Description

MIAX OPTIONS EXCHANGE

LIMIT UP/LIMIT DOWN STATES AND THE OBVIOUS ERROR RULE ASSESSMENT

Background:

The Plan to Address Extraordinary Market Volatility Pursuant to Rule 608 of Regulation NMS was

implemented on April 8, 2013. MIAX proposed to exclude transactions executed during a Limit State or

Straddle State from MIAX Rule 521 (Obvious and Catastrophic Errors), to the extent set forth in

paragraph (j) of MIAX Rule 530 (Limit-Up-Limit-Down) for a one-year pilot basis (see SR-MIAX-2013-12).

MIAX believes that the application of the Obvious and Catastrophic Error Rule to all transactions

occurring during a Limit or Straddle State would be impracticable during Limit and Straddle States, and

could produce undesirable effects. MIAX believes that market participants should not be able to benefit

from the time frames allotted to them from the time of the affected transaction within which they may

request a review of their transactions in these situations and that it is appropriate to suspend

application of Rule 521 for all transactions occurring during a Limit or Straddle State (except for

erroneous transactions that resulted from a verifiable disruption or malfunction of an Exchange

execution, dissemination, or communication system, or due to an erroneous quote or print in the

underlying NMS Stock).

The purpose of this report is to, in connection with assessing the impact of the Obvious Error Rules

during Limit and Straddle States, (1) evaluate the statistical and economic impact of Limit and Straddle

States on liquidity and market quality in the options markets, and (2) assess whether the lack of obvious

error rules in effect during the Straddle and Limit States are problematic.

Data:

The MIAX analyzed the trades that occurred during the Limit and Straddle States (“States”) between the

months of May 2014 and April 2015. MIAX tracked trades and market quality for situations where there

was at least one trade in an option series during a State.

During the review period mentioned above, there were a total of 25 underlying stocks that entered the

State phase and there was at least one trade in an option series during the State.

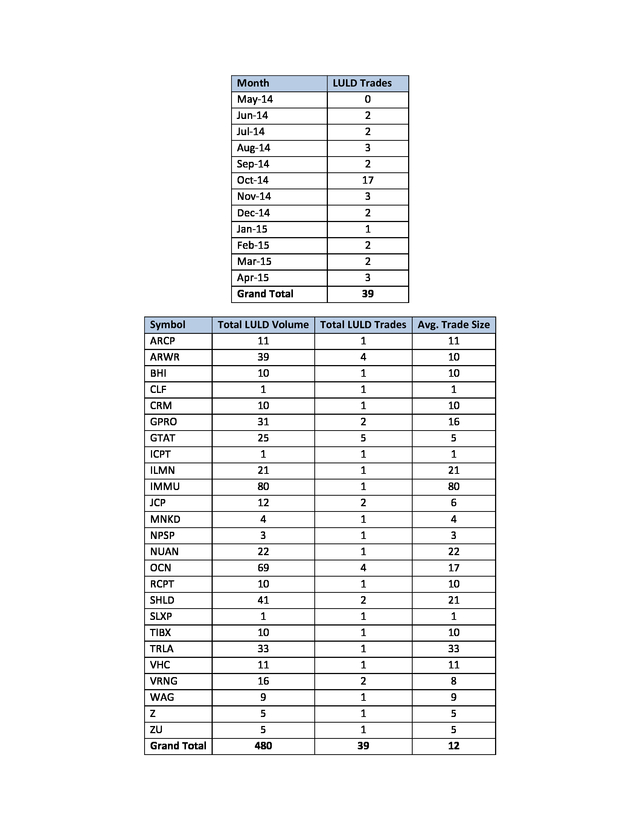

There were 39 trades during the States for a total quantity of 480 contracts. October 2014 contained the highest number of LULD trades accounting for 17 of the 39 total trades. There were 6 transactions during a Limit State and 33 transactions during a Straddle State.

There was a single LULD transaction in 18 of the 25 securities listed. With regard to price volatility, 5 of the instances had a price change in an option series of 30% or more during the State phase compared to the last trade before the State phase; and 4 of the instances had a price change in an option series’ price move 30% during the five minute period after it exited the State phase. Finally, there were no obvious error reviews during the review period. The tables below summarize the information contained in the periodic LULD reports submitted to the Commission on a monthly basis. . Month May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 Grand Total LULD Trades 0 2 2 3 2 17 3 2 1 2 2 3 39 Symbol Total LULD Volume Total LULD Trades Avg. Trade Size ARCP 11 1 11 ARWR 39 4 10 BHI 10 1 10 CLF 1 1 1 CRM 10 1 10 GPRO 31 2 16 GTAT 25 5 5 ICPT 1 1 1 ILMN 21 1 21 IMMU 80 1 80 JCP 12 2 6 MNKD 4 1 4 NPSP 3 1 3 NUAN 22 1 22 OCN 69 4 17 RCPT 10 1 10 SHLD 41 2 21 SLXP 1 1 1 TIBX 10 1 10 TRLA 33 1 33 VHC 11 1 11 VRNG 16 2 8 WAG 9 1 9 Z 5 1 5 ZU 5 1 5 Grand Total 480 39 12 . Conclusion: MIAX believes that there is insufficient data to make a reliable statistical and economic evaluation of market quality in the options market during States. MIAX further believes that there is insufficient data to make a reliable assessment of whether the lack of obvious error rules in effect during straddle and limit states are problematic. As noted above, to date, the Exchange has not received any requests for review of a transaction pursuant to Rule 521 when the underlying security was in a State. As such, MIAX has not identified any problematic outcomes as a result of the pilot rule. .

There were 39 trades during the States for a total quantity of 480 contracts. October 2014 contained the highest number of LULD trades accounting for 17 of the 39 total trades. There were 6 transactions during a Limit State and 33 transactions during a Straddle State.

There was a single LULD transaction in 18 of the 25 securities listed. With regard to price volatility, 5 of the instances had a price change in an option series of 30% or more during the State phase compared to the last trade before the State phase; and 4 of the instances had a price change in an option series’ price move 30% during the five minute period after it exited the State phase. Finally, there were no obvious error reviews during the review period. The tables below summarize the information contained in the periodic LULD reports submitted to the Commission on a monthly basis. . Month May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 Grand Total LULD Trades 0 2 2 3 2 17 3 2 1 2 2 3 39 Symbol Total LULD Volume Total LULD Trades Avg. Trade Size ARCP 11 1 11 ARWR 39 4 10 BHI 10 1 10 CLF 1 1 1 CRM 10 1 10 GPRO 31 2 16 GTAT 25 5 5 ICPT 1 1 1 ILMN 21 1 21 IMMU 80 1 80 JCP 12 2 6 MNKD 4 1 4 NPSP 3 1 3 NUAN 22 1 22 OCN 69 4 17 RCPT 10 1 10 SHLD 41 2 21 SLXP 1 1 1 TIBX 10 1 10 TRLA 33 1 33 VHC 11 1 11 VRNG 16 2 8 WAG 9 1 9 Z 5 1 5 ZU 5 1 5 Grand Total 480 39 12 . Conclusion: MIAX believes that there is insufficient data to make a reliable statistical and economic evaluation of market quality in the options market during States. MIAX further believes that there is insufficient data to make a reliable assessment of whether the lack of obvious error rules in effect during straddle and limit states are problematic. As noted above, to date, the Exchange has not received any requests for review of a transaction pursuant to Rule 521 when the underlying security was in a State. As such, MIAX has not identified any problematic outcomes as a result of the pilot rule. .