Description

GUIDE TO:

Claims

SPONSORED BY

FC_SR_Claims2013.indd 1

22/11/2013 15:55

. Your claims

take expertise.

We have the tools and the knowledge.

Wherever your business operates, whatever your industry, you can expect the same

seamless claims service from AIG. Working with our clients before a claim happens means

our experts can respond effectively at the moment of truth. Our sophisiticated tools and

systems ensure that your claims are processed promptly. Learn more at www.AIG.com

Insurance and services provided by member companies of American International Group, Inc.

Coverage may not be available in all jurisdictions and is subject to actual policy language. For additional information, please visit our website at www.AIG.com. AIG Europe Limited is registered in England: company number 1486260. Registered address: The AIG Building, 58 Fenchurch Street, London, EC3M 4AB. Pages.indd 1 22/11/2013 16:51 .

INTRODUCTION Finding the path of least resistance Almost everyone hopes they will never need to use their insurance but if it becomes necessary, understanding how to navigate a path through the claims process is crucial B USINESSES BUY INSURANCE hoping that they will never have to make a claim. Yet the reality of modern corporate life is that almost every company will at some point be forced to do exactly that. And when a claim is made it is crucial that the process is handled as smoothly as possible so that the claimant can continue to operate unencumbered by any losses. However, the claims process is o en complex, particularly for large corporate businesses dealing with multinational jurisdictions. The aim of this Guide to Claims is to help ï¬rms navigate this procedure and also to understand how to ensure they are best placed to tackle any problems they may face. Through a series of comprehensive chapters, this guide considers such varied issues as insurance buying, dealing with major losses, claims preparedness and regulatory concerns. A number of leading European risk professionals were consulted extensively for this publication and they provide sage advice and the voice of considerable experience throughout. Dealing with claims can sometimes be difficult and time consuming. This can be particularly acute when the claimant has not prepared properly.

Of course, there are some Guide to claims 01_Intro_Claims13.indd 1 scenarios which cannot be foreseen, but by increasing their knowledge of the way in which the claims process functions, this guide aims to help companies be in a position to work effectively with their insurer. At the heart of any claims process is the relationship between the insurer and the claimant. This guide will explore ways in which insurance companies and their customers can achieve a quick and satisfactory outcome no matter what the loss scenario might be. It is important insurers and their customers work together as a partnership if the claims process is to be tackled speedily and comprehensively and there are helpful tips on how to make this work for both parties. Trust is an essential part of this relationship so that customers know when they buy insurance that the insurer will pay out in the event of a claim. While some trust is largely developed from existing relationships, this guide will show businesses what to look out for and also the type of questions to ask so they are conï¬dent that when the time comes to claim they will not be le out of pocket. Mike Jones, editor StrategicRISK www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 1 22/11/2013 15:57 . CONTENTS 04_06 Communication with insurers Editor Mike Jones Deputy editor Kin Ly Asia editor Sean Mooney Junior reporter Asa Gibson 21 A sustainable relationship 07_09 22 Workshop enterprise Operate globally, think locally 12 23_25 Be prepared Infrastructure Art editor Nikki Easton 13 26_27 Business development manager Lucy Weston Insurer innovation Data 14 28 Deputy chief sub-editor Graeme Osborn Sub-editor Janina Godowska Commercial director, Asia-Paciï¬c Adam Jordan Senior production controller Alec Linley Data intelligence analyst Fez Shriwardhankar Associate publisher Tom Byford Executive publisher, Asia-Paciï¬c William Sanders Managing director Tim Whitehouse Published by Newsquest Specialist Media Ltd London office: 30 Cannon Street, London EC4M 6YJ tel: +44 (0)20 7618 3456 fax: +44 (0)20 7618 3420 (editorial) +44 (0)20 7618 3400 (advertising) email: strategic.risk@newsquest specialistmedia.com Asia-Paciï¬c office: 3/9 Barrack Street, Sydney, NSW 2000, Australia tel: +61 (0)2 8296 7611 Involve the boss Making a claim 15 29 Stress testing Be in control 16_17 30 Expect the right attitude Need for speed 18_20 31_32 Get the right experts When it’s over SPONSORED BY © Newsquest Specialist Media 2013 To email anyone at Newsquest Specialist Media, please use the following: ï¬rstname.surname@ newsquestspecialistmedia.com 2 StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 02_03_Contents_Claims13.indd 2 Guide to claims 22/11/2013 15:53 . Guide to claims 02_03_Contents_Claims13.indd 3 www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 3 22/11/2013 15:54 . COMMUNICATION WITH INSURERS When honesty really is the best policy Building a relationship with an insurer and providing as much information about what your business does is vital in the event that you have to make a claim 4 B E OPEN, BE HONEST, LISTEN WELL – and don’t hold back. Risk managers across Europe interviewed for this report all agreed on one particular point: the importance of prioritising good communication with your insurer. It was referenced again and again, both as the single best way to speed up claims and get paid, and as the most effective strategy to keep the whole process in house and avoid recourse to lawyers. It sounds simple, but in a world deï¬ned by legal language and with potentially large sums of money a stake, it is not always easy. The ï¬rst stage of successful communication is all to do with attitude: you have to be willing to engage. “Be polite, but show clearly what your goals are,” says Hans-Jürgen Allerdissen, chairman of the German risk and insurance managers’ association DVS. But it is also essential to make sure your insurer has the same attitude and the same willingness to engage. Daimler Insurance Services managing director of corporate insurance Ingo Telschow says: “As risk managers, we need to foster transparency and open communication.” The most important way of achieving this is through regular contact with your insurer, according to Belgium-based Marie Gemma Dequae, board member of several companies and risk associations, consultant, adviser and Ferma president from 2005–2009. “This goes broader than claims management,” she says. “It’s important, not just to have contact with your account manager, but also your underwriter and your claims handler.” You need to be familiar with all your key contacts long before making a claim. Key to making these important relationships work is information.

“First of all, StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 04_06_Comms_Claims13.indd 4 well-prepared data is essential for successful co-operation,” says Telschow. “What’s more, setting up regular meetings with your partners can be particularly helpful to create trust. The most common pitfall may be a loss of trust because of a lack of transparency.” Good communication means keeping your insurer informed about your operations, and risk managers need to check that their insurance contract has the right information about what is going on in their company – the last thing anyone wants is a surprise. Information, information “Claims management is linked to the type of risk,” says Dequae.

“For example, if you have a property claim then it’s important when you are preparing to make a claim you need to make sure that your insurer has all the information about the buildings, what goes on in the buildings, what machinery is there, what the business interruption issues are. “For transport-related claims your insurer needs to know the destinations, the transport means – rail, airplane, truck – the type of products.” Failing to provide this information can severely complicate the claims process, making investigations longer and potentially delaying settlements. “For example, if you have a transport claim and your insurer wasn’t aware you were sending goods to the US, then you can have a problem right there,” says Dequae. “For me, the most important area is product liability, because there you have also a potential risk to reputation. It’s important you keep your insurers aware of what you are making, the speciï¬cations and processes.” Insurers also need to be kept informed about how your risk function operates. Communicate clearly and demonstrate how your company handles risk, illustrate what Guide to claims 22/11/2013 14:46 .

Shutterstock has been put in place in terms of risk management – organisation, policy, processes, enterprise risk management – and don’t hesitate to give some concrete illustrations to illustrate your point. Detail is important. But communication is two-way, and not only does the insured have to ensure a clear flow of appropriate information to the insurer, the insurer has to prove that it is able to understand it. It works both ways. “Implement your own processes to be able to provide good and relevant data to insurers in order to describe the risks you want to them to cover,” says French energy service company Dalkia’s head of risk management François Beaume. “Data consistency and quality are key in building trust and relationship with insurers. Pay attention to that and allocate some times to work on it. A good way to achieve this is to implement a network of internal correspondents that will deploy your risk management policy throughout the company. “A risk management information system could be a strong support to structure this approach.

In addition, it will give you an advantage and a way to leverage your discussions with brokers and insurers as you will be able to rely on your own data – such as a list of locations, insured values and loss history.” In short, all sides need to provide clarity. “The risk manager should understand the world of the insurers and vice versa,” says aerospace and defence company EADS’s chief risk officer Christoph Schwager. “They should be able to speak the same language.” Understanding the business Good communication is also essential within – as well as between – both organisations. Guide to claims 04_06_Comms_Claims13.indd 5 “The risk manager should be embedded in the business and should know the operations,” says Schwager. “However, this is unfortunately sometimes not the case.

Risk managers need to know what can be insured, and insurers need to understand the business to develop new insurable solutions.” Also, while consistency is an important asset in an insurer, risk managers need to know that their insurer is capable of viewing them as an individual: sectors vary in their needs and businesses vary within sectors. The dialogue between insurance managers and risk managers needs to be open and frank and cover all aspects of the industry in which they operate, its dynamics and the wider environment in which the risk is embedded. “We need to educate and foster a better understanding about our industries,” says Olivier Balmat, head of group risk management and responsible for enterprise risk management within global agri-business Syngenta. “Too o en I encounter underwriters and account executives who only have a faint understanding of manufacturing and operating in a global economy. ‘Risk managers need to know what can be insured, and insurers need to understand the business to develop new insurable solutions’ Christoph Schwager EADS » www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 5 22/11/2013 14:46 . COMMUNICATION WITH INSURERS » ‘We need to awaken the curiosity of our insurance counterparts to learn more about what we do, how we think and how we operate’ Olivier Balmat Syngenta “Most insurance people have no professional background outside insurance. However, without a general understanding of the industry activities one will have difficulties understanding the associated risks. “We need to awaken the curiosity of our insurance counterparts to learn more about what we do, how we think and how we operate. This should not be limited to renewals. “A learning process takes time and should engage outside immediate business pressures: creating an atmosphere where asking questions is rewarded rather than being unwelcome is important.” Balmat says that risk managers should also be invited to challenge their insurance contacts by asking questions and talking about industry and risk. “We should get away from the game of hiding behind the bushes and being afraid of opening up to a factual and honest discussion about what we do and what we face as risks,” he says. “The trust-building effect of transparent communication is not to be underestimated and ultimately will beneï¬t the insurance and risk managers. “I love talking about our business and I am passionate about it. My experience is that some underwriters highly appreciate the storytelling that brings the account much closer and renders it a more tangible and lively experience. “We need to see open communication in the light of positioning our risks and lending them an honest proï¬le,” Balmat says. A matter of trust Successful risk management is about many things – but when it comes to insurance it is important to remember that it is also a people business, and relationships and clear 6 StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 04_06_Comms_Claims13.indd 6 communication can be as important as policy wording and good data. Trust is key.

The insured needs to have faith that their risks are covered – and the insurer needs to communicate this to them fully and wholeheartedly. A claim is a business issue Julia Graham, director of risk management and insurance for the global law ï¬rm DLA Piper and newly elected president of Ferma says: “The payment of claims is, at the end of the day, fundamentally what you are buying when you procure insurance or other forms of risk ï¬nancing. “The willingness and ability of those who provide risk ï¬nancing is consequently key. “This may sound blindingly obvious, but if it is, parts of the insurance sector still have some way to go to produce solutions that live up to this.” When a claim occurs it’s a stressful time and an organisation should have an expectation that an event will be treated as a business issue by their insurers – not an event when you need to think about bringing in the lawyers to check over the wording. However, in addition to organisations such as Ferma lobbying the insurance sector to tidy up wordings and be more modern and transparent in their policy language, there is much that the risk manager, insurer and broker individually can do, working as a partnership, to minimise the likelihood of the above scenario. Making a claim is a business activity and as a risk manager it’s the activity when you have one of the greatest opportunities to demonstrate your value. Be prepared. Build up long-lasting relationships with people rather than with companies – and keep talking. SR Guide to claims 22/11/2013 14:46 .

WORKSHOP ENTERPRISE A hand-holding exercise to put ï¬rms back on their feet Clambering out of the devastation caused by a major loss can be a lonely and treacherous journey for any company, but AIG offers its clients survival classes Guide to claims 07_09_Workshop_Claims13.indd 7 W HEN IT COMES TO HELPING your ï¬rm negotiate the tricky maze of a major claim, there is no experience like experience. “Think in advance about potential loss scenarios and identify who the stakeholders’ key to recovery might be, understand how to reach them and agree how they might respond,” says Ferma president Julia Graham. “Particularly with a major loss, how is your insurer going to handle that claim, how are they going to put their team together and how are they going to work with you through the recovery and claims process? If you have a broker, do they have a role? This role might be especially productive where co-insurers or excess layer insurers are involved, taking pressure off your shoulders, with the brokers making sure that the full programme of insurers are engaged and on side. “On other occasions, brokers may simply add unnecessary and frictional activity – but speak to them – there is no right way or blueprint for engaging them. Engineering this process a er an event has occurred is too late.” In addition, some insurers are now offering dedicated claims relationship managers. “AIG in the UK has claims relationship managers (CLMs) to service and to stay close to our commercial clients and brokers,” says AIG UK claims client and broker service manager Stuart Rose. “The team have several professionals with many years’ experience and are among our most capable personnel. “We are involved both with prospective new clients and in relationships with our existing clients. CLMs are aligned to individual accounts and offer regular dialogue through stewardship and service meetings.

We also promote our claims service, including client training, and are a single point of contact to easily navigate the organisation. “Another way we engage is through our claims advisory board, where we sit down with key brokers and talk through topics of interest and update our brokers on what’s happening at AIG.” Developing a way to help clients get back on their feet in the event of a major loss led insurer AIG to launch a series of workshops to educate clients about what to expect when the worst happens. “We listened to our clients and recognised their feeling that there was a gap,” says AIG head of property and energy claims – Europe, Nick Barber. “We needed to work with them not just during the lifetime of a claim, but pre-loss as well.” The idea of providing workshops forms part of a wider drive at AIG to deepen its relationship with clients. “It is important that a client builds their relationship with their insurer outside of a loss claim,” says Barber. “One of our key strategies in achieving this is to organise pre-loss workshops with clients to run through potential claims scenarios with them long before they actually make a claim. This lets them explore the process and ensures that they understand what is expected of them and what they can expect from us, but it also gives them a chance to explore their own business continuity training.” Many ï¬rms – and even more executives – don’t have direct experience of a major loss. “It really can be a shock to the system,” says Barber.

“We need to be there to help them prepare by showing them what to do and who to contact in a variety of scenarios.” These theoretical scenarios give the insured the chance to explore what happens when they ask the question, OK, an incident has occurred – what do we do next? » www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 7 22/11/2013 14:51 . Shutterstock WORKSHOP ENTERPRISE 8 StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 07_09_Workshop_Claims13.indd 8 Guide to claims 22/11/2013 14:51 . » “They can explore how to make a claim and see the way that we will respond to that claim,” says Barber. “We work through the whole process from start to ï¬nish.” Potential perils Key to the success of the workshops is making sure the whole team is in the room, and workshops are to be attended by AIG experts, the client, the adjuster and the broker, if relevant. “We look at the client’s risk together and develop a scenario,” says Barber. “For example, we may look at some of their key locations and potential perils, come up with a ‘what if’ and then go through who to contact and what time frame to act within. “Clients need to understand who their key experts are.

They need to be able to deï¬ne their team. This may be added to at a later date, but they need to be aware of its basic structure. We also look to test and review policy wording around the scenarios. “We go into detail.

For example, if we were looking at a property claim we ask, is the building occupied? How many staff are inside? Is it owned by the client? Or rented? If we were dealing with a ï¬re we look at everything from making the claim to getting contractors on site to clear up. We look at who gets appointed, from carpenters to engineers and remediation ï¬rms,” he says. Workshopping scenarios A capable insurer’s advice will help the client through the maze Guide to claims 07_09_Workshop_Claims13.indd 9 Feedback from the insured has been positive. “Our clients seem upbeat and pleased with the level of detail,” says Barber. “There is a variety of examples where we are the lead insurer for a client and they have gone through this process with us and report back real beneï¬ts to their understanding. “In some cases just having a client in the room with their loss adjuster and hearing ‘We can’t predict everything or plan for every eventuality, but we can start the process – and that has to make things easier’ Nick Barber AIG how they talk and what their issues are can help their understanding.

It also works the other way round. O en, adjusters don’t know basic stuff about, say, staff numbers and building ownership, which is all very useful to know pre-loss. “What we have found is that the process works best over two or three sessions. First, we focus on workshopping the scenarios and then go on to review policy wording at a subsequent meeting.” The workshops take the insured through claims, helping them prepare for the worst in detail, to understand how they need to prepare themselves and their colleagues to make a claim, to show the information that they need, the people to contact and what steps to take when, and in what order. “We can’t predict everything or plan for every eventuality,” says Barber.

“But we can start the process – and that has to make things easier.” SR www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 9 22/11/2013 14:51 . Shutterstock THOUGHT LEADERSHIP Raising the bar for service delivery In an increasingly competitive environment, the ongoing challenge for insurance claim functions is to ï¬nd ways to continually improve and differentiate their service delivery. The speciï¬c needs of each client are shaped by many factors, including their industry sector, geographical footprint, supply chain challenges, as well as their approach to risk and insurance solutions. As change is happening more rapidly than ever there is a clear need for insurers and clients to work together or risk being disconnected at the time of greatest need – when the claim occurs. There is no simple answer to this challenge. Aside from investing in technology and other infrastructure improvements (which many have done), claims functions must get the underlying service delivery right. What constitutes “service delivery” in claims is evolving, though, as companies seek to differentiate themselves.

There is much more emphasis now on understanding the speciï¬c needs of the client and having the right level of expertise on hand to prepare for and respond to incidents when they occur. One area of differentiation is likely to be how insurers can leverage their expertise and knowledge and make this available to clients. This can be in speciï¬c and obvious areas (helping the client 10 learn from their own data), or in more innovative ways – perhaps by seeking opportunities to look at processes and, say, machinery exposures that may reside in different industry sectors but are similar in nature. Those who are best placed to help clients and risk managers be more informed and apply this knowledge into the risk framework will undoubtedly be more highly valued. Another area of differentiation will be in the area of risk/loss prevention, planning and mitigation – using actual scenarios and stress testing to work through how the respective parties will work and solve the many issues that will arise.

This is something that we have been doing for some time and the demand for it is increasing. O en, the client perception and experience will be determined by just getting the basics right, something that sounds easy. In practice this can be difficult to achieve, particularly where a client’s exposure sits across multiple products and geographies. Being seen as easily accessible, responsive, knowledgeable (about the client, the sector, the law, the geography and so on) and being seen as someone that clients can turn to even outside the context of a claim is increasingly the norm. Success will ultimately come down to how well the claims organisation is StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 10_11_EV1_Claims13.indd 10 Guide to claims 22/11/2013 14:57 .

designed to support clients (including how well it is joined up, top to bottom) and the skills, expertise and proactivity of the front-line claims teams and whether this is at the client’s disposal or is primarily looking a er the insurer’s interests. Our focus at AIG has been to work out how we design and build this, and it has led us to focus on several core design principles. First, segmentation of expertise and creating true product specialism. This means in practice that wherever we can we build local expert knowledge through specialising our people into one product area. This makes claims staff better informed about product issues and more equipped to apply lessons learned locally, both in handling and back into the product design process.

It also makes them a better resource for clients to tap into. Secondly, we have also actively segmented claims by severity/ complexity, recognising that the critical success criteria is quite different for small, straightforward claims as opposed to large and complex ones. The skill set and operational approach to each needs to be different for the insurer to deliver high-quality outcomes in claims of all types and sizes. This has led us to create three centres of excellence in our organisation, Guide to claims 10_11_EV1_Claims13.indd 11 namely Express (for smaller, less complex cases), Complex (for claims requiring a more in-depth level of review and investigation) and Major Loss – for the largest and most complicated/impacted claims on our clients. Finally, proactivity is critical. This term tends to be overused.

Experience tells us that the early stages of every claim are absolutely critical to getting the best outcome. This is as true for ï¬rst-party claims as it is for third-party, and includes completing investigations quickly, making early pragmatic coverage and liability decisions and making early partial/full settlements where possible. Proactivity also extends to how information that is key to progressing each case is chased down, how clients are informed throughout the lifecycle and also when key decisions are being made. Those who are able to demonstrate that they are empowering the front-line teams with the time, space and authority to proactively understand, focus on and satisfy the rapidly evolving client demands will ultimately achieve greater loyalty and a far higher satisfaction rating. Steve Eckhardt, chief claims officer, EMEA www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 11 22/11/2013 14:57 .

BE PREPARED The more you read, the more you’ll know SMEs and medium-sized businesses must know up front exactly what cover they are buying – as the costs that may be triggered by a failure to be meticulous could ruin their business Y OU CAN DO SO MUCH IN ADVANCE of ever having a claim to make sure that the relationship doesn’t have to be awful,” says AIG head of ï¬nancial lines claims Europe Noona Barlow. “It might not be the best relationship you’ve ever had, but take some basic steps and it will be mature and professional.” The ï¬rst thing to do is take a good long look at your policy. “One of the things we ï¬nd o en with our less sophisticated insured is that they are totally surprised by what the policy does – or doesn’t – cover, and what we are prepared to cover and prepared to do, and not do,” says Barlow. “You need to be asking questions before you make a claim because by the time you come to be making a claim it is already far, far too late. Far too late to ask what is covered, what is not covered. “You need to aware of what to ask in order to make sure that you are getting the most possible out of an insurance product. “The most fundamental piece of advice – and I realise it sounds obvious – but actually read your insurance policy.” Conflicting responses “Some policies limited upfront payments and this can be a real problem,” says Carl Leeman, chief risk officer at Belgium-based multinational logistics ï¬rm Katoen Natie. “Getting blended coverage is very important because the silo effect that has been created by insurers is not natural and not at all in line, in some cases, with the legal aspects. “For example, I have known insurers give conflicting responses to a theoretical claim.

I have given them an example and asked, is it clear? Yes. Is it third-party liability or personal liability? And they give different answers.” 12 StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 12_14_BePrepared_Claims13.indd 12 Particularly in smaller and medium-sized ï¬rms, cost and time pressures can lead to a superï¬cial acceptance of an insurance policy and a lack of analysis of the ï¬ne detail. Failure to report “When we are dealing with medium-sized ï¬rms and SMEs it is amazing how o en directors and risk managers don’t actually know what their policy covers them for,” says Barlow. “Two things happen: they either report things to us that would never be covered in any circumstance, or they fail to report in a timely fashion things that they are covered for. It’s that kind of experience. “Make sure you know up front what you are buying.

It’s just not enough to be able to say, ‘I know we have a policy in place’. “You have to worry because the potential consequences as a director if you are not indemniï¬ed by your company is that, if you have to pay, you could lose your house, you could go to jail, you could lose your marriage, whatever,” she adds. “Quite possibly you could be disqualiï¬ed from ever being a director again, and if that’s your livelihood then you have a signiï¬cant problem.” Defence costs According to Barlow, another important consideration is defence costs. Always know where your money is going, she advises. “If this is within a European context, beware of the pitfalls of local legal issues.

Don’t assume that because you have bought a ‘global’ product that you are covered everywhere. For example, in some countries your company is not allowed to indemnify you? Do you know that? “You need to take a rigorous and proactive approach to your policy.” SR Guide to claims 22/11/2013 15:01 . INSURER INNOVATION It’s the 21st century – mind your language G IVEN THE EMPHASIS ALL SIDES – insurer and insured – place on clarity of communication, it is strangely anachronistic that the document at the heart of their relationship can frequently be so opaque it needs a lawyer to translate it. “Why are we still burdened with oldfashioned ways of doing things?’ asks Julia Graham, who became president of the Federation of European Risk Management Associations at its bi-annual conference in October. “Why are wordings still used that probably didn’t mean much when they were dra ed 150 years ago? Yet alone today? What can we do together to modernise our sector? Because, when you have a claim, it’s not the time that you want to be thinking about the intention of the policy.” Graham says that, within a reasonable degree of tolerance a ï¬rm wants to know exactly what it is buying and what the insurer is willing to pay for – and poor writing can obscure this. “You need contract certainty,” she says. “The time to test the policy is not when you have to make a claim. “Why are wordings still conventionally bundled into ï¬rst and third-party products? Why, when new risks emerge, are new products designed rather than a fundamental re-look at what already exists not revisited? “One of my key words for this Ferma term as president is ‘Innovation’ – there is some way to go before we can call the insurance sector consistently innovative.

I sensed a recognition and enthusiasm at the Ferma Forum in Maastricht this year from our insurer panel that while we or they should Guide to claims 12_14_BePrepared_Claims13.indd 13 Shutterstock Ferma’s new president calls on the industry to shake up the way insurance tries to capture new risks by designing policies for today’s consumers not disregard all that is great about the insurance sector – including the knowledge, data, experience, trust and conï¬dence upon which this sector has been built – the sector recognises that there is room for improvement and that they are up for the challenge.” Reality gap Olivier Balmat believes that there is an increasingly dangerous “reality gap” between insurers’ risk perception and the policies they underwrite. “The world has moved, but basically we are o en stuck with policies that date back in the basic original form to the 1980s,” he says. “There is close to a quarter of a century between current risks and the products supposed to cover them; 25 years ago mobile phones were a rare item.

Today, they are an everyday product, sold and used in the billions. There needs to be a shi in the way insurance tries to capture modern risks with modern insurance products.” SR www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 13 22/11/2013 15:01 . INVOLVE THE BOSS Where the buck stops It’s tough at the top and knowing what your employees are up to is o en even harder, but in any company the boss must ensure that nothing is le to chance when buying insurance A know their level of protection at the purchasing stage. “One of the other things we o en see is, when we meet with a risk manager on a directors’ and officers’ policy, we’re not always meeting the directors and the others affected by that policy,” says AIG head of ï¬nancial lines claims, Europe, Noona Barlow. “So, we all need to know what time – if any – the director has spent with a policy. A policy should cover a director for everything that they would normally do while being a director, except the stuff that is illegal or fraudulent or intentional. But within that context they need to know about managing the associated costs. “Be aware that for the insurer, it’s just money.

But for the insured it’s so much more: their relationships, their reputations, their jobs – even their liberty. You have to factor all those things in. According to Barlow, it is essential that board members know what they are getting into – and that doesn’t stop with buying insurance. You need to look around at the corporate culture and structures in place and ask: are they good enough? “As a director you have to make enquiries and make sure that the company that you work for has appropriate corporate governance,” she says.

“I think that in the past a director would believe that as long as they did nothing wrong, they would be ï¬ne. But the reality is that now, if the Financial Conduct Authority is investigating, a director can still get targeted as a witness and have to hire a lawyer, and that’s time money and stress. It’s not enough to say, ‘I didn’t notice.’ Because you can still get a caution against you for having turned a blind eye and not acknowledging what was going on.

You have to make sure you know that what your colleagues are doing is appropriate.” SR StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com Guide to claims ‘You have to make sure you know that what your colleagues are doing is appropriate’ Shutterstock Noona Barlow AIG T MANY FIRMS BUYING INSURANCE is seen as a job for the executives. But placing all the responsibility on the shoulders of a risk manager – or even, in some cases, the procurement department – can be a big mistake. In the modern business, those at the top carry the ultimate responsibility when something goes wrong and they need to 14 12_14_BePrepared_Claims13.indd 14 22/11/2013 15:01 . STRESS TESTING Engender trust with a stress test Playing with hypothetical loss scenarios is an authentic way to measure how durable a company’s liability insurance is S OME FIRMS ARE ALREADY TAKING steps to stress-test their policies and see how they hold up under various loss scenarios – for example, to more closely understand their liabilities and how they differ across their territories. “Our objective is to use liability scenarios to assess how good our liability insurance is,” says Group CMI group risk and insurance manager Gaëtan Lefèvre. “To do this we developed several hypothetical loss scenarios linked to our engineering processes and maintenance of industrial equipment. One we used was an error in the design of a boiler, ï¬rst in Europe and then in the US, to see how thing differed. We also explored the impact of an accident owing to failure in maintenance of industrial equipment, and a ï¬re at a CMI warehouse.” The liability stress tests were attended by representatives from the insurance company, the underwriter and claims manager, insurance broker, account manager, a liability technical adviser from CMI and Lefèvre as risk and insurance manager. “The minutes of the meeting were written up by the insurer, and we had some good outcomes, including clariï¬cation of some policy clauses,” says Lefèvre. “We were also able to explore the underwriting of a new insurance programme linked to environmental liabilities. “More generally, this kind of exercise increases our insurers’ understanding of our operations and I hope that in the case of a ‘real’ claim there will be no surprises. “Step by step, we are building a trust relationship between our companies.” SR Guide to claims 15_17_Stress_Claims13.indd 15 INVOLVING BUSINESS CONTINUITY Major loss can have a huge impact on your business and it is important to make sure all possible resources within your company are focused on ï¬nding solutions to the challenges you will face. “When you have a big claim, you really have huge problems. This affects not just the site and the local area, it affects the whole company,” says independent consultant on insurance and risk management Guenter Droese, former managing director of Deutsche Bank AG and broker Deukona. “You need a crisis management plan. If you are not prepared because your company is too small – or that you think it is too small – then you need to know where you can get good advice in an emergency. “This contact might be linked to an insurer; some companies provide this. In other instances you have to go to a loss adjuster who can help you, and you know that all you are paying him will be covered by the policy.” If you have a business continuity facility, use it, advises Ferma president Julia Graham.

“There are different schools of thought about how the relationship between the claims process and the business continuity management and associated recovery process should operate. For me, they are inextricably linked, although the link should be forged much earlier in the management process than a er a claim. “It never ceases to surprise me how any recovery time objective can be forged by business continuity managers and business interruption insurance solutions designed by risk managers without these being simultaneous and fully engaged processes. “We talk a great deal about ‘enterprise-wide risk management’ – we should also talk about ‘enterprise-wide business continuity’.” » www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 15 22/11/2013 15:25 . Shutterstock EXPECT THE RIGHT ATTITUDE The right people, A the right advice Need to make a claim? Do your preparation for the claims team and never be afraid to ask the tricky questions 16 StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 15_17_Stress_Claims13.indd 16 S A RISK MANAGER, WHEN choosing an insurer you need to zero in on their ability to handle claims. They need to have the right people with the right knowledge, skills, experience, and attitude. Good insurers know this and communicate their advantage at every opportunity. “Our value is very much tied into the expertise of our claims handlers,” says AIG regional claims manager, liabilities, Europe, Andrew Walker. “We’ve always had a very strong reputation for the technical expertise of the people within our claims team. In particular those who deal with the high end, the severe end of most lines of business. “This has always been valued by our key brokers and big accounts – and anyone, really, who has been unfortunate enough to have to make a major claim.” Guide to claims 22/11/2013 15:25 . ASK THE RIGHT QUESTIONS Before you sign on the dotted line make sure you have properly interrogated both your policy and your insurer. Ask these questions: • • • • • • • • How much do you pay in claims every year? How many claims do you pay? What’s your process if you are going to deny a claim? Do you reserve your rights on every claim? Does your insurer have an in-house claims department? Does it have the expertise to deal with your claim? Because some of these risks can be very complex. Does it just refer everything to a lawyer? Will you be dealing with someone at the insurance company or someone at a law ï¬rm? A good insurer will also always be able to offer you good advice on making a claim. You shouldn’t be unsure about asking any questions. Andrew believes AIG’s strength in claims comes from its ability to bring a broader understanding of the law, regulation and the technical nature of the claims process. “We give the broker and the client comfort from an early stage that we have the knowledge to help them deal with a crisis. “This might even be at a stage before a claim has even been made – perhaps there has been an accident and a client is expecting claims. It can be in connection with a criminal issue when we are involved in their defence; anything that could be a reputation issue. “Having us behind them, able to offer them the right advice and guidance – I think that is a valuable thing, to be able to add to the insurance activity at that level.” Walker believes clients increasingly expect their insurers to act as a commentator on the changes in the regulatory environment in their countries around the world. “They look Guide to claims 15_17_Stress_Claims13.indd 17 to us as insurers to guide them through any regulatory or statutory changes that are about to happen, and give them comfort that we can protect them from, or take advantage of new rules in certain jurisdictions,” he says. “For example, in the UK the changes around the Ministry of Justice portal and referral fees being outlawed and non-recoverable.

The insured want to know that we have amended our rules and are well placed to take advantage of new timescales.” Claims control is more of a signiï¬cant issue than it used to be, both on large losses and on trends with smaller losses. “They want speed of payment, too,” says Walker. “That speaks to a certainty of coverage.

In the past it was tolerated for an insurance company to say that it needed time to come to a decision, but not any more. Claims conï¬dence and clarity is very important. We want to pay as much as we can, as soon as we can.” SR ‘In the past it was tolerated for an insurance company to say that they needed time to come to a decision, but not any more’ Andrew Walker AIG www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 17 22/11/2013 15:25 .

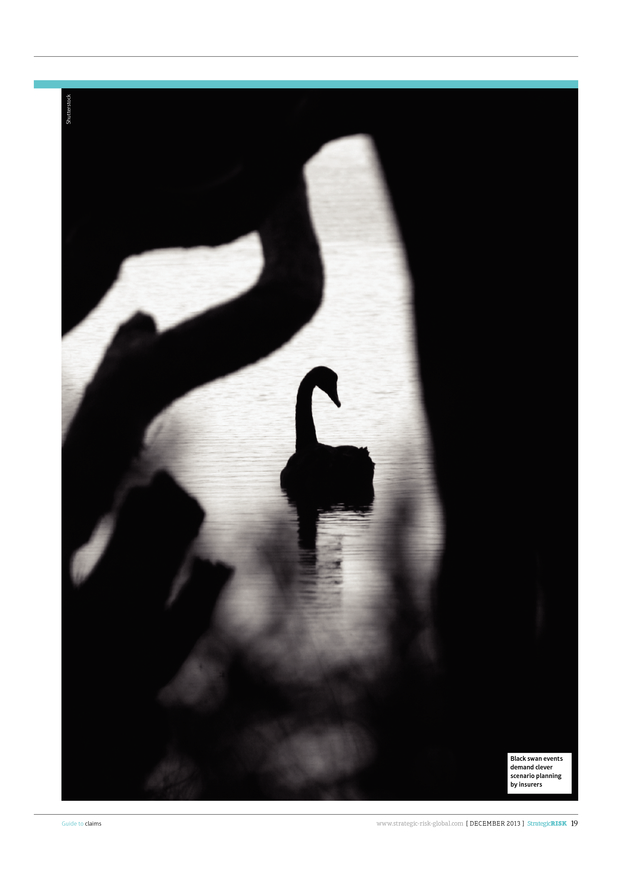

GET THE RIGHT EXPERTS Be prepared for disaster before the worst happens Your insurer may have the best experts in your ï¬eld, but knowing how to make the most of what’s on offer is also vital ‘Expertise mainly is expertise of people, not of computers and models. So you have to check the expertise of those people you talk to and who make decisions on behalf of the insurance company’ Hans-Jürgen Allerdissen DVS 18 M AKE NO MISTAKE, A MAJOR LOSS can be an emotional business for a company and you will need support from your insurer. “No one makes a claim for fun,” says Katoen Natie’s chief risk officer Carl Leeman. “As a company, it does take a lot of your time and energy, and all the while you have to carry on with your business and keep your clients happy.” For smaller and medium-sized ï¬rms, their survival may be at stake. As a risk manager, you will need to be conï¬dent that your claim will be paid, and that in the meantime, defence costs and legal liability will be covered, if necessary. If this is not provided the result can be distressing – small things like verbal communication and conï¬rmation of a claim can make a huge difference, but ultimately you need to know that your insurer has the right team in place and that it can cover all your territories. “Expertise mainly is expertise of people, not of computers and models. So you have to check the expertise of those people you talk to and who have to make decisions on behalf of the insurance company,” says Deutsche Verkehrs-Assekuranz -Vermittlungs managing director Hans-Jürgen Allerdissen. Risk managers looking for reassurance should be asking their insurers some tough questions.

You need to know who your experts will be. Who are your adjusters? Who are you going to use for salvage recovery? Who are your architects? Who are your lawyers? Who are your security advisers? StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 18_20_Experts_Claims13.indd 18 Who is going to hold your hand if you have a massive loss and how do you reach them? “Meeting with your insurer and going through a few ‘what if’ scenarios of major loss management, and saying ‘how would this work?’ is important,” says Ferma president Julia Graham. “If you are talking about major damage, ï¬re or flood, supply chain issues, failure of an insured IT system, breach of data or a malpractice event it’s essential to sit down with your insurer – and perhaps your broker – to talk through who will be doing what in the event of a loss. “They are your primary support team.

Ask ‘what role will each of us play?’ and how, insurer, would you like us to manage this process? I have experienced major loss claims and it was surprising to me, ï¬rst time round. You ï¬nd yourself asking obvious questions – things you should already know. This taught me a big lesson. You have to have everything in place and work closely with your business continuity people.

We don’t all deal with big claims every day of the week, but when you do, you need to know what to do.” Multi-jurisdictional aspects This is especially true in big multinationals and business with multi-jurisdictional aspects or complex supply chains, says Graham. “We saw this in the a ermath of the Thai floods and the Japanese tsunami,” she says. “You can be looking at complex and unexpected situations – some of which people might call ‘black swan’ events – which is why you have to be clever with your scenario planning to make sure you include all the possibilities and try to think the unthinkable. “This said, try to keep it simple – don’t over-engineer it, even for a major loss.” Risk managers need to make sure that their insurer understands all of the territories » Guide to claims 22/11/2013 15:20 . Shutterstock Black swan events demand clever scenario planning by insurers Guide to claims 18_20_Experts_Claims13.indd 19 www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 19 22/11/2013 15:20 . GET THE RIGHT EXPERTS » in which they operate – something that is becoming increasingly key in making purchasing decisions. “We have a lot of clients that have international business, so perhaps a German client will have business in France or Germany,” says AIG senior claims officer for Germany Olivier Netz. “The minimum that they expect is a consistency in the way that their claims are handled throughout the AIG world. It would be fair to say that this has not always been the case in the past. So our new approach is not just about realigning people; that would be too simple.

It’s about realigning our whole approach and creating consistency across all our operations. In the past a claims handler could have worked quite passively. They would get a claim, wait for reports, take a decision and write a letter explaining the decision to pay or not. One of the aims of our new model is to be more proactive. 'Now the claims handler reaches out to customers to get information early and create transparency about where a claim is residing and how it is processing.

Throughout the process we must be transparent and take the time to explain decisions verbally, if possible, not just in a letter. Obviously, letters will be written, but a central element of our new process is to be more transparent.” For the risk manager, it is not enough to satisfy yourself that your insurer has the right experts – knowing how to take advantage of what’s on offer is also vital. “Most insurers have a lot of experience in their organisation – the question is how to make best use of it and how to leverage it for creating mutual value,” says Syngenta International AG head group risk manager Olivier Balmat. “In my view the underwriting process has to become much more integrative by pulling multiple resources to the table. 20 “As interconnectivity is increasing, we should engage by associating claims specialists, engineers and even other indirectly concerned functions in our regular business processes and transactions.

The expertise is not only coming from individuals; expertise is also built in by teams. A multidisciplinary approach would also foster a climate of problem recognition, preventive problemsolving and ultimately innovation.” Spend time discussing your risks with your insurer. “[That is] the kind of claims or loss you face, or can face, the prevention and protection policy in place, whether there is room for improvement,” says Dalkia risk management director François Beaume. Regular meetings The risk manager should ask the insurer to describe its knowledge of the client’s business and how it has structured its reinsurance – this could have an impact on price and conditions, or could lead an insurer to refuse to cover some activities – incineration or transport and distribution, for instance.” This should be discussed at regular meetings between client and the insurer, who needs to be proactive in approach: “To climb on the maturity scale, to better understand the business and the business needs, the insurer should seek advice from external experts who know the business,” says EADS head of risk Christoph Schwager.

“This provides them with a third-party view on what’s really going on, where the big obstacles are and how to price them.” The insured may want to appoint some of its own experts – particularly when it comes to underwriters. “Considering the experience and the know-how of our team, we’ve chosen to work with our own loss adjusters dealing with the StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 18_20_Experts_Claims13.indd 20 ASK THE EXPERTS Make sure you ask the right questions, says Julia Graham: • Do you understand what the policy constraints might be? Do you know how your loss adjusters might deal with regulatory issues – for example, working cross-border in the US? It can be quite a challenge to gather a cross-state team – do you understand this? • And wherever you can, when you are going to pre-appoint people, you need service-level agreements. Say if you are in a situation where there is a wide area affected by an event, you need agreements that your people will come and deal with you as a priority. This is not always possible, but where you can, it’s advisable. • Does the reach of your partners match yours? • Do they really understand your business? • Do partners in turn sub-contract services? If they do, is the quality of the subcontractor up to the standard you expect? insurance company loss adjusters,” says France Telecom group and corporate insurance director Johnny Merlot. “These experts work closely with our claims department to optimise the assessment of damages and losses and to identify the costs, expenses related to the damages.

These free debate and cross-examination to give us the opportunity to obtain a more objective evaluation and therea er a fair indemniï¬cation.” SR Guide to claims 22/11/2013 15:20 . A SUSTAINABLE RELATIONSHIP Look before you leap into partnership Trust and conï¬dence build up over time in any relationship, but to enjoy a rosy future risk managers must forge personal links with an insurer W HICHEVER INSURER YOU DECIDE to partner with, think hard about how to nurture a sustainable relationship that can thrive even when exposed to the stresses and pressure of making a claim on a major loss. “This is critical,” says Ferma president Julia Graham. “It’s not only about buying a product for the cheapest price. While you have to consider price, any risk ï¬nancing decision is about designing a solution for how you are going to protect the assets of your business and how you are going to use the capital of that business to risk ï¬nance that protection.” Graham says this is one of those issues where people in risk management can fall foul of the procurement department, which is o en focused by different drivers. “Some of the drivers are shared, but some are different,” she says. “If you want to understand properly how each of you is going to respond to a claim you can’t do that if you have a different insurer or broker on too frequent a basis.

Trust and conï¬dence build up over time, not overnight.” But it’s also crucial that risk managers don’t try to ignore or bypass procurement. “Risk managers have an opportunity to take an initiative and act as educators and advisers of procurement,” says Graham. They don’t necessarily understand insurance, just as you might not fully understand procurement. It’s a question of respecting each other’s professional expertise and business position. “The relationship between insurers and risk management needs to be a two-way Guide to claims 21_22_Sustainable_Claims13.indd 21 ‘It doesn’t matter if you are making cars or if you are a law ï¬rm, you need insurers and underwriters who understand what you do’ IS YOUR INSURER PREPARED? • Does your insurer have what it takes to get you through a claims process? • Does your insurer have the right IT systems? Can it handle claims and claims data in a timely and accurate manner? And what is it planning for the future when it comes to IT? Is it investing? What are its goals? • Are your insurer’s IT systems compatible with your internal systems? • How open are your insurer’s communication channels? Are contact details clear and updated? Can you speak to key contacts quickly and easily? • Does your insurer have offices and staff in all your key locations? Are you happy that there are representatives available on the ground where you need them? Julia Graham Ferma street.

There has to be give and take. I think insurers have done a great deal to provide value-added services that can help you in the event of a claim and it is up to risk managers to ï¬nd out what they are and pick an insurer that offers services that match their need,” adds Graham. “You’ve got to mirror their claims ability to your own needs; it’s not just about money, it’s about ï¬t. “It doesn’t matter if you are making cars or if you are a law ï¬rm, you need insurers and underwriters who understand what you do. “It works both ways.

I think someone who has been an underwriter or involved in claims makes a great risk manager. They understand the process.” SR www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 21 22/11/2013 15:19 . OPERATE GLOBALLY, THINK LOCALLY Avoiding cross-border controversies Law and claims working practices around the world can vary greatly, so it is essential to ï¬nd a strategy that offers consistent service at home and abroad ‘In a lot of countries the insured has no contact with his insurer, underwriter and claims people. You have to go through a broker’ Guenter Droese independent risk management consultant 22 I N AN INCREASINGLY INTERCONNECTED and homogenous world in which businesses tend to emphasise their similarities, it’s easy to forget that if you scratch the surface huge differences remain between countries – particularly when it comes to the law and the obligations placed on companies by local authorities. As a result, consistency of support from your insurer is crucial when making a claim. “We really excel at providing international coverage,” says AIG’s senior claims officer for Germany, Austria and Switzerland Oliver Netz. “We were one of the ï¬rst to be working in an international context, not just expanding outwards but growing together out of operations we have had in various countries for many years. We spent years building relationships.

We mingle and mix. Silo thinking is common in this business, and while local knowledge and expert knowledge is vital, there are many cases where customers can beneï¬t a great deal from our ability to operate in breadth as well as depth.” Providing this level of service can be a challenge for insurers. “We had a major issue with a client in France who had a subsidiary in Belgium and in the UK,” says AIG head of claims in France Evelyne Boyer. “There was some discussion about the claims handling, and the risk manager was not happy with the way things were being handled in the UK and Belgium so he came to me to solve the issue.

I was able to do this because we can take a global view. I was in each meeting so I could demonstrate the local contact. From the feedback we get, the insured like to see that StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 21_22_Sustainable_Claims13.indd 22 we are a team tuned to their service, not divided into silos.

This requires close work internally, but we are doing this well. “I am in charge of three major accounts and when we can say that I am the one point of contact for any issue around the world they are really impressed. The point of contact is dedicated and this is really an added value.” Varied working practices But the insured needs to be aware that claims working practices around the world can vary greatly – and risk managers need to adjust their strategies accordingly. “In a lot of countries the insured has no contact with his insurer, underwriter and claims people. You have to go through a broker.

In some places they use loss adjusters 100% of the time, while in other places they use them as a consultant, a specialist to work over the ï¬gures on damage or business interruption,” says independent insurance and risk management consultant Guenter Droese, former managing director of Deutsche Bank AG and Deukona, its in-house broker. “When you look into policy wordings, things can be different. A business interruption policy in Canada is different from one in Europe. Based on the wordings you may ï¬nd that you have a policy that means losses at a single factory will not be settled as long as the company has the opportunity to move part of the production to another country.

They see other countries as a substitute. This can have a huge impact and make claims difficult. The insured must have the best advice on where to get the best wording.” SR Guide to claims 22/11/2013 15:19 .

INFRASTRUCTURE A clear chain of command means joined-up thinking In any insurance strategy there should be a reporting structure of experts in all disciplines helping the risk manager to maintain a coherent overview Guide to claims 23_25_Infrastructure_Claims13.indd 23 P RE-LOSS PREPARATION DOESN’T begin and end with an interrogation of your policy and your insurer’s expertise. You need to know what your own operations are doing during a claim – and how they will work together to get it all done. As with all aspects of business processes, successful claims management has to be backed up by a clear set of systems and management tools that allow everyone involved in what is always a complicated operation to contribute to the ï¬nal goal in a clear and consistent manner. “I think it’s helpful in a stressful situation that not only do you know who all the players are, but that you have flow diagrams that show how things work – who is managing what, when they are doing whatever they’re doing,” says Ferma president Julia Graham. At a minimum, risk managers should have a tool that allows them to keep track of all that is insured, of the associated risks and of all incidents. “Proper documentation is key,” says EADS chief risk officer Christoph Schwager. “In addition, there should be a reporting structure to allow the risk manager to keep a view over the risk situation.” Furthermore, they should know their contacts in the businesses with whom they regularly consult about their risk situation. “Two things I would stress: the organisation before a claim and the situation of the insurers,” says Carl Leeman who, in addition to his chief risk officer role at Katoen Natie, is president of the International Federation of Risk and Insurance Management Association (Ifrima) and a Ferma board member.

“It is key to have agreements with your insurers so that you know exactly which surveyors to contact in which countries. You need phone numbers because those things will not wait. Plus, working on a global scale means you have to make allowances for different time zones. “Your local people on the ground also need this information.

Your surveyor also needs to understand your type of business. He needs to understand your activities, where you are operating and what you are doing.” Staffing is also critical and you need to have the right people on your time. “In today’s business environment it’s all about the right mix,” says Daimler managing director of corporate insurance Dr Ingo Telschow. “You need to have an appropriate combination of engineers, lawyers, insurance experts and IT professionals.” Collecting risk data The latter are of special importance when it comes to collecting risk data and developing appropriate risk management systems, including geographical data. In terms of organisational structure, it makes sense to focus on the main insurance lines – “property/casualty, and special lines – as well as claims management”.

Small things can make a huge difference when dealing with a crisis – such as naming a claims adjusting company in your contract. “Having a good risk culture is important,” says Leeman. “Every employee needs to be aware of risk and be prepared to have an open dialogue in the case of a claim. You want to avoid surprises.

In our case, insurers attend internal meetings – we are very open. Many SMEs have a different view and I know that can be hard for insurers. While the larger companies are mainly concerned with the larger risks, some of the smaller companies take the view that, because they are paying an amount each year in premiums, they need to get that amount back in claims.” Time is money and you need quick responses, says former Ferma president Marie Gemma Dequae.

“In terms of infrastructure, within my department I initially had the sole www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK » 23 22/11/2013 15:24 . Shutterstock INFRASTRUCTURE 24 StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 23_25_Infrastructure_Claims13.indd 24 Guide to claims 22/11/2013 15:24 . » responsibility for insurance, but as we evolved we had an engineer who was also able to be involved from a technical perspective,” she says. “You also need excellent administrators. You must know who you can contact. You may not need to know everyone on the insurance side but, internally, you need to know your legal contact, for example. “If it is a product liability claim you need to know who to ask for advice in the product quality department. You need to be in close contact with the ï¬nancial controller, who can advise on costs.

It’s also important that you have a good reporting process. Every two months I have a management meeting and that is on the agenda to make sure anything important is discussed. Every quarter we look at the global situation.

That is important for the learning process and for preventing these claims happening in future,” she adds. Time to report a loss Every employee needs to know and understand the correct timeframes for reporting a loss, however small, and contact the claims team in a timely fashion. “The problem is we can receive the claims information too late,” says president of the Belgium risk managers’ association Belrim, Gaëtan Lefèvre. “Make sure you can react quickly. Be open – and be correct.” “With a large claim you need to know the local laws,” says Leeman.

“It can be crucial to have assistance from people who are really on top of this in the location where your claim occurs. You also must understand disclosure. In some countries you have to disclose huge amounts of information and in some parts of the world there is no point in holding documents for ï¬ve years when local law only obliges you to keep ï¬les for two years; in this world old info could be used against you.” SR Guide to claims 23_25_Infrastructure_Claims13.indd 25 INFRASTRUCTURE CHECKLIST According to Dalkia head of risk management François Beaume, risk managers need to make sure they have: • a global written enterprise risk management (ERM) policy, describing what an ERM means and how every employee of the company relates to this policy in day-to-day activities; • a transverse network at HQ level, which is able to work with, and rely on every other department with HQ operations – including legal and technical; • a global network made up from a team of local colleagues or risk managers who are able to deploy the risk management policy as closely as possible to operations in the ï¬eld, and also use this network to record and feedback all data relevant to risk management and claims handling; • a broker (if you have one) who is a strong supporter of this policy; • a risk management information system that is used to embed everyone in your risk management network – including on the broker side, globally and locally; • international programmes with reliable insurers; • the right processes in place, including claims management processes, insured values update processes, new project or tender risk analysis processes; and • a risk manager making sure that any collaborative projects, such as global risk mapping, are all linked in to the company’s strategic goals. ‘In today’s business environment it’s all about the right mix. You need to have an appropriate combination of engineers, lawyers, insurance experts and IT professionals’ Dr Ingo Telschow Daimler www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 25 22/11/2013 15:24 .

DATA Knowledge is power – guard it well Handling your business data with skill will transform raw facts into precious intelligence 26 G ATHERING GREAT DATA AND knowing how to leverage that data in relations with your insurer is an important skill for the modern risk manager. “Good data management is the key to success,” says Drägerwerk AG head of insurance Mathieas Kohl. “You always need to identify the real issue and the impact within your value chain as soon as possible.” Gathered skilfully, and curated with care, data is a business asset every bit as valuable as property or human resources. It has both a potential and a realised value that can be quantiï¬ed, accounted for and leveraged to create maximum value. It can be used to guide and prioritise insurance purchasing decisions and maximise the value of any investment in risk management infrastructure. Data gathering needs to be a live process, active before, a er and throughout a claim. Getting this right starts with your own internal procedures and here time and accuracy are everything, says Kohl. For example, if someone within your ï¬rm waits a week or two to notify you of a claim, it can make it much harder to identify what kind of impact and management attention the claim might require. “Being able to understand how information is linked, where it comes from, how it relates to company targets, is a key milestone in increasing company performance,” agrees EADS chief risk officer Christoph Schwager. “Good and intelligent data management enables the risk manager to perform a better risk management process. To keep ahead of the others it is necessary to protect the data from cyber attacks. However, the quality of data should always be considered because, as you know – garbage in, garbage out.

A lot of effort should be given to the data quality.” StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 26_27_Data_Claims13.indd 26 The importance of accuracy and good data gathering from all sources was emphasised by recent research by MSM Risk Management, which found that 84% of risk professionals were losing time and money by re-keying risk data and sourcing it from multiple locations and people. In the research paper Managing Insurable Risk Data in 2013, the ï¬rm canvassed the views of 100 underwriters, risk managers and risk engineers and questioned them about how insurable data was managed. It says: “A shockingly high percentage of professionals are experiencing problems with sharing insurable risk information.

In this day and age where everything is at your ï¬ngertips, it is astounding to ï¬nd that in such an important area of business, organisations are making decisions based on only partial facts.” Environmental claims But it is not only data quality that is an issue for risk managers; having access to a full range of data is becoming increasingly important. “What is very useful to a risk manager is knowing how o en claims like yours have occurred in the past,” says ArcelorMittal corporate asset risk manager Adrian Clements, whose business is steel and mining. “Insurance companies have this data, but they hoard it like crazy because they feel it gives them a competitive advantage.

Most companies don’t have access to this data and this can be very frustrating. Clements believes this is particularly relevant when it comes to environmental claims, where clarity about what constitutes a claim is sometimes lacking. “It would be really useful if the guys from the insurance company could give an indication of how big they pay. A lot of the time if you pollute the air, that’s a ï¬ne.

It’s not an insurance claim. Guide to claims 22/11/2013 15:36 . Shutterstock But with enterprise risk management you need to quantify your environmental risk, and to do this you need frequency and severity data. Both of these are within the data sets of the insurers, but they don’t always tell us. As a result it can be hard for companies to understand their environmental risk. If they have environmental risk on their risk register, it is a very approximate guess. We are going to the insurance companies asking for help with this and they are all saying ‘no’.” But some insurers are starting to meet these demands and offer a more open service. “Risk managers expect more from the service than they did even two years ago,” says AIG regional claims manager, liabilities, Europe, Andrew Walker.

“They expect access to clean and reliable data, and they expect that to be much more current than they were able to tolerate in the past. Part of our attraction as a global insurer is that we can take data from our offices across the world and put that together into one management Guide to claims 26_27_Data_Claims13.indd 27 tool and give the risk manager the opportunity to see in one report the claims and loss experience occurring across the world.” This kind of service is becoming increasingly important. “Of course, it means that you have to have managers in place in all your locations around the world and who can pass on to their team the importance of clean data entry on the desktop,” says Walker.

“They need to know the importance of this. It sounds simple and metronomic, but it is important.” But, while data is vital, it’s also important to be aware of its limitations. Even the best data can only extrapolate from the past – and there are risks from drawing too many conclusions from aggregated studies. “When you look at the data you get from brokers, when you look at the breakdown of what is happening, remember, this is just data,” says European Captive Insurance and Reinsurance Owners Association chairman Guenter Droese.

“In the ï¬nal analysis, every company is different.” SR DATA CHECKLIST • • • • • Is your data safe? Find out if your insurer has taken the proper steps to protect your privacy and comply with all relevant data protection legislation – in every territory. Is it accurate? What is your insurer doing to make sure that data entry meets the required standard? Does your insurer proactively look for evidence of inaccuracy or fraud through pattern recognition or risk analysis? What are your insurer’s policies on data retention and data sharing? Is it complying with all relevant legislation across your operations? Can you get access to the data you need? How is your data protected against a major loss at your insurer? www.strategic-risk-global.com [ DECEMBER 2013 ] StrategicRISK 27 22/11/2013 15:36 . MAKING A CLAIM Claims handling makes or breaks a reputation Communication and simplicity in the claims process and maintaining an open mind are key ingredients to keeping everybody happy COMMUNICATING A CLAIM There are four key stages to communicating a claim to your insurer, according to France Telecom group and insurance director Johnny Merlot. 1. Properly explain to your insurer the situation immediately a damage or loss occurs. 2. Ensure that appropriate decisions and choices will be made. For example, ask: why should we activate a business continuity plan right now? 3.

Be fair and honest in your communication, supply the right information and hold regular meetings to explain how the situation has developed since the loss occurred. 4. Set up a task force within your organisation, and choose a leader to be the point of contact for communication with your insurers. 28 C LAIMS HANDLING IS TODAY PART OF reputational risk,” says the International Federation of Risk and Insurance Management Association president Carl Leeman. “Good claims handling can make your reputation, while bad claims handling can ruin your reputation.” To succeed, try to design an internal claims process that is simple and robust. “This process should allow you to catch the relevant information as close as possible to where the loss occurred and as soon as possible a er the occurrence,” says French energy service company Dalkia’s head of risk management François Beaume.

“The quality of that information is key to give everyone the best orientation in terms of loss management.” When going through a claims process you have to be quick, efficient and consistent. “With any loss you have to be honest,” says ArcelorMittal general manager of asset risk management Adrian Clements. “You have to provide the relevant information, the expertise, to help the loss adjuster and the claims handler. “Always be open and discuss – and don’t ï¬ght for pennies. If the claims people think I am going to ï¬ght for every penny, then they don’t want to come to me next year.

It’s swings and roundabouts. A claim is never black and white. Bear this in mind and people will come StrategicRISK [ DECEMBER 2013 ] www.strategic-risk-global.com 28_30_Making_Claims13.indd 28 into meetings with open minds, ready to talk. Fight on every point and your insurer will come in ready for a ï¬ght, and that is never a good start, especially if you are talking about a $100m claim.

In the end it doesn’t matter if you get paid $99m or $101m. What the hell.” It’s also worth remembering that it’s not only the insurer and the insurance manager who needs to be happy. “The manager of the plant needs to be happy as well,” says Clements.

“Because, at the end of the day it’s his bottom line. He needs to get his proï¬t/ loss accounts on track and he doesn’t want to feel like the corporate guy didn’t ï¬ght for him. There are three parties involved.” Everyone involved needs to have appropriate training. “Everyone should know, all the time, where they are in the process, which milestone comes next and when to do what in the interest of the company,” says EADS chief risk officer Christoph Schwager.

“This starts with the ability to rightly identify the root causes of the risks. Only then are they in a position to assess properly whether the insurance coverage is appropriate. Should a risk then occur, by knowing the root cause it is much easier for the risk manager to deal with the insurance and manage the claim.” It’s also worth considering a dedicated leader team across all insurance lines.

SR Guide to claims 22/11/2013 15:37 . BE IN CONTROL OF THE PROCESS Overall view is vital to managing an operation To ensure a smooth operation you need a thorough understanding of every part of your supply chain and its processes from start to ï¬nish Guide to claims 28_30_Making_Claims13.indd 29 I T GOES WITHOUT SAYING THAT IN A major loss scenario you need to know what you are doing – and good operations management – the ability to effectively manage the processes from initiation to conclusion – is critical. “If you fail in operational management you never will be in the driving seat,” says DVS chairman Hans-Jürgen Allerdissen. According to EADS chief risk officer Christoph Schwager: “Without being able to properly operationally manage the business process, a company inevitably fails. For example, if you manage the production process and forget one important control point in this process, the business continuity control, in the case of a ï¬re, you are at best dependent on luck.” French energy service company Dalkia’s head of risk management François Beaume agrees, saying that risk managers should see their operations management as a key component in the enterprise risk management process, as it has an impact on understanding the risk itself. “Good operations management will reinforce the position of the company towards its insurers and by lowering its total cost of risk increase its performance,” says Beaume. Successful operations management is rooted in an in-depth knowledge of your ï¬rm and all its activities – and risk management needs to have both a broad and detailed understanding of everything its employers are doing.