'Zero infrastructure -- anything-as-a-service': How CSPs can harness the full power of the cloud (Jan 2016)

PwC

Description

Communications Review / January 2016

Insights for telecom, cable, satellite, and Internet executives

‘Zero infrastructure –

anything-as-a-service’:

How CSPs can harness the

full power of the cloud

As cloud computing moves into the business mainstream and sees rising adoption

across all industries, leading global communication service providers (CSPs)—

including wireline, wireless, cable, and other/integrated communications carriers—

are increasingly seeking to harness the power of the cloud in their operating models.

Cloud’s combination of cost benefits, scalability, manageability and agility can create

an advantage for CSPs who are facing the challenges of an increasingly competitive

communications ecosystem. As a result, cloud is rapidly becoming the new core

delivery model for provisioning business technology across a CSP’s operations, with

the aspiration to achieve an IT footprint based on ‘zero infrastructure – anything-asa-service’. To help CSPs turn this aspiration into reality, we’ve developed a framework

for a cloud-centric operating model that fulfills their industry-specific IT and business

imperatives. In this article we examine the key components of the framework, and

describe how to make it a reality in a CSP.

www.pwc.com/communicationsreview

.

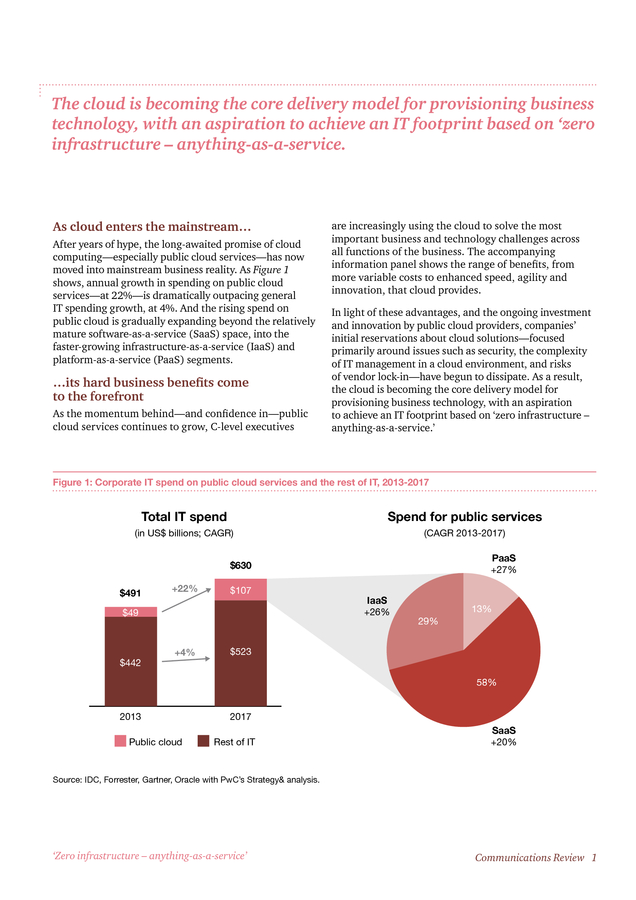

The cloud is becoming the core delivery model for provisioning business technology, with an aspiration to achieve an IT footprint based on ‘zero infrastructure – anything-as-a-service. As cloud enters the mainstream… After years of hype, the long-awaited promise of cloud computing—especially public cloud services—has now moved into mainstream business reality. As Figure 1 shows, annual growth in spending on public cloud services—at 22%—is dramatically outpacing general IT spending growth, at 4%. And the rising spend on public cloud is gradually expanding beyond the relatively mature software-as-a-service (SaaS) space, into the faster-growing infrastructure-as-a-service (IaaS) and platform-as-a-service (PaaS) segments. …its hard business benefits come to the forefront As the momentum behind—and confidence in—public cloud services continues to grow, C-level executives are increasingly using the cloud to solve the most important business and technology challenges across all functions of the business. The accompanying information panel shows the range of benefits, from more variable costs to enhanced speed, agility and innovation, that cloud provides. In light of these advantages, and the ongoing investment and innovation by public cloud providers, companies’ initial reservations about cloud solutions—focused primarily around issues such as security, the complexity of IT management in a cloud environment, and risks of vendor lock-in—have begun to dissipate.

As a result, the cloud is becoming the core delivery model for provisioning business technology, with an aspiration to achieve an IT footprint based on ‘zero infrastructure – anything-as-a-service.’ Figure 1: Corporate IT spend on public cloud services and the rest of IT, 2013-2017 Total IT spend (in US$ billions; CAGR) Spend for public services (CAGR 2013-2017) PaaS +27% $630 $491 +22% $107 $49 $442 +4% IaaS +26% 29% 13% $523 58% 2013 Public cloud 2017 Rest of IT SaaS +20% Source: IDC, Forrester, Gartner, Oracle with PwC’s Strategy& analysis. ‘Zero infrastructure – anything-as-a-service’ Communications Review 1 . As telecoms markets become saturated and price competition heats up, they need to drive costs—including technology costs—out of the business much more aggressively than before. Some benefits of cloud computing • • • • • Costs: An ability to move from fixed to variable costs, and create a more competitive IT environment based on pay-per-use provisioning Scalability/elasticity of supply: Resources can be scaled based on user demand, and resource utilisation becomes more transparent Manageability: Greater self-service and automation, with SaaS/PaaS replacing complex legacy solutions Agility: Faster time-to-market for new offerings, and an enhanced ability to pilot solutions and ‘fail fast’ Mobility: Greater alignment with new customer behaviour, and enhanced ability to support mobile workforces For CSPs, today’s business imperatives… …are raising significant IT challenges As CSPs plan out their strategies for this new world, they’re focusing on fulfilling several business imperatives. Amongst these, one of the highest-priority items on their agenda is re-imagining customer experience to be much more digital-centred. This includes advances such as enhanced mobile self-service apps and improved digital commerce capabilities. Further imperatives include reshaping the retail experience to meet the distinct expectations of millennial customers, and showcasing the product portfolio in a way where digital assists and enriches the end-to-end shopping and purchasing experience. As they strive to achieve all these goals, CSPs are coming up against several IT challenges. One of the biggest is talent: they need to supplement traditional business support systems/operation support systems-type (BSS/ OSS) IT engineering skills with new talent that can deliver against the digital agenda, and is well-versed in front-end user experience/user interface design, modular service integration, and content management and delivery. At the same time, CSPs are also prioritising the building and delivery of a new range of products—including IPTV, mobile video and other digital content services—together with the advertising and (e)commerce engines needed to drive sales of, or otherwise monetise, these products. Further key components of their product sets include internet-of-things (IoT) solutions ranging from consumer wearables to solutions for the connected car and smart home.

And as telecoms markets become saturated and price competition heats up, they need to drive costs— including technology costs—out of the business much more aggressively than before. ‘Zero infrastructure – anything-as-a-service’ A further challenge is the need to build new capabilities that combine the traditional carrier-grade ‘waterfall’ engineering and release management required for the BSS/OSS legacy, with the more iterative, agile, rapid prototyping methods needed for the digital user experience and expanded product suite. CSPs must also open up their IT architecture to enable interoperability with an increasingly broad ecosystem of partners, in areas including content provisioning, IoT, data analytics, advertising, and more. And they have to bring down IT costs by relying more heavily on outsourcing, and using more scalable and efficient cloud services—which increasingly means public cloud. Communications Review 2 .

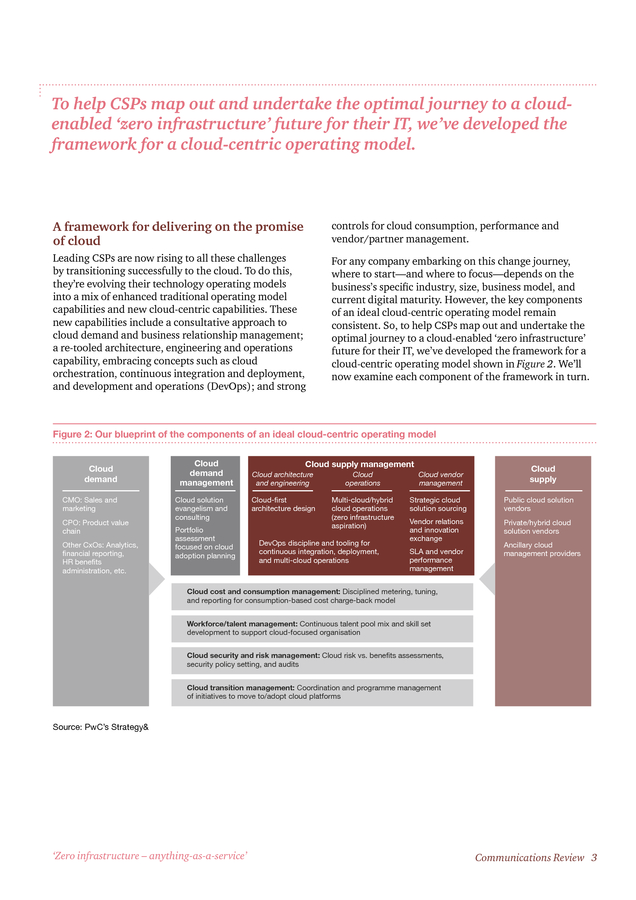

To help CSPs map out and undertake the optimal journey to a cloudenabled ‘zero infrastructure’ future for their IT, we’ve developed the framework for a cloud-centric operating model. A framework for delivering on the promise of cloud controls for cloud consumption, performance and vendor/partner management. Leading CSPs are now rising to all these challenges by transitioning successfully to the cloud. To do this, they’re evolving their technology operating models into a mix of enhanced traditional operating model capabilities and new cloud-centric capabilities. These new capabilities include a consultative approach to cloud demand and business relationship management; a re-tooled architecture, engineering and operations capability, embracing concepts such as cloud orchestration, continuous integration and deployment, and development and operations (DevOps); and strong For any company embarking on this change journey, where to start—and where to focus—depends on the business’s specific industry, size, business model, and current digital maturity. However, the key components of an ideal cloud-centric operating model remain consistent.

So, to help CSPs map out and undertake the optimal journey to a cloud-enabled ‘zero infrastructure’ future for their IT, we’ve developed the framework for a cloud-centric operating model shown in Figure 2. We’ll now examine each component of the framework in turn. Figure 2: Our blueprint of the components of an ideal cloud-centric operating model Cloud demand CMO: Sales and marketing CPO: Product value chain Other CxOs: Analytics, financial reporting, HR benefits administration, etc. Cloud demand management Cloud solution evangelism and consulting Portfolio assessment focused on cloud adoption planning Cloud supply management Cloud architecture and engineering Cloud operations Cloud-first architecture design Multi-cloud/hybrid cloud operations (zero infrastructure aspiration) DevOps discipline and tooling for continuous integration, deployment, and multi-cloud operations Cloud vendor management Cloud supply Strategic cloud solution sourcing Public cloud solution vendors Vendor relations and innovation exchange Private/hybrid cloud solution vendors SLA and vendor performance management Ancillary cloud management providers Cloud cost and consumption management: Disciplined metering, tuning, and reporting for consumption-based cost charge-back model Workforce/talent management: Continuous talent pool mix and skill set development to support cloud-focused organisation Cloud security and risk management: Cloud risk vs. benefits assessments, security policy setting, and audits Cloud transition management: Coordination and programme management of initiatives to move to/adopt cloud platforms Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 3 .

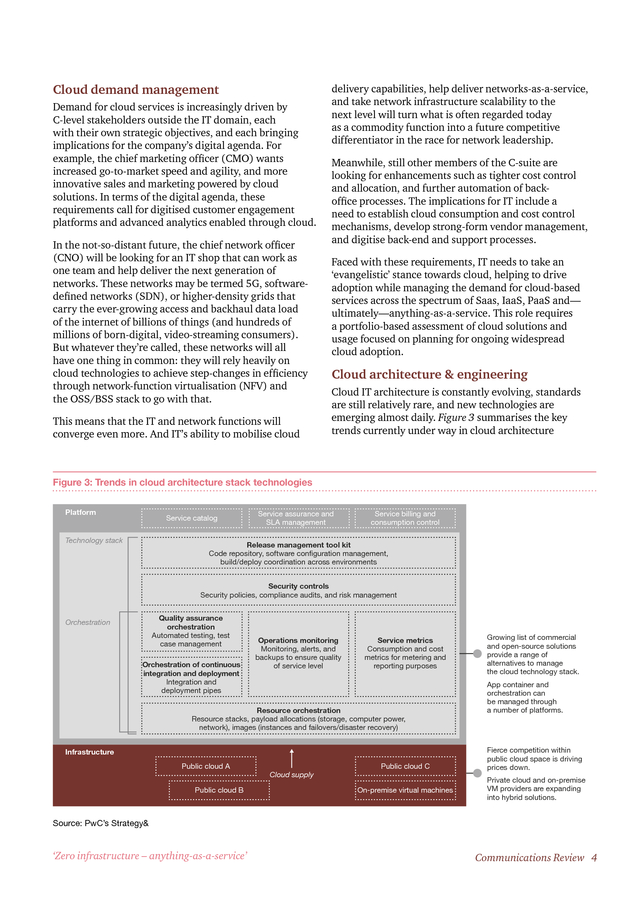

Cloud demand management Demand for cloud services is increasingly driven by C-level stakeholders outside the IT domain, each with their own strategic objectives, and each bringing implications for the company’s digital agenda. For example, the chief marketing officer (CMO) wants increased go-to-market speed and agility, and more innovative sales and marketing powered by cloud solutions. In terms of the digital agenda, these requirements call for digitised customer engagement platforms and advanced analytics enabled through cloud. In the not-so-distant future, the chief network officer (CNO) will be looking for an IT shop that can work as one team and help deliver the next generation of networks. These networks may be termed 5G, softwaredefined networks (SDN), or higher-density grids that carry the ever-growing access and backhaul data load of the internet of billions of things (and hundreds of millions of born-digital, video-streaming consumers). But whatever they’re called, these networks will all have one thing in common: they will rely heavily on cloud technologies to achieve step-changes in efficiency through network-function virtualisation (NFV) and the OSS/BSS stack to go with that. This means that the IT and network functions will converge even more.

And IT’s ability to mobilise cloud delivery capabilities, help deliver networks-as-a-service, and take network infrastructure scalability to the next level will turn what is often regarded today as a commodity function into a future competitive differentiator in the race for network leadership. Meanwhile, still other members of the C-suite are looking for enhancements such as tighter cost control and allocation, and further automation of backoffice processes. The implications for IT include a need to establish cloud consumption and cost control mechanisms, develop strong-form vendor management, and digitise back-end and support processes. Faced with these requirements, IT needs to take an ‘evangelistic’ stance towards cloud, helping to drive adoption while managing the demand for cloud-based services across the spectrum of Saas, IaaS, PaaS and— ultimately—anything-as-a-service. This role requires a portfolio-based assessment of cloud solutions and usage focused on planning for ongoing widespread cloud adoption. Cloud architecture & engineering Cloud IT architecture is constantly evolving, standards are still relatively rare, and new technologies are emerging almost daily.

Figure 3 summarises the key trends currently under way in cloud architecture Figure 3: Trends in cloud architecture stack technologies Platform Service catalog Technology stack Service assurance and SLA management Service billing and consumption control Release management tool kit Code repository, software configuration management, build/deploy coordination across environments Security controls Security policies, compliance audits, and risk management Quality assurance orchestration Automated testing, test case management Orchestration Orchestration of continuous integration and deployment Integration and deployment pipes Operations monitoring Monitoring, alerts, and backups to ensure quality of service level Service metrics Consumption and cost metrics for metering and reporting purposes Resource orchestration Resource stacks, payload allocations (storage, computer power, network), images (instances and failovers/disaster recovery) Infrastructure Public cloud A Public cloud B Cloud supply Public cloud C On-premise virtual machines Growing list of commercial and open-source solutions provide a range of alternatives to manage the cloud technology stack. App container and orchestration can be managed through a number of platforms. Fierce competition within public cloud space is driving prices down. Private cloud and on-premise VM providers are expanding into hybrid solutions. Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 4 . stack technologies. Even a cursory review of this chart underlines that many CSPs currently have only a few of the components and capabilities shown in the chart. This means they need to move fast, most importantly, by building a cloud orchestration stack with a strong focus on public cloud. CI/CD best practice and the corresponding tools in areas including code repository management, automation build, self-testing and automated deployment. The second aspect of effective cloud operations is multicloud service management, both to ensure a consistent, high-quality user/customer experience across distributed clouds, and to coordinate multiple third-parties that contribute to delivering a given service. This requires the design of end-to-end measures at platform and aggregated service level, and the adaptation of proven IT service management disciplines to a multi-cloud setting—including activities around monitoring, events and alerts; incident and problem flows; and monitoring and managing performance against service-level agreements (SLAs). In building their cloud architecture, CSPs must balance their business requirements with the rapidly-changing technology landscape, and select the architecture components that are right for their own business. A key factor in achieving the right balance is adopting the idea of ‘cloud first’—designing for the cloud as the primary platform, rather than designing first for on-premise and then adapting for the cloud.

Cloud-first means architecting for speed, flexibility and modularity, and enables the business to avoid getting stuck in the tangle of complexities that still afflicts many CSPs. Cloud operations A cloud-centric delivery model requires a new, more fluid, DevOps-style approach to service deployment and operations. This has two aspects. The first is continuous integration and deployment (CI/CD), reflecting the need to roll out simultaneous—and more frequent—software releases, and to coordinate multiple cloud platforms with the ability to scale rapidly according to changing build/ test/run needs.

In response, organisations need to adopt With these two aspects addressed, the new cloud-based delivery capabilities will then provide the foundation and means to ‘clean house’ and migrate a significant share of on-premise IT to the cloud. Whilst this may not initially enable a CSP to deliver fully against its ‘zero infrastructure’ aspiration, it does open up significant and ongoing potential to reduce infrastructure. The four-step pathway towards a zero infrastructure footprint is shown in Figure 4, with every step being applied across the complete apps, computing, and storage stack. Figure 4: The four-step pathway towards a zero infrastructure footprint Decommission: ‘Stop’ Reduce infrastructure estate by identifying and eliminating underutilized assets Move to the cloud: ‘Ship’ Migrate eligible on-premise hosted applications and services to cloud-based solutions Virtualise: ‘Shrink’ Consolidate: ‘Merge’ Shrink remaining physical asset estate through virtualisation of servers and storage Reduce remaining physical infrastructure footprint through consolidation of assets within and across data centres Performance and utilisation should be consistent boundary conditions across the steps Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 5 .

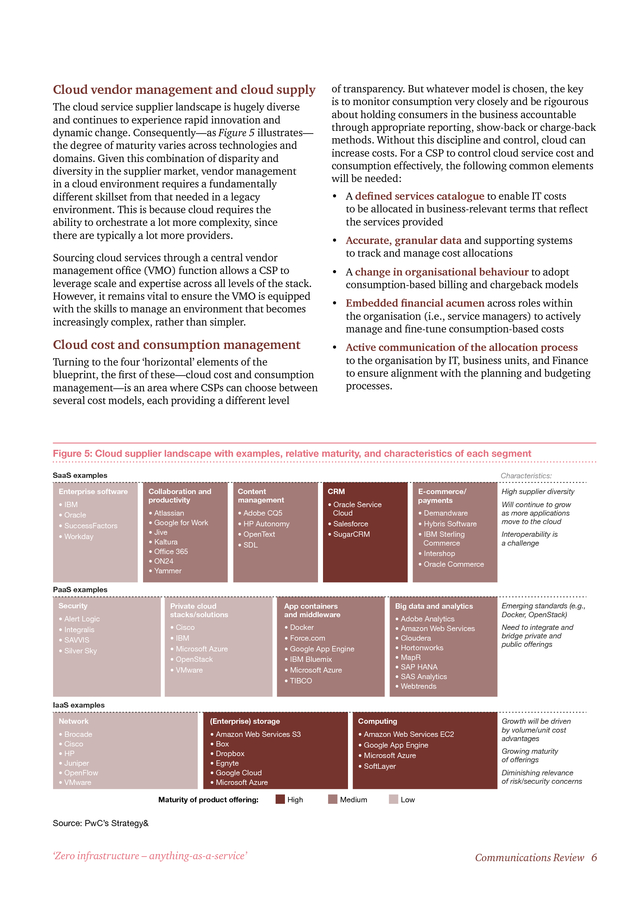

Cloud vendor management and cloud supply The cloud service supplier landscape is hugely diverse and continues to experience rapid innovation and dynamic change. Consequently—as Figure 5 illustrates— the degree of maturity varies across technologies and domains. Given this combination of disparity and diversity in the supplier market, vendor management in a cloud environment requires a fundamentally different skillset from that needed in a legacy environment. This is because cloud requires the ability to orchestrate a lot more complexity, since there are typically a lot more providers. Sourcing cloud services through a central vendor management office (VMO) function allows a CSP to leverage scale and expertise across all levels of the stack. However, it remains vital to ensure the VMO is equipped with the skills to manage an environment that becomes increasingly complex, rather than simpler. Cloud cost and consumption management Turning to the four ‘horizontal’ elements of the blueprint, the first of these—cloud cost and consumption management—is an area where CSPs can choose between several cost models, each providing a different level of transparency.

But whatever model is chosen, the key is to monitor consumption very closely and be rigourous about holding consumers in the business accountable through appropriate reporting, show-back or charge-back methods. Without this discipline and control, cloud can increase costs. For a CSP to control cloud service cost and consumption effectively, the following common elements will be needed: • A defined services catalogue to enable IT costs to be allocated in business-relevant terms that reflect the services provided • Accurate, granular data and supporting systems to track and manage cost allocations • A change in organisational behaviour to adopt consumption-based billing and chargeback models • Embedded financial acumen across roles within the organisation (i.e., service managers) to actively manage and fine-tune consumption-based costs • Active communication of the allocation process to the organisation by IT, business units, and Finance to ensure alignment with the planning and budgeting processes. Figure 5: Cloud supplier landscape with examples, relative maturity, and characteristics of each segment SaaS examples Enterprise software � IBM � Oracle � SuccessFactors � Workday Characteristics: Collaboration and productivity Content management � Atlassian � Google for Work � Jive � Kaltura � Office 365 � ON24 � Yammer � Adobe CQ5 � HP Autonomy � OpenText � SDL CRM E-commerce/ payments � Oracle Service Cloud � Salesforce � SugarCRM High supplier diversity � Demandware � Hybris Software � IBM Sterling Commerce � Intershop � Oracle Commerce Will continue to grow as more applications move to the cloud Interoperability is a challenge PaaS examples Security � Alert Logic � Integralis � SAVVIS � Silver Sky Private cloud stacks/solutions App containers and middleware � Cisco � IBM � Microsoft Azure � OpenStack � VMware � Docker � Force.com � Google App Engine � IBM Bluemix � Microsoft Azure � TIBCO Big data and analytics � Adobe Analytics � Amazon Web Services � Cloudera � Hortonworks � MapR � SAP HANA � SAS Analytics � Webtrends Emerging standards (e.g., Docker, OpenStack) Need to integrate and bridge private and public offerings IaaS examples Network Infrastructure � Brocade � Cisco � HP � Juniper � OpenFlow � VMware (Enterprise) storage Computing � Amazon Web Services S3 � Box � Dropbox � Egnyte � Google Cloud � Microsoft Azure � Amazon Web Services EC2 � Google App Engine � Microsoft Azure � SoftLayer Maturity of product offering: High Medium Growth will be driven by volume/unit cost advantages Growing maturity of offerings Diminishing relevance of risk/security concerns Low Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 6 .

Workforce/talent management In terms of talent, moving to a cloud-first organisational model requires a CSP to shift the balance away from the IT knowledge and skills in today’s workforce—such as traditional development methodologies based on a strong engineering and technical focus—and towards the more service-oriented skills needed in a cloud environment. These new skills are likely to include fitfor-purpose development methodologies such as agile and DevOps; skills in configuring and integrating SaaS apps and platforms; deep finance and business acumen; information and service management skills; and capabilities in outcomes-based vendor management. A particular focus should be on finding and developing ‘digital keystone’ skills such as project and programme management, quality assurance, prototyping, security, business requirements management, and user experience design. Cloud security and risk management As a CSP moves to cloud-centricity, it must adapt and evolve its security and risk management, while taking account of the fact that the benefits of cloud adoption continue to outweigh the security risks. Whilst concerns over cloud security and exposure to third-parties have historically acted as inhibitors to cloud adoption, acceptance of cloud’s benefits over the related risks is growing rapidly—along with a realisation that security levels can actually be improved through cloud solutions. Key actions include establishing a cloud security capability to manage the risks of cloud adoption, developing a response plan in the event of a breach, and avoiding collecting and processing un-curated data in the cloud. Cloud transition management For CSPs worldwide, cloud presents exciting opportunities to drive speed and agility, and to lower costs throughout their operations.

These benefits mean that harnessing the cloud is critical to many parts of the CSPs’ strategic agenda, and make navigating the transition to a cloud-centric operating model an urgent priority for many companies. The key question is how to get started. The solution lies in combining a methodical approach with a commitment to moving at pace. To help CSPs achieve this, we’ve developed the approach shown in Figure 6, enabling a successful transition to be managed through a clear five-step process.

CSPs that undertake this journey will be well placed to compete and win in tomorrow’s communications services marketplace—and to realise the aspiration of ‘zero infrastructure – anything-as-a-service’. Figure 6: A five-stage transition management process for moving to a cloud-centric operating model 0. Baseline assessment Baseline infrastructure and application portfolio estate to determine feasibility of the organisation’s cloud adoption aspirations 1. 2. 3. 4. Value assessment and business case Strategy and road map development Cloud operating model Readiness and maturity assessment Determine the business value of the cloud solution chosen by an enterprise and evaluate it through the lenses of cost, usability, functionality, and agility Enable organisations to develop a unified cloud strategy that aligns business vision, values, and objectives with a cloud solution Define the processes, organisation structure, roles, skills, and governance required to effectively operate in a cloud environment Assess cloud adoption readiness based on infrastructure, governance, and process maturity 5. Target-state service and architecture development Define cloud functionality to meet business objectives, develop architecture to achieve these functionalities, and design capabilities to manage cloud services Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 7 . www.pwc.com/communicationsreview About the authors Florian Groene Florian Groene is a principal with PwC Strategy& US. For more information, contact Florian by phone at +1 212 551 6458 or by email at florian.groene@strategyand.us.pwc.com Bryan Herdé Bryan Herdé is a director with PwC Strategy& US. For more information, contact Bryan by phone at +1 305 375 7393 or by email at bryan.herde@strategyand.us.pwc.com Danielle Phaneuf Danielle Phaneuf is a director with PwC Strategy& US. For more information, contact Danielle by phone at +1 415 653 3518 or by email at danielle.phaneuf@strategyand.us.pwc.com Florian Stürmer Florian Stürmer is a director with PwC Strategy& Germany. For more information, contact Florian by phone at +49 89 54525 568 or by email at florian.stuermer@strategyand.de.pwc.com © 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 157 countries with more than 208,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com.

112277-2016 LL .

The cloud is becoming the core delivery model for provisioning business technology, with an aspiration to achieve an IT footprint based on ‘zero infrastructure – anything-as-a-service. As cloud enters the mainstream… After years of hype, the long-awaited promise of cloud computing—especially public cloud services—has now moved into mainstream business reality. As Figure 1 shows, annual growth in spending on public cloud services—at 22%—is dramatically outpacing general IT spending growth, at 4%. And the rising spend on public cloud is gradually expanding beyond the relatively mature software-as-a-service (SaaS) space, into the faster-growing infrastructure-as-a-service (IaaS) and platform-as-a-service (PaaS) segments. …its hard business benefits come to the forefront As the momentum behind—and confidence in—public cloud services continues to grow, C-level executives are increasingly using the cloud to solve the most important business and technology challenges across all functions of the business. The accompanying information panel shows the range of benefits, from more variable costs to enhanced speed, agility and innovation, that cloud provides. In light of these advantages, and the ongoing investment and innovation by public cloud providers, companies’ initial reservations about cloud solutions—focused primarily around issues such as security, the complexity of IT management in a cloud environment, and risks of vendor lock-in—have begun to dissipate.

As a result, the cloud is becoming the core delivery model for provisioning business technology, with an aspiration to achieve an IT footprint based on ‘zero infrastructure – anything-as-a-service.’ Figure 1: Corporate IT spend on public cloud services and the rest of IT, 2013-2017 Total IT spend (in US$ billions; CAGR) Spend for public services (CAGR 2013-2017) PaaS +27% $630 $491 +22% $107 $49 $442 +4% IaaS +26% 29% 13% $523 58% 2013 Public cloud 2017 Rest of IT SaaS +20% Source: IDC, Forrester, Gartner, Oracle with PwC’s Strategy& analysis. ‘Zero infrastructure – anything-as-a-service’ Communications Review 1 . As telecoms markets become saturated and price competition heats up, they need to drive costs—including technology costs—out of the business much more aggressively than before. Some benefits of cloud computing • • • • • Costs: An ability to move from fixed to variable costs, and create a more competitive IT environment based on pay-per-use provisioning Scalability/elasticity of supply: Resources can be scaled based on user demand, and resource utilisation becomes more transparent Manageability: Greater self-service and automation, with SaaS/PaaS replacing complex legacy solutions Agility: Faster time-to-market for new offerings, and an enhanced ability to pilot solutions and ‘fail fast’ Mobility: Greater alignment with new customer behaviour, and enhanced ability to support mobile workforces For CSPs, today’s business imperatives… …are raising significant IT challenges As CSPs plan out their strategies for this new world, they’re focusing on fulfilling several business imperatives. Amongst these, one of the highest-priority items on their agenda is re-imagining customer experience to be much more digital-centred. This includes advances such as enhanced mobile self-service apps and improved digital commerce capabilities. Further imperatives include reshaping the retail experience to meet the distinct expectations of millennial customers, and showcasing the product portfolio in a way where digital assists and enriches the end-to-end shopping and purchasing experience. As they strive to achieve all these goals, CSPs are coming up against several IT challenges. One of the biggest is talent: they need to supplement traditional business support systems/operation support systems-type (BSS/ OSS) IT engineering skills with new talent that can deliver against the digital agenda, and is well-versed in front-end user experience/user interface design, modular service integration, and content management and delivery. At the same time, CSPs are also prioritising the building and delivery of a new range of products—including IPTV, mobile video and other digital content services—together with the advertising and (e)commerce engines needed to drive sales of, or otherwise monetise, these products. Further key components of their product sets include internet-of-things (IoT) solutions ranging from consumer wearables to solutions for the connected car and smart home.

And as telecoms markets become saturated and price competition heats up, they need to drive costs— including technology costs—out of the business much more aggressively than before. ‘Zero infrastructure – anything-as-a-service’ A further challenge is the need to build new capabilities that combine the traditional carrier-grade ‘waterfall’ engineering and release management required for the BSS/OSS legacy, with the more iterative, agile, rapid prototyping methods needed for the digital user experience and expanded product suite. CSPs must also open up their IT architecture to enable interoperability with an increasingly broad ecosystem of partners, in areas including content provisioning, IoT, data analytics, advertising, and more. And they have to bring down IT costs by relying more heavily on outsourcing, and using more scalable and efficient cloud services—which increasingly means public cloud. Communications Review 2 .

To help CSPs map out and undertake the optimal journey to a cloudenabled ‘zero infrastructure’ future for their IT, we’ve developed the framework for a cloud-centric operating model. A framework for delivering on the promise of cloud controls for cloud consumption, performance and vendor/partner management. Leading CSPs are now rising to all these challenges by transitioning successfully to the cloud. To do this, they’re evolving their technology operating models into a mix of enhanced traditional operating model capabilities and new cloud-centric capabilities. These new capabilities include a consultative approach to cloud demand and business relationship management; a re-tooled architecture, engineering and operations capability, embracing concepts such as cloud orchestration, continuous integration and deployment, and development and operations (DevOps); and strong For any company embarking on this change journey, where to start—and where to focus—depends on the business’s specific industry, size, business model, and current digital maturity. However, the key components of an ideal cloud-centric operating model remain consistent.

So, to help CSPs map out and undertake the optimal journey to a cloud-enabled ‘zero infrastructure’ future for their IT, we’ve developed the framework for a cloud-centric operating model shown in Figure 2. We’ll now examine each component of the framework in turn. Figure 2: Our blueprint of the components of an ideal cloud-centric operating model Cloud demand CMO: Sales and marketing CPO: Product value chain Other CxOs: Analytics, financial reporting, HR benefits administration, etc. Cloud demand management Cloud solution evangelism and consulting Portfolio assessment focused on cloud adoption planning Cloud supply management Cloud architecture and engineering Cloud operations Cloud-first architecture design Multi-cloud/hybrid cloud operations (zero infrastructure aspiration) DevOps discipline and tooling for continuous integration, deployment, and multi-cloud operations Cloud vendor management Cloud supply Strategic cloud solution sourcing Public cloud solution vendors Vendor relations and innovation exchange Private/hybrid cloud solution vendors SLA and vendor performance management Ancillary cloud management providers Cloud cost and consumption management: Disciplined metering, tuning, and reporting for consumption-based cost charge-back model Workforce/talent management: Continuous talent pool mix and skill set development to support cloud-focused organisation Cloud security and risk management: Cloud risk vs. benefits assessments, security policy setting, and audits Cloud transition management: Coordination and programme management of initiatives to move to/adopt cloud platforms Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 3 .

Cloud demand management Demand for cloud services is increasingly driven by C-level stakeholders outside the IT domain, each with their own strategic objectives, and each bringing implications for the company’s digital agenda. For example, the chief marketing officer (CMO) wants increased go-to-market speed and agility, and more innovative sales and marketing powered by cloud solutions. In terms of the digital agenda, these requirements call for digitised customer engagement platforms and advanced analytics enabled through cloud. In the not-so-distant future, the chief network officer (CNO) will be looking for an IT shop that can work as one team and help deliver the next generation of networks. These networks may be termed 5G, softwaredefined networks (SDN), or higher-density grids that carry the ever-growing access and backhaul data load of the internet of billions of things (and hundreds of millions of born-digital, video-streaming consumers). But whatever they’re called, these networks will all have one thing in common: they will rely heavily on cloud technologies to achieve step-changes in efficiency through network-function virtualisation (NFV) and the OSS/BSS stack to go with that. This means that the IT and network functions will converge even more.

And IT’s ability to mobilise cloud delivery capabilities, help deliver networks-as-a-service, and take network infrastructure scalability to the next level will turn what is often regarded today as a commodity function into a future competitive differentiator in the race for network leadership. Meanwhile, still other members of the C-suite are looking for enhancements such as tighter cost control and allocation, and further automation of backoffice processes. The implications for IT include a need to establish cloud consumption and cost control mechanisms, develop strong-form vendor management, and digitise back-end and support processes. Faced with these requirements, IT needs to take an ‘evangelistic’ stance towards cloud, helping to drive adoption while managing the demand for cloud-based services across the spectrum of Saas, IaaS, PaaS and— ultimately—anything-as-a-service. This role requires a portfolio-based assessment of cloud solutions and usage focused on planning for ongoing widespread cloud adoption. Cloud architecture & engineering Cloud IT architecture is constantly evolving, standards are still relatively rare, and new technologies are emerging almost daily.

Figure 3 summarises the key trends currently under way in cloud architecture Figure 3: Trends in cloud architecture stack technologies Platform Service catalog Technology stack Service assurance and SLA management Service billing and consumption control Release management tool kit Code repository, software configuration management, build/deploy coordination across environments Security controls Security policies, compliance audits, and risk management Quality assurance orchestration Automated testing, test case management Orchestration Orchestration of continuous integration and deployment Integration and deployment pipes Operations monitoring Monitoring, alerts, and backups to ensure quality of service level Service metrics Consumption and cost metrics for metering and reporting purposes Resource orchestration Resource stacks, payload allocations (storage, computer power, network), images (instances and failovers/disaster recovery) Infrastructure Public cloud A Public cloud B Cloud supply Public cloud C On-premise virtual machines Growing list of commercial and open-source solutions provide a range of alternatives to manage the cloud technology stack. App container and orchestration can be managed through a number of platforms. Fierce competition within public cloud space is driving prices down. Private cloud and on-premise VM providers are expanding into hybrid solutions. Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 4 . stack technologies. Even a cursory review of this chart underlines that many CSPs currently have only a few of the components and capabilities shown in the chart. This means they need to move fast, most importantly, by building a cloud orchestration stack with a strong focus on public cloud. CI/CD best practice and the corresponding tools in areas including code repository management, automation build, self-testing and automated deployment. The second aspect of effective cloud operations is multicloud service management, both to ensure a consistent, high-quality user/customer experience across distributed clouds, and to coordinate multiple third-parties that contribute to delivering a given service. This requires the design of end-to-end measures at platform and aggregated service level, and the adaptation of proven IT service management disciplines to a multi-cloud setting—including activities around monitoring, events and alerts; incident and problem flows; and monitoring and managing performance against service-level agreements (SLAs). In building their cloud architecture, CSPs must balance their business requirements with the rapidly-changing technology landscape, and select the architecture components that are right for their own business. A key factor in achieving the right balance is adopting the idea of ‘cloud first’—designing for the cloud as the primary platform, rather than designing first for on-premise and then adapting for the cloud.

Cloud-first means architecting for speed, flexibility and modularity, and enables the business to avoid getting stuck in the tangle of complexities that still afflicts many CSPs. Cloud operations A cloud-centric delivery model requires a new, more fluid, DevOps-style approach to service deployment and operations. This has two aspects. The first is continuous integration and deployment (CI/CD), reflecting the need to roll out simultaneous—and more frequent—software releases, and to coordinate multiple cloud platforms with the ability to scale rapidly according to changing build/ test/run needs.

In response, organisations need to adopt With these two aspects addressed, the new cloud-based delivery capabilities will then provide the foundation and means to ‘clean house’ and migrate a significant share of on-premise IT to the cloud. Whilst this may not initially enable a CSP to deliver fully against its ‘zero infrastructure’ aspiration, it does open up significant and ongoing potential to reduce infrastructure. The four-step pathway towards a zero infrastructure footprint is shown in Figure 4, with every step being applied across the complete apps, computing, and storage stack. Figure 4: The four-step pathway towards a zero infrastructure footprint Decommission: ‘Stop’ Reduce infrastructure estate by identifying and eliminating underutilized assets Move to the cloud: ‘Ship’ Migrate eligible on-premise hosted applications and services to cloud-based solutions Virtualise: ‘Shrink’ Consolidate: ‘Merge’ Shrink remaining physical asset estate through virtualisation of servers and storage Reduce remaining physical infrastructure footprint through consolidation of assets within and across data centres Performance and utilisation should be consistent boundary conditions across the steps Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 5 .

Cloud vendor management and cloud supply The cloud service supplier landscape is hugely diverse and continues to experience rapid innovation and dynamic change. Consequently—as Figure 5 illustrates— the degree of maturity varies across technologies and domains. Given this combination of disparity and diversity in the supplier market, vendor management in a cloud environment requires a fundamentally different skillset from that needed in a legacy environment. This is because cloud requires the ability to orchestrate a lot more complexity, since there are typically a lot more providers. Sourcing cloud services through a central vendor management office (VMO) function allows a CSP to leverage scale and expertise across all levels of the stack. However, it remains vital to ensure the VMO is equipped with the skills to manage an environment that becomes increasingly complex, rather than simpler. Cloud cost and consumption management Turning to the four ‘horizontal’ elements of the blueprint, the first of these—cloud cost and consumption management—is an area where CSPs can choose between several cost models, each providing a different level of transparency.

But whatever model is chosen, the key is to monitor consumption very closely and be rigourous about holding consumers in the business accountable through appropriate reporting, show-back or charge-back methods. Without this discipline and control, cloud can increase costs. For a CSP to control cloud service cost and consumption effectively, the following common elements will be needed: • A defined services catalogue to enable IT costs to be allocated in business-relevant terms that reflect the services provided • Accurate, granular data and supporting systems to track and manage cost allocations • A change in organisational behaviour to adopt consumption-based billing and chargeback models • Embedded financial acumen across roles within the organisation (i.e., service managers) to actively manage and fine-tune consumption-based costs • Active communication of the allocation process to the organisation by IT, business units, and Finance to ensure alignment with the planning and budgeting processes. Figure 5: Cloud supplier landscape with examples, relative maturity, and characteristics of each segment SaaS examples Enterprise software � IBM � Oracle � SuccessFactors � Workday Characteristics: Collaboration and productivity Content management � Atlassian � Google for Work � Jive � Kaltura � Office 365 � ON24 � Yammer � Adobe CQ5 � HP Autonomy � OpenText � SDL CRM E-commerce/ payments � Oracle Service Cloud � Salesforce � SugarCRM High supplier diversity � Demandware � Hybris Software � IBM Sterling Commerce � Intershop � Oracle Commerce Will continue to grow as more applications move to the cloud Interoperability is a challenge PaaS examples Security � Alert Logic � Integralis � SAVVIS � Silver Sky Private cloud stacks/solutions App containers and middleware � Cisco � IBM � Microsoft Azure � OpenStack � VMware � Docker � Force.com � Google App Engine � IBM Bluemix � Microsoft Azure � TIBCO Big data and analytics � Adobe Analytics � Amazon Web Services � Cloudera � Hortonworks � MapR � SAP HANA � SAS Analytics � Webtrends Emerging standards (e.g., Docker, OpenStack) Need to integrate and bridge private and public offerings IaaS examples Network Infrastructure � Brocade � Cisco � HP � Juniper � OpenFlow � VMware (Enterprise) storage Computing � Amazon Web Services S3 � Box � Dropbox � Egnyte � Google Cloud � Microsoft Azure � Amazon Web Services EC2 � Google App Engine � Microsoft Azure � SoftLayer Maturity of product offering: High Medium Growth will be driven by volume/unit cost advantages Growing maturity of offerings Diminishing relevance of risk/security concerns Low Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 6 .

Workforce/talent management In terms of talent, moving to a cloud-first organisational model requires a CSP to shift the balance away from the IT knowledge and skills in today’s workforce—such as traditional development methodologies based on a strong engineering and technical focus—and towards the more service-oriented skills needed in a cloud environment. These new skills are likely to include fitfor-purpose development methodologies such as agile and DevOps; skills in configuring and integrating SaaS apps and platforms; deep finance and business acumen; information and service management skills; and capabilities in outcomes-based vendor management. A particular focus should be on finding and developing ‘digital keystone’ skills such as project and programme management, quality assurance, prototyping, security, business requirements management, and user experience design. Cloud security and risk management As a CSP moves to cloud-centricity, it must adapt and evolve its security and risk management, while taking account of the fact that the benefits of cloud adoption continue to outweigh the security risks. Whilst concerns over cloud security and exposure to third-parties have historically acted as inhibitors to cloud adoption, acceptance of cloud’s benefits over the related risks is growing rapidly—along with a realisation that security levels can actually be improved through cloud solutions. Key actions include establishing a cloud security capability to manage the risks of cloud adoption, developing a response plan in the event of a breach, and avoiding collecting and processing un-curated data in the cloud. Cloud transition management For CSPs worldwide, cloud presents exciting opportunities to drive speed and agility, and to lower costs throughout their operations.

These benefits mean that harnessing the cloud is critical to many parts of the CSPs’ strategic agenda, and make navigating the transition to a cloud-centric operating model an urgent priority for many companies. The key question is how to get started. The solution lies in combining a methodical approach with a commitment to moving at pace. To help CSPs achieve this, we’ve developed the approach shown in Figure 6, enabling a successful transition to be managed through a clear five-step process.

CSPs that undertake this journey will be well placed to compete and win in tomorrow’s communications services marketplace—and to realise the aspiration of ‘zero infrastructure – anything-as-a-service’. Figure 6: A five-stage transition management process for moving to a cloud-centric operating model 0. Baseline assessment Baseline infrastructure and application portfolio estate to determine feasibility of the organisation’s cloud adoption aspirations 1. 2. 3. 4. Value assessment and business case Strategy and road map development Cloud operating model Readiness and maturity assessment Determine the business value of the cloud solution chosen by an enterprise and evaluate it through the lenses of cost, usability, functionality, and agility Enable organisations to develop a unified cloud strategy that aligns business vision, values, and objectives with a cloud solution Define the processes, organisation structure, roles, skills, and governance required to effectively operate in a cloud environment Assess cloud adoption readiness based on infrastructure, governance, and process maturity 5. Target-state service and architecture development Define cloud functionality to meet business objectives, develop architecture to achieve these functionalities, and design capabilities to manage cloud services Source: PwC’s Strategy& ‘Zero infrastructure – anything-as-a-service’ Communications Review 7 . www.pwc.com/communicationsreview About the authors Florian Groene Florian Groene is a principal with PwC Strategy& US. For more information, contact Florian by phone at +1 212 551 6458 or by email at florian.groene@strategyand.us.pwc.com Bryan Herdé Bryan Herdé is a director with PwC Strategy& US. For more information, contact Bryan by phone at +1 305 375 7393 or by email at bryan.herde@strategyand.us.pwc.com Danielle Phaneuf Danielle Phaneuf is a director with PwC Strategy& US. For more information, contact Danielle by phone at +1 415 653 3518 or by email at danielle.phaneuf@strategyand.us.pwc.com Florian Stürmer Florian Stürmer is a director with PwC Strategy& Germany. For more information, contact Florian by phone at +49 89 54525 568 or by email at florian.stuermer@strategyand.de.pwc.com © 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 157 countries with more than 208,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com.

112277-2016 LL .