or TFR an institution uses. If your institution is a state- or nationally-chartered bank, you should use the Supplemental Report for Banks. If your institution is a savings association, you should use the Supplemental Report for Savings Associations.

And if your institution is a holding company, you should use the Supplemental Report for Bank Holding Companies or the Supplemental Report for Savings and Loan Holding Companies, as applicable. Treasury will post these forms at http://www.treasury.gov/resourcecenter/sb-programs/Pages/Supplemental-ReportingRequirements.aspx as they become available. 06/27/2011 16 . CHAPTER FOUR: AFTER YOUR BANK RECEIVES FUNDING The Small Business Lending Fund is intended to provide institutions with incentives to responsibly increase their small business lending. While the Small Business Lending Fund was designed to minimize the costs associated with participation, institutions must comply with certain requirements. The requirements are: • Continuation of dividend payments and share repurchases • Downstreaming of SBLF funding • Reporting and certification requirements • Repayment of SBLF funding • How small businesses can know which banks are participating in the Small Business Lending Fund Continuation of dividend payments and share repurchases Subject to any existing regulatory reviews and limitations, accepting SBLF funding should not affect your institution’s ability to pay dividends to other shareholders or to repurchase shares. There are, however, certain limited restrictions, which are tailored to be consistent with normal dividend and share repurchase plans – permitting even dividend/earnings ratios in excess of 100%. In general, your bank can make a dividend payment or share repurchase provided that, after the payment or repurchase, the institution’s Tier 1 capital would be at least 90% of the amount existing at the time immediately after the closing date, excluding any subsequent net charge-offs and partial repayments of the SBLF funding. After two years, and until the tenth anniversary of the investment date, the 90% limitation decreases by a dollar amount equal to 10% of the SBLF funding for every 1% increase in Qualified Small Business Lending your bank has achieved over its baseline level.

These restrictions will no longer apply after an institution has repaid its SBLF funding in full. Failure to pay dividends on your SBLF funding carries consequences. On such an occasion, the senior management of your institution must provide Treasury with written notice as to why your bank’s board of directors did 06/27/2011 not declare dividends. And, your institution may not repurchase shares or pay dividends on shares that are pari passu or junior to the SBLF shares during the quarter of nonpayment and for the following three quarters. If your institution does not pay SBLF dividends for four quarters, and during such time it was not subject to a regulatory determination that prohibits the declaration and payment of dividends, then your institution’s board of directors must certify to Treasury, in writing, that your institution used its best efforts to declare and pay such quarterly dividends in a manner consistent with safe and sound banking practices and the directors’ fiduciary obligation. If your institution fails to pay its SBLF dividends for five quarters, Treasury will have the right, but not the obligation, to appoint an observer to its board of directors. This right expires when full dividends have been paid for four consecutive dividend periods. After six missed payments, if the amount of your institution’s SBLF funding totals $25 million or more, Treasury will have the right, but not the obligation, to elect two directors to its board.

The right to elect directors expires once full dividends have been paid for four consecutive quarters. For privately held banks, paying dividends on shares ranking pari passu or junior to SBLF shares also is prohibited from the tenth anniversary of the investment date onward. Treasury expects any outstanding SBLF funding to be repaid before that time. Downstreaming of SBLF funding The dividend rate on SBLF funding is determined based on the quantity of Qualified Small Business Lending reported by insured depository institutions. When SBLF funding is provided to a holding company, the holding company must contribute at least 90% of the amount to its insured depository institution subsidiaries that originate small business loans. Funding must be downstreamed to insured depository institution subsidiaries immediately following receipt of the SBLF funding. If the holding company owns more than one insured depository institution, no insured depository institution may receive more than 5% of its risk-weighted assets, if the holding company has total assets of $1 billion or less, or 3% of its risk-weighted assets, if the holding company has total assets of more than $1 billion and less than $10 billion. 17 .

For institutions that refinance capital investments from CPP or CDCI through SBLF, the requirement to downstream not less than 90% of Treasury’s investment will only apply to incremental capital received from SBLF, not capital that is refinanced from CPP or CDCI. Reporting and certification requirements As explained in Chapter Three, if your institution participates in the Small Business Lending Fund, it will need to submit an Initial Supplemental Report and Quarterly Supplemental Reports, which will determine the dividend rates for the SBLF funding. In addition, your institution will be required to complete a short annual lending survey and provide certain annual certifications to Treasury, as required by the Small Business Jobs Act of 2010. Each Supplemental Report must be certified as accurate by your Chief Executive Officer (CEO) and Chief Financial 2 Officer (CFO) . The same members of your board of directors that sign your institution’s Call Report must also sign the Supplemental Report. The process is very similar to the Call Report certification process, except that, in this case, the CEO must also certify the report. Repayment of SBLF funding As outlined in Chapter One, with the approval of its regulator, your institution can repay its SBLF funding at any time.

All redemptions will be at 100% of liquidation value, plus accrued and unpaid dividends for the current dividend period, regardless of whether dividends have been declared. Your bank can also repay in part, provided the part is equal to at least 25% of the original SBLF funding. How small businesses can know which banks are participating in the Small Business Lending Fund Information about the Small Business Lending Fund is available on this website, www.treasury.gov/SBLF. At least once per month, Treasury will publish the list of banks participating in the Small Business Lending Fund on this website, www.treasury.gov/SBLF. 2 If the institution is a savings association, the CFO’s signature is replaced with an authorized officer of the savings association who signs the Thrift Financial Report. 06/27/2011 18 .

FOR MORE INFORMATION To learn more about the Small Business Lending Fund, visit www.treasury.gov/SBLF. For general inquiries and questions, please call the Small Business Lending Fund information line at 888-832-1147 (Monday-Friday, 9:00 AM-7:00 PM ET). For communications pertaining to a specific institution, please email SBLFInstitutions@treasury.gov, a Treasury email address. For media inquiries, please call the U.S. Department of the Treasury Press Office at 202-622-2960. The U.S. Department of the Treasury provides this Getting Started Guide for the Small Business Lending Fund (SBLF), the SBLF information line, and other SBLF resources for informational purposes. Although efforts have been made to ensure the accuracy of the information provided, the information is subject to change or correction.

Any SBLF funding provided to an institution will be subject to the terms and conditions of the definitive agreements entered into by Treasury and the respective institution. 06/27/2011 19 .

Enacted into law as part of the Small Business Jobs Act of 2010 This guidebook is divided into four chapters. Chapter One provides a general overview of Small Business Lending Fund benefits, eligibility, and terms. Chapter Two provides information relating to the application process.

Chapter Three provides more detailed information about how the Small Business Lending Fund works – specifically, what qualifies as small business lending, how dividends are calculated, and how to address applicable reporting requirements. Chapter Four describes what happens after an institution receives SBLF funding. If you have questions at any point, please contact the information line for the Small Business Lending Fund at 888-832-1147 (Monday-Friday, 9:00 AM-7:00 PM ET). to increase small business lending, the Small Business Lending Fund is designed to provide up to $30 billion in capital to qualified community banks and other eligible financial institutions. The Small Business Lending Fund will help TABLE OF CONTENTS AT A GLANCE: The Small Business Lending Fund for Community Banks 1 CHAPTER ONE: Introduction 2 CHAPTER TWO: How to Apply to the Small Business Lending Fund 6 create jobs and promote economic growth in local communities across the nation while enabling Main Street banks to better extend credit to their customers by utilizing 06/27/2011 CHAPTER THREE: How the Small Business Lending Fund Works 11 CHAPTER FOUR: After Your Bank Receives Funding the incentives that the Fund provides. 17 . AT A GLANCE: THE SMALL BUSINESS LENDING FUND FOR COMMUNITY BANKS Overview Through the Small Business Lending Fund, the U.S. Department of the Treasury provides Tier-1 capital to community banks and other eligible institutions. Each institution pays dividends at rates that go down as its small business lending goes up. • Eligibility Insured depository institutions with assets of less than $10 billion, not controlled by a holding company or an entity with assets of $10 billion or more (as of the end of the fourth quarter of calendar year 2009) • Bank and savings and loan holding companies with consolidated assets of less than $10 billion • Treasury will publish separate terms for mutual institutions, Subchapter S corporations, and community development loan funds; this guidebook does not apply to those institutions Institutions currently or recently on the FDIC problem bank list (or similar list) are ineligible. Senior perpetual noncumulative preferred stock (or equivalents) qualifying as Tier 1 capital Amount of Funding Holding companies: • • Up to 5% of risk-weighted assets (RWA) if assets are $1 billion or less Up to 3% of RWA if assets are more than $1 billion but less than $10 billion • Depository institutions: Up to 5% of RWA if consolidated assets of all depository institution subsidiaries are $1 billion or less Up to 3% of RWA if consolidated assets of all depository institution subsidiaries are more than $1 billion but less than $10 billion • Treasury may require matching private capital and limit SBLF funding to 3% of RWA even if assets are $1 billion or less. Qualified Small Business Lending for purposes of the Small Business Lending Fund is defined as follows: Qualified Small Business Lending Qualified Small Business Lending includes all: 1. Commercial and industrial loans 2.

Loans secured by owner-occupied nonfarm, nonresidential real estate 3. Loans to finance agricultural production and other loans to farmers 4. Loans secured by farmland so long as: • the original principal and commitment amount is $10 million or less • the loan is not to a business with more than $50 million in revenues and excluding loan portions guaranteed by the U.S. Government or for which a third party assumes risk. An institution that receives capital from the Small Business Lending Fund will supplement its Call Report with a Supplemental Report that identifies Qualified Small Business Lending. Dividend rates upon funding and for the following nine calendar quarters, adjusted quarterly (based on outstanding loans at the end of the second previous quarter): Dividend Rates Dividend rate for the tenth quarter after funding through the end of the first four and one-half years: Lending Increase Less than 2.5% 2.5% or more, but less than 5% 5% or more, but less than 7.5% 7.5% or more, but less than 10% 10% or more If lending has increased at the end of the eighth quarter after funding If lending has not increased at the end of the eighth quarter after funding Dividend rate after four and one-half years (if funding has not already been repaid): • Entry and Exit • Dividend Rate 5% 4% 3% 2% 1% Rate set as above for the tenth quarter 7% 9% The application deadline for C Corporation banks is May 16, 2011.

Treasury encourages eligible institutions to submit their application as soon as possible to allow sufficient time for processing. Provide a small business lending plan, approximately two pages in length, to the institution’s regulator (not directly to Treasury). Repay SBLF funding at any time with regulatory approval. More Info For general inquiries and questions, please call the Small Business Lending Fund information line at 888-832-1147. For communications pertaining to a specific institution, please email SBLFInstitutions@treasury.gov, a Treasury email address. 06/27/2011 1 . CHAPTER ONE: INTRODUCTION This chapter provides an overview of the Small Business Lending Fund, which is administered by the U.S. Department of the Treasury. The chapter is designed to provide answers to general questions your institution might have about the Small Business Lending Fund, including: • What is the Small Business Lending Fund? • Which institutions does this guidebook address? • How can the Small Business Lending Fund help my institution? • Is my institution eligible to apply to participate in the Small Business Lending Fund? The more a bank increases its small business lending, the lower the rate it will pay for the SBLF funding. Through the Small Business Lending Fund, community banks and small businesses can work together to create jobs and promote local economic growth in neighborhoods across the nation. Many loans made by community banks will qualify as small business lending under the Jobs Act. The law defines small business lending to include loans of up to $10 million to businesses with up to $50 million in annual revenue. Those loans include: • Commercial and industrial loans • Loans secured by owner-occupied nonfarm, nonresidential real estate • Loans to finance agricultural production and other loans to farmers • Loans secured by farmland • How much funding can my institution receive? • If my institution’s Small Business Lending Fund application is approved, is it obligated to participate? • After receiving capital, can my institution exit the Small Business Lending Fund at any time? • How is small business lending defined for purposes of the Small Business Lending Fund? • How is the Small Business Lending Fund dividend rate calculated? • What kind of reporting is required? • Can my institution continue paying dividends and repurchasing stock if it receives SBLF funding? • Can my institution refinance outstanding CPP or CDCI securities through the Small Business Lending Fund? • Is the Small Business Lending Fund related to the Troubled Asset Relief Program (TARP)? What is the Small Business Lending Fund? Enacted into law as part of the Small Business Jobs Act of 2010 (the Jobs Act), the Small Business Lending Fund encourages lending to small businesses by providing capital to community banks with under $10 billion in assets. Which institutions does this guidebook address? This material applies to community banks and community development loan funds that have total assets of less than $10 billion. For purposes of this guidebook, the terms “community bank” and “bank” encompass banks, thrifts, and bank and thrift holding companies with consolidated assets of less than $10 billion. This guidebook does not apply to mutual institutions, Subchapter S Corporations, or community development loan funds. How can the Small Business Lending Fund help my institution? The Small Business Lending Fund aims to stimulate small business lending by reducing the dividend rate paid by a community bank on SBLF funding as the bank increases its lending. The cost of capital provided through the Small Business Lending Fund will start no higher than 5%.

If your community bank’s small business lending increases by 10% or more, then the rate will fall to as low as 1%. For increases in small business lending that are less than 10%, the rate can fall to between 2% and 4%. Treasury will make SBLF funding available by purchasing senior preferred stock or equivalents in institutions that 06/27/2011 2 . apply and are approved for participation in the Fund. SBLF funding will be Tier-1 capital. Participation in the Small Business Lending Fund is entirely voluntary. Banks may repay their SBLF funding at any time with regulatory approval. Access to capital through the Small Business Lending Fund can boost your institution’s lending capacity while helping to create jobs and promote economic growth in local communities across the nation. The Small Business Lending Fund: • supports Main Street banks and small businesses Treasury will publish separate terms for mutual institutions, Subchapter S corporations, and community development loan funds (CDLFs). Terms for such institutions may vary from those described in this guidebook. An institution is not eligible if it is on the FDIC’s problem bank list (or similar list) or has been removed from that list in the previous 90 days. The Small Business Lending Fund also provides an option for community banks to refinance preferred stock issued to Treasury through the Capital Purchase Program (CPP) or the Community Development Capital Initiative (CDCI) under certain conditions.

However, simultaneous participation in CPP or CDCI and the Small Business Lending Fund is not permitted. • is available only to community banks and community development loan funds How much funding can my institution receive? • enables eligible community banks to access Tier 1 capital at rates as low as 1% • carries no compensation restrictions and does not require the issuance of any warrants • is focused on generating increases in lending to small businesses If your institution has total assets of $1 billion or less, it may apply for SBLF funding that equals up to 5% of its riskweighted assets (as reported in the Call Report immediately preceding the date of application). If your institution has assets of more than $1 billion, but less than $10 billion, it may apply for funding that equals up to 3% of its riskweighted assets. Is my institution eligible to apply to participate in the Small Business Lending Fund? If my institution’s Small Business Lending Fund application is approved, is it obligated to participate? Your institution is eligible if it has total assets of less than $10 billion (as of the end of the fourth quarter of calendar year 2009) and it meets the other requirements for participation. If your institution is controlled by a holding company, the combined assets of the holding company determine eligibility and your holding company must apply. For detailed information on eligibility, please see the section titled “What counts as ‘Qualified Small Business Lending’” in Chapter Three. No.

Submitting an application to the Small Business Lending Fund does not create any obligation on the part of your institution or Treasury. In the case of an insured depository institution that is controlled by a bank holding company, the bank holding company must apply and at least 90% of the funds must be immediately downstreamed. After receiving capital, can my institution exit the Small Business Lending Fund at any time? Bank holding companies that are organized as limited liability companies may participate in the Small Business Lending Fund. The terms published on the SBLF website, www.treasury.gov/SBLF, will generally apply. 06/27/2011 Once approved, your institution will have a reasonable amount of time to decide whether it would like to participate in the Small Business Lending Fund and enter into a definitive agreement with Treasury. Yes. Subject to the approval of your regulator, your institution can exit the Small Business Lending Fund at any time simply by repaying the funding provided along with any accrued dividends.

There is no prepayment penalty. If your institution wishes to repay its SBLF funding in partial payments, each partial payment must be at least 25% of the original funding amount. 3 . How is small business lending defined for purposes of the Small Business Lending Fund? The Small Business Lending Fund uses a definition of small business lending that differs from “loans to small businesses” and “loans to small farms” as those terms are used in the quarterly Call Reports that banks submit. Generally, business loans of up to $10 million to companies with up to $50 million in annual revenue will be included in the Fund’s definition of small business lending. For many community banks, this definition will capture most of the business loans they make. For detailed information, please see the section titled “What counts as ‘Qualified Small Business Lending’” in Chapter Three of this document. How is the Small Business Lending Fund dividend rate calculated? The dividend rate during the first two years will be, at most, 5% per annum. With a 10% increase in small business lending, the rate will drop to as low as 1%.

Lesser increases in lending can cause the rate to drop to between 2% and 4%. The rate in the tenth quarter will continue to apply until the end of the first four and one-half years after your institution receives SBLF funding. For detailed information, please see the section titled “How Qualified Small Business Lending affects dividend rates on SBLF funding” in Chapter Three of this document. Can my institution continue paying dividends and repurchasing stock if it receives SBLF funding? What kind of reporting is required? Under the terms of the SBLF funding, most banks should be able to continue with their existing dividend and share repurchase practices. The terms associated with SBLF funding provide institutions with broad flexibility to establish dividend and share repurchase practices that reflect each institution’s individual circumstances, while helping to ensure that SBLF funding is used to foster increased small business lending. If your institution participates in the Small Business Lending Fund, it will be required to submit the reports and certifications listed in the following chart: Can my institution refinance outstanding CPP or CDCI securities through the Small Business Lending Fund? If your institution is a participant in CPP or CDCI, it may apply to refinance its outstanding CPP and CDCI securities through the Small Business Lending Fund. To be eligible for refinancing, your institution must be in material compliance with all the terms, conditions, and covenants of its CPP or CDCI agreement, be current on its dividend payments to Treasury, and not previously have missed more than one dividend payment (although a payment submitted 60 days or fewer after the due date will not be considered a missed payment for this purpose).

In addition, all outstanding CPP and CDCI securities must be refinanced or repaid in full at the time of the refinancing. 06/27/2011 4 . Please consult the Summary of Terms for Current CPP and CDCI Participants for further detail. If your institution applies for refinancing, its application will be evaluated by Treasury under the same process used for other applicants. (Read more about refinancing requirements and how applications are evaluated in Chapter Two). Warrants issued in connection with CPP investments will remain outstanding. Is the Small Business Lending Fund related to the Troubled Asset Relief Program (TARP)? No. The Small Business Lending Fund is not related to TARP.